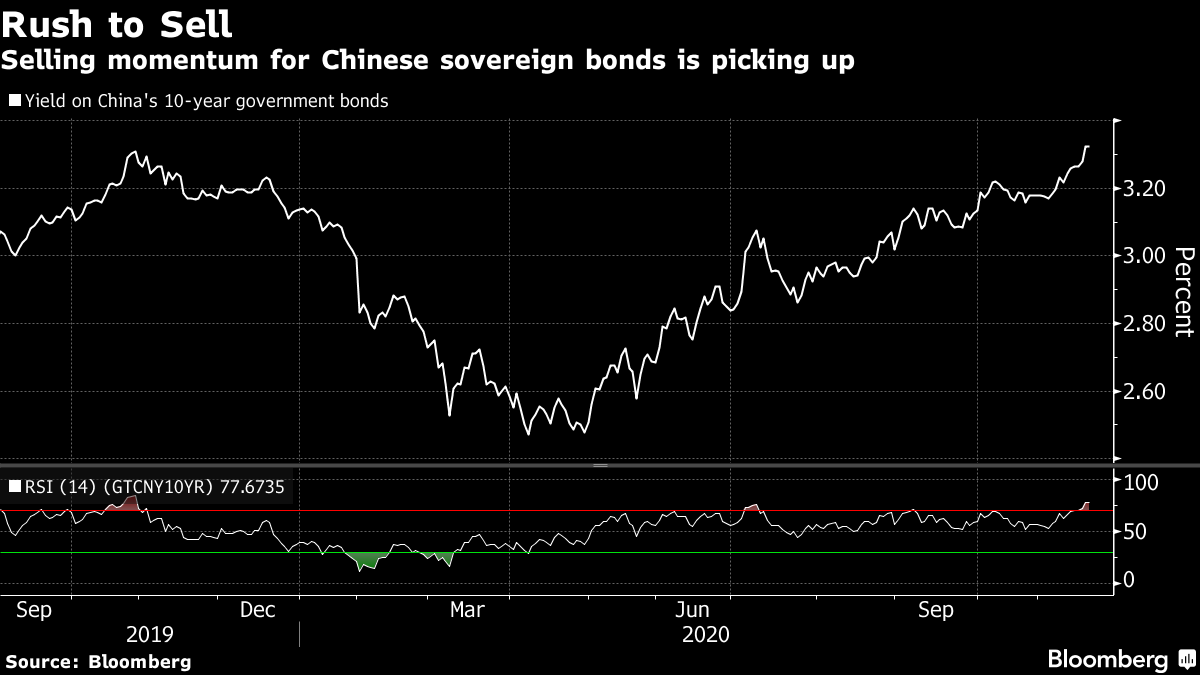

| Welcome to the Weekly Fix, the newsletter that's relieved after all those Senate hearings on Judy Shelton's nomination to the Fed, we finally have cloture. -- Emily Barrett, Asia FX/Rates Editor. That SpatThe Fed chief says it's too soon put away its emergency tools to help markets and the economy. Now it looks like the Trump Administration will confiscate some of them. Jerome Powell looked set this week to extend key lending facilities that were due to expire at the end of the year: "When the right time comes -- and I don't think that time is yet or very soon -- we will put those tools away," he said. "The recovery is incomplete." The Treasury has other plans. Secretary Steven Mnuchin on Thursday sent the central bank a list of funds to be repaid, that would allow Congress to "re-appropriate" $455 billion that was earmarked for Fed support programs. That means a number won't be carried into the new year, including the Main Street lending facility, and backstops for the municipal- and corporate bond markets.  This is a very different tone to the collegial spirit that seemed to prevail between the two officials during their long hours of House testimony together this year -- a vision of fiscal and monetary forces battling together for the U.S. economy. The Fed's response, that it would rather "the full suite" of special facilities "continue to serve their important role as a backstop for our still-strained and vulnerable economy" leaves us wondering about what's next, legally speaking, and what purpose is being served. It's unclear when or how the reclaimed funds might be redeployed -- clearly they're not anywhere near the $2-trillion-plus spending bill proposed by the Democrats, or President Donald Trump's promise of something even bigger prior to the election. It's fair to say that the market doesn't need help right now, but this action knocks out a safety net at a time when lawmakers have no clear plan. And no one needs reminding that the U.S. is heading into a tough winter, with infection rates setting daily records, renewed restrictions on activity, school shutdowns and more businesses closing. Moreover, terminating the programs on Dec. 31 means they may be tougher to restart under the new Biden Administration 20 days later. New funds will need Congressional authorization, though JPMorgan's Mike Feroli said the incoming Treasury Secretary could agree to restart the facilities with pre-CARES Act cash available in the department's Exchange Stabilization Fund, which he puts at just over $70 billion. So for now the upshot is more delays and uncertainty over crucial support for the economy -- and more to come if the last Senate races in Georgia next month deliver another bitterly divided Congress. Treasuries, unsurprisingly, rallied on the administration's message, sending the 10-year bond yield back toward 0.80%. Evercore's Krishna Guha remarked on the "politicization of market stabilization policy," which he expects will force the Fed to more action at its Dec.16-17 meeting. That probably means laying out a more-detailed bond-buying plan, shifting its purchases to longer-dated Treasuries, and if needed, speeding up the pace. "However, QE is a very imperfect substitute for a credit market backstop," Guha wrote. The credit facilities have their detractors. The runup in asset prices since the primary- and secondary-market purchases were announced made even some investors queasy. And this month yields on lower-quality corporate bonds sank to record lows, a worrying sign for those warning of a zombie-company apocalypse. ("The training wheels are coming off," DoubleLine Capital's Jeffrey Gundlach, tweeted Thursday -- he's been dour on credit throughout the Fed-induced rallies.) But the key point of these and the municipal bond facilities were that they didn't need to be tapped. Their presence helped keep the market open for many borrowers, and gave investors confidence to lend. They are just no substitute for government action -- a point Powell himself emphasized many times to lawmakers in his testimonies alongside the Treasury Secretary. Hopefully the "targeted stimulus" that Mnuchin touted in his contributions to the Congressional discussion will materialize, to see households and businesses through what's shaping up to be a painful holiday season. China Default-linesThis was a landmark week for China and its neighbors, as 15 Asia-Pacific countries signed the largest-ever regional trade deal. The Regional Comprehensive Economic Partnership covers about a third of all people on the planet and a similar proportion of global output. It's hard to overstate the significance for the participants -- and for the superpowers left out, namely the U.S. and India. The region's stocks responded accordingly: an MSCI gauge of Asia-Pacific shares climbed to a record. But China's bond markets had other issues to contend with. The defaults of two more state-linked firms -- a top chipmaker and a car manufacturer -- spilled over into the government market.  As corporate bonds weaken, fears that clients might redeem their money have motivated financial institutions to offload their most easily traded assets. The 10-year benchmark government yield is headed to an 18-month high above 3.32%. The solvency of China's corporate sector has long been a point of unease, of course, as global investors have weighed whether the state is willing -- assuming it's able -- to continue propping up weaker enterprises that have binged on debt. Regulators have been busy lately slapping down the practice among some firms of snapping up their own bonds at the point of issuance.  What happens next depends partly on how much appetite global investors have to step in to buy. Demand for Chinese bonds has gained momentum over the past year, since they started joining benchmark indexes in September 2019. In September, FTSE Russell became the last of the three main index compilers to add Chinese debt after JPMorgan and Bloomberg Barclays (which is owned by Bloomberg News parent Bloomberg LP). That said, it's not all been plain sailing recently -- JPMorgan has moved to exclude from its listings debt that falls under the U.S. sanctions announced this month. Its indexes include 72 such securities, and for now the existing bonds can stay, while new issues from the sanctioned companies, or taps of the existing ones, will be off-limits. The attractions of China's market may also overwhelm investor concerns. A strongly appreciating currency adds to the appeal of Chinese assets -- the yuan has gained almost 10% from the year's low in May, thanks in large part to the country outpacing the rest of the world in its recovery from the pandemic. That's a welcome state of affairs for Chinese authorities seeking to promote the currency's global use. Moreover, a yield north of 3% on its 10-year government bond is hard to pass up when more than $17 trillion of the world's debt is so expensive it's yielding less than zero. It's still a borrower's market -- and that brings us to a new milestone for China. The country sold its first debt at negative interest rates this week, with a five-year euro-denominated note alongside two longer-dated issues. Orders for the bonds were more than quadruple the total 4 billion euros offered. Europe's Best-Laid Plans...And to bring us full circle on negative rates, and government spending discord – there's notably less harmony in the European Union. The promise of an historic pan-nation rescue package earlier this year sparked talk of steps toward a real fiscal union, and, who knows? German yields above zero? But now that common purpose is looking a bit fractious, with Hungary and Poland pushing back on a 1.8 trillion euro ($2.1 trillion) plan. The country's prime ministers apparently object to tying the disbursement of aid to upholding democratic standards, according to the latest from our reporters Nikos Chrysoloras and Viktoria Dendrinou. The veto means that the spending agreed by EU leaders in July won't be up and running in the beginning of the year as planned. To add insult to injury, the setback may also force the EU into a partial shutdown in the new year, and it could spill over into other prized policy areas, such as climate. So far European markets are keeping their sang-froid, with bonds continuing to rally in the bloc's more-indebted southern member states. But that has a lot to do with the expectations that continue to be pinned on the European Central Bank as it approaches its Dec. 10 policy meeting. President Christine Lagarde has already pledged a forceful stimulus package from the central bank, and urged governments to unleash their own pandemic relief spending "without delay." Most economists predict an additional 500 billion euros in bond purchases. It will take the market some time to have similar faith in a coordinated government effort. Bonus PointsA year on from the first stirrings of the global pandemic. Here's a moment to appreciate the things that haven't gone wrong… Cerberus shelved its look-a-like commercial mortgages CDO Not Dead Yet: The French killed off quite a few celebrities, accidentally Hang on. Does Judy Shelton still have a chance? Be inspired by the world's bravest journalists |

Post a Comment