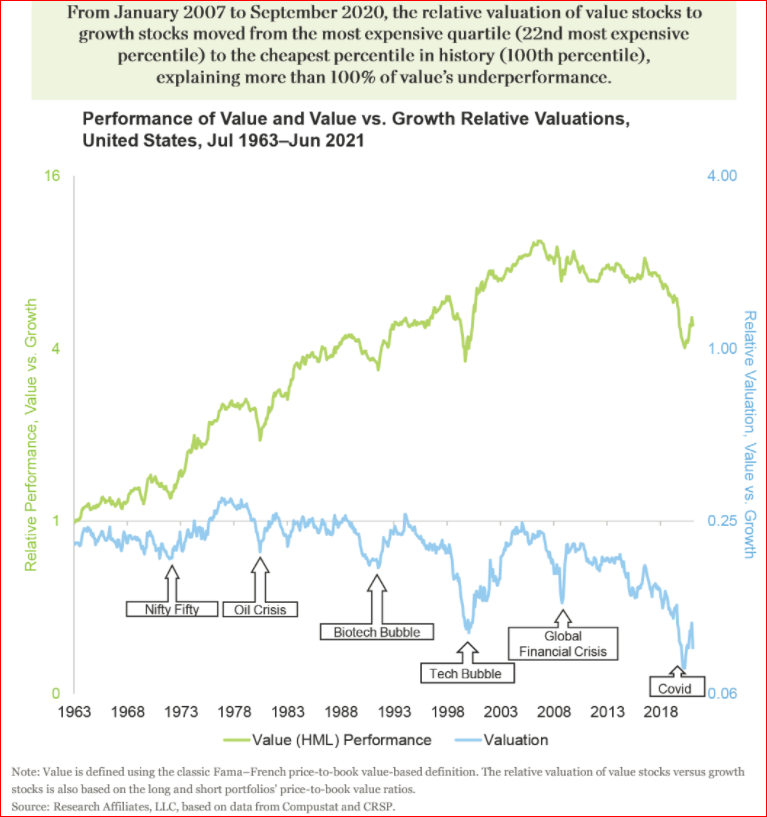

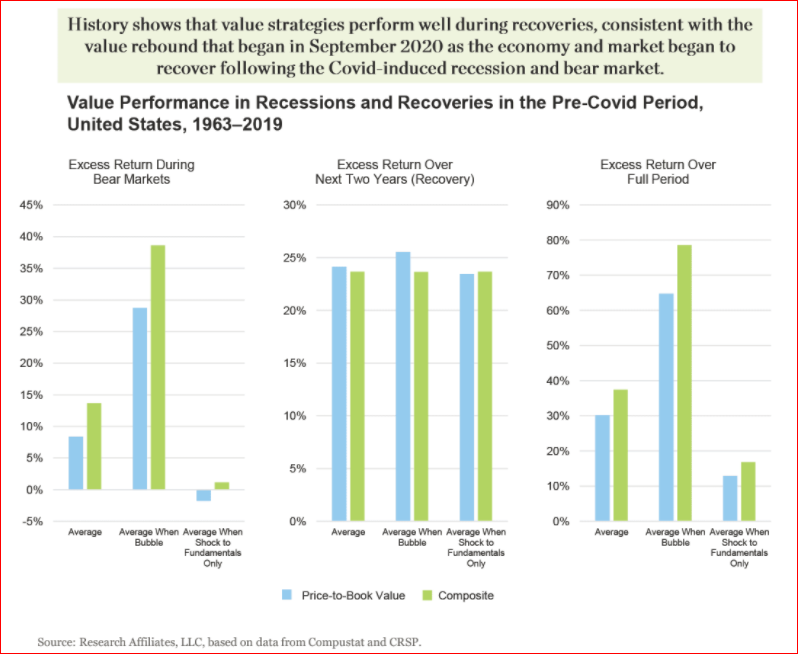

| Investing is about opportunism, as much as it is about hard work, discipline and patience. That is the founding creed of value investing. As laid out by Benjamin Graham almost 90 years ago, Mr. Market is a manic-depressive who will occasionally give you the opportunity to buy stocks for less than they are worth. Doing so is more easily said than done. But is it just about possible that Mr. Market is giving us a second chance to buy into value stocks at ridiculously cheap valuations? That is the argument made by Rob Arnott, the quantitative guru who founded Research Affiliates LLC, in a new research paper called "Did I Miss The Value Turn?" It's worth 20 minutes of your time, if you're an opportunistic investor. And it's just possible that Arnott is right. Let's take the argument in steps. In recent years value, using the classic simplified definition of just taking the stocks with the lowest price-to-book multiples, has badly underperformed growth, where companies are chosen based on how fast their earnings are increasing. After a rally at the end of last year, which was sparked by the successful results of initial Covid-19 vaccine tests, value has sagged once more. This is true in the U.S., and also in Europe and Japan:  We get a similar result if we look at the performance of value compared to momentum (a factor beloved of professional investors, which involves piling into winners while selling or shorting losers). Momentum suffered a particularly savage reversal with the vaccine tests, and a further reversal as the incoming Biden administration started by splashing around a lot of money. The following chart uses the pure factor returns for value and momentum as calculated for U.S. stocks by the Bloomberg FTW, or Factors To Watch, function:  Value had a terrible run, then, rallied for a while, and then relapsed. Why should we believe that this is a good time to buy? Arnott's theory is that we should look at valuation. By definition, value will always look cheap relative to growth. The point is to look at how much cheaper value is, and how this compares with history. That calculation is shown in the blue line, going back almost six decades. Over that time, value has typically outperformed growth (the green line), with occasional sharp drawdowns driven by major crises, after which it tends to bounce back quickly. But since the global financial crisis, value hasn't enjoyed a big rebound, and its relative valuation has become extraordinarily cheap:  The deeper the discount at which you can buy value stocks, the greater the opportunity to profit as they return to normal. And Arnott shows that the excess return (compared to the market) over the two years of a recovery from a major shock sees great performance for value. This is particularly true when the crisis has itself been driven by a bubble, or misvaluation (as was true of the bursting of the dot-com bubble in 2000 or the fall of the Nifty Fifty stocks three decades):  Invest when things are particularly bad, and the virtue of buying cheap gets all the stronger. This may not help you get the timing exactly right — it's always possible that value stocks can do even worse for a while. But it does mean that on a medium-term basis you should do well. Valuation matters, according to Arnott, because it explains literally all of value's travails since its peak. The disaster for value stocks since the global financial crisis hasn't been about bad fundamental performance by the companies involved, but about a collapse in the relative valuation that investors are prepared to pay: the average discount for US value stocks over the period July 1963–June 2021 is about 21%, or put another way, US growth stocks typically sport a price-to-book value ratio about five times that of value stocks. From January 2007 to September 2020, the relative valuation moved from the most expensive quartile (specifically, the 22nd most expensive percentile) to the cheapest percentile in history (100th percentile); this revaluation explains more than 100% of value's underperformance through September 2020. In other words, net of this downward revaluation relative to growth, value would have beat growth by a respectable margin.

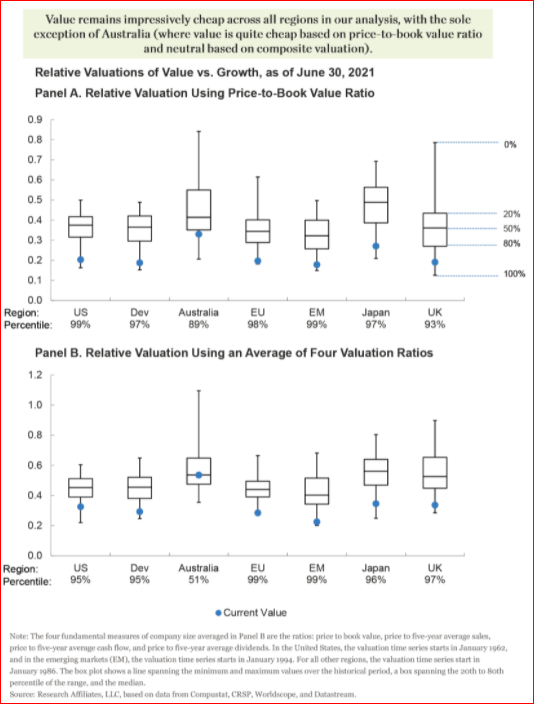

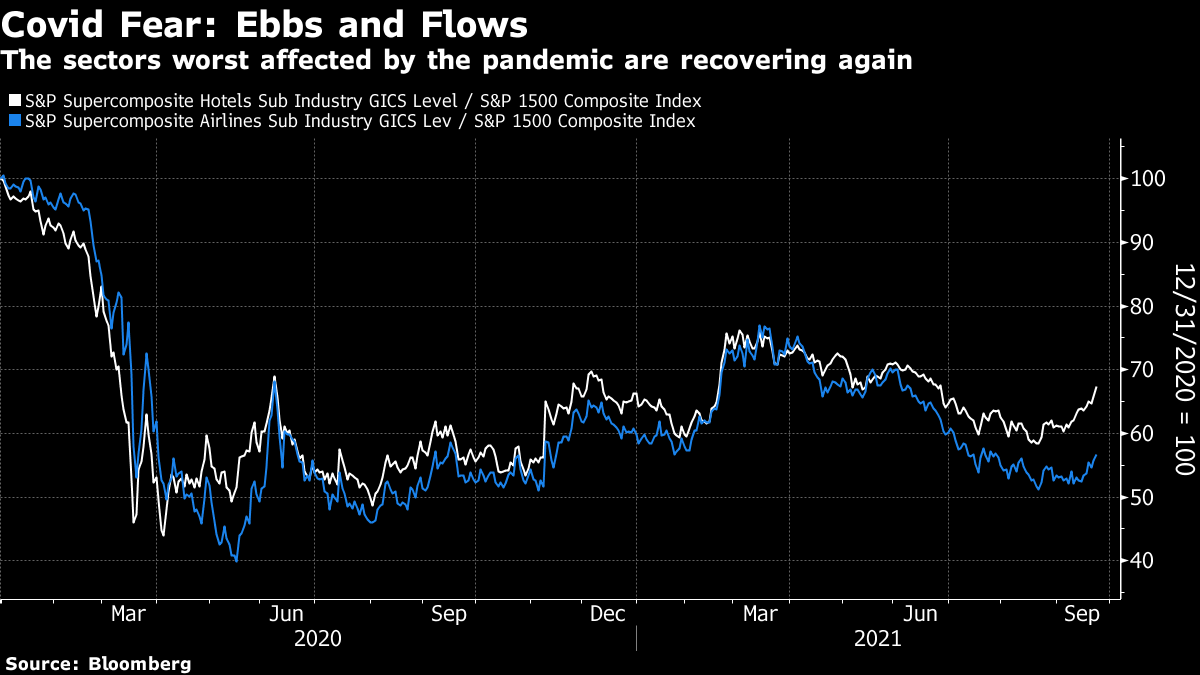

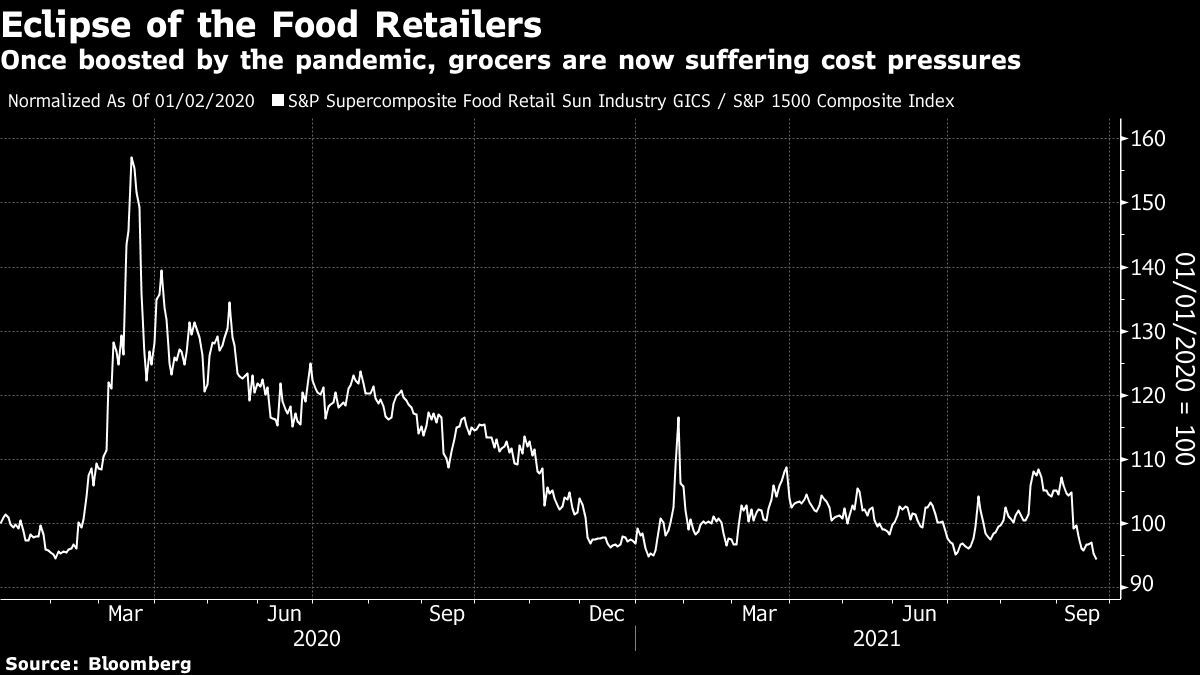

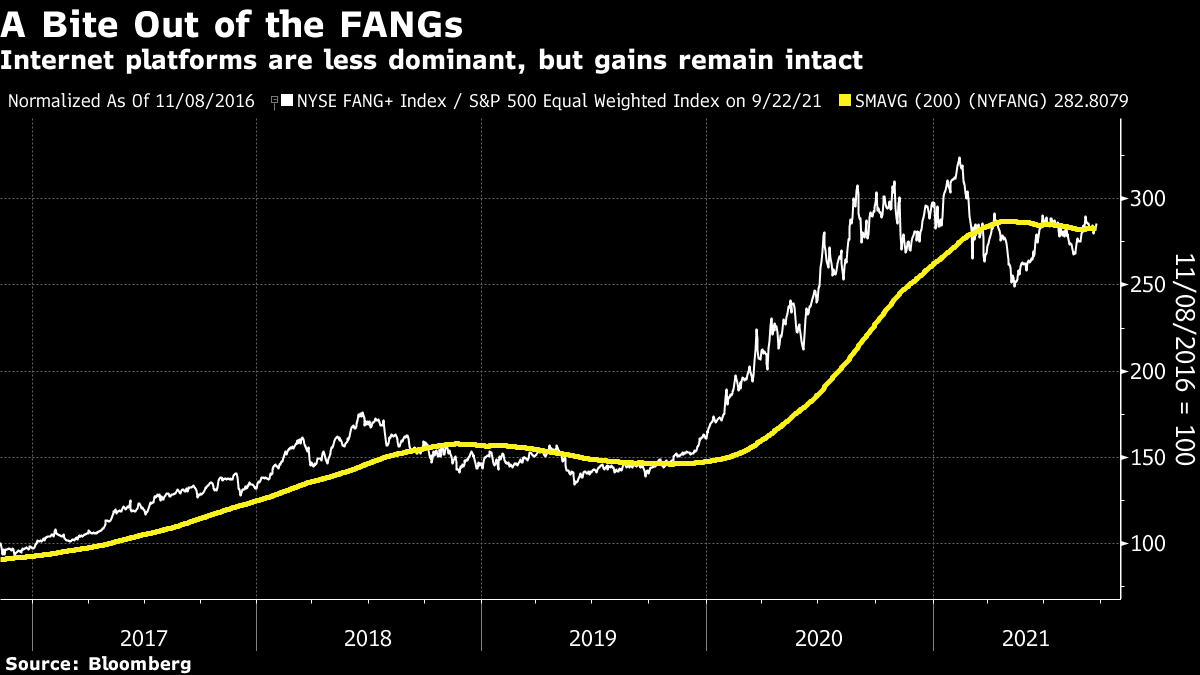

This cheapness shows through whether we use a crude price-to-book valuation alone, or a composite of different metrics. In the U.S. and in emerging markets, value stocks are in the 100th relative valuation percentile; using a composite, Europe drops them into the 100th percentile and those in the U.S. rise a bit. But with the sole partial exception of Australia, the fact remains that value stocks look compellingly cheap everywhere:  So, it looks like Mr. Market really has given us a second bite of the cherry. Why might this have happened? The first and most obvious answer is Covid. If we look at the performance of airline stocks and hotels, two sectors that were directly and brutally affected by the pandemic, we see an impressive recovery earlier this year, followed by a renewed slide over the summer. As everyone is aware, the delta variant dampened everyone's travel plans this summer. Many of these stocks are dirt cheap, and show up on value screens. So Covid plainly has a lot to do with the second chance to buy value. And as hotels and airlines are putting together a recovery, the opportunity might not last long:  But there is far more to current market conditions than the virus. This week has seen a rash of central bank meetings, punctuated by a virtual promise by the Federal Reserve to start tapering its asset purchases in November and by the decision of Norway's Norges Bank to raise interest rates — the first central bank to do so in the Group of 10 developed economies. This suggests a shift in economic momentum. And after a quiet Wednesday, the bond market responded with sharply higher yields Thursday. Yields remain within their recent ranges. But we still need to ask: Why did bond yields rise Thursday, in what looked like some kind of limp and delayed taper tantrum? My colleague Joe Weisenthal asked that question on Twitter as bonds sold off, and received lots of responses. I'm sure Points of Return will have ample opportunity to delve into the bond market over the weeks and months ahead. For the time being, note that the strength of the economy, and with it the steepness of the yield curve, has an obvious and strong relationship to the relative performance of value. As this chart shows, value's horrid relative performance since 2017 has overlapped with a steady flattening of the yield curve, which was briefly inverted (the classic signal of an oncoming recession) in 2019. Value's resurgence and then dip overlapped with a steepening and then flattening of the yield curve:  Note also that value's continued bad performance in the last few weeks has come even as the yield curve steepened. If the yield curve steepens further (not a subject for now but it easily could), then it's reasonable to expect value to recover. What of the broader impact of the pandemic? Value's continuing travails are happening even though a number of the more obvious distortions caused by the pandemic are beginning to work their way out of the system. For example, food retailers were regarded early last year as the ultimate safe haven from pandemic disaster. They could rely on continuing demand. The sector's spectacular spike compared to the broader market was over by the end of 2020. At this point, food retailers are actively suffering from the effects of the pandemic on supply. The food retailers' index has actually lagged the market since the beginning of last year. The main reason for this was the announcement by Kroger Co., the largest U.S. specialist food retailer, earlier this month that rising costs had bitten into its margins.  Another pandemic anomaly now partially corrected involves the FANG internet platform stocks. Companies that make money when people sit at home at their computer screens naturally outperformed last year, and the NYSE Fang+ index outperformed massively. The FANGs are growth stocks, and their ascendancy contributed to value's underperformance. But that ascendancy peaked early last year. Over the last 12 months, the FANGs have slightly underperformed the average stock — although it is unclear whether they are locked into a downward trend:  This looks a lot like the kind of extreme valuation imbalance that makes for great value performance thereafter. Arnott draws an analogy with the 2000 tech bubble: As the pandemic wanes, many of the tech companies that greatly benefitted from the lockdowns and widespread work-from-home policies will likely cede some of those benefits. While some pandemic-era behavior changes will prove lasting, we believe most people will revert partway to the normal habits of the past. Amazon, for example, grew its revenues by 84% in 2020 relative to 2019, profiting from the massive switch to primarily online purchasing behavior; some of that behavior will mean revert. As this happens, many of the economic and behavioral trends that supported these high-flying companies are likely to reverse course. The high valuations and high market concentrations typical of these (mainly tech) stocks create further risks to investors who hold them. Cisco, for example, has had double-digit growth in sales, profits, and book value in the 21 years since it was briefly the largest-cap stock in the world, and yet its share price is still down from its 2000 peak price. As one wit during the 2000 tech bubble quipped: "Some of these share prices are not only discounting the future, but also the hereafter."

Value investors have had to deal with plentiful disappointments in the last decade or so, as have those predicting a turn toward higher yields in the bond market, and a return to inflation. But with relative valuations extreme once more, the basic case is made. Asset allocators would be well-advised to shift toward value stocks at a time when so many assets look badly overpriced. In the medium term it will work. You really should try reading Winning the Loser's Game by Charles D. Ellis. We will be discussing it with him for the Bloomberg book club on Oct. 5 on the terminal — all questions are welcome. I'm enjoying re-reading it for the first time in a while. Beyond setting out the case for passive investing, it also sets out a compelling definition for a "winners' game" as opposed to a "losers' game," drawn from tennis. Watch tennis, and it in fact boils down to two different games; a "winners' game" played by professionals and the most serious of amateurs, in which winning is about finding the perfect strategy to beat the opponent, and a "losers' game" played by the rest of us, where the winner is the one who doesn't lose. For most of us, winning in tennis is about scrambling around and not hitting the ball into the net or out of bounds enough times to survive until the opponent makes a mistake first. To quote Ellis: Amateurs seldom beat their opponents. Instead, they beat themselves. The actual outcome is determined by the loser… Rather than try to add power to our serve or hit closer to the line to win, we should concentrate on consistently getting the ball back so the other player has every opportunity to make mistakes. The victor in this game of tennis gets a higher score because the opponent is losing even more points.

He cites research that shows that in professional tennis, 80% of points are won, while in the amateur game 80% of points are lost. And then he goes on to explain how investing used to be a winner's game, with brilliant investors like Ben Graham or Peter Lynch snapping up great opportunities, but now it's a losers' game, where all the other players are institutions, and the aim is to avoid mistakes. I hope this whets the appetite for more reading. Meanwhile, tennis as a winner's game is even more entertaining than investment. You might try watching Bjorn Borg and John McEnroe's epic tie-breaker from the 1980 Wimbledon final; the eternal final game of Andy Murray's victory over Novak Djokovic in the Wimbledon final of 2013; or Venus Williams reeling in Martina Hingis at the U.S. Open in 2000, in a game I was lucky enough to see live; it's an amazing contrast in styles and shows there's more than one way to play the winner's game. Have a good weekend everyone. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment