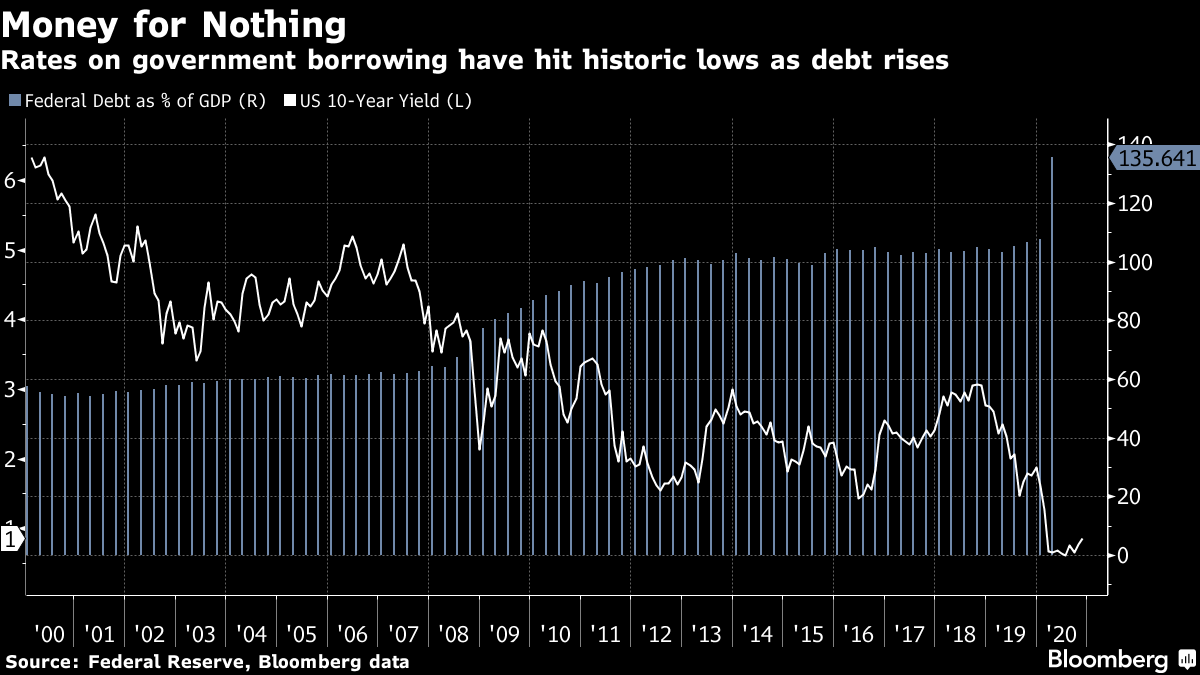

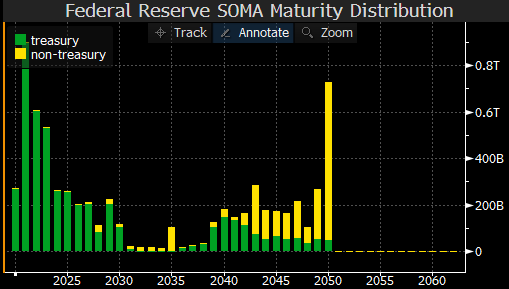

| Welcome to The Weekly Fix, the newsletter that's raising a toast to breaking glass, and giving thanks. --Emily Barrett, Asia FX/Rates Editor Madam SecretaryJanet Yellen likes to arrive early to things, according to one profile this week, as well as a Twitter mini-gallery of her poised and almost preternaturally composed in a range of settings -- including an airport and the White House Correspondents' Dinner. So it's fitting that she should be the first woman to head the Treasury, though the precedent itself is long overdue. If confirmed, Yellen will also be the first Treasury secretary to have served as chair of both the White House Council of Economic Advisers and the Federal Reserve. Her extraordinary qualifications augur a tighter coordination between fiscal and monetary policies at a critical juncture. Emergency programs terminated by the previous administration -- including the little-used and much-criticized Main Street facility aimed at lending to small businesses -- may need to be rebooted or reworked, so that relief for households and businesses stricken by the pandemic can be stepped up and better targeted. This cooperation would be akin to new dawn after several years of White House attacks on the Fed's leadership and policies. "Yellen will work well with the Fed, which could be useful in the near term in re-establishing the 13(3) facilities and potentially using them more aggressively to support mid-sized businesses and state and local governments in particular," says Julia Coronado, founder of MacroPolicy Perspectives LLC and a former Fed economist. "Her nomination not only shatters another glass ceiling, it gets the Administration's economic policy off on a solid footing." Yellen is widely heralded as a dove at a time when the world most needs them. She is best known for making a powerful case for low interest rates to create jobs, writing in a recent op-ed that "when unemployment is exceptionally high and inflation is historically low…the economy needs more fiscal spending to support hiring." The dove shorthand is tinged with irony -- Yellen presided over one of the Fed's pivotal hawkish moves, raising interest rates for the first time in a decade after the global financial crisis. (And though the lift-off was long delayed, under the Fed's revised inflation-targeting strategy it now qualifies as premature.) And at the Treasury, she'll likely be pushing an expansive economic policy as the fiscal tone turns more hawkish. A Republican-controlled Senate would turn sharp eyes back on the deficit -- which was inflated even before the pandemic by tax cuts that they'll not want to see repealed.  And borrowing to fund further relief efforts -- not to mention the Biden Administration's planned $2 trillion "Build it Back Better" infrastructure program -- probably won't be as cheap as it was under Yellen's predecessor. Treasury Secretary Steven Mnuchin was able to sell government debt at a record pace at the lowest interest rates in history, thanks to the Federal Reserve's emergency actions in cutting borrowing costs. In 2021, the prospect of a vaccine and gradual economic recovery should see the 10-year benchmark rate lift off its lows. But even if this year's 0.5% was the trough, it's unlikely to get close to levels north of 2% seen the last time an austerity battle was raging in the U.S. JPMorgan sees the benchmark peaking at 1.3% by the end of the year. As for how fast it gets there, and how much more room it has to rise, all eyes will be on the Fed, for any signs of flinching in its commitment to keep rates rock-bottom for years to come to ensure a full economic recovery. That Brings Us to the Fed...... which doesn't sound like it's on the brink of more action. Markets have been speculating about when the central bank might unveil changes to its asset purchase program, which is currently scooping up $80 billion of Treasuries and $40 billion of mortgage bonds a month. Some of the market's money has been on the Fed shifting its purchases to longer-dated securities as soon as its Dec. 16-17 meeting. That's kept alive some bets on a flatter curve -- a tough call when it hasn't held a trend for more than two weeks straight since August.  This week those positions were looking more embattled, and the gap between the two- and 10-year yields widened back out to about 70 basis points. New York Fed President John Williams wasn't stoking expectations with his comments that the central bank's existing purchases are "serving their purposes really well right now." He pointed out that fiscal policy "would be most effective in getting us through the next six months." That chimes with the just-released minutes from the Federal Reserve's Nov. 4 meeting, which suggested that the Committee wants to put some parameters around its asset purchase program -- "fairly soon" -- before it makes any changes. That probably means December's meeting will lay more groundwork, and crucially the contours of an exit strategy that could help the Fed avoid a repeat of the taper tantrum in 2013 (when then-Chair Ben Bernanke's suggestion that the Fed might soon slow its asset purchases sparked a market frenzy). The majority of FOMC members want the program to be guided by how economic conditions are shaping up. Of course last week's strange spat between the Treasury and the Fed, which means some of its emergency facilities won't be extended into the New Year, may sway policy makers to move faster on additional measures to help the economy. The minutes also reflected concern among "a few" participants that the lower odds of another big relief package mean greater risks to the economy. Nevertheless, Bloomberg Intelligence's Ira Jersey expects that skew to longer-dated purchases will happen in the first quarter of next year, as the effects of the spiking virus cases and shutdowns weigh on economic data. He and analyst Angelo Manolatos note that the Fed has bought almost $2 trillion of Treasuries since cutting interest rates to 0-0.25% on March 15, and it could buy another $1.2 trillion of long-dated bonds, even before more are issued. One other thing of note in the minutes -- the Fed isn't about to fall again into a trap of its own transparency. The minutes flagged that the central bank is overhauling its summary of economic projections -- the charts that plot policymakers' best estimates of the path of growth, inflation and the policy rate. The SEP is in for a little fuzzy-ing up, as the projections will have a new diffusion feature to reflect uncertainty -- possibly something like what the Brits do with their Monetary Policy Reports. They'll also be released alongside the policy statement, rather than with the minutes three weeks later. Vaccine Buzz

Even defining a band of uncertainty might prove pretty tricky as we look into the New Year. One of the biggest recent changes is the encouraging news from three separate vaccine trials, starting with a Pfizer/BioNtech. This highlights the importance of the Fed's exit strategy, should meaningful advances come sooner than expected to help the world return to some semblance of normalcy.

Advances in vaccine studies are coinciding with a pullback in expectations for further easing from the world's central banks, our money markets reporter observed this week. In the U.K., overnight index swaps trimmed the likely drop in interest rates by the end of next year to eight basis points from 12 prior to the Pfizer report. Markets in Wellington have gone from pricing in a move to negative interest rates, to all but erasing expectations for a rate cut by the end of next year. Both central banks appear to have cooled on their flirtation with taking rates below zero. Knowing what he knows now about these latest milestones in the pharmaceutical race, BOE's Chief Economist Andy Haldane said on Monday it's "tough to know for sure" if he would have voted for the 150-billion-pounds increase in bond buying this month. That's yet another twist for investors to consider in the leadup to the final meetings of the year in the U.K, Europe and U.S.

Bonus PointsChina's bond market poised to reshape the financial world Inside China's stunning about-face on climate policy As the pandemic rebounds, 26 million people in America say they don't have enough to eat Platypuses glow in the dark You should talk to your plants Your moment of zen -- Rockefeller the Owl is free |

Post a Comment