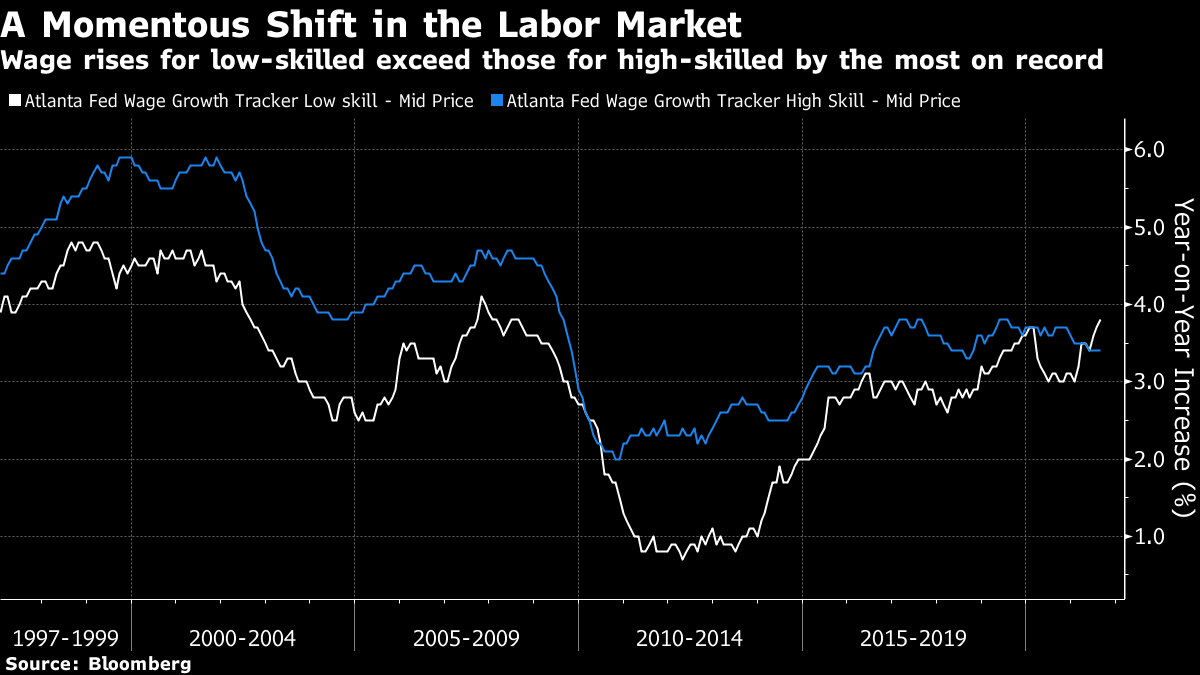

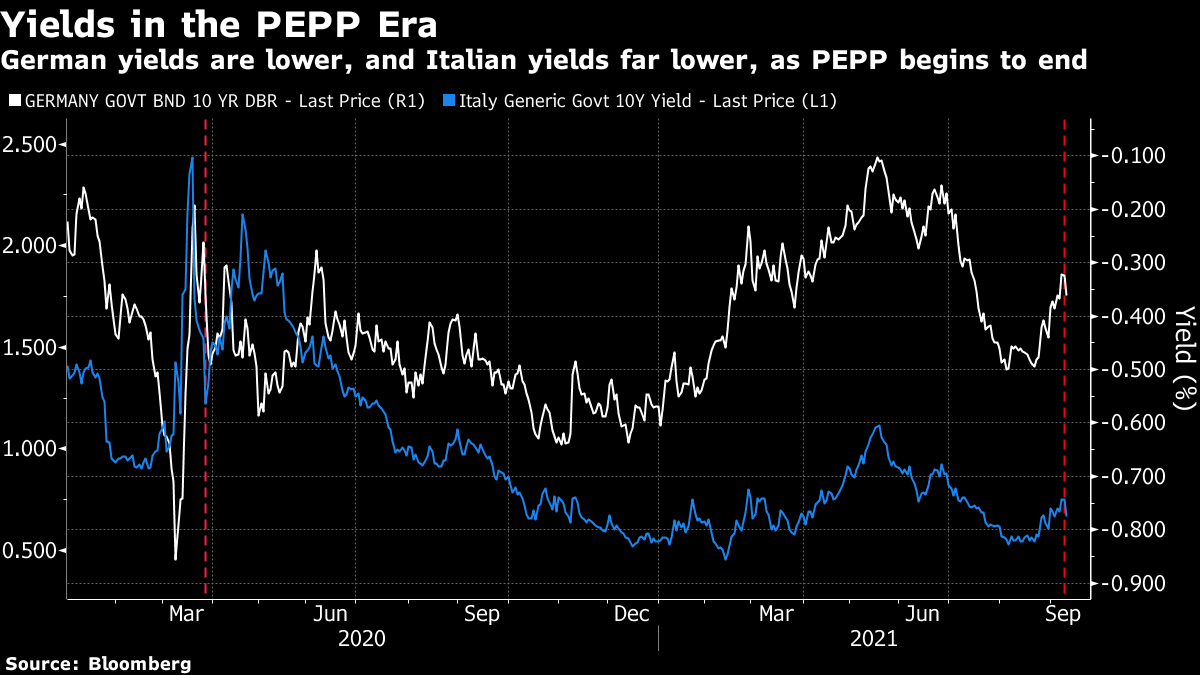

| To get John Authers' newsletter delivered directly to your inbox, sign up here. I spend a lot of my professional life drawing charts. You had probably noticed this. Often, producing a chart that tells a story clearly and without distortion takes a lot of work. And sometimes, the first numbers I key into the terminal lead to something truly fascinating that needs no further explanation. This is one of those charts. The latest revision of the Atlanta Federal Reserve's Wage Tracker, for August, is now out. It's enthralling research that has been running since 1997, and breaks down earnings growth by gender, age, skill, level of education and so on. This is how wages have risen since 1997 for the high-skilled, compared to the low-skilled:  For the third month in a row, wages for the low-skilled have risen faster than for the high-skilled. In the previous history of the survey, which now goes back almost 25 years, this had only ever happened in two months, in early 2010. Wage growth for the low-skilled is also exceeding that for the high-skilled by the most on record. In terms of the momentous macroeconomic issues of the moment, this is good for growth, as poorer people are more likely to spend their pay rises than richer people. It's also potentially bad for inflation. Wage growth for the lowest skilled is the fastest since August 2008 (not coincidentally, the month before the Lehman bankruptcy), and that could easily lead to higher prices. More interestingly still, it does suggest a shift in the balance of power between labor and capital. This isn't as yet a deep-seated or well-established trend, of course. But if it continues it could rattle a lot of assumptions, and alleviate a lot of social tension. And that leads to one final readthrough. Low-skilled workers endured a truly terrible deal from 2011 to 2013, when their wages didn't even gain 1% per year. Higher-skilled workers did far better. Barack Obama was president at the time. If any one chart helps to explain how Donald Trump was able to disrupt the coalition that elected Obama, this might be it. And if this continues, it could be fantastic political news for Joe Biden, who could do with some at present. It's worth watching this, very closely. My late parents-in-law used to have a large sign prominently displayed in their kitchen: "Make New Mistakes." It's a great dictum for life, and central banks are doing their level best to follow it. They aren't making the old mistake, of messing up their communications and scaring the market into throwing a tantrum when they try to start removing support. We await with trepidation to find out what the new mistake is. The latest example of avoiding the mistakes of the 2013 "taper tantrum" comes from the European Central Bank, which on Thursday duly announced what most of us would call a taper of its Pandemic Emergency Purchase Program, or PEPP, that was introduced last year to deal with the pandemic. It will make purchases in the final quarter at a "moderately slower pace" than in the preceding two quarters. But President Christine Lagarde channeled her inner Margaret Thatcher to say that "the lady isn't tapering." Rather, she said, "we are recalibrating, just as we did back in December and back in March. We are doing that on the basis of the framework, which is a joint assessment." The market believed her. Euro-zone bond yields fell after the announcement. Both German yields and, quite dramatically, Italian yields are lower now than they were when when the PEPP started. No tantrums here.  Why so relaxed? In part, Jorg Kramer of Commerzbank AG says, all the nudges and winks from the ECB suggest that the PEPP purchases will go on for longer into next year, even if at a somewhat slower pace than before.

the ECB will decide on the more important question of how the PEPP programme will continue after March 2022 only at its meeting in December. We are more than ever of the opinion that the ECB will then loosen its monetary policy further: Economic growth is expected to slow significantly in the fourth quarter – because of the new Corona wave, less growth in the important export market China and because of the continuing supply bottlenecks. This significant growth slowdown is not yet included in the ECB's forecasts. The many doves on the ECB Governing Council will not let such a negative economic surprise slip by as an argument for further easing.

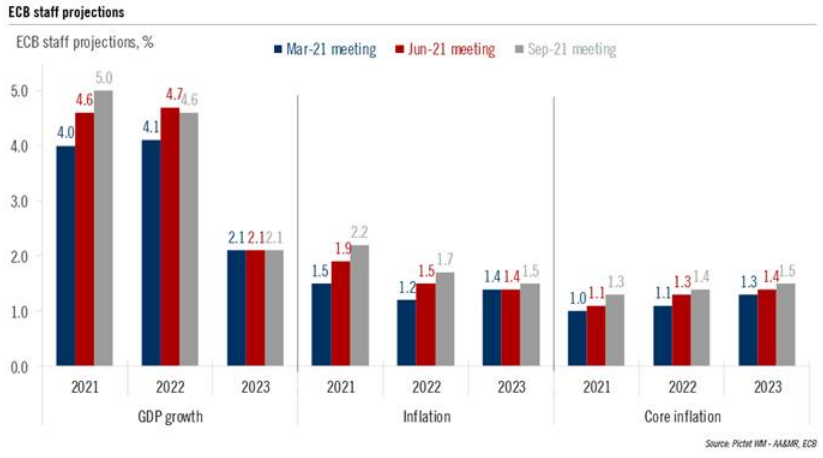

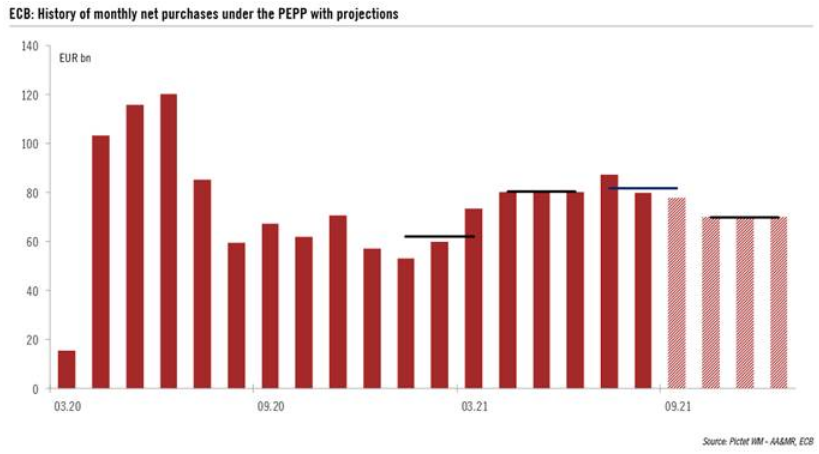

Beyond that, he points out that the ECB's inflation projections are rising, which implies that it will be more aggressive about tapering. The ECB also increased its growth projections, which on the face of it would also imply that it is time to taper. Lagarde conceded that inflationary pressures look more durable than they did earlier this year — which in itself sounds a little hawkish. However, Lagarde continues to say she is confident that the current inflation is driven by transitory bottlenecks, and the market evidently attached lot of importance to that. Further, growth is still expected to regress to an anemic 2.1% in 2023, when inflation is projected to be 1.5% on both a headline and a core basis — not remotely the kind of projection to worry anyone, and indeed a justification for continuing to juice the market with asset purchases. This chart of the ECB's projections comes from Pictet Asset Management Ltd:  Kramer also points out that many governors of the ECB will want to keep borrowing costs low for their indebted governments, which also gives them an incentive to keep feeding in support. Put all this together, and it seems reasonable to expect a continuation of the PEPP in December. This projection comes from Pictet, and many other analysts seem to expect a pattern of purchases along these lines:  That is how the lady managed to taper without the faintest sign of a tantrum. It has been achieved with a slight strengthening of the euro compared to the dollar. The fact that she has done this probably makes it a little easier for the Fed to start to taper sooner rather than later — although the inflation data over the next week, starting with producer prices on Friday, will be rather more important. And even if the central banks have avoided the mistake of eight years ago, there remains the risk that they will commit a new one.  | I was planning to offer some tip to do with 9/11, whose 20th anniversary falls this weekend. But frankly although that dreadful day has produced a lot of great art, all the material I can find that actually does some justice to those events is too painful to recommend in a slot called "survival tips." It just hurts. There is also a lot of material that is just plain awful. A further problem is that once you think about 9/11 for a while, positive thoughts grow close to impossible. I considered something totally escapist (I found a few good Muppets clips). I also thought about offering up some of the Saturday Night Live sketches from the time; it was their finest hour and they produced a lot of great comedy. I also considered various requiem masses. But if you have 9/11 on your mind, it's probably best to try to deal with it more directly. So, the musical piece on mortality that I have offered before but which comes closest to capturing how I feel about that day is Arvo Part's Cantus in Memoriam Benjamin Britten. And for a reminder of the beauty of the human spirit, and of the possibilities to transcend the ugly world ushered in by the terrorist attacks of 20 years ago, I can't think of anything better than sitting down to listen to Bach's Mass in B Minor. Have a good weekend everyone. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment