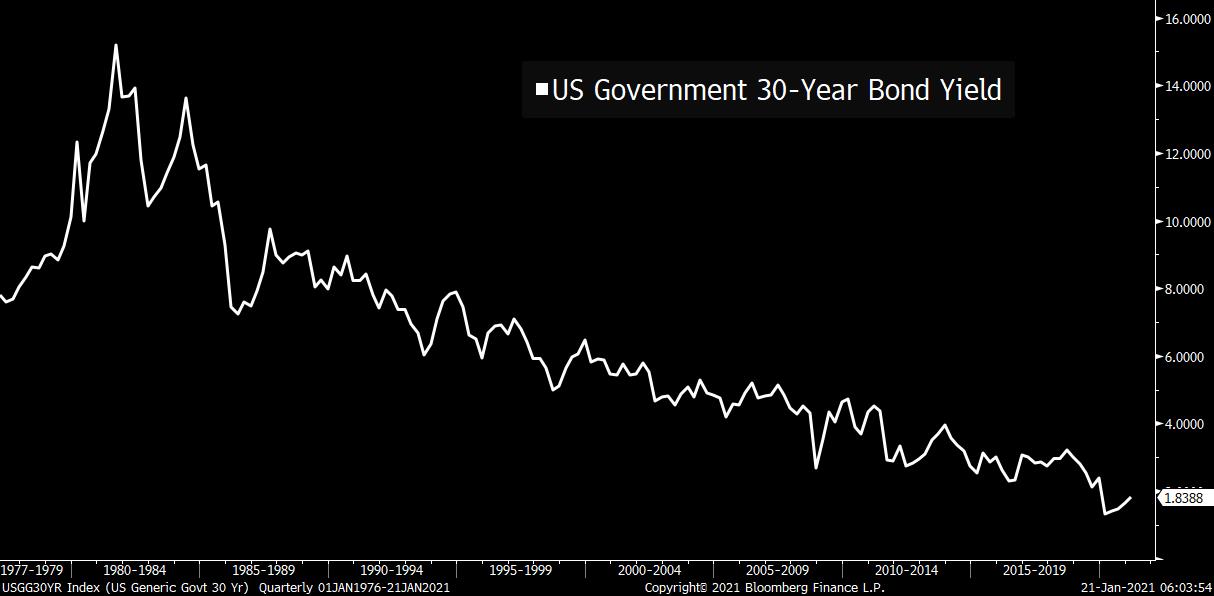

| Biden's new pandemic approach, claims data due, and ECB decision day. Busy start President Joe Biden began unwinding some of the previous administration's policies almost immediately after his inauguration yesterday. Today he will start to address the pandemic with orders to overhaul and unify the country's response to the outbreak. The market reaction to the change in administration has been positive, with the S&P 500 Index hitting a new record. Claims The pandemic that has seen more than 400,000 American deaths means that the Biden administration will only have the briefest of honeymoon periods. There will be another check on the damage that is being done to the economy at 8:30 a.m. Eastern Time this morning when the latest jobless claims data is published. The number of people signing on for benefits is expected to remain elevated after last week's surprising jump to close to 1 million. Continuing claims may creep higher to 5.3 million. Decision day The European Central Bank is not expected to announce any changes to its ultra-loose polices when the latest decision is announced at 7:45 a.m. President Christine Lagarde will face questions on the bank's response to the pandemic at the press conference at 8:30 a.m., as a raft of new measures kick in to curb the spread of the virus. German Chancellor Angela Merkel will hold a press conference later with the death toll passing 50,000. Already today the central banks of Japan, Norway and Turkey held rates unchanged. Markets rise Global equities continue to move in one direction today, with the MSCI World Index touching an intraday high earlier. Overnight the MSCI Asia Pacific Index added 0.8% while Japan's Topix index closed 0.6% higher. In Europe, the Stoxx 600 Index had gained 0.5% by 5:50 a.m. as investors waited for the latest ECB decision. S&P 500 futures pointed to a small rise at the open, the 10-year Treasury yield was at 1.089%, oil slipped and gold was broadly unchanged. Coming up...U.S. housing starts data for December is published is 8:30 a.m., with the latest Philadelphia Fed Business Outlook also at that time. The tech sector, which got a lift from Netflix Inc.'s earnings, will get another test later today when Intel Corp. and International Business Machines Corp. report earnings. PPG Industries Inc., Baker Hughes Co. and Northern Trust Corp. are among the many other companies announcing results. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningAt her confirmation hearing earlier this week, Treasury Secretary nominee Janet Yellen was asked whether the government should consider issuing ultra-long dated bonds, perhaps going out to 50 years. This idea pops up every once in awhile, because people have this intuition that the government should take advantage of low rates by locking them in for the long term. It sounds great. You borrow tons of money that you pay back over 50 years, and spend it all today on new roads and broadband and healthcare and stuff like that.

The problem is that once again, this logic rests on the premise that the government is like a money-constrained household. Households, of course, are in fact doing exactly this, refinancing their mortgages at low rates in order to reduce monthly payments. But the government, as the issuer of the U.S. dollar, doesn't face the same consideration or have the same priorities. Why would the government need to borrow and build up a huge pile of cheap cash now, when it can literally create cash at the snap of a finger?  If anything, you could make the argument that issuing more long-dated debt is not only unnecessary, but would be bad for the economy. After all, one of the ways QE supposedly works is that by purchasing Treasuries with reserves, the Fed is taking duration out of the market. Long-dated Treasuries would be doing the exact opposite, adding duration to the market, working cross-purposes to QE.

It's conceivable that there are some reasons why going longer makes sense. Maybe they would have some liquidity benefit, or perhaps there are some types of institutional buyers of government debt (like pension funds or insurance companies) for whom these instruments would be useful for hedging purposes or something like that. But if you're thinking in terms of spending and stimulus, there's no need. There's only one constraint that matters when it comes to spending more on broadband and healthcare and new roads, and that's whether a bill can get 51 votes in the Senate. Joe Weisenthal is an editor at Bloomberg. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment