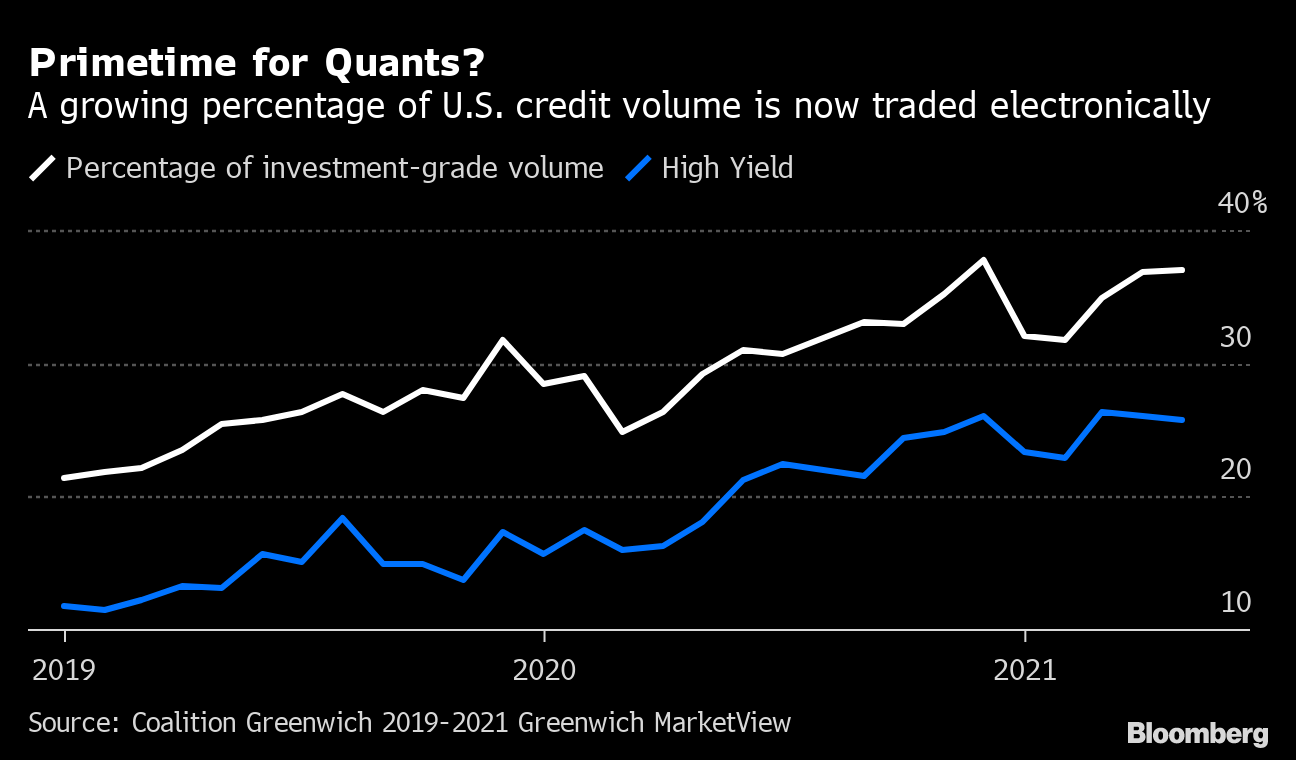

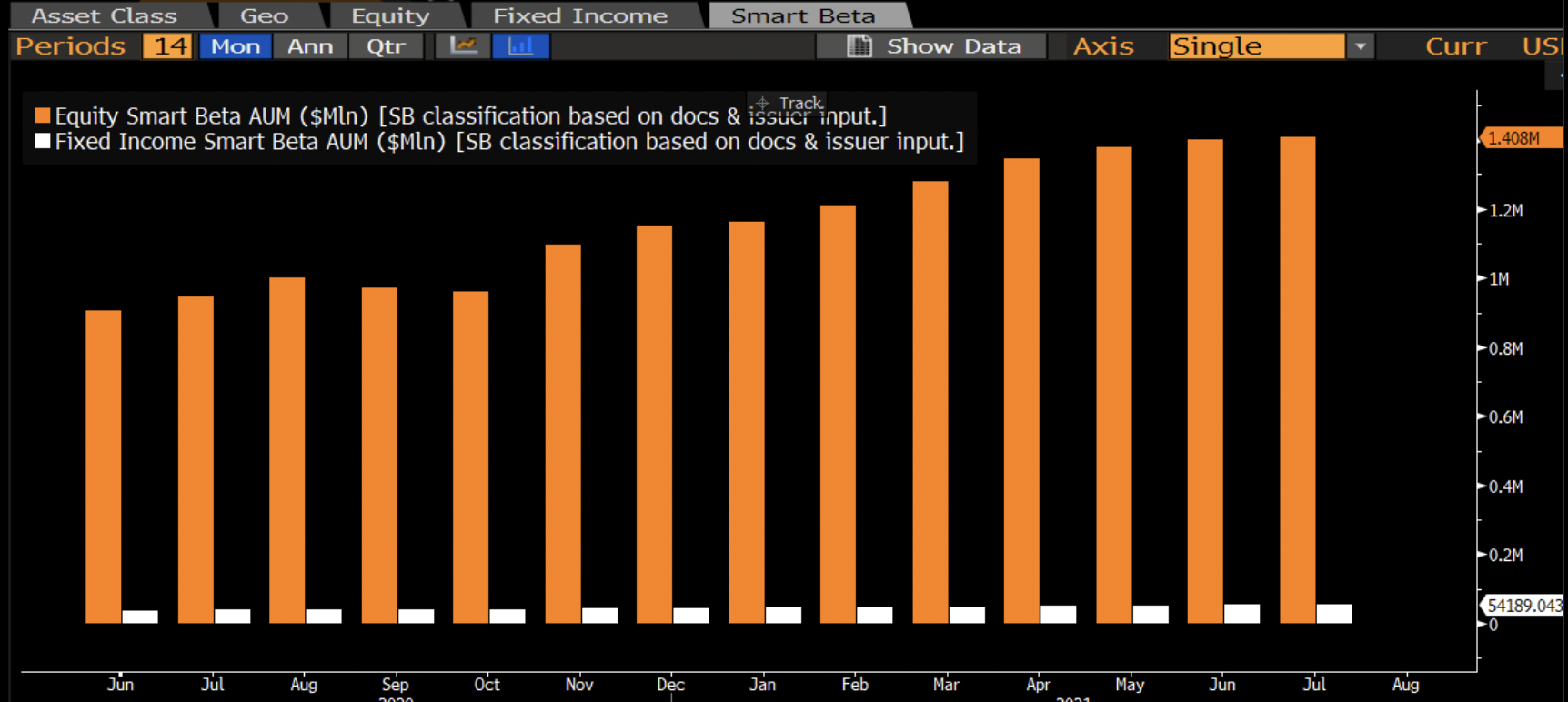

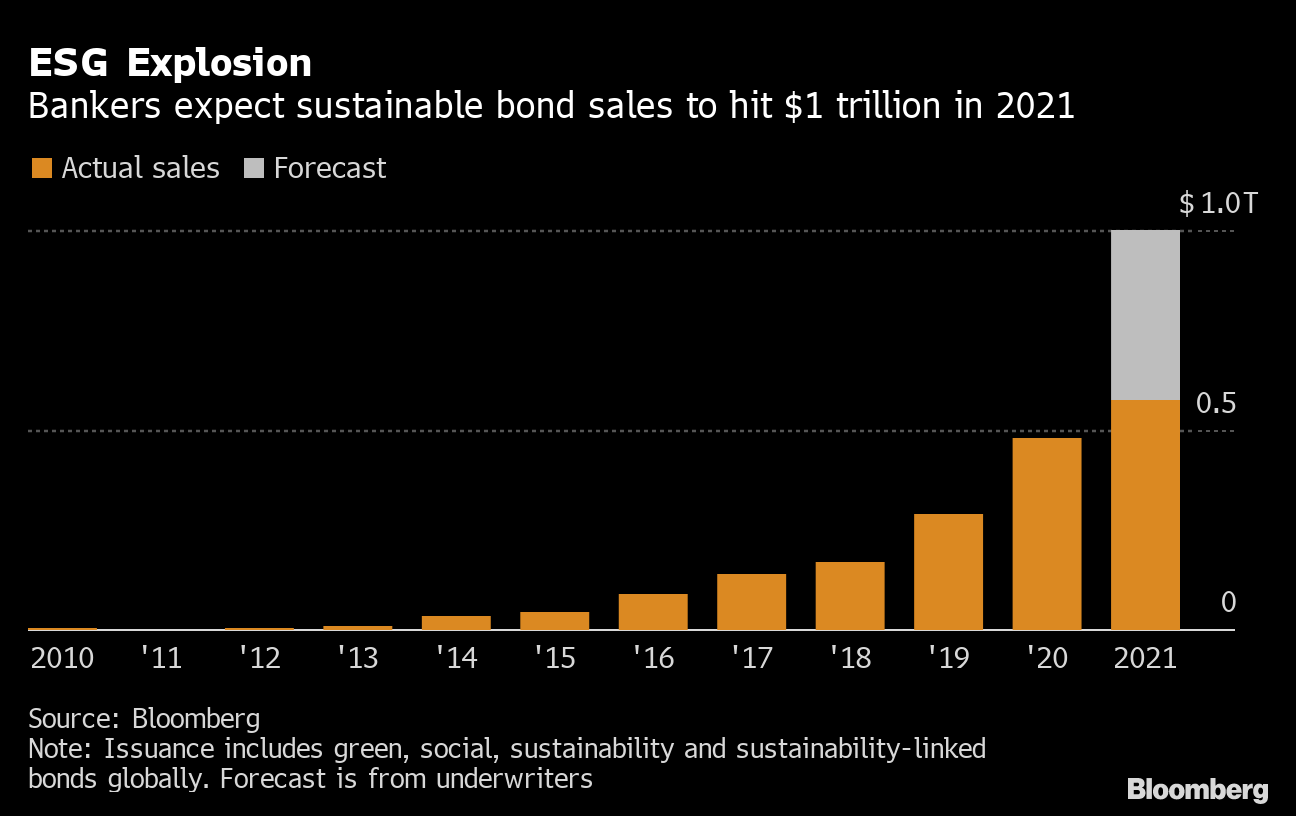

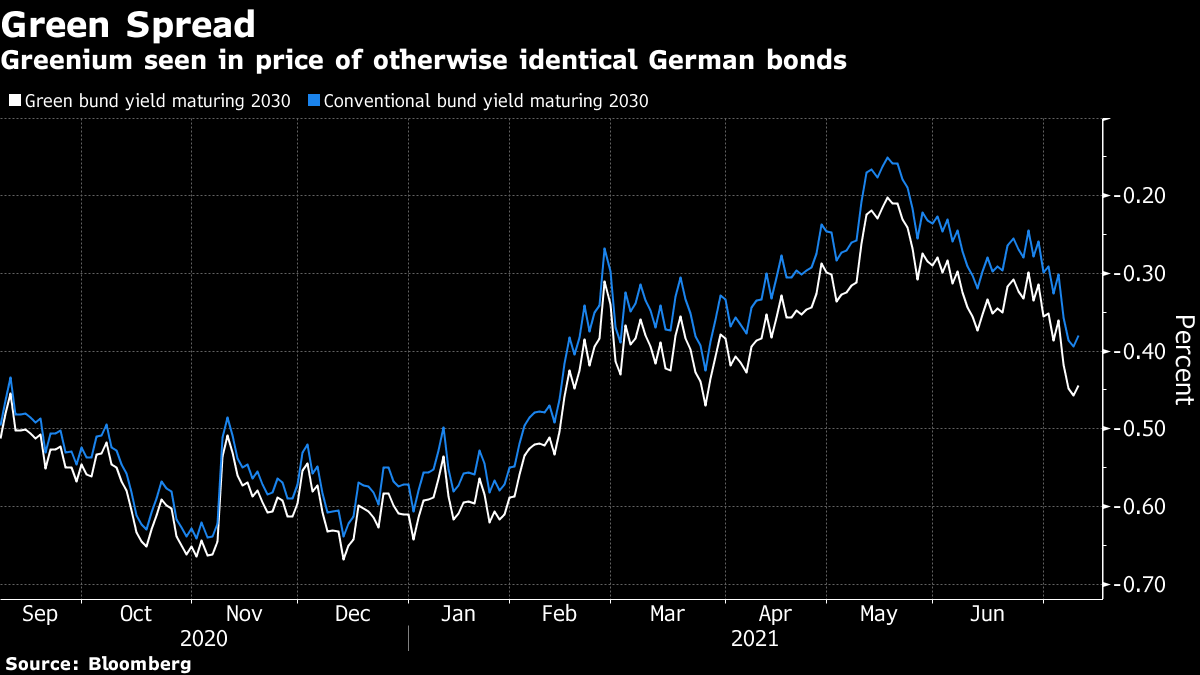

| Welcome to The Weekly Fix, the newsletter that's still working on its poker face. I'm cross-asset reporter Katie Greifeld. Don't Call it a Policy ErrorAnother week, another surprisingly intense Treasury rally. Yields on 10-year Treasuries are set to drop for a third straight week, and briefly cracked below 1.3% in U.S. trading Thursday. However, the real action -- as it often is -- is in real yields. A precipitous drop took 10-year real rates as low as minus 1.05% this week, the most deeply negative since February.  You'd be forgiven for looking at the 10-year real yield chart and wondering what's changed. Sure, U.S. growth is probably peaking right now. Sure, there's still a 6.8 million payrolls hole in the U.S. labor market versus pre-pandemic levels. And alright, Federal Reserve Chair Jerome Powell says "substantial further progress" is still a ways off. But still, is the economic outlook cloudy enough to justify a 45 basis points drop in real rates since mid-March? Maybe not in the U.S. But for the rest of the world? Many other nations are lagging well behind the U.S. in terms of reopening their economies -- plans which delta-variant woes are threatening to scramble. All of those concerns are cycling through the U.S. bond market. "Real yields are low because the market is worried about the global growth outlook," BMO Capital Markets strategist Ian Lyngen said. "The Treasury market doesn't trade solely on the U.S. macros of growth and inflation."  Meanwhile, the 5s30s curve crept flatter this week -- an impulse that Powell only added to during his Congressional testimony. The Fed chief referred to the inflation spike we're seeing as "unique," which seems to be a fancy word for transitory. That's kept upward pressure on the front-end of the curve as traders price in liftoff, while the back-end is weighed down by the longer-term growth outlook. In a way, it feels like the bond market is trying to call the Fed's bluff on this average inflation targeting business -- that policy makers aren't actually going to let things run that hot for all that long. But don't call it a policy error, Lyngen said. "It's too soon," he said. "The economy is fine." Racing to the BottomHigh-grade credit spreads are basically at rock-bottom levels, but by some measures, the tightening in junk spreads has been even more dramatic. The spread between investment grade and high-yield spreads dropped to the lowest level since 2007 last week, according to Bloomberg data. At 271 basis points, junk spreads have much more room to tighten than high-grade spreads at around 80 basis points. But still, there's a takeaway to be found about just how rosy things have gotten in the corporate bond market, helped by ample Federal Reserve liquidity and a recovering economy.  As a result of the Fed's safety net, companies have taken advantage of ultra-low financing costs to borrow record amounts. Those issuers then look more capable of servicing their debt, which is one of the reasons why rating upgrades have outpaced downgrades this year. And forget about default risk. "Default rates continue to fall in high yield -- my model shows 1% in the next 6 to 12 months -- leverage is collapsing, interest coverage is accelerating, and portions of the market are still relatively cheap-ish given the collapse in default expectations," said Michael Contopoulos, Richard Bernstein Advisors's director of fixed income and portfolio manager. "So to me, it makes sense the spread between the two is falling." Still, Contopoulos sees IG spreads bumping up against a floor -- investors need some level of compensation for liquidity and credit risk. Quants Are (Slowly) ComingThere have been some interesting developments in fixed-income market structure over the course of the year-and-a-half-long pandemic. As chronicled by Bloomberg News's Justina Lee, electronic bond trading has accelerated and then some over the past 16 months -- convincing quants that now is their time to shine. Wiring up the bond market has proven more difficult than say, equities, because fixed-income is famously fiddly. Traders still do quaint things like place orders over the phone, while individual bonds may not trade for weeks or months, limiting liquidity. Compare that to the stock market, where all it takes is the click of a button and bid-ask spreads are razor-thin. That can make it difficult to do even basic quant-y things, like actually acquire the bonds that your algorithm spits out.  Bloomberg Bloomberg However, there are signs that the seas are shifting. Coalition Greenwich data show electronic platforms like MarketAxess and Tradeweb accounted for 37% of investment-grade and 26% of high-yield trading in May -- a whopping 8 percentage points higher versus the prior year. Amid the uptick, long credit positions held by quants have doubled since 2018, according to Man Group data -- outpacing the 20% growth for other asset managers. Of course, it's important not to overstate those numbers. Those long positions total around $23 billion, Man Group says, versus $537 billion for other managers. And the human touch remains important in fixed-income trading, which is why Asita Anche at Barclays is building algos and data analytics for voice traders. "The future is not algos taking flows away from humans," Anche, the head of systematic market making and data science, told Lee. "It's humans enhanced by algos and automation."  Bloomberg Bloomberg The premium placed on the human hand could help explain why demand for smart-beta bond exchange-traded funds -- which are largely passively managed -- is virtually non-existent. Even amid skyrocketing demand for debt ETFs, such funds only command about $50 billion in assets. Meanwhile, smart-beta equity ETFs hold about $1.4 trillion. "Advisers still have a lot of faith in bond managers. They tend to view bond managers as having an extra skill set," Bloomberg Intelligence analyst Eric Balchunas said. "They view the stock market as checkers and the bond markets as chess." The $1 Trillion Green GiantGreen bonds are having a moment. Global sales of debt issued with environmental, social and governance goals in mind have already reached a record $577 billion this year, according to data compiled Bloomberg -- already $100 billion more than 2020's entire haul. Underwriters expect an even busier second half, which is expected to push issuance past $1 trillion for the first time ever.  Partly fueling the boom is an uptick in sustainability-linked bonds, which put some teeth behind the ESG label as the likes of former U.S. vice president Al Gore warn about greenwashing. So-called SLBs raise borrowing costs should issuers fail to hit ESG goals, and global sales currently clock in at about $73 billion. JPMorgan Chase & Co.'s Marilyn Ceci expects the SLB to jump to as high as $150 billion by year-end, and expects overall ESG debt issuance to double. "What began with 'why should I issue?' is now 'why aren't you?'," Ceci, global head of ESG debt capital markets at JPMorgan, told Bloomberg News's Caleb Mutua. "Your absence in the market says something now," said Ceci, who expects issuance volume to double by year-end. Those who follow the space won't be surprised to read that Europe is the powerhouse behind ESG bond issuance -- and it's only getting stronger. In the first half, a stunning 26% of of all euro-denominated high-grade corporate bonds issued were ESG-linked. That compares to about 9% this time last year.  Ethical bonds are such a phenomenon in Europe that they often trade at a premium to your run-of-the-mill debt -- a greenium, if you will. That markup is expected to widen even more after the European Union unveiled a self-proclaimed "gold standard" rulebook, which will require mandatory impact reporting and external reviews by issuers -- who in turn will likely see their debt command higher prices, since buyers know it's legit. But while most of the ESG spotlight tends to shine on environmental issues, social bonds are increasingly getting more airtime. That trend took root during the pandemic, with countries to corporations issuing coronavirus response bonds, and has accelerated since, according to Morgan Stanley's Audrey Choi. "We've seen that continue to accelerate, a real interest in all sustainable investing, on the 'S' in particular and understanding the integration of the three," Choi, the firm's chief sustainability officer, said during a Bloomberg Sustainable Business Summit panel this week. Bonus Points Treasury Wants Large Holders of 2020 Note to Identify Themselves Reddit Traders Are Upending the World of Credit Investing, Too Shark advocates call for rebranding violent attacks as 'interactions' |

Post a Comment