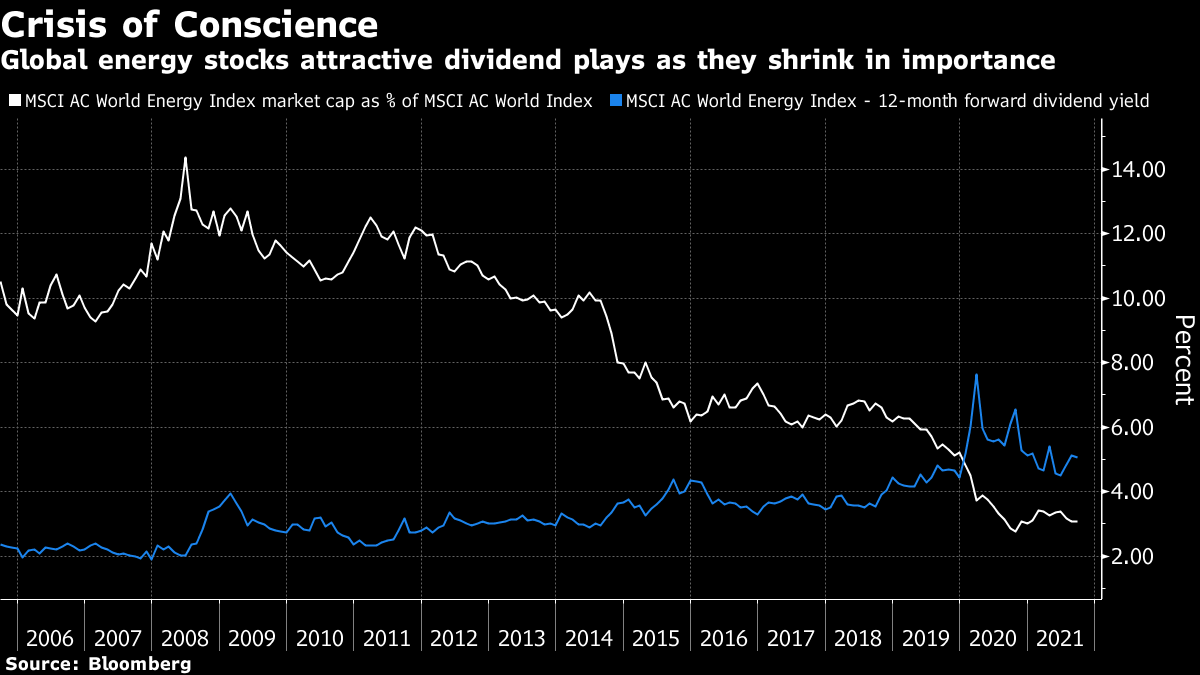

| Good morning. The ECB slows the pace of bond purchases, the U.S. adds to the vaccine push, equity concerns grow and China intervenes in the oil market. Here's what's moving markets. The European Central Bank has decided to slow the pace of purchases under a giant emergency program it unleashed in the wake of the coronavirus pandemic. President Christine Lagarde was careful not to call it a tapering but a "recalibration" amid a stronger near-term outlook for prices and growth. And bond purchases may still end up lasting for years as conditions for a rate rise are unlikely to be met, according to a Pimco money manager. U.S. President Joe Biden will ask federal employees, contractors and health-care workers to get vaccinated against the coronavirus, adding to government efforts around the world to deal with unprotected parts of the population. The decision follows a rise in delta variant infections that triggers fresh concerns about the pandemic. Meanwhile, researchers are warning that the proliferation of Covid-19 variants in Africa, partly attributed to a low vaccination rate, could lead to vaccine-evading mutations. Deutsche Bank analysts are adding to concerns about high stock valuations, flagging growing risks of a "hard" valuation correction. Five-year forward returns have tended to be negative on average when stocks trade at similar valuations to today. This follows recent warnings from Goldman Sachs, Morgan Stanley and Citi that equity gains in the U.S. are increasingly vulnerable to shocks, ranging from Covid-19 to the easing of central bank support. China is selling oil from its strategic reserves, explicitly to lower prices, in a major intervention from the world's largest oil importer. The government is combating rising raw materials costs and indicated it could release more reserves to balance the market. The move comes as factory-gate inflation has risen to a 13-year high, which puts pressure on consumer prices worldwide. It's looking like a good day for European stocks after equities rose across the board in Asia, with Japan resuming its Suga-free rally and Chinese tech shares rebounding. A phone call between President Joe Biden and China's Xi Jinping helped to lift the mood. Today, Russia is in focus with the central bank expected to deliver a fifth straight rate hike as prices continue to run hot. Elsewhere, ECB Governing Council Member Olli Rehn speaks at monetary policy conference, and the U.K. reports monthly GDP figures. GVS, El.En, Medacta report in Europe while in the U.S., retailer Kroger is among the reports in a quiet day. This is what's caught our eye over the past 24 hours. Harvard's declaration that it will no longer invest in fossil fuels comes at a time when global energy stocks are looking increasingly attractive to less environmentally-minded investors. The American university's endowment has no investments in companies that explore for or develop fossil fuels and "does not intend to make such investments in the future," according to a letter from President Larry Bacow on the Harvard website. The move echoes a trend of prominent investors shifting their energy holdings toward renewable names and green technologies. The market cap of the MSCI AC World Energy Index has shrunk to just 3% of the global stocks gauge, down from about 14% in 2008. Yet the exodus has made the energy cohort super cheap -- it trades on just 10 times forward earnings -- and it has an attractive 5% forward dividend yield, three percentage points above the global average. Of course, investors still have to wrestle with their own consciences -- a legitimate debate on a warming planet -- and quite possibly their fund mandates, if more asset managers take a stance like Harvard's. But it's notable that even ESG indexes contain old school energy stocks, so they have not yet reached uninvestable status.  Cormac Mullen is a cross-asset reporter and editor for Bloomberg News in Tokyo. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment