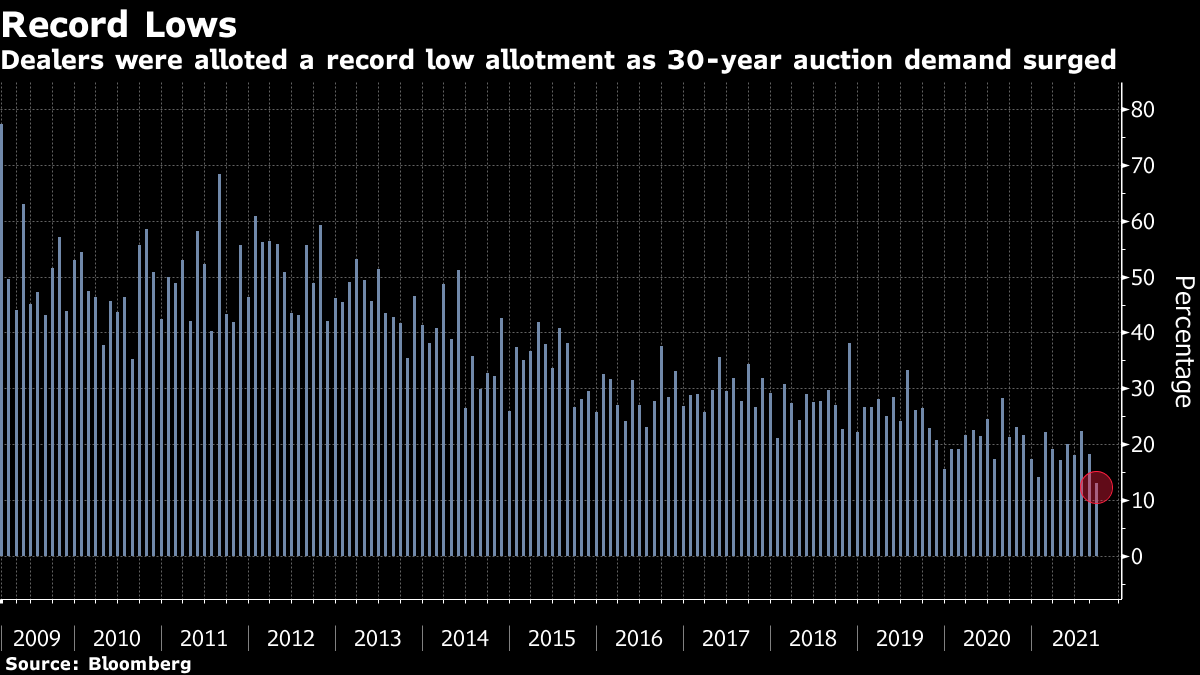

| Welcome to The Weekly Fix, where demand for blue-chip bonds is always insatiable. I'm cross-asset reporter Katie Greifeld. If there's a single takeaway from this week, it's that investors really, really want bonds right now. Luckily, they had plenty to pick from: in the span of 72 hours, 52 separate investment-grade credit deals hit the market. While the week after Labor Day tends to be busy, those three sessions rank among the busiest of all time. Wednesday's slate of sales saw order books three times covered on average, while deal execution has been orderly overall. Not to mention, IG spreads barely budged at all this week.  "Buyers have not been scared at all. We have not seen spreads back up or any deals struggle to get done," Matt Brill, head of U.S. investment-grade credit at Invesco Ltd., told Bloomberg's Jack Pitcher. "Us investors are saying 'Hey, keeping bringing more. We're not getting enough bonds." It was a similar story on the government debt side as the U.S. Treasury auctioned $120 billion worth of 3-, 10- and 30-year securities this week. All three sales stopped through, but Thursday's $24 billion 30-year offering was the real show-stopper. Not only did the sale draw a yield 2 basis points below the when-issued rate, but dealers -- who are obligated to bid -- were allotted just 13.1%, a historic low.  Taken together, all those superlatives point to insatiable demand for bonds, says Richard Bernstein Advisors's Michael Contopoulos. There is so much money out there and balance sheets are so strong and continue to improve, I think there is little at the moment that will upset the apple cart for credit. With regard to Treasuries, it's a similar story with regard to so much cash. Then throw in a payroll miss, the narrative of peak everything, and low global yields, and Treasuries at local highs seems to have made sense for a large cohort of investors.

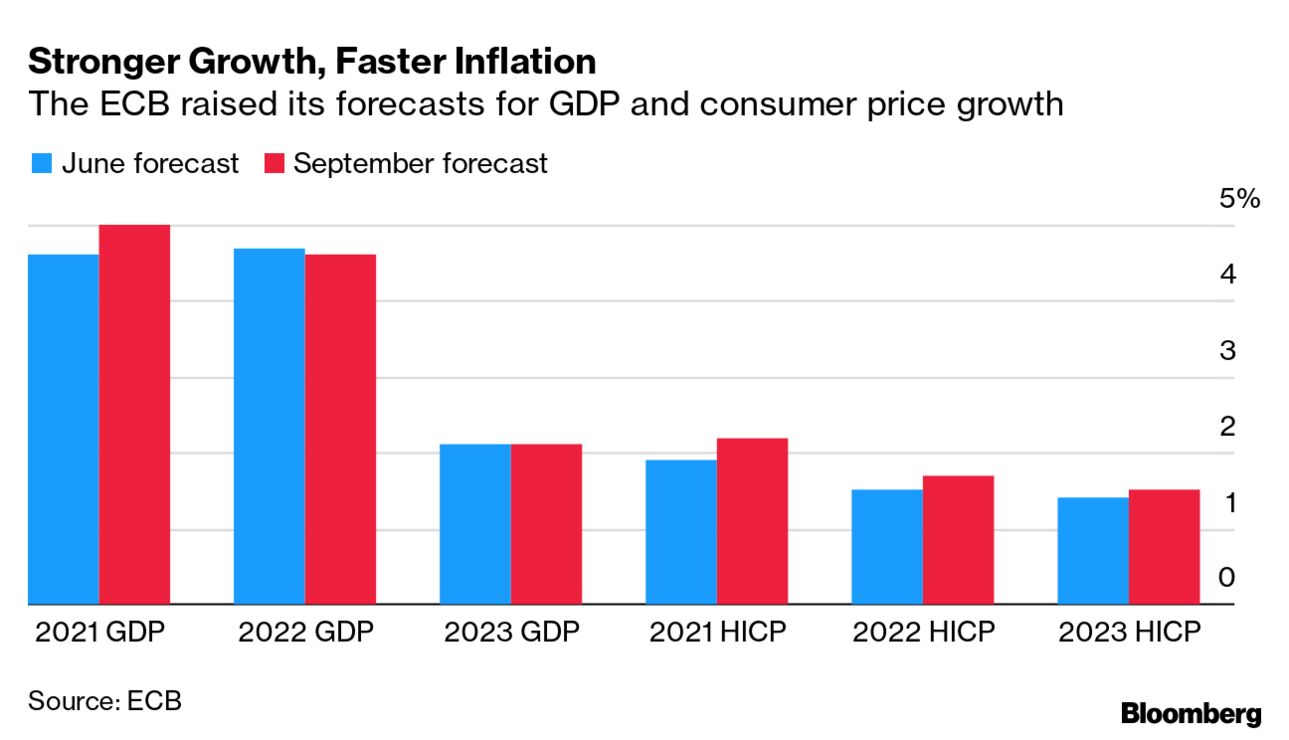

At the European Central Bank meeting Thursday, policy makers pledged to slow the pace of pandemic bond-buying in the final quarter of 2021, in a move that President Christine Lagarde insists is not tapering. "The lady isn't tapering," she told reporters in Frankfurt, which multiple colleagues have told me is a nod to Margaret Thatcher. Rather, the ECB's decision is "a recalibration of the pandemic emergency purchase program for the next three months." Alright, fine. That stirred some predictable snark on Twitter, with Janney Montgomery Scott's Guy LeBas quipping "Tapering is not tightening, and recalibrating is not tapering. Apparently. @ecb" Bespoke Investment Group's George Pearkes largely shared that sentiment, tweeting "If a central bank reduces accommodation while upgrading inflation forecasts, what exactly do we call that."  I followed up with Pearkes, who noted that yield curves flattened "like a banshee" all day Thursday. Sure enough, 10- and 30-year bund yields both dropped by about 3 basis points. Still, Invesco chief market strategist Kristina Hooper made the point on Bloomberg's " QuickTake Stock" that the while 'recalibration' could be taken as an extreme example of central-banker speak, it highlights how the ECB approaches quantitative easing: We can quibble over terms, I think they want to call it an adjustment, and I think it's probably fair to describe it that way. At least the way the ECB interprets asset purchases, it thinks of it more as a dial. So that this is some kind of recalibration, it can always be dialed up again. Whereas the Fed tends to take an approach that when we begin this we're looking to end it in the near future and we're not treating it as a dial.

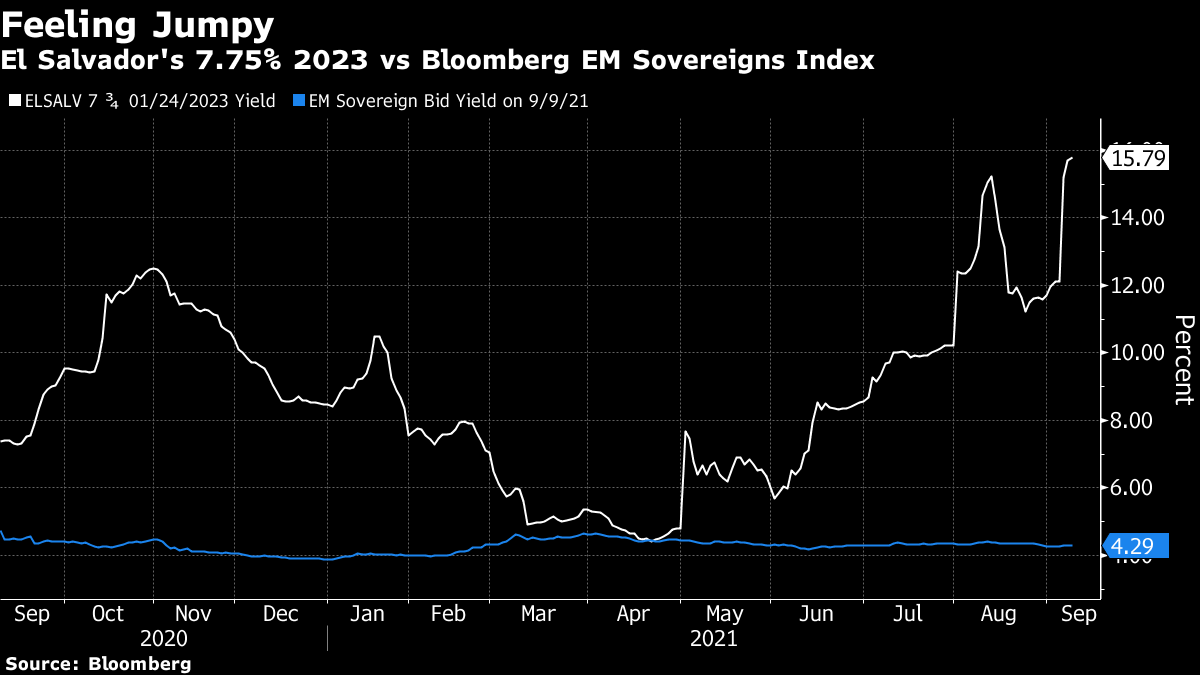

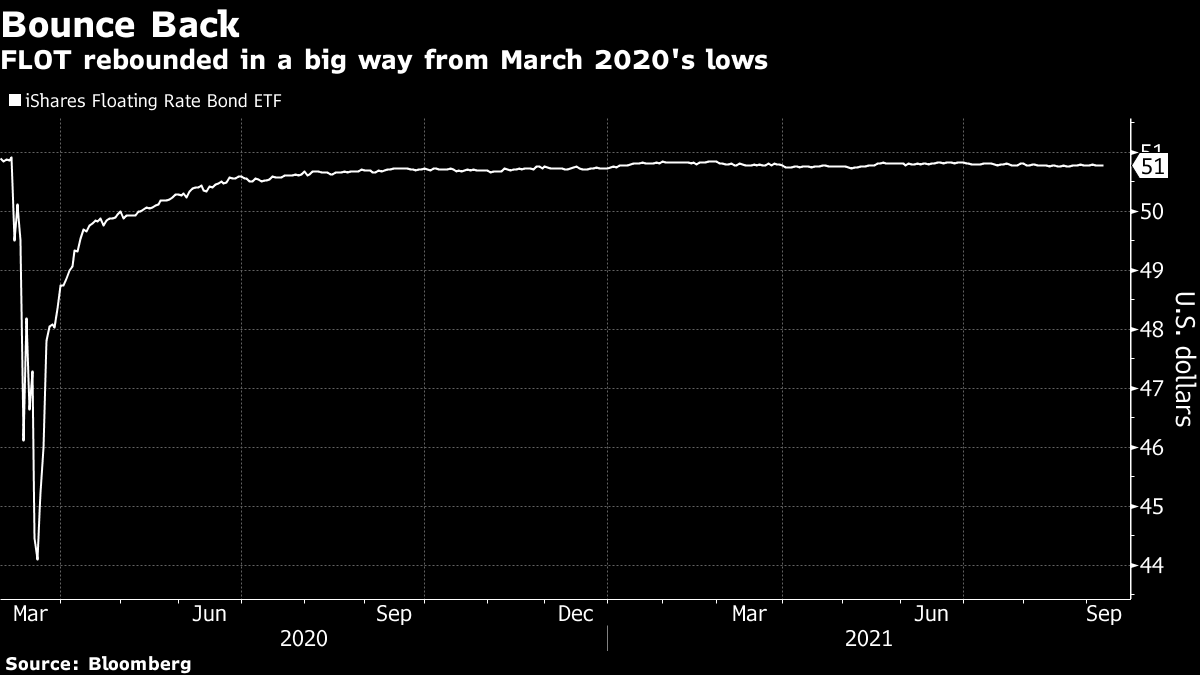

What was heralded as the biggest test ever for Bitcoin turned into a real bust for El Salvador bondholders. The nation became the first to accept the coin as legal tender on Tuesday -- a day when the price of Bitcoin plunged as much as 17% amid a glitch-riddled rollout. That's great for traders, maybe not so much for El Salvador's citizens and creditors. Bloomberg's Sebastian Boyd noted that the bid yield on the country's 7.75% bonds due 2023 spiked to a record high, while El Salvador's CDS moved to price in a 25% chance of default by March 2026. That spike inverted El Salvador's entire yield curve, a move that began in June -- when the law to adopt Bitcoin was initially passed, wrote Bloomberg's Tracy Alloway.  However, both Boyd and Alloway point out that the bond slump may have more to do with a ruling that El Salvador's sitting president -- in this case, the popular but unpredictable Nayib Bukele -- can run for a second term. Bukele has roiled the nation's debt market in the past, and this latest bout of volatility comes at a precarious time as the country neogiates with the International Monetary Fund for some much-needed support. But in the eyes of Ambrus Group co-chief investment officer Kris Sidial, the rocketing yields have more to do with debtholders fretting about Bitcoin rather than another Bukele term. "People are fearful that the currency will be too integrated with crypto and the debt could default if crypto gets hurt," Sidial said. "Realistically, foreign investors have been positive on Bukele. He seems to want to turn the country around, which is good for emerging-market investors. If I was a bond holder and Bukele did another term, I would probably be more inclined to have more bond exposure, not lighten it." It feels like everyone's a trader now, including Federal Reserve regional bank presidents. Boston Fed chief Eric Rosengren and Dallas Fed's Robert Kaplan came under fire this week after annual disclosures filed last month showed the pair engaged in active trading across a range of asset classes and investment vehicles. The disclosures showed that Rosengren -- who has warned repeatedly about overheating risks in the U.S. real estate market -- held stakes in four separate real estate investment trusts. He also bought and sold shares of Annaly Capital Management Inc., a REIT that holds agency mortgage-backed securities. The Fed currently buys $40 billion of this type of debt each month. Meanwhile, current Dallas Fed chief and former senior Goldman Sachs Group executive Kaplan made multiple $1 million-plus trades in 2020 as the economy and financial markets convulsed under the weight of a rapidly spreading pandemic. Those transactions touched dozens of companies, including Delta Airlines, Alphabet's Google and Verizon Communications -- some of the stocks at the epicenter of the stay-at-home versus economic-reopening trades that dominated the equity market.  Kaplan's disclosure also showed that he bought and sold shares of the iShares Floating Rate Bond ETF. The fund tracks debt maturing in five years or less -- securities that are directly influenced by the central bank's adjustments to the Fed funds rate. The Fed's ultra-accomodative monetary policy has faced fierce criticism from certain quarters for elevating asset prices over the past eighteen months, disproportionately benefiting wealthier Americans. By late Thursday, both Rosengren and Kaplan said that they would sell their individual stock holdings by Sept. 30, and cycle the proceeds into diversified index funds or cash. Both also pledged to not trade stocks for the duration of their tenures as reserve bank presidents. But to some, it's too late. "Doing things like this, although not prohibited by the rules, shows poor judgment and really hurts the reputation of the Fed," Roberto Perli, a partner at Cornerstone Macro LLC and a former Fed economist, told Bloomberg News. While it's positive that Kaplan and Rosengren said they'd cease trading in their roles, "The damage to the institution is done." Wall Street Lends Corporate America ESG Credibility for 0.01% BofA's Subramanian Likens S&P 500 to 36-Year, Zero-Coupon Bond Wealthy Black Homes Still Suffer Segregation, Fed Study Says |

Post a Comment