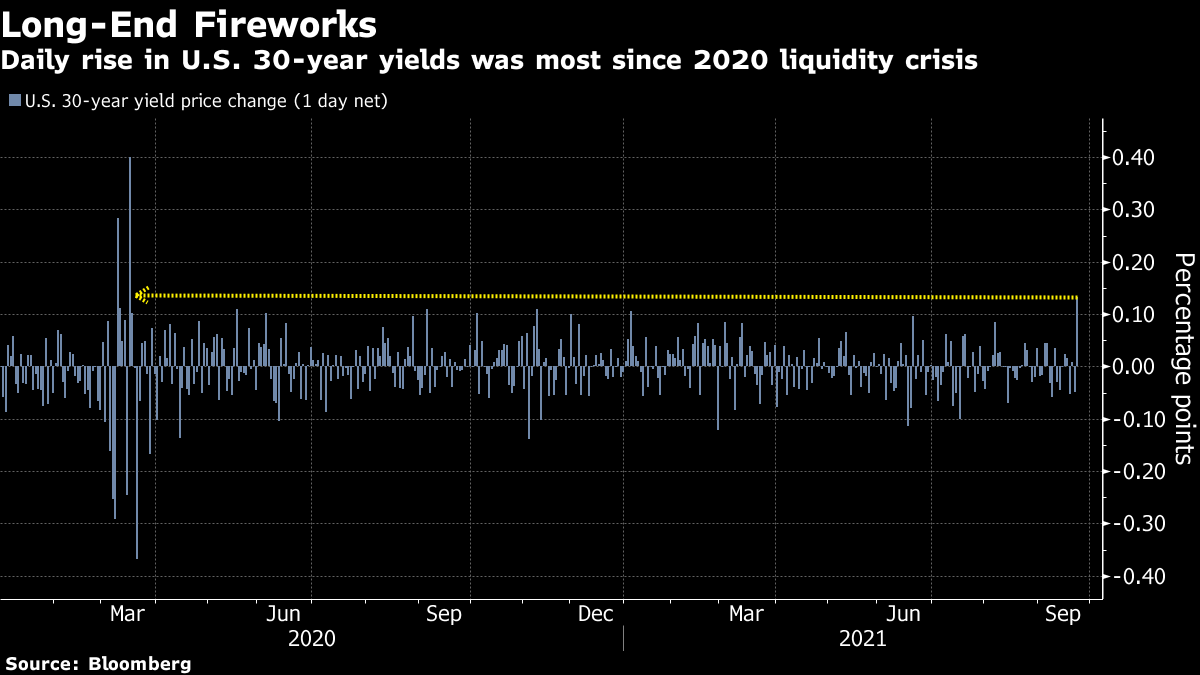

| Welcome to the Weekly Fix, the newsletter that has no obvious explanation but all the justification in the world. I'm cross-asset reporter Katie Greifeld. It took about 18 hours for bond traders to decide that this week's Federal Reserve meeting was hawkish. The Treasury market was shockingly sleepy after Fed chief Jerome Powell said the central bank could start scaling back its massive bond-buying purchases in November, and complete the process by mid-2022 -- a "turbocharged taper," in the words of UBS global chief economist Paul Donovan. FOMC Wednesday was just another day in the bond market, with 10-year Treasury yields actually drifting lower. Thursday was a completely different story. Long-term rates screamed higher, with yields on 30-year bonds staging the biggest one-day jump since March 2020.  The delayed reaction is a bit of a head-scratcher, since all the elements of a selloff were in place on Wednesday. BMO's Ian Lyngen summed it up well: Today's bearish price action in Treasuries is one of those classic moves that simultaneously has no obvious explanation and all the justification in the world.

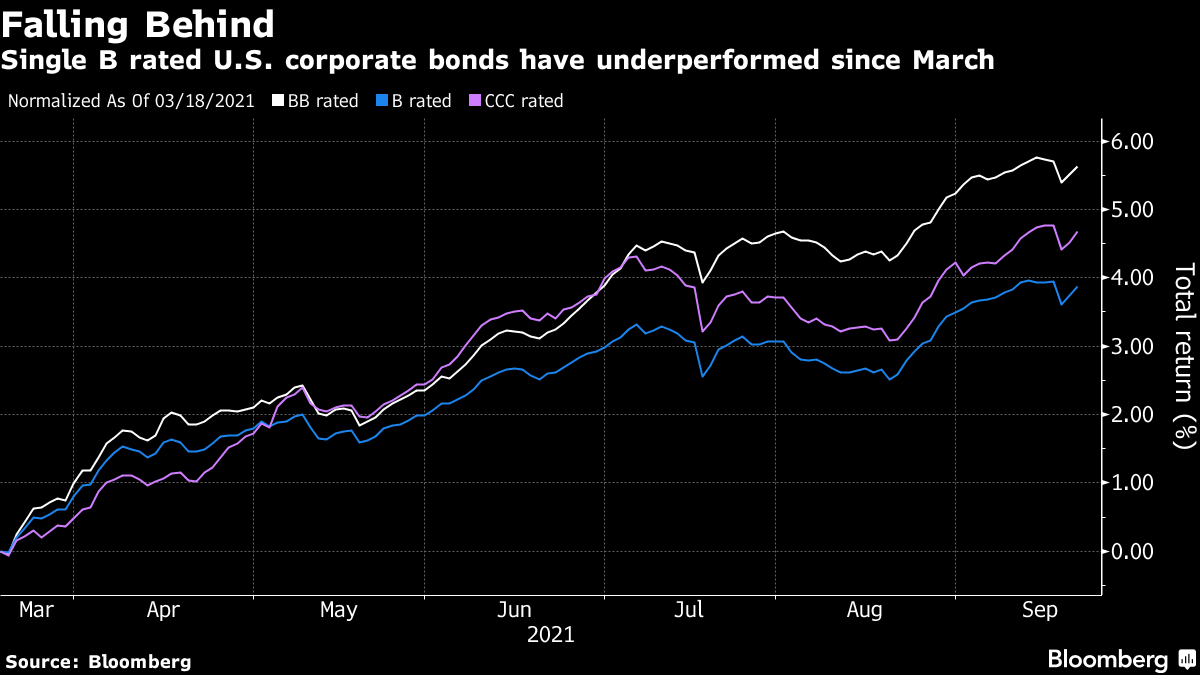

Sure, virus variants are a still very much concern and growth is undoubtedly slowing. But contagion from the Evergrande ordeal appears contained and markets now have clarity on the Fed's plan for tapering, which is more aggressive than most expected. "November versus December should not have mattered. I think the start was priced in (November or December), but not the end," Priya Misra, global head of rates strategy at TD Securities, wrote in an email. "Market thought September to October, and Powell said mid-year."  The violent move in nominal yields, combined with the jump in long-term real rates -- which strip out the effects of inflation -- makes it fair to call Thursday's session "tantrum-esque," Misra said. But BMO's Lyngen isn't ready to go there yet. "1.40% on 10-year yields does not a tantrum make," Lyngen said. "Try that at 2%." Speaking of sanguine, the corporate bond market was remarkably unruffled by this week's Evergrande events. Contagion was the word of the day on Monday, with traders around the world and across asset classes worried about the potential fallout should the heavily indebted Chinese real estate developer go bust. Credit markets -- both investment grade and high-yield -- were a relative port in the storm, with spreads barely changed on the week. Junk spreads widened to 290 basis points on Monday, still well below last month's peak of 314 basis points.  To some, the serenity looks short-lived. JPMorgan Chase & Co. credit strategists wrote Thursday that investors should consider hedging their credit exposure short term. After this year's rally, there's not much margin for error left in the bond market, while China Evergrande Group's debt crisis is far from resolved and the coming weeks could bring another U.S. debt ceiling showdown. "The challenge is that the risk/return on this is skewed to the downside," strategists led by Eric Beinstein wrote. "There is not much room for a spread rally on positive news, while a surprise negative outcome on either issue could lead to a large sell off." Yet the hunt for yield is alive and well: T. Rowe Price and Brandywine Global Investment Management are among the money managers reaching down the risk spectrum.  Given that the Fed's taper could ultimately lift bond yields, it's better to be in shorter duration bonds like Bs, which take less of a hit when yields are rising, Barclays's Scott Schachter told Bloomberg News's Caleb Mutua this week. There are few things more delightful than the intersection of the crypto universe with fixed-income. Luckily, Joseph Abate from Barclays seems equally as charmed. He argued in June that perhaps tokenization could improve repo settlement; he's explored the financial stability risks stablecoins might pose; and just this week, Abate posed the question in a research note: "Securities lenders, dealers, and banks have plenty of experience repo'ing traditional assets, but what about crypto assets?" Yes, I cried, what about crypto assets? Banks and dealers would be a natural home for crypto repo, Abate writes, given that there's "little conceptual difference" between the custody of traditional assets and a digital wallet. And there's clearly demand -- a sort of decentralized repo market for crypto has sprung up outside the realm of bank intermediation, where an ecosystem of asset financing, lending and deposit taking is developing without brokers or exchanges. However, Abate notes that banks and dealers have been reluctant to enter the financing market for digital assets. There are several good reasons for that: for instance, legal documentation and enforcement mechanisms are limited and counterparty and data risks are a concern. But beyond that, there's also the issue that crypto repo can be astronomically balance-sheet intensive for dealers. As Abate lays out, the Basel Committee on Bank Supervision proposed two classifications for crypto assets as they relate to banks' exposure: one group includes tokenized versions of traditional securities and stablecoins, and the other contains everything else. For the latter group, the risk weighting of capital requirements would be as high as 1250%. In addition, minimum repo haircuts would be 25%. That's a strong incentive to stay away -- maybe too strong. If the BCBS's proposed treatment makes it prohibitively expensive for banks to offer crypto repo, participants may instead turn to the developing decentralized networks to meet their needs. That could create another headache, Abate writes: While this would protect banks from crypto asset risks, shifting all this activity outside the regulated sector makes it harder to monitor, and this could create other challenges to financial stability.

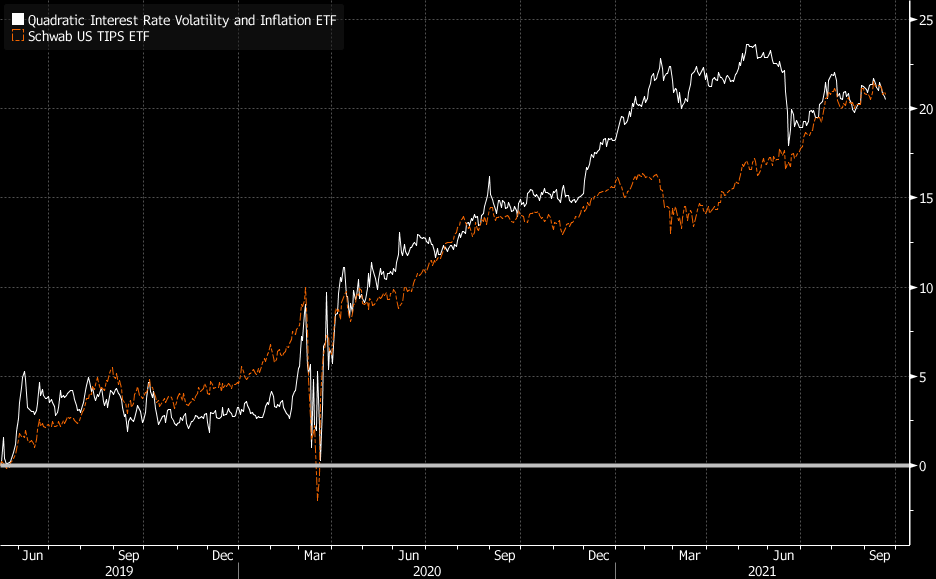

Sure, inflation has been the bogeyman of choice for most of the past year. But investors looking to take the other side of that trade with relatively minimal effort may want to check out the Quadratic Deflation exchange-traded fund (ticker BNDD), which launched on Tuesday. BNDD is designed to flourish as prices fall and economic growth flags amid sinking or negative long-term interest rates -- an environment that most would describe as deflationary. The actively managed fund will concentrate the bulk of its assets in Treasuries -- either by investing directly or through other bond ETFs -- while less than 20% will generally be in options, according to a filing. That's a similar structure to the Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL), which boomed this year as investors sought shelter from an upward price spiral. Nearly 90% of IVOL's $3.3 billion worth of assets are invested in the Schwab U.S. TIPS ETF (SCHP) -- which happens to be far cheaper. IVOL's expense ratio clocks in at 0.99%, while SCHP charges just 0.05%.  You'd be forgiven for wondering, why not just save a few dozen basis points and buy SCHP? The answer is the over-the-counter options, which are generally not available to general investors. Fund manager Nancy Davis is responsible for rolling over the contracts in IVOL, and will do so for BNDD to make sure the exposure doesn't exceed the 20% threshold. IVOL launched in May 2019 and has returned about 20.5% since its inception, compared with 20.8% for SCHP in the same period. IVOL pulled ahead in the first five months of 2021 as inflation fears rose to a fever pitch, delivering gains of some 2.3% through the end of May while IVOL drifted 0.5% higher. But year-to-date, IVOL has dropped about 0.6% while SCHP has climbed roughly 1.5%. Investors are paying a lot for that level of performance, considering IVOL's expense ratio of 0.99%. But it seems they are willing to for a promise of uncorrelated returns. Time will tell if they feel the same about BNDD, which comes with the same fee. Bonus Points Crypto Market 'Starting to Knock on the Doors' of Big Bond Funds Twitter Adds Bitcoin Tipping, Pushes Further Into NFTs Wall Street Faces Tough Transition in Return-to-Office Push |

Post a Comment