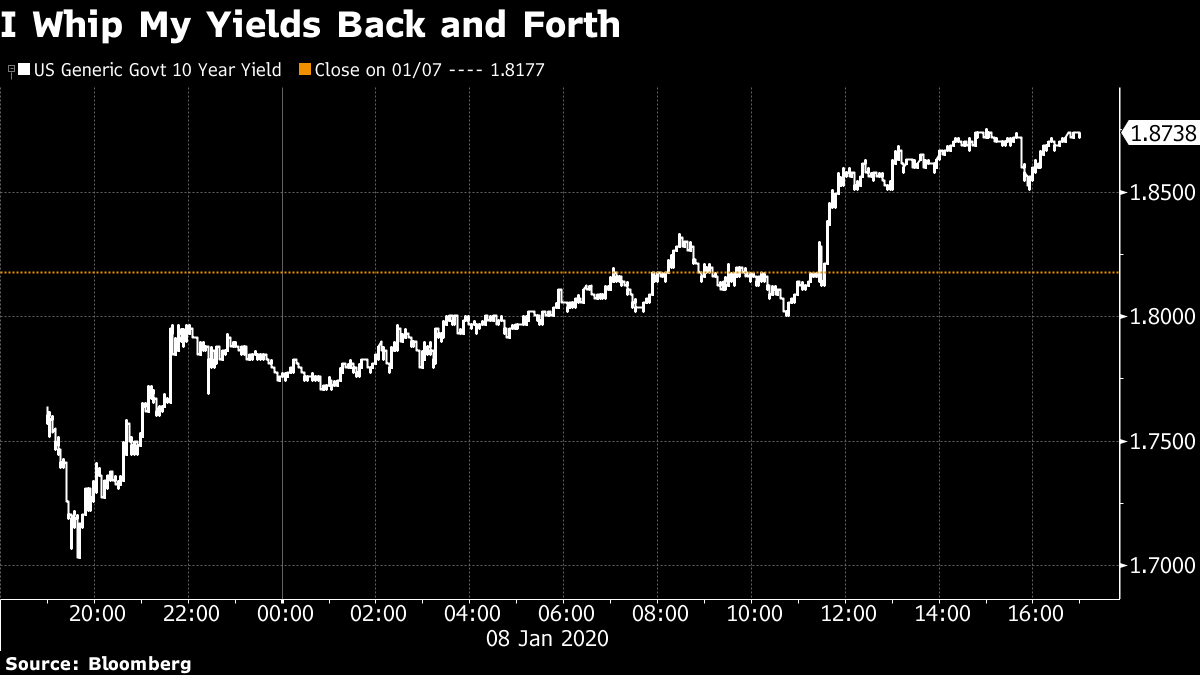

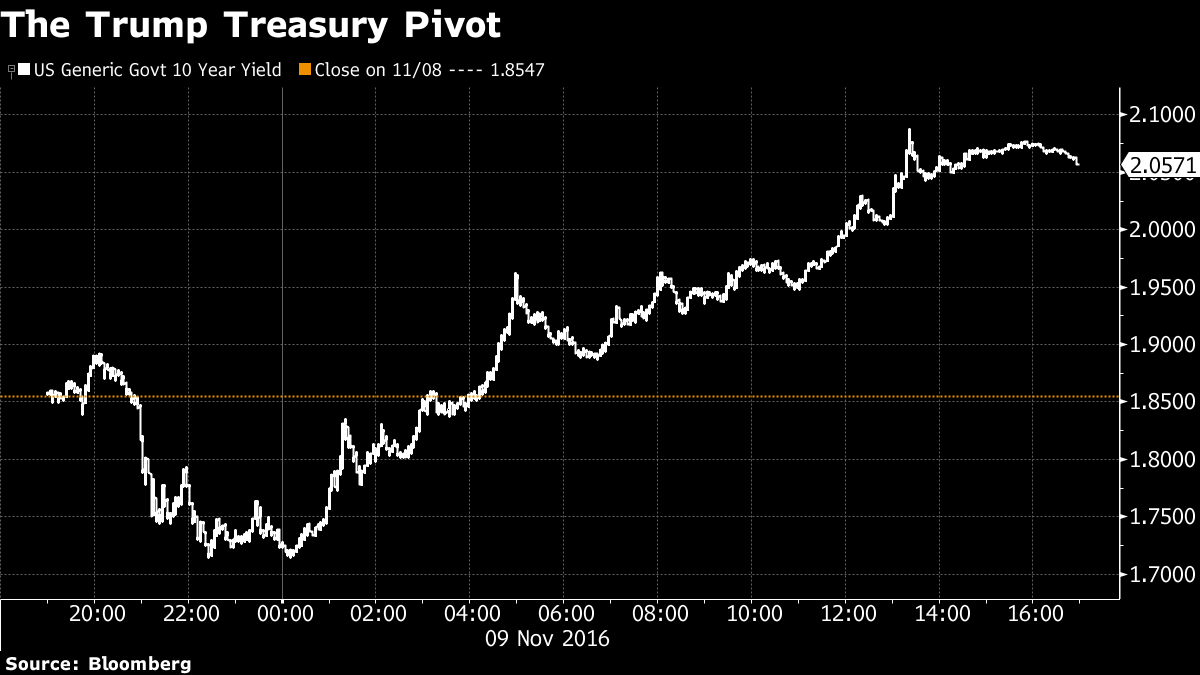

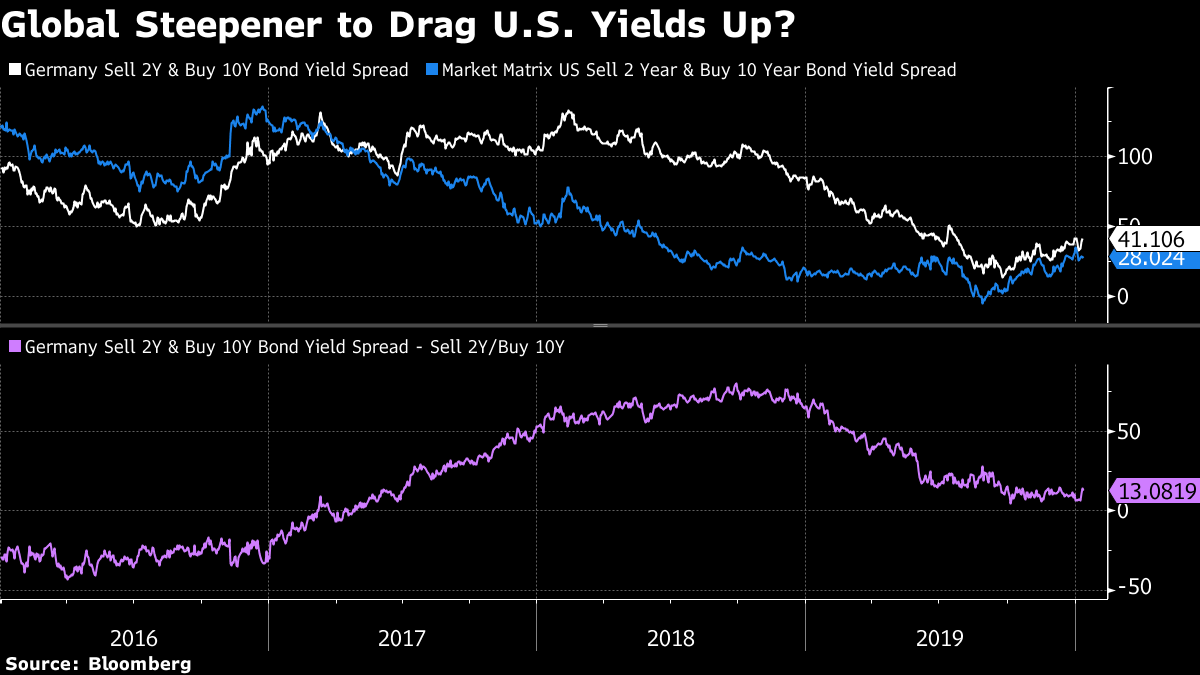

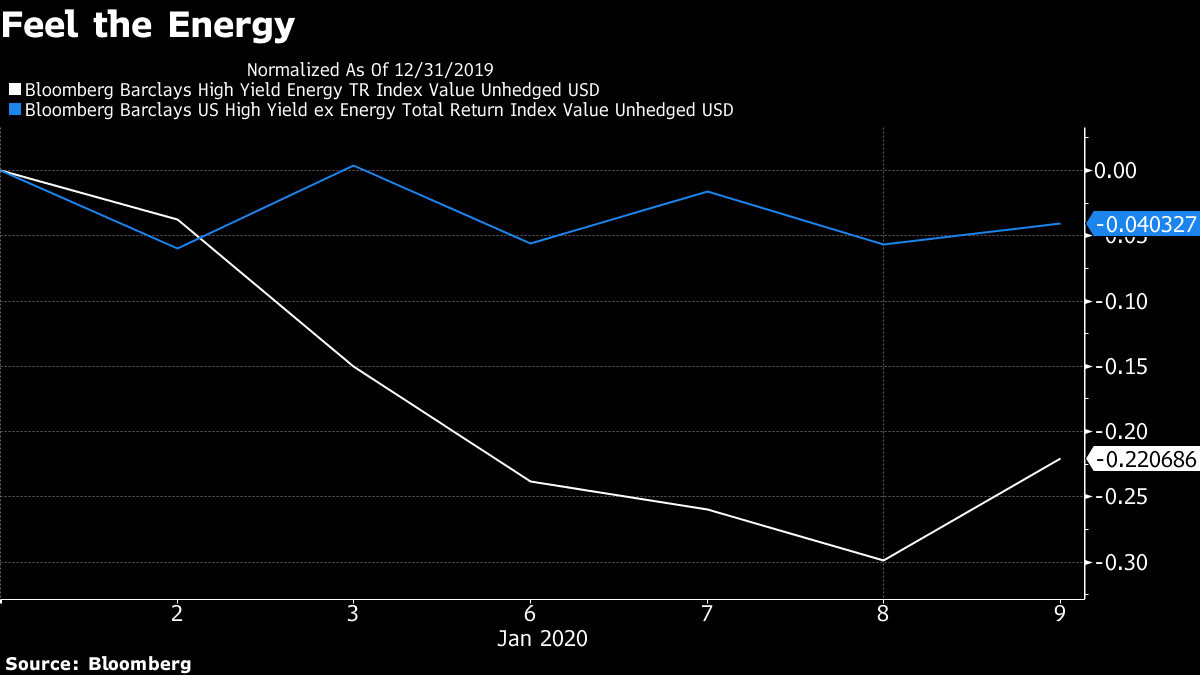

| Welcome to the Weekly Fix, the newsletter that wishes it could draw more implications from the massive reversal in Treasury yields this week. – Luke Kawa, Cross-Asset Reporter Big-League Reversal This week saw a milestone for the Treasury market the likes of which hasn't been seen since the 2016 U.S. presidential election. The 10-year yield slumped more than 11 basis points on Tuesday night, to as low as 1.7%, following Iranian airstrikes on joint U.S.-Iraqi military bases that sparked a wide risk-off response across global markets. By the close Wednesday, 10-year yields were higher – the biggest such reversal since November 9, 2016, the session following Donald Trump's surprising victory.  Treasury yields fell more than 14 basis points on election night in 2016, before closing a whopping 23 basis points higher the next day.  The two events have some, but not a lot, of basic similarities. In a sense, both reflect an evolving understanding of the implications of a given outcome. Investors decided that Trump's election had fundamentally pro-growth implications they hadn't adequately appreciated, after they mulled over the implications of Republicans controlling the House, Senate, and White House. In the aftermath of Iran's response, crucial details came to light that influenced investors' understanding. Namely, the lack of U.S. casualties – and reports that these were intentionally avoided – fostered the belief that additional escalation would be less likely. These notions were supported by Trump's comments in a national address Wednesday. Recency bias might lead one to think that reversals of this magnitude are a powerful indicator for the forward outlook, based on the bond retreat in the two years following the 2016 presidential election. But the reality is much more muddled, with limited historical references to draw upon. There have been only 16 instances in which the U.S. 10-year yield has fallen at least 10 basis points at its lows of the day yet ended higher over the past 40 years. Granted, that time period begins at pretty much the start of the long bond bull market, so the results might be what you'd expect. The forward average one-month, three-month, and one-year moves in the 10-year Treasury yield following such events are +5 basis points, -35 basis points, and -20 basis points since the start of 1980. In other words, one-day reversals do not make for reliable trend reversals, if this history is any guide. The current state of play for long-term debt: everyone expects higher yields stateside. A BMO Capital Markets investor survey showed that an elevated share would be ready to take profits should bonds rally following Friday's nonfarm payrolls report, and 81% expect the 10-year yield to boast a 2-handle before the end of March. On the other hand, bigwig investors in a Federal Reserve Bank of New York survey expect that the federal funds rate will average just 1.88% over the next decade, and a Fed economist sees longer-term rates falling close to zero in the event of only a mild recession.  Meanwhile, U.S. labor market outcomes continue to present potential asymmetry for bond investors. A strong December job report may not lift yields too much, as the Fed is seen as having set a high bar to tighten policy. That is, unless the payrolls report points to an outright surge in wages with the potential to feed through to prices in a manner that materially steepens the breakeven curve. Under other scenarios, the recipe for higher yields in 2020 seemingly has a major global convergence component. Either core government-bond yields outside the U.S. will allow Treasuries to sell off in sympathy and the curve to steepen, or government bonds stateside will remain relatively capped by their substantial premium to other developed-market yields. On that front, while German two-year, 10-year yield spreads are wider than in the U.S., they've been higher virtually all the time since the start of 2016, save a stretch during 2019.  Big Debt Energy The story of the year in credit markets is the decline of more than 20 basis points in high-yield energy spreads, versus a narrowing of less than five basis points for ex-energy.  That's despite West Texas Intermediate futures being down since the start of the year – making a stark contrast to the start of 2019, when oil futures posted their biggest annual gain since 2016, yet junk-rated energy bonds underperformed by 10 percentage points. And this beleaguered sector has been besting the asset class despite comprising nearly 60% of new issues this week. Genesis Energy LP, Range Resources Corp., Laredo Petroleum Inc., Transocean Ltd., Nabors Industries Ltd., CVR Energy Inc., and WPX Energy Inc. have all declared an intent to come to market or done so already. For all but one of these firms, refinancing debt is among the stated uses of proceeds. Elevated U.S. corporate indebtedness is the biggest visible imbalance that threatens to serve as the catalyst that brings the record U.S. expansion to an end. It may be only mildly controversial to suggest that the market reaction to the U.S. airstrike against a top Iranian general helped reduce the vulnerability of the weakest link in the most susceptible sector by aiding refinancing opportunities – or at the very least, providing a can-kicking opportunity for some of these firms. The window for junk issuers in the energy sector may have gotten a little wider thanks to the temporary fillip to crude prices, in the wake of rising U.S.-Iranian tensions. It helps that producers are actively hedging, too. Nearly all of the energy issuers that came to market this week will be paying out higher coupons for this fresh debt than on their existing obligations. That's the trade-off for pushing out the maturity wall further into the future. This cohort was largely out of the market last year, as Bloomberg has reported. It's a bit like dealing with a blister on your foot if you've taken up running to improve your cardiovascular system. Sure, there's a persistent pain while you're awake, but it's now easier to sleep peacefully at night. "Extreme high-quality valuations, geopolitical headlines supporting the critical energy sector, and a robust calendar that could eventually provide a lifeline to stressed issuers all lead us to believe the high-beta rally has legs," writes Michael Anderson at Citigroup Inc. |

Post a Comment