| Welcome to the Weekly Fix, the newsletter where 30 basis points is a big deal. I'm cross-asset reporter Katherine Greifeld, filling in for Emily Barrett. Reflation Pulse CheckThose waiting for the big reflation trade to finally take off were dealt another head-fake this week. First came the news of a potential breakthrough in the hunt for a Covid-19 vaccine, unleashing a wave of selling in the Treasury market. Benchmark yields promptly surged to 0.97% on Monday, briefly boosting the 2s10s curve to the steepest level since 2017. The excitement was palpable. Morgan Stanley's Matthew Hornbach told Bloomberg News that is was a "tremendous day for the world" and that there was "good scope" for further curve steepness. ING strategists wrote that Monday brought "the 'vaccine' moment the rates market had waited for" and that this time is truly different: The big difference here from previous moves is that we won't need to take this back. We have moved from a digital state of no vaccine to one where there is one.

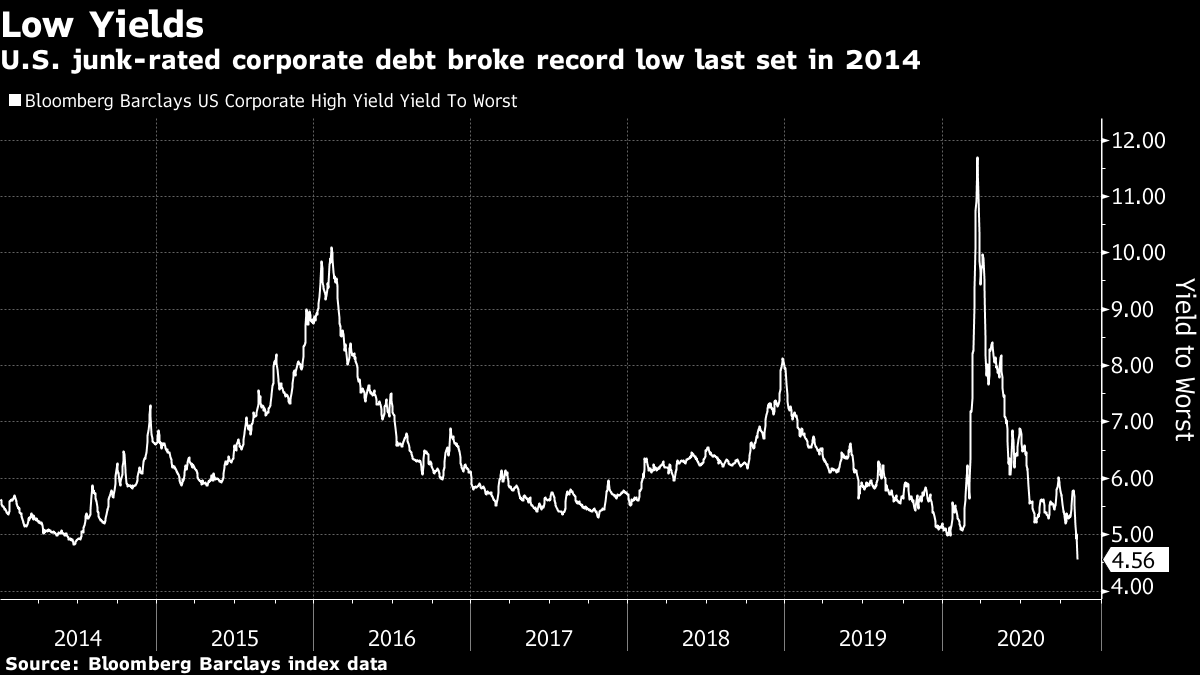

That a large-scale study of a vaccine being developed by Pfizer Inc. and BioNTech SE prevented 90% of infections is extraordinary. The absence of such a development was a gaping hole in every reflation thesis. But the reality of how long it will take to see such a vaccine distributed broadly and the economic pain possible in that time quickly set in. U.S. case counts rose to a new record this week, while cities from Chicago to Minneapolis to New York City reinstated containment measures.  And there were already signs economic activity was slowing before that. Only about a quarter of workers among 10 large U.S. metro areas returned to the office last week. Southwest Airlines warned its revenue recovery is slowing as cases surge. High-frequency data from OpenTable -- a measure of restaurant bookings -- show "a significantly larger decline in indoor dining activity in states with higher case growth," according to Goldman Sachs. The combined weight of such headlines was enough to crush another budding reflation bet. Rates slammed lower, led by a long-end rally in the face of a whopping $27 billion auction of 30-year bonds. The 10-year yield fell to 0.87% in Asian trading on Friday. But what if rates had kept rising? What if the 10-year yield had actually breached the much-hyped 1% level? It's worth noting that even with this week's sell off, financial conditions -- a measure of strains across risk markets -- barely moved.  That muted movement -- combined with the fact bonds sold off for good reasons -- means that Federal Reserve policy makers probably would have been fairly relaxed. "If there was this massive move-up in yields, then they might get concerned and signal they'll buy more bonds. But if it's this gradual creeping higher on better economic news, I think they'll sit back and say, 'This isn't so bad,'" said Kathy Jones, Charles Schwab's chief fixed-income strategist. "We're not seeing a whole lot of stress in the system." Goldman's (Small) Big CallGoldman made waves this week with its annual year-ahead investment outlook, where it named a steepening U.S. yield curve as one of its key global themes for 2021. The thesis is straightforward: the Fed will keep the front-end anchored, while expectations for growth and inflation will buoy the long-end. However, for some, the call's magnitude left something to be desired, as laid bare by my Bloomberg Opinion colleague Brian Chappatta. The bank sees roughly 30 basis points of steepening for the 2s10s curve. They expect 10-year yields will top out at 1.3%, while 2-year yields may edge up to 0.25%. As a markets reporter, the thought that 2021 will bring just 30 basis points of movement paints a fairly bleak picture. But that non-action -- should it materialize -- has important ramifications across asset classes.  Consider the stock market's latest attempt to wean itself off tech and rotate back into value shares -- those that look cheap relative to fundamentals. Like the reflation trade, that was quickly somewhat squashed. But while it was taking root, bank stocks helped power the rebound. In fact, financials are still up about 6.6% this week, even after Thursday's hosing. It's a basic tenet of the banking business model to borrow at short-term rates and lend out at longer rates -- a tricky proposition with a relatively flat U.S. curve. That's a problem for value strategies, given than financials are the largest sector weighting in the Russell 1000 Value Index. If the bull case on value is a bearish bet on bonds, just 30 basis points of steepening may not bode well for the strategy's prospects in the new year. Maybe a 4.56% Yield on Junk Makes SenseHere's another headline that turned heads this week: The average yield for the Bloomberg Barclays U.S. corporate high yield index plummeted to an all-time low of 4.56% on Monday, sinking below the previous record of 4.83% set in June 2014. That 45 basis point drop from Friday's close was the biggest decline since April 9, when the Fed expanded its corporate bond-buying program to include certain junk bonds. Naturally, that inspired some snark on social media, and awe that 4.56% is what passes for high-yield these days amid the worst pandemic in modern history. Of course, several factors got us here: an almighty Fed with seemingly unlimited firepower, the global hunt for yield sparked by unprecedented central bank stimulus and finally, this week's pivotal vaccine news.  But it's also worth taking a peek under the index's hood. Over 53% of the Bloomberg Barclays high-yield index is made up of double B rated bonds -- the highest rating tier in the junk market -- while triple C bonds made up 11.8%. Coming into the year, those figure were closer to 47% and 13%, respectively. "It's a different high-yield market than we had the beginning of the year," said Gene Tannuzzo, deputy global head of fixed income at Columbia Threadneedle. "The highly-levered companies that can't make it through a pandemic have already defaulted. So it's less risky in that sense." Another large factor behind junk's increasing quality is 2020's proliferation of fallen angels, or companies that have lost their investment-grade status. Ford Motor Co. became the largest such issuer in March, removing $35.8 billion of debt from the Bloomberg Barclays high-grade index. Currently, three of the five largest issuers in the Bloomberg Barclays high-yield index are fallen angels this year -- Ford, Occidental Petroleum and Kraft Heinz. Concentrated in the double B tier, that's helped skew the high-yield index towards the least-junkiest junk. A $150 Billion Bond-Trading BoomPortfolio trading is at the bleeding edge of bond market structure, and it's getting even bigger. Tradeweb Market told Bloomberg News this week that it processed $19 billion worth of portfolio trades in October, the most since it launched its service in 2019. All told, the company handles volume totaling more than $150 billion in these transactions. Portfolio trading is new, and it's exciting: market players are able to turn over entire baskets of bonds in one fell swoop. That's especially handy for transacting in less-liquid securities: by packaging them in a bundle with other bonds, it's easier to move them. Several years of explosive growth in credit exchange-traded funds has helped fuel portfolio trading's rise. Traditional ETFs disclose their holdings daily, providing independent prices and giving both banks and investors a blueprint from which to value their own portfolios.  Additionally, while portfolio trades don't have to be linked to an ETF, they tend to take advantage of the structure. Shares of an ETF are created and redeemed by middlemen known as authorized participants, who will swap a basket of assets matching the fund's profile for shares from the ETF issuer, or vice versa. Fixed-income ETFs have boomed this year, with assets in U.S.-based funds ballooning to a record $1 trillion. While the Tradeweb figures are the latest evidence that ETFs have helped drive portfolio trading's advent, harvesting the benefits aren't necessarily straightforward. Getting the most out of the strategy is "conditional on a few factors being met pre-trade such as a diverse list of bonds, sectors and maturities," Stuart Campbell, head of trading at BlueBay Asset Management, told Bloomberg News. Bonus PointsJudy Shelton -- one of President Donald Trump's Fed nominees -- moves closer to a confirmation vote U.S. veteran-owned banks are getting a bigger piece of the U.S. investment-grade corporate bond underwriting pie Joe Biden Had Quite the Week. So Did Japanese Mayor Jo Baiden. |

Post a Comment