Karma ConundrumThere is still no way to avoid the great bond market conundrum. Why do yields continue to fall, along with inflation breakevens, on the back of U.S. consumer price numbers that are the highest in decades? Yes, there's a good chance that inflation will prove transitory, for reasons I went through exhaustively earlier this week, and on many other occasions before that. But for now, inflation is a fact, and there are plenty of economists and analysts who expect it to establish itself. Why is the bond market growing more confident that inflation will be avoided?

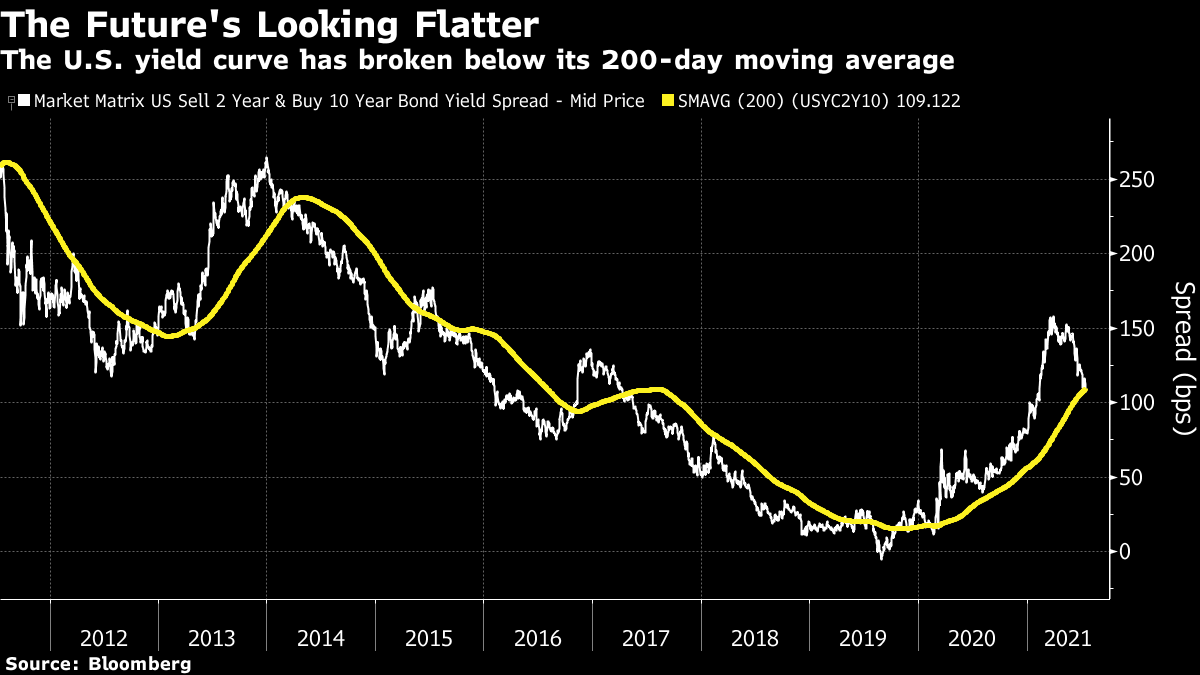

The decline persists, with the 10-year bond yield now below 1.3%. Meanwhile, the spread between two- and 10-year yields, arguably the clearest bond market judgment on the prospects for reflation, is back down to 106 basis points, having canceled out its rise since February and fallen below its 200-day moving average. As this chart of the yield curve shows, this rarely happens unless there is a clear flattening trend, and is a remarkable outcome when inflation is rising:

There are any number of good technical reasons why people might have bought bonds recently, which I have covered. What fundamental reasons might there be for shifting your money to bet on deflation? Louis Gave of Gavekal, who freely admits that (like me) he had expected yields to keep rising, offered this summary of the most plausible three reasons: - The first is fears that the spread of the Covid delta variant will postpone a full reopening of the global economy.

- The second is the perception that policy in the US may actually turn less dovish, and at an earlier date, than initially thought. After all, President Joe Biden has scaled back his infrastructure plans from US$2.2 trillion to less than US$1.2 trillion being spent over a longer period, while the Federal Reserve has begun to sound less dovish (with fears that the Jackson Hole confab for central bankers in August could signal a more hawkish shift).

- The third reason is a fear that China's attempts to cool down its economy could have a deflationary impact on the world. The last of these seems to offer the best explanation of recent market behavior.

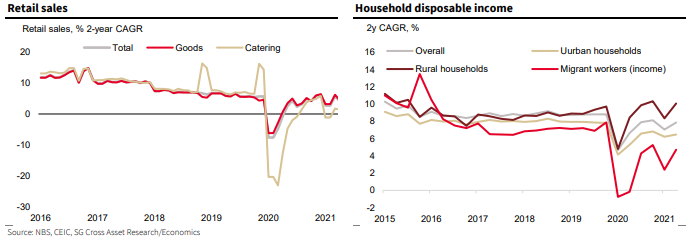

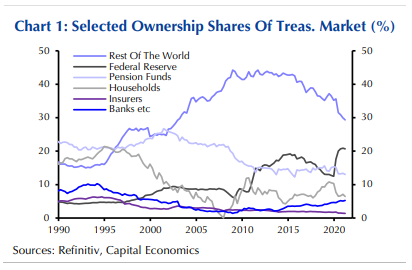

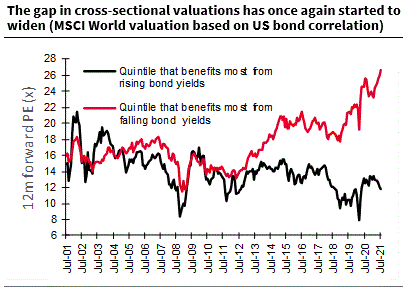

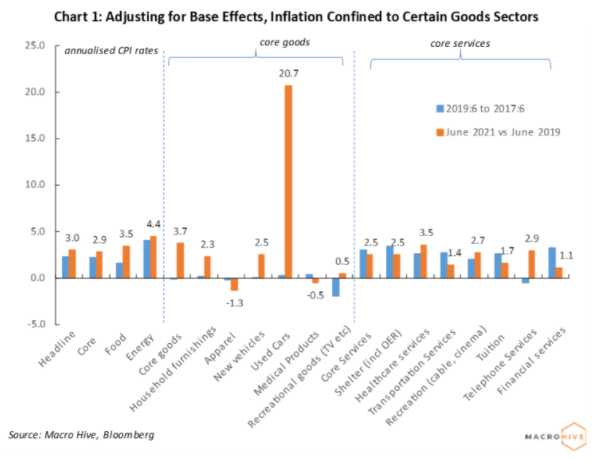

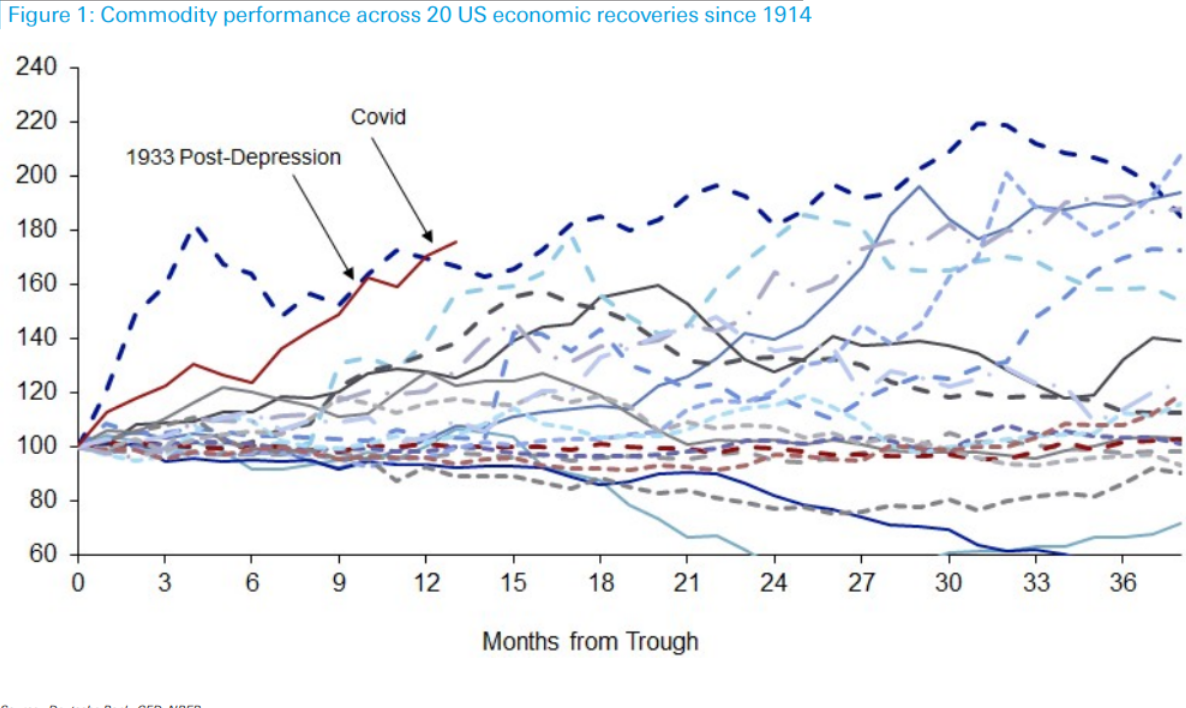

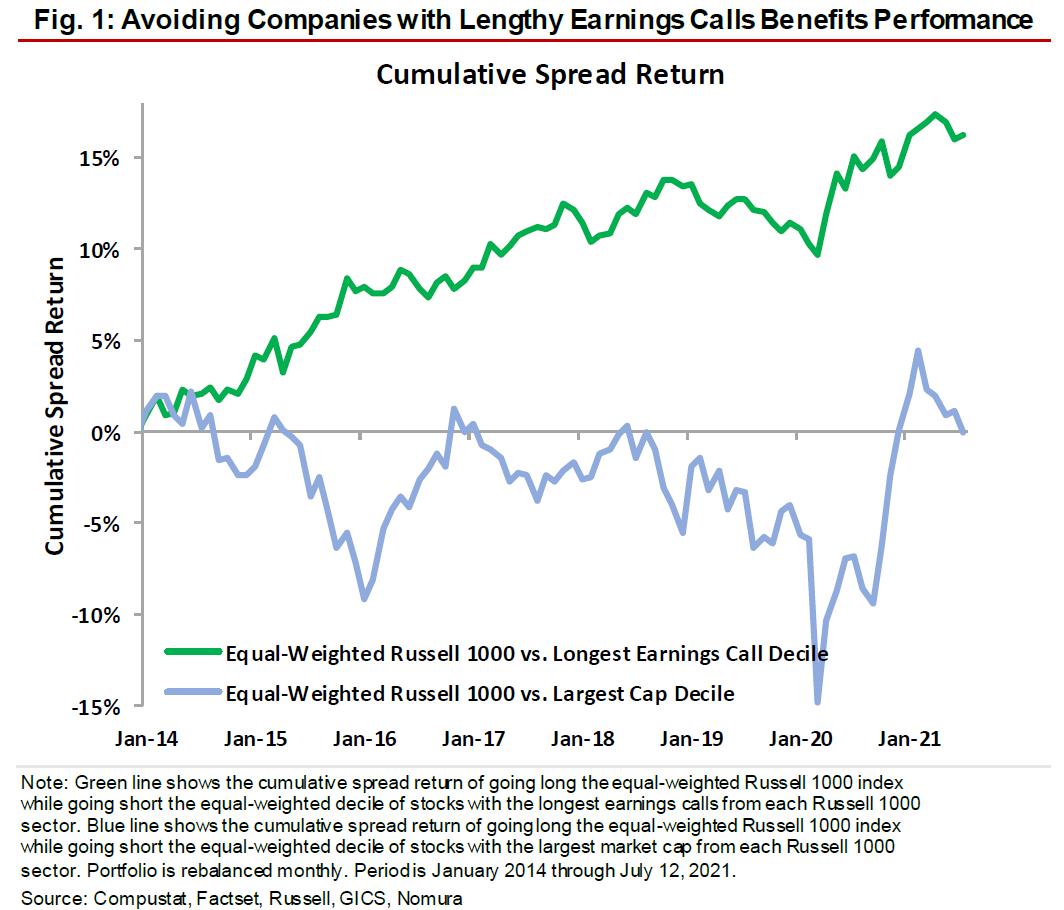

The second is important. The Georgia senatorial elections in the first week of January sparked a big move forward in the "reflation trade" as they opened the chance of more expansive U.S. fiscal policy. Now, with the Biden honeymoon over, markets may be over-compensating. Big presidential initiatives in their first year tend to go down to the wire — just look at the Trump tax cut, which appeared dead in the summer of 2017, or Obamacare eight years earlier. As for the delta variant, while it should alarm all of us, it's not clear that it would be enough to have some of the macroeconomic effects we are seeing at present. As Gave points out, it might lead to a weaker dollar (which is what happened with the first wave of Covid), and yet the dollar is rallying. It might also exacerbate supply disruptions and make inflation worse. Instead, he was probably right in singling out China for most attention. Last week's cut in banks' required reserve ratios, as I noted earlier this week, is the kind of thing that only happens if the authorities are worried about the economy. And we now have more Chinese data. Retail sales are up 12.1% year on year, and perhaps more importantly have risen at an annualized rate of only 5.32% over the two years since June 2019. GDP growth is 7.9%; over the last two years, the annualized rate is slightly higher, at 8.2%. If we look at the data on a two-year basis, to try to cancel out the extraordinary happenings since the beginning of last year, we get a picture of a China growing a tad disappointingly, but not obviously in the kind of trouble that would justify tumbling Treasury yields. Here, Societe Generale SA shows retail spending and household incomes on a two-year basis:  Overall, this suggests a gradual slowing in the pace of growth, after pandemic effects are excised, which is problematic for the notion of a grand reflation trade, but also does little to justify an all-out bet on deflation and Japanification. As for the influence of Chinese (or other foreign) buying on Treasuries, it is much less important than in the "conundrum" era, when it was popular to blame a Chinese "saving glut" for low yields. As this chart from Capital Economics Ltd. shows, that no longer holds:  One other interesting point demonstrates that the decline in bond yields isn't just some technical quirk. The equity market is also positioning in exactly the way you would expect if it was bracing for a sustained period of low yields. On a global basis, and not just in the U.S., valuations are increasing for stocks that benefit most from falling bond yields, and decreasing for those that perform best when yields are rising. The following chart is from Andrew Lapthorne, chief quantitative strategist at SocGen:  It looks as though markets, both in stocks and bonds, are being traded by people who truly believe that this bout of inflation will prove transitory, and that there is a danger of deflationary ennui once it's over. Time alone will tell if they are right; for now, the conundrum remains unsolved. The Two-Year ItchA number of readers suggest that the fairest way to deal with the transitory effects of inflation is to look at the annualized rate over the last two years. That makes sense but still doesn't resolve the issue, in my opinion. This chart is by Bilal Hafeez of Macro Hive:  On this basis, headline and core inflation are at 3% and 2.9% respectively. This is nothing terrifying, but is at the top of the Fed's level of tolerance. If a broader economic reflation lies in our future, these numbers are consistent with a problem at some point. But they certainly don't prove that any such thing will happen. Meanwhile, the chart also illustrates that the pandemic is still having possibly deflationary effects. Services inflation is slightly down compared to the two years from 2017 to 2019. Recreation inflation is falling, and must be likely to increase if people really start spending. Shelter inflation over the last two years has run at 2.5%; that is where the attention will increasingly focus over the next few months. In short, this exercise plainly removes the shock value of the big headline increases. It still leaves us with an inflation picture that doesn't fit with falling bond yields and a flattening yield curve. CommoditiesWhat should be made of the rise in commodity prices, and its deceleration in recent weeks? There is a great optimism that the retreat for some commodities, notably lumber futures, shows that inflationary pressure is reducing. There is also the possibility that higher commodity prices will themselves be deflationary, as money spent on basic necessities displaces other spending. That's a reasonable hope, but the following chart, in which Deutsche Bank AG's Jim Reid charted the performance of the Thomson Reuters CRB CoreCommodities index over every economic recovery going back to 1914, suggests that it is premature to sound the all-clear. Commodities are further ahead on this basis than at 12 months into any previous recovery, and have overtaken their 1933 rebound amid the Great Depression. That 1933 rally carried on for another couple of years. This rally is considerably greater than any other at this stage in an economic recovery.:  As with so many things in the post-pandemic world, it's hard to know which precedents to use, and whether any are valid. This was an abnormally sharp shutdown, followed by an abnormally sharp bounce back. It's reasonable to think that the effect on the commodity market could be similar. That said, the Covid shutdown came as most commodities had endured almost a decade in a bear market. It's just as easy to hypothesize that Covid provided the cathartic selloff that creates an investable bottom, and then an enduring recovery. It will take a while for us to find out, but it's premature to take the commodity market as an argument to believe the inflation threat is merely transitory. Keep It Snappy, StupidThere is a famous anecdote that Winston Churchill once had to apologize to his tutor that he hadn't had time to write a short essay. Saying things concisely is difficult and takes time and preparation. It's also worth the effort. If you have a good story, any advertiser or public speaking consultant will tell you that you need to be able to convey it snappily. The more you have to explain yourself, the weaker your story appears. It's always great when machine learning and big data crunching confirms basic common-sense intuitions like this. And thanks to Nomura Instinet, we can say that it does. Nomura quantitative strategist Joseph Mezrich, let loose on a trove of corporate earnings call transcripts, tested for a simple variable: How did the length of a call affect subsequent performance? The result was emphatic. Over the last seven years, the average stock outperformed the 10% of companies whose earnings calls dragged on the longest by a cumulative 15%:  One explanation can be dismissed. Bigger and more complicated companies will naturally have more to discuss. Jack Welch's earnings calls at General Electric Co. used to go on for a while even though the company was doing excellently. But over the same period, the average stock did exactly as well as the largest 10% of stocks by market cap. Mezrich's advice: A relatively long earnings call may simply indicate that a company has much to explain. However, that could be a sign of trouble. In any case, be cautious with verbose companies.

Put another way, the next time you find yourself drumming your fingers with frustration as an earnings call drags on, and you feel like just selling the stock, that may not be such a bad idea. Survival tipsData isn't the Plural of Anecdote, they say, but if you'd like evidence that the pandemic is still having directly deflationary effects on some parts of the economy, I have some. A few weeks ago, I bought a Pinstripe Pass to see the Boston Red Sox play the New York Yankees at Yankee Stadium on June 5. Tickets were $60 each (plus extortionate Ticketmaster charges), we had a great time, and the Red Sox won. So we decided to buy Pinstripe Passes for last night's Red Sox-Yankees game. This time the price was down to $45 (plus Ticketmaster levy). This morning, some other friends decided to come with us, and I bought more passes, at $30 each, plus levy. Then, just as I was about to leave for the game, the news came that due to an outbreak of Covid in the Yankees team, the game had been postponed. With a refund in prospect, the price just dropped to zero.

It's true that the Yankees' season has been steadily going from bad to worse (the Sox have won all six games between the two so far this season), so they may be finding it harder than usual to get bodies through the turnstile. But a 50% price cut in six weeks does suggest there's at least one sector that's still feeling the deflationary blast. And the need to postpone the game illustrates that Covid still has the ability to mess up our lives. It also injects an element of uncertainty that might make people unwilling to book ahead for sporting events.

The standard assumption is that our appetite for big public entertainments will recover in full. That certainly applies to those who root for the Red Sox and are enjoying a surprisingly good season after last year's disaster. But it's not clear that people really feel comfortable spending money on such things yet, and it's worth keeping an eye on two risks. The first is that the pandemic makes us all lastingly more conservative (which I doubt). The second is that there will be more one-off inflationary reopening pressures in future, which I think is more likely. The cost of concession stands at Yankee Stadium is as outrageous as ever; I fear the cost of tickets will recover in due course as well. Meanwhile, try watching this, this, this, and this for reminders of this friendly rivalry in its pomp. And have a great weekend everyone. (For me, it's going to be a long one; I'll be back in your inboxes on Tuesday). Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment