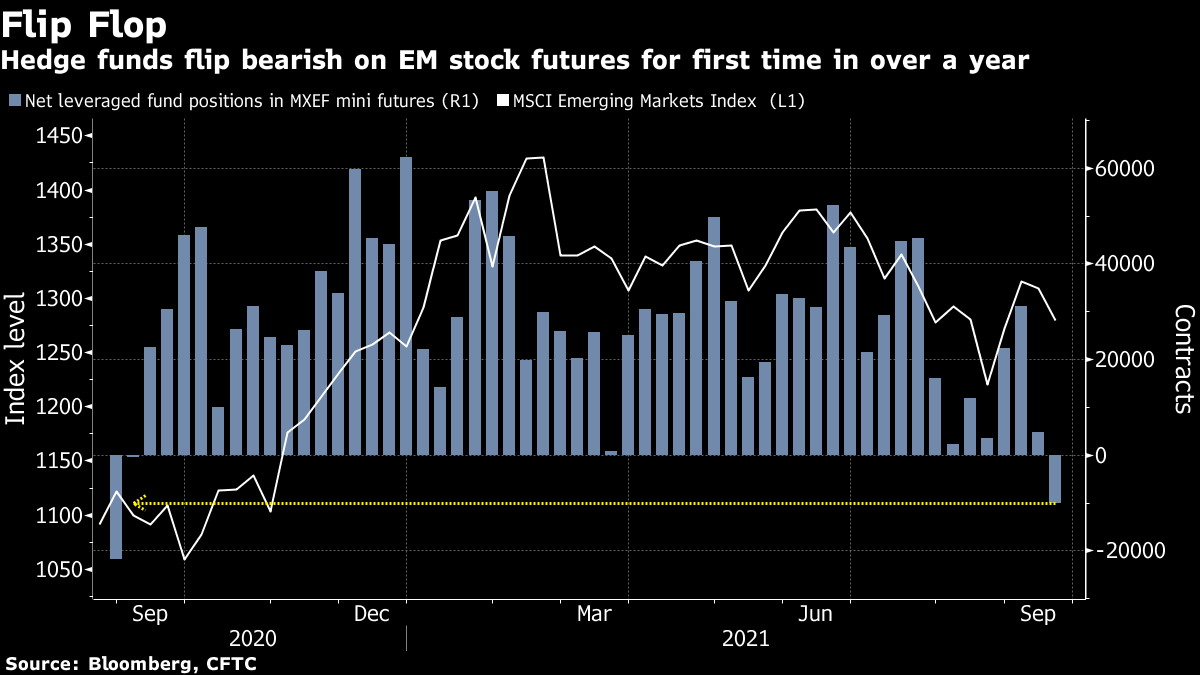

| Good morning. A more hawkish Fed stance, more rate decisions and a worsening energy crisis. Here's what's moving markets. Federal Reserve Chair Jerome Powell said the U.S. central bank could begin scaling back asset purchases in November and complete the process by mid-2022. Officials revealed a growing inclination to raise interest rates next year. Powell, explaining the U.S. central bank's first steps toward withdrawing emergency pandemic support for the economy, told reporters Wednesday that tapering "could come as soon as the next meeting." That would be on Nov. 2-3. The Fed also raised its 2022 inflation outlook to 2.2% from 2.1%. You thought the Fed, BOJ and Riksbank were enough for a week? The marathon continues today with rate decisions in the U.K., Switzerland, South Africa, Turkey and Norway. The latter is expected to actually raise rates this morning, and to confirm another hike for December, followed by more increases next year. It'll be the first such post-pandemic tightening among nations with the world's 10 most-traded currencies. No change to rates or asset purchases is expected from the Bank of England, though at least one monetary policy committee member is likely to vote for an early end to asset purchases.  | mRNA-based vaccines like Pfizer-BioNTech and Moderna's are likely to come in three-shot regimens in the future, the U.S.'s Anthony Fauci said, just before the country's regulators authorized a third Pfizer shot for people 65 and over. Europe's already embarked on a booster vaccine effort, with Britain declaring it'll offer such shots for over-50s and similar offerings underway in countries including Germany and Italy. The wave of failing British energy suppliers is starting to arrive in people's radiators. More than 1.5 million U.K. households are being forced to switch energy suppliers after two more retailers collapsed on Wednesday, bringing the tally of companies going out of business to seven since early August. Companies have been asking for the price cap on default tariffs to be lifted to allow them to shift some of the pain onto consumers, but the government has stated that this won't happen. Instead, state-backed loans are being considered to help ease costs for larger firms to take on the customers of failed companies. European futures are up after Asian markets edged higher with worries about China Evergrande Group somewhat abating. There's little earnings except for Brit midcaps Playtech, CVS Group and Harbour Energy. South Africa's Investec is set to post a trading update while in the U.S., Nike, Accenture and Costco are reporting. Apart from all the rate decisions, macro highlights include flash purchasing managers' index (PMI) data for the Eurozone, the U.K. and U.S. Major candidates for Germany's upcoming election face off in a final TV debate tonight. Angela Merkel's designated successor Armin Laschet will be under pressure to perform, after floundering in past debates and amid dismal poll numbers just three days before the vote. This is what's caught our eye over the past 24 hours. The rising wall of worry in global markets -- from the Evergrande debt crisis to the Fed's plans for tapering -- seems almost specifically designed to target emerging-market stocks and investors are reacting accordingly. Hedge funds are growing increasingly bearish with leveraged fund positions on futures linked to the MSCI Emerging Markets Index flipping net short for the first time in more than a year, according to the latest data from the Commodity Futures Trading Commission. And data from Bank of America this week showed long-only funds have been reducing their active exposure to EM all year, with recent outflows concentrated in China. Investors have legitimate fears about the impact a restructuring of a firm with about 2 trillion yuan in assets -- equivalent to 2% of China's gross domestic product -- would have on the world's second-largest economy, which is already slowing. They also remember the 2013 tantrum, when the EM stocks gauge fell 14% in the month after then-Fed Chair Ben Bernanke's taper comments. Before this week's volatility, the index had underperformed its developed-markets peer by about 16 percentage points so far in 2021. That's a lot to claw back with just over three months left in the year.  Cormac Mullen is a cross-asset reporter and editor for Bloomberg News in Tokyo. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment