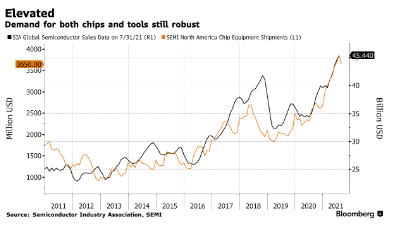

| Hello. Today we look at the economic fallout from Evergrande's financial woes, the costs and benefits of the global chip shortage and uneven job creation in the U.K. Because of its huge debt pile of more than $300 billion, the cash crunch at China Evergrande Group is often presented as a financial story. With dire "Lehman moment" scenarios unlikely because of Beijing's enormous influence over credit markets, the more lasting significance may actually be economic. That's because authorities' willingness to flirt with a messy cash crunch shows Beijing is more convinced than ever about shifting away from reliance on real estate development for growth. China's leaders are signaling that they want both house price growth and new construction to remain roughly flat in the years to come. That would be a huge shift for China, and the world. The expansion of China's real estate sector has outpaced total GDP growth for decades, meaning the sector's share of the economy has steadily risen to reach about 15% of annual output. Countries such as Australia, Brazil, and Zambia depend on its relentless demand for steel, copper, and other construction materials. The stable real estate sector which Beijing is targeting will be a drag on China's demand growth, rather than a driver. Beijing hasn't given up on real estate entirely — it still wants about 10 million people to move to cities each year through to 2025. But officials want to steer more economic resources toward areas it views as central to national security—above all, high-tech manufacturing that can help it reduce its reliance on the U.S. and its allies. The party is also emphasizing financial stability and reducing emissions rather than just the pace of economic growth. That shift pre-dated the pandemic. Chinese cities introduced tough curbs on housing purchases from 2017, which stabilized property prices in the biggest cities. But it was accelerated by China's brush with the coronavirus. Policy makers were alarmed when prices started spiking again due to looser monetary policy it introduced during the pandemic, and decided to clamp down more tightly than before. Beijing has mainly acted by using its leverage over the financial system: It ordered developers including Evergrande to cut their debt piles, and banks to slow the pace of mortgage lending and channel loans towards manufacturing instead. Those policies helped push Evergrande, which has been financially stretched for years, toward a cash crunch. Evergrande has 1.4 million customers waiting for homes. But it only accounts for about 4% of China's property sales per year. The world economy will feel a bigger impact if Beijing continues its tough campaign to slow growth in the real estate market, hitting consumer sentiment and demand for commodities. The strain is already visible in China's economic data and the price of iron ore. For now, policy makers seem willing to inflict economic pain to alter expectations that real estate prices will always rise. So even if it's not China's "Lehman moment," it's still huge news for the global economy. Click here to read the full story. —Tom Hancock The cost of the intractable semiconductor shortage has ballooned by more than 90%, pushing the total hit to 2021 revenue for the world's automakers to $210 billion. That's the latest dire forecast from AlixPartners, which predicted global automakers will build 7.7 million fewer vehicles due to the chip crisis this year. It's nearly double the consultant's previous estimate of 3.9 million in lost production. Despite ongoing efforts to shore up the supply chain, semiconductor availability has worsened as automakers exhaust stockpiles and other industries have no more to spare. And the year-long boom in global semiconductor demand that has supported key Asian exporters still has room to run, according to a set of indicators tracking the industry. The economies of South Korea and Taiwan, both major chipmakers, have held up better than many others during the pandemic thanks to surging purchases of tech products. An extension of the uptrend would provide a further fillip to their recovery. Click on the links to read any of the stories in full: - Central bank diary | Another day of central bank decisions has already seen Norway become the first developed economy to raise its key interest rate post-pandemic and Switzerland stick with ultra-low rates. Philippines held steady too as did Taiwan, which tightened selective credit control measures. Coming up: Turkey, the U.K. and South Africa.

- Taper timing | Federal Reserve Chair Jerome Powell said the U.S. central bank could begin scaling back asset purchases in November and complete the process by mid-2022, after officials revealed a growing inclination to raise interest rates next year.

- Data disappoints | Business activity in the euro area "markedly" lost momentum in September, while early data suggested South Korea's exports will slow. In the U.K., a survey showed the private sector had its weakest month since the height of the winter lockdown and inflation pressures escalated.

- Chip demand | A year-long boom in global semiconductor demand that has supported key Asian exporters still has room to run, according to a set of indicators tracking the industry.

- Dubai Inc. | What may have been the steepest population decline in the Gulf is giving way to the hottest jobs market Dubai has seen since China detected its first coronavirus case in December 2019

- Minorities lagging | Local unemployment rates by race and ethnicity for 15 major U.S. metro areas show a slow recovery and still painful economic reality for minority groups.

- Vote MMT? | Australian economist Steve Keen plans to run for parliament in next year's election, campaigning for a reshaping of the economy that would be financed through Modern Monetary Theory.

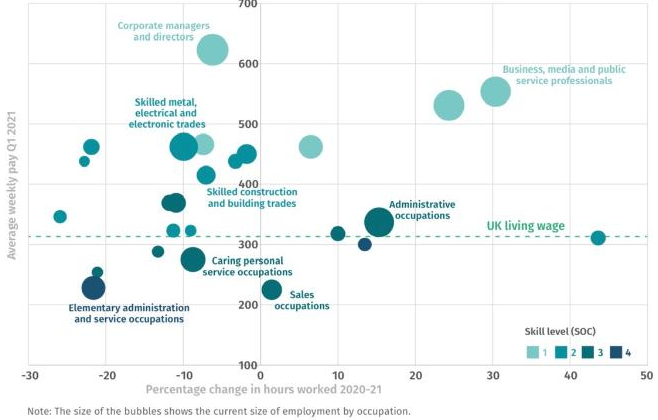

Change of employment between Q1 202 and March-May 2021. Source: IPPR analysis of Office for National Statistics data U.K. job creation was concentrated in high-skilled, high-pay roles during much of the pandemic, while job destruction occurred mostly among low-paid, low-skilled roles. That's according to a report published Wednesday by the Institute for Public Policy Research. Noting that the decline in employment has been unevenly spread across sectors, the research group warned that most people who lost their jobs during the crisis are likely to lack the skills and training required to be hired in a the newly created role. Powell's approach to bed time: Read more reactions on Twitter - Click here for more economic stories

- Tune into the Stephanomics podcast

- Subscribe here for our daily Supply Lines newsletter, here for our weekly Beyond Brexit newsletter

- Follow us @economics

The fourth annual Bloomberg New Economy Forum will convene the world's most influential leaders in Singapore on Nov. 16-19 to mobilize behind the effort to build a sustainable and inclusive global economy. Learn more here.

Delta Spread, Inflation Fear, Fed Taper — Bloomberg Economics Outlook Webinar: Join Stephanie Flanders, Head of Bloomberg Economics, at 10:00 Eastern Time TODAY, as she leads a discussion with Bill Dudley, David Wilcox, Tom Orlik, and Dan Hanson on the outlook for 2022. Sign up here.

Bloomberg New Economy Conversations — Getting to Net Zero: The cost of scaling up renewable energy has fallen dramatically. Is 2021 the year in which we'll see major investments in areas like green hydrogen, carbon capture and other technologies needed to prevent environmental catastrophe? What are the most promising new areas and who is at the forefront? Join New Economy Editorial Director Andrew Browne on Sept. 28 at 10 a.m. as he discusses these issues with HSBC Group Chief Executive Noel Quinn, Hyundai Motor Co. Vice President of New Energy Business Development Jae-Hyuk Oh, and others. Register here. |

Post a Comment