| This is the time of year when investors (and people who write about investing, like me) have to pretend to see the future. We can sometimes appear to be in control of our fate, but as 2020 reminded us, we aren't. Anybody who correctly predicted the current level of stock and bond markets 12 months ago did so by accident and blind luck; the pandemic, possibly not known even in China in mid-November last year, changed everything. There is also the risk that something could happen in the last few weeks of the year. My favorite in this genre is The Economist's "The World in 1990," published after the Berlin Wall came down, which rated the chance of reform for the heavily embedded communist regime in Romania at -10 out of 10. In the event, Nicolae Ceaucescu, the dictator, had been put against a wall and shot before 1990 had even started. Over the next six weeks, there will be a row over whether to devote any more taxpayer funds to coronavirus aid, and also over the Treasury department's announcement that it expects most of the Federal Reserve's emergency programs to end on Dec. 31 — which provoked an immediate and unusual public protest from the Fed. There could be quite a "cliff" at the year's end, even if nobody is in quite as much danger as Ceaucescu. To be clear how much this matters, the money the Treasury made available for use as a backstop, and which it now wants back, propped up a range of sectors. Some, notably municipal governments and small businesses, are sure to come under renewed pressure before the year is out, and that support could prove useful. Some immediate speculation centered on the possibility that the Fed is more likely to expand its balance sheet earlier now, to cushion the damage. Beyond that, the cooperation between fiscal and monetary authorities during the crisis in March made a real difference. This comment comes from Jeroen Blokland of Robeco: Only a few times in the last century have we experienced such strong cooperation between fiscal and monetary authorities. This is the main reason why financial markets recovered so strongly after the fastest downturn in history back in March.

It's not a great idea to end this cooperation just as the pandemic is doing its worst again. Add the non-renewal of benefits at year's end and a transition to a new U.S. president with little political capital, and January looks like a point of high vulnerability. So what happens in the next six weeks could crucially change the outlook for the 52 that follow. Even if all goes well, there is reason for humility. To quote Steven Wieting, CIO of Citigroup Private Bank: We would assume many setbacks in confidence over the coming year. COVID itself presents an immediate economic restraint, albeit less damaging than the first shock. Certain COVID cyclical industry groups within energy and real [estate] were under downward secular pressure before the pandemic.

Much depends on how quickly the pandemic ends, and how politicians manage the trade-offs, as Blokland says: The Covid-19 outbreak is confronting policymakers with a 'trilemma': finding an acceptable trade-off between public health, economy and personal freedom. It is precisely this trade-off and the easing thereof that will shape the economic, market and social circumstances in 2021. …. much is dependent on the timeliness and effectiveness of a Covid-19 vaccine, and the extent to which we 'return' to a kind of 'New Normal'.

There is however a fairly straightforward roadmap that politicians will want to follow, and the good news over the last 10 days from scientists developing a vaccine makes that a little clearer. Don Rissmiller of Strategas in Washington laid out the base case as follows: The pathway forward likely involves:

• Work > Fun ("smart lockdowns")

• Goods > Services (China helps globally)

• Contact tracing > Privacy (Tech helps)

• Sustainable, safe behavior (masks, temperature taking) > not safe

• Rich > Poor

• Debt > Austerity (the solution to the previous item)

• Eventual vaccine/therapeutic/testing endgame

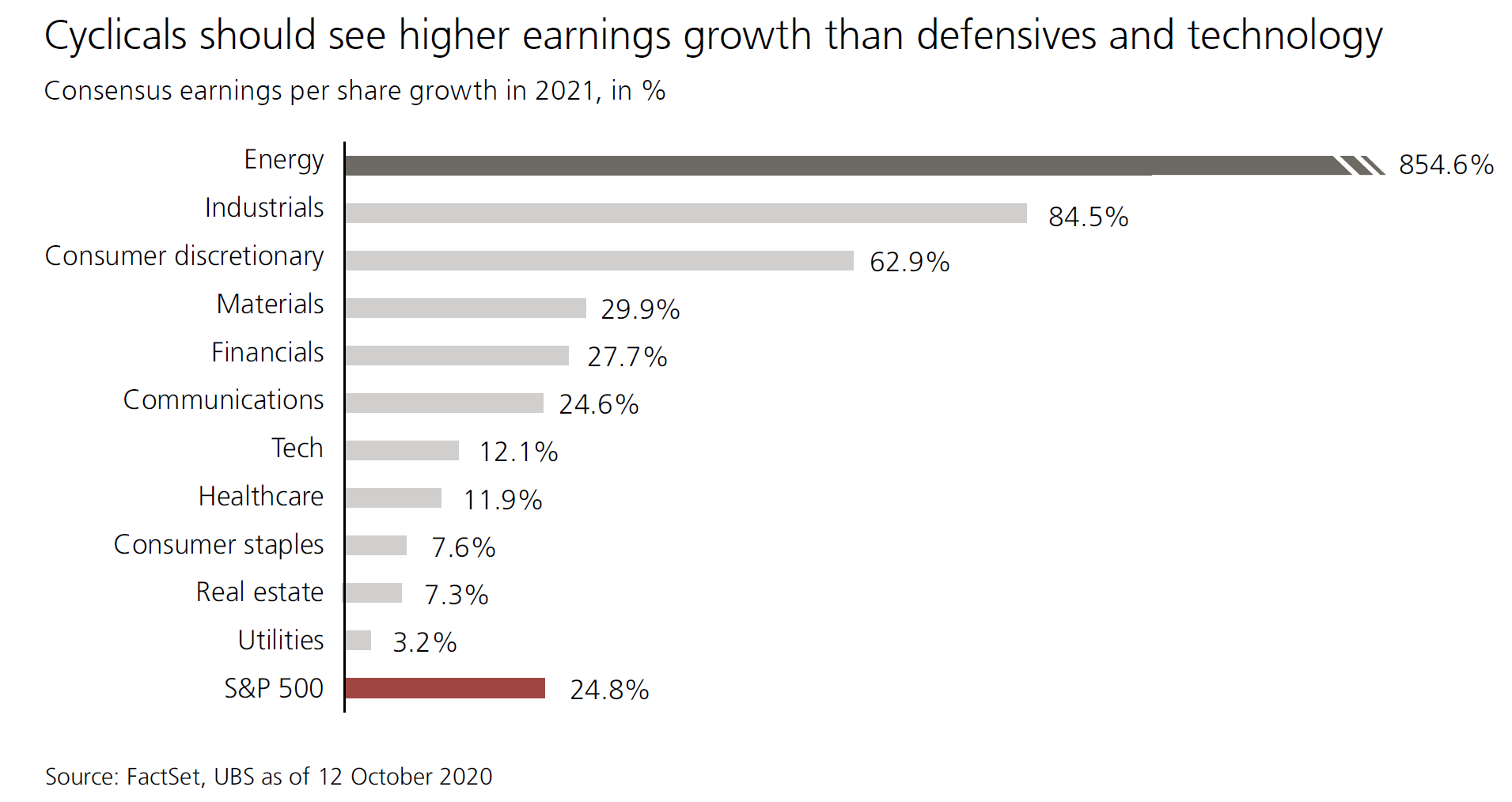

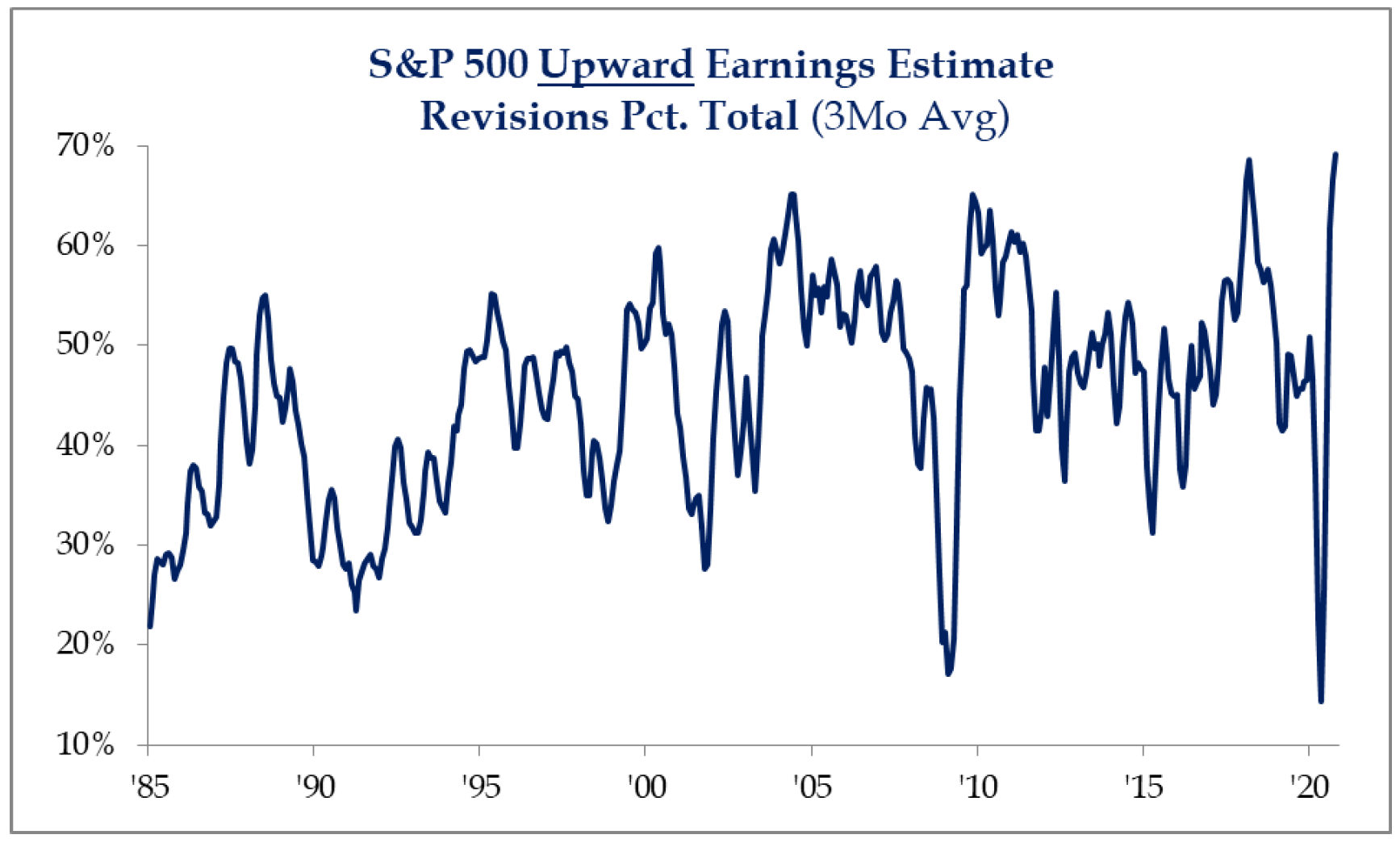

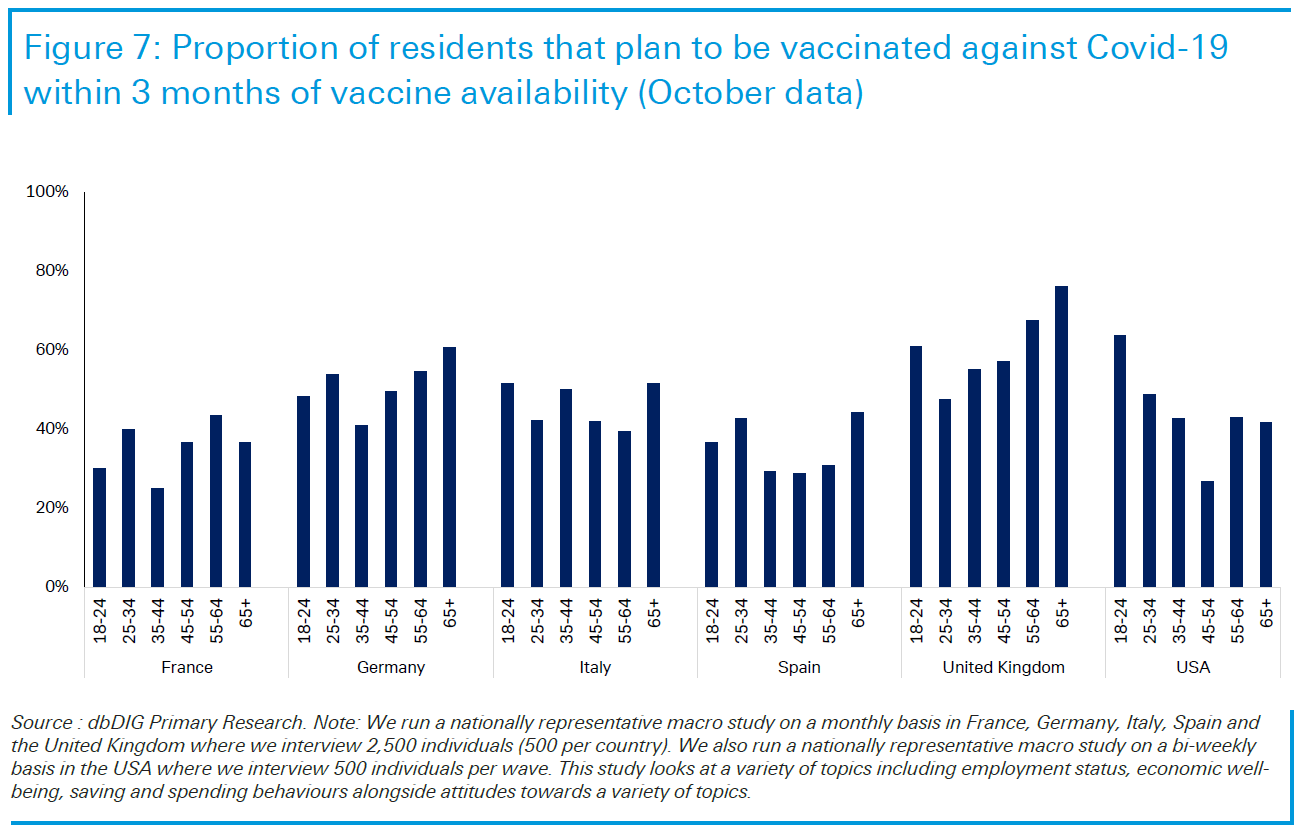

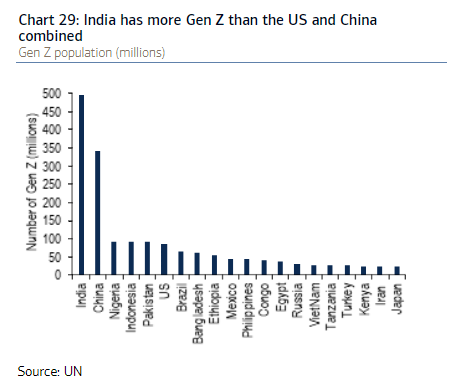

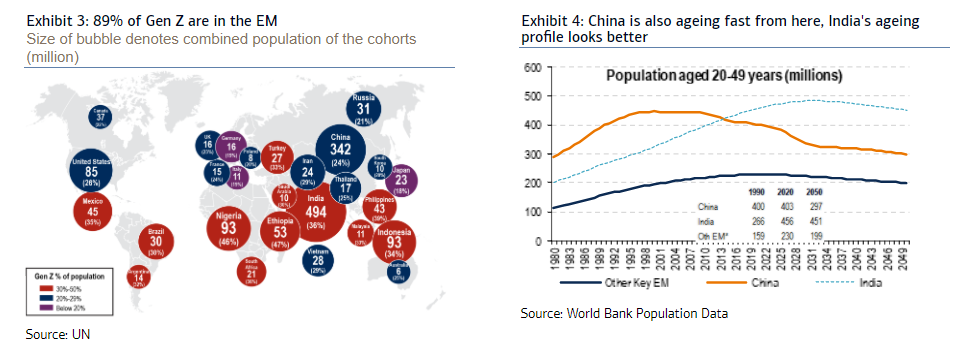

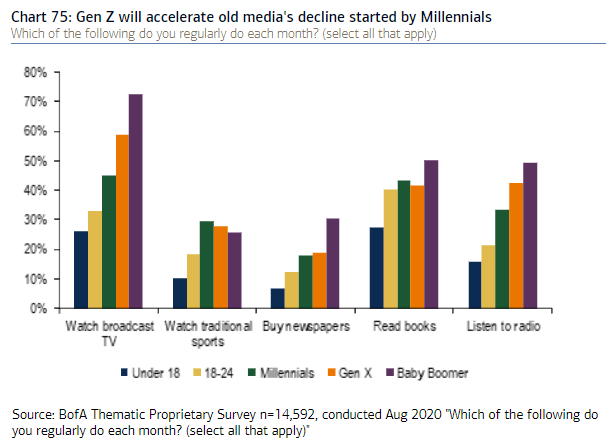

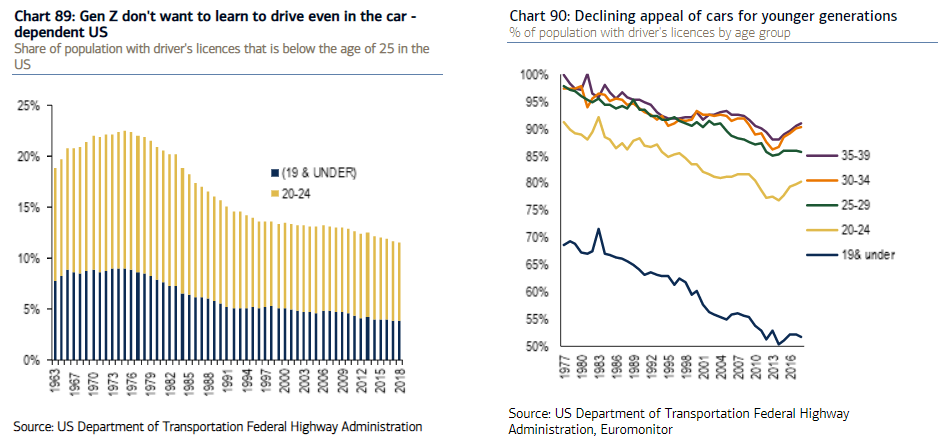

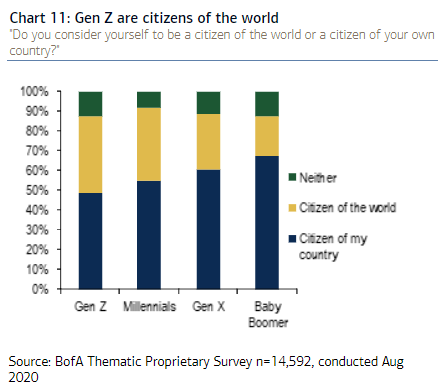

The most difficult questions are whether a jaded and angry populace (particularly in the U.S.) will go along with "smart" lockdowns and sustainable, safe behavior, and whether austerity really can be avoided (again, particularly in the U.S., where the Republicans are very likely to control the Senate). And much still rests on the timing of vaccines. If this has played out by the end of the second quarter, then the outlook for life, the economy, and asset values looks much better. How to deal with all this uncertainty? What slightly alarms me is that almost everyone seems to be arguing in the same direction. And, to be clear, I tend to agree with them. It's always dangerous when a consensus becomes too strong. That said, it is almost universal to propose diversifying out of the U.S., particularly the FANGs, and into global stocks, particularly cyclicals and emerging markets. This is coupled to the almost universal belief in a weaker dollar. Within the U.S., the popular recommendation is to rotate out of large-caps and consumer staples. The following chart of global earnings expectations for next year, produced by Mark Haefele at UBS Group AG, shows why people think this is a good idea:  There need to be wide uncertainty bounds around all of these estimates, however. Earnings forecast for the S&P 500 suffered their sharpest three-month average decline earlier this year. At present, revisions are running at their most positive in records going back to 1985, as shown by this chart from Strategas. Swings like this are only to be expected. But it wouldn't be difficult to shock them in a different direction again:  In fixed income, the consensus is that while 2021 will see a return to cyclical growth, inflation won't reappear. The fact that 10-year Treasury yields failed to go back above 1% in the last 10 days despite the vaccine news suggests strong confidence that inflation isn't an immediate concern. For 2021, that implies a "search for yield," taking higher risks (such as in emerging markets dollar-denominated debt or high-yield corporate debt) in return for eking out a little more income. This call also reflects a consensus that a solvency crisis has been averted. As for commodities, they also are enjoying a recovery, aided by China, without as yet causing inflation to rise. What could possibly go wrong with all of this? Let's assume we don't get hit with an uppercut out of nowhere for two years in a row; no nuclear wars on the Korean peninsula, no San Francisco earthquake, no 9/11-level terrorist attack on the U.S., etc. Almost all the outlooks for next year focus solely on the road map for escaping Covid-19. The most immediate concern is that our collective discipline breaks down, and health systems are finally flooded. That would lead to a bear scenario. Then there is the risk of botching the fiscal and possibly even monetary response. And then there are the daunting vaccine logistics. There's a possibility vaccines will bring a quicker-than-anticipated end to the problem. By spring, it's conceivable that all those most at risk will have been vaccinated, and the Western world can return to normal. It's also conceivable that something goes wrong with vaccine safety or the manufacturing process. Most precariously, there is what is known as "vaccine-hesitancy." Across the world, many are reluctant to take one. These are the results of surveys conducted in the U.S. and western Europe for Deutsche Bank AG. They suggest that politicians may be forced to make vaccinations mandatory, which could make the politics of 2021 very dangerous:  As Blokland says, achieving all three parts of the "trilemma" will be mighty difficult. The risks may explain why there is still so much room for investors to make moves that all seem to think necessary once Covid finally goes away. If all goes well, next year will see a further hunt for yield in fixed income, higher commodity prices, and a rotation toward cyclical equities and away from the U.S. Let's hope all goes well, and try not to think about Nicolae Ceaucescu. Generation ZMillennials get too much attention. Demographers are now looking at the generation that succeeds them, Generation Z, currently aged 24 or less. BofA Securities Inc. last week published a massive report headed OK Zoomer. Once the pandemic is behind us, it will seem very relevant. What follows are a few of the points that most caught my attention. It's not scientific. First, the future may well be Indian. In India, Generation Z has almost half a billion members.  Demographics should give fresh impulse to the emerging markets, where 89% of Generation Z live:  For me, the most pleasant surprise is this generation's attitude to media consumption. It's no surprise that they are ever less interested in "old media," particularly newspapers. What is intriguing is the stickiness of books. If you want to make a statement about something, you still write a book about it. Kindles are popular, but they haven't displaced physical books. Generation Z is now more likely to read a book than to listen to radio or watch a traditional sport — almost inconceivably, they are as likely to read a book as watch broadcast television. I really must remember to write that book proposal:  More intriguingly, and perhaps positively for the environment, Generation Z doesn't feel the need to have its own wheels, or even to learn how to drive. This is true even in a country as deeply in love with the automobile as the U.S. Self-driving cars have a future. So does investment in better public transit:  One other fascinating finding is that this is the least nationalistic generation yet born. In Britain, former Prime Minister Theresa May once derided opponents of Brexit as "citizens of the world," with the implication that this was a bad thing. A slight majority of Gen Z are happy to consider themselves thus:  This generation's priorities are very different, and they could soon have a big political impact. One theory in the U.S. is that the Democrats' interest in left-wing identity politics may have cost them the decisive mandate they wanted this month. Large numbers of older Americans had no interest in notions like "defund the police," and this affected the way they voted. In another decade, when all of Generation Z has the vote, things might be different. The generational strife caused by the coronavirus won't, we can be sure, go away. Survival TipsRudy Giuliani's antics of the last few weeks have been a disgrace to his country, and have trashed his legacy, in my sad opinion. As someone who was in Manhattan on Sept. 11, 2001, I recommend this clip for a reminder of why the man had such a strong reputation. And I also want to thank him for his latest press conference, which at many points lurched into absurdity, but did at least cite the great 1992 comedy My Cousin Vinny. I'm now going to take off for the next week. A happy Thanksgiving to American readers, and an enjoyable week for everyone else. We all have something to be thankful for, hard though that is to see at times like this. I'll be back in your inbox on Nov. 30. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment