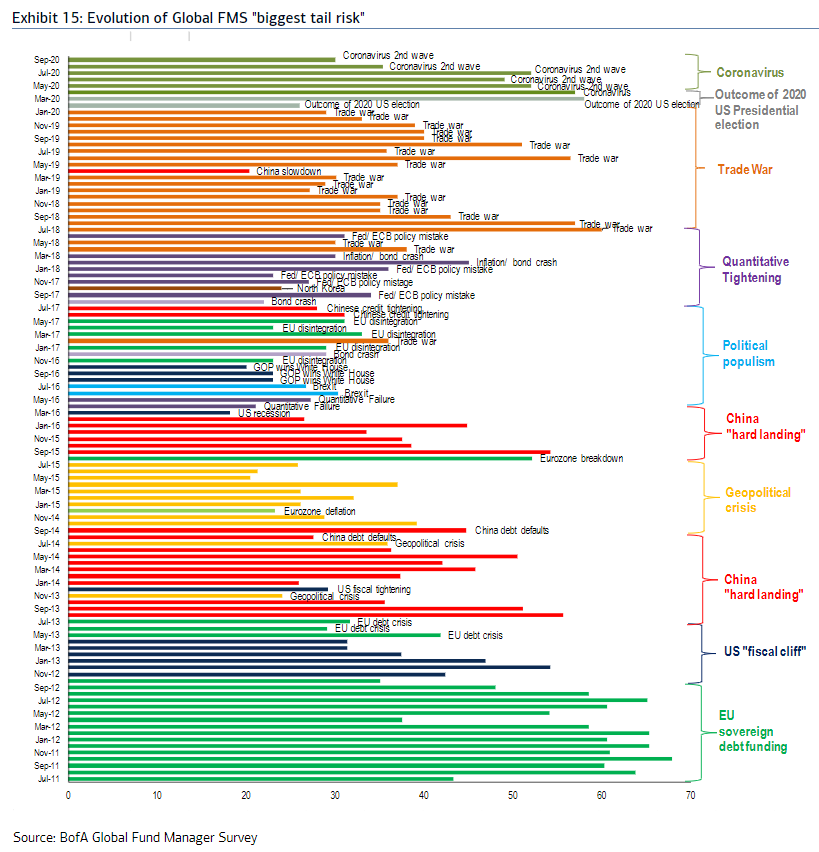

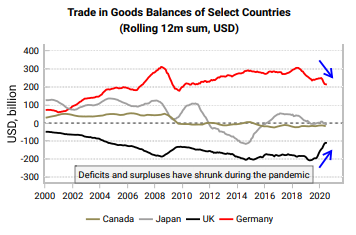

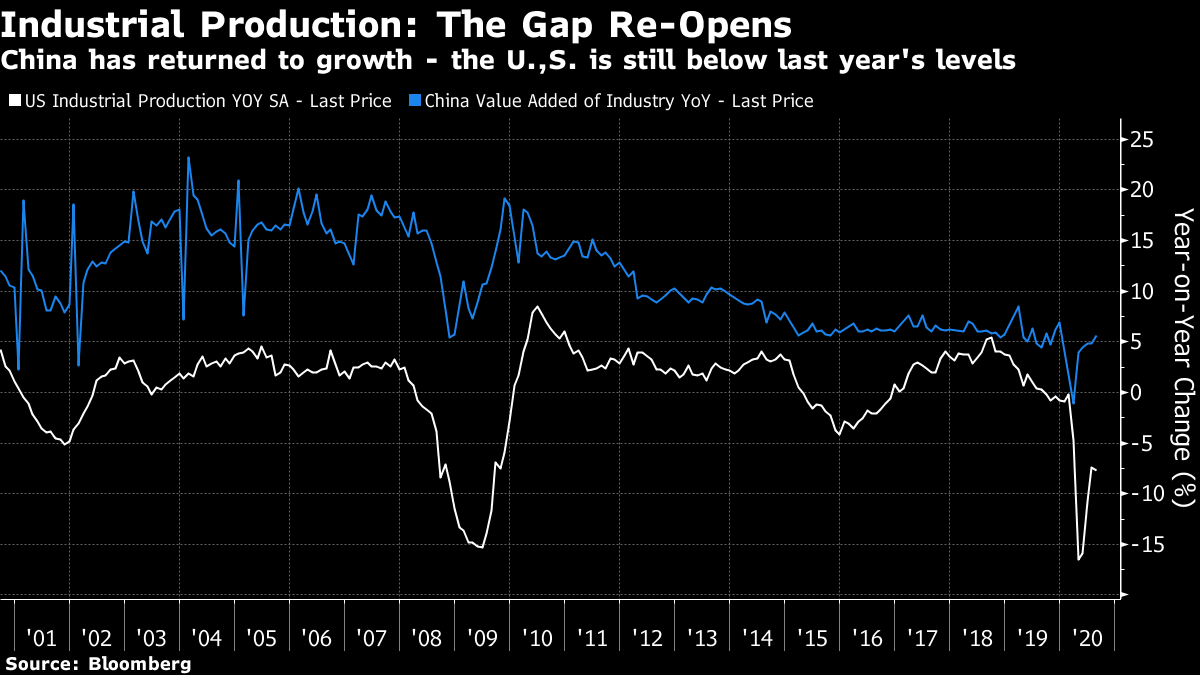

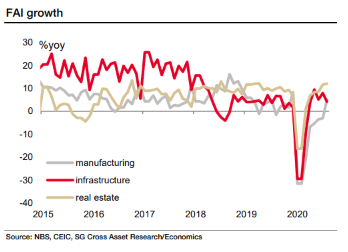

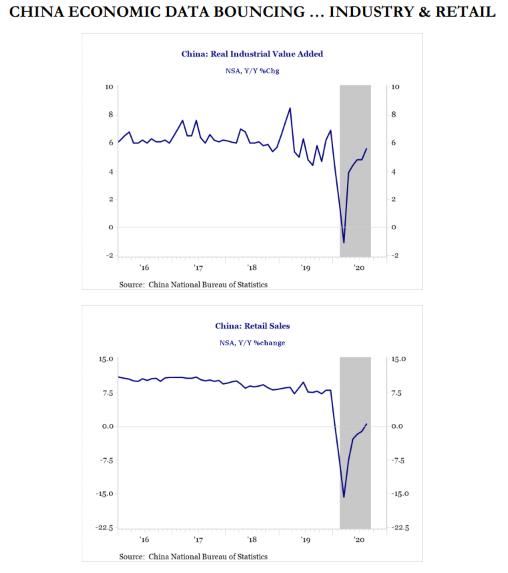

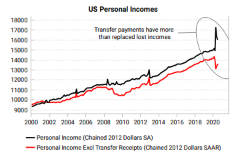

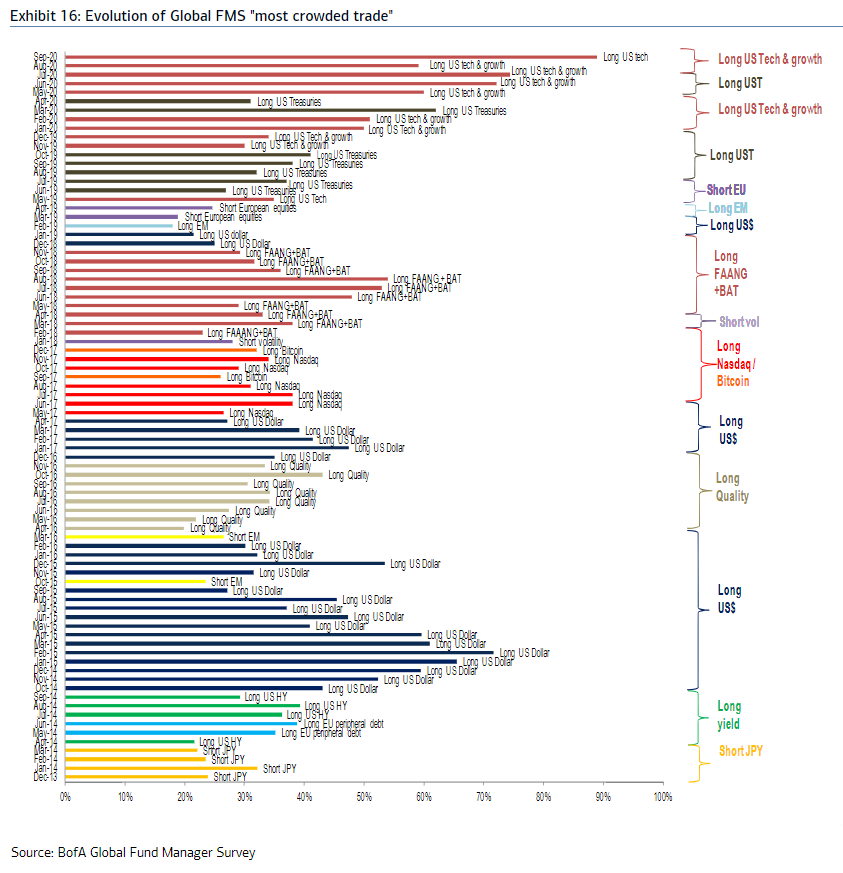

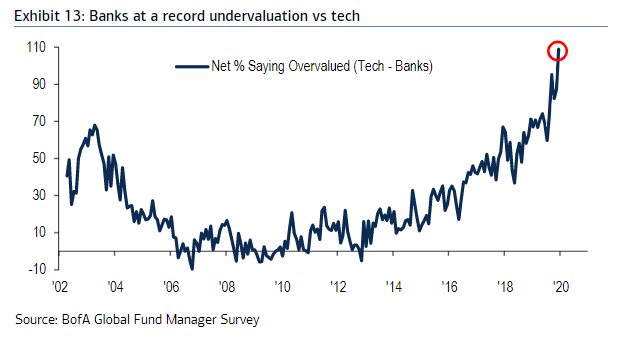

China and the U.S. It seems as though everyone has forgotten about the trade war between the U.S. and China. And that is a shame because the latest data suggest that it matters more than ever. According to the latest version of BofA Securities Inc.'s closely followed monthly survey of global fund managers, the long preoccupation with U.S.-Chinese trade has almost dropped off the list of professional investors' concerns. It now ranks only fourth, behind the coronavirus, the U.S. election, and a possible credit event. Before the pandemic struck, the trade war had been feared as the greatest tail risk for two years:  This is odd because the latest trade data suggest that the sudden stop caused by Covid-19 has intensified the imbalance between the world's two biggest economies. Generally, most countries have seen imports and exports decrease by the same percentage, which means that their balances, whether positive or negative, have tightened. This is true of Canada, Japan, the U.K. and Germany, as Variant Perception illustrates below. But China and the U.S., whose balances had narrowed slightly during the Trump era, have bucked the trend., The Chinese trade surplus is widening, and the U.S. deficit is deepening:   This has happened despite higher tariffs. Why? One clear reason, evident from this week's data, is that Chinese industrial output has now completed its recovery, while U.S. production, which normally grows more slowly in any case, is still running behind its pace from last year:  This has less to do with deliberate decisions about trade, and more to do with the consequences of decisions about how to run their internal economies. As this Societe Generale SA chart shows, China embarked on infrastructure and real estate spending to boost fixed assets, and has now brought back its manufacturing sector, which is export-driven.  Meanwhile, its attempts to rebalance the economy by stimulating greater consumer activity have taken a back seat. Retail sales growth — which tends to pull in imports — has had a much less impressive rebound (as shown in this chart from Strategas):  Meanwhile in the U.S., support for people idled by the Covid shutdown has translated into sharply higher personal incomes. Thus, for now, American policy has backed retail over industry, tending to pull in more imports, while China's policy of boosting manufacturing rather than consumers has buoyed its exports:  If Americans truly want to avoid a trade deficit with China, then, this is a problem. (It's not clear to me that the deficit as such should matter much, but evidently plenty of American politicians disagree.) The most likely way to see this change would also involve pain; if politicians cannot find a way to extend the benefits passed to aid people through the Covid slowdown, and the pandemic continues to slow activity, then there is likely to be much less consumer demand, which will feed through into lower imports. But this wouldn't be a good solution, and indeed Variant Perception suggests that it would probably lead to yet more easy money from the Federal Reserve, which would suck in yet more imports. This isn't what China was hoping to achieve. Stimulating the housing market and investment-driven spending tends to ratchet up inequality. Chinese rebalancing would mean narrowing the U.S. trade deficit. For the time being, its currency, long a flashpoint, is strengthening noticeably. Indeed it has now returned to almost exactly the level at which it was pegged against the dollar during the financial crisis era. As China has had much higher inflation over the interim, this means the yuan is now much less competitive:  For the time being, the current imbalanced state of affairs helps companies listed in China or exposed to the country. As the following chart shows, MSCI's index of the most China-exposed developed market stocks has recovered much ground against other developed market stocks in the last few months, while Chinese stocks themselves have far outperformed other emerging markets:  Absent political breakthroughs in the U.S. that allow further cushioning of the Covid blow, expect these trends to continue. It would also be extremely wise for leaders of the two countries, now more dependent on each other than ever, to thrash out some kind of a lasting trade deal. If they can't, then the tail risks look alarming, even if big fund managers are no longer worried by them. What the Smart Money Thinks…. That brings us back to the BofA Securities survey of fund managers. While big institutional investors aren't worried about U.S.-China trade at present, they are very much worried about a potential bubble in U.S. technology and growth stocks. U.S. Big Tech is named as the "most crowded trade" by the biggest majority recorded since the survey started posing the question:  Looking further into the responses, we find that a greater majority than ever before also think banks are undervalued relative to technology:  There is ample reason to believe that banks are undervalued relative to Big Tech at present, but scant evidence that large institutions are doing anything about this by loading up on cheap stocks. At least if they are doing this, they have failed to have much impact on banks' share prices. Anyone with the prescience (maybe Hindsight Capital LLC?) to place a "long NYSE Fang+ balanced with a short of the KBW banks index" trade at the beginning of the year would be sitting on a 150% profit now, even after the recent correction. (There'd be some shorting and trading costs too, but still.):  Fund managers are unlikely to abandon their bearishness about the banks until rates rise, and most believe that this will require either a coronavirus vaccine, or a return of inflation. The theory doing the rounds of investment managers that the virus has more or less burned itself out already is still far from the consensus:  That is what the smart money thinks. We will find out whether it is right. For now, one of the most interesting conclusions to draw from the survey is that Robinhooders and other retail investors may indeed have a lot to do with the extraordinary ascendancy of the FANGs. The big institutions are terrified that there is already a crowded trade; the new breed of retail traders are happily crowding in tech stocks, and probably not even wearing masks. Survival Tips The few hours before a Federal Open Market Committee meeting can often be dull, although seldom as dull as the spectacularly uninteresting trading put up by the U.S. Treasury market on Tuesday:  How to deal with the tension and the tedium? Well, you could join in with the live blog discussion on inflation that I will be having with my colleagues Laura Cooper and Kriti Gupta, and special guest Robin Brooks, chief economist of the International Institute of Finance, at 10 a.m. New York time (3 p.m. in London and 4 p.m. in Frankfurt). We will be fielding questions and holding a wide-ranging discussion. Go to TLIV on the Bloomberg terminal. With any luck it will all aid survival. If a discussion of inflation doesn't get you excited, then for American readers I can recommend Borgen, which is at last available on Netflix. A wonderful political drama centered on Denmark's fictional first female prime minister (not long before the country elected its first real one), it can perhaps be best summed up as what you would get if you crossed House of Cards with The Girl with the Dragon Tattoo. All the Danish actors have been dubbed into British English, and several have some rather strange regional accents (why can't they just get the original Danish actors, all of whom doubtless speak perfect English, to dub it?) . But that only adds to the fun. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment