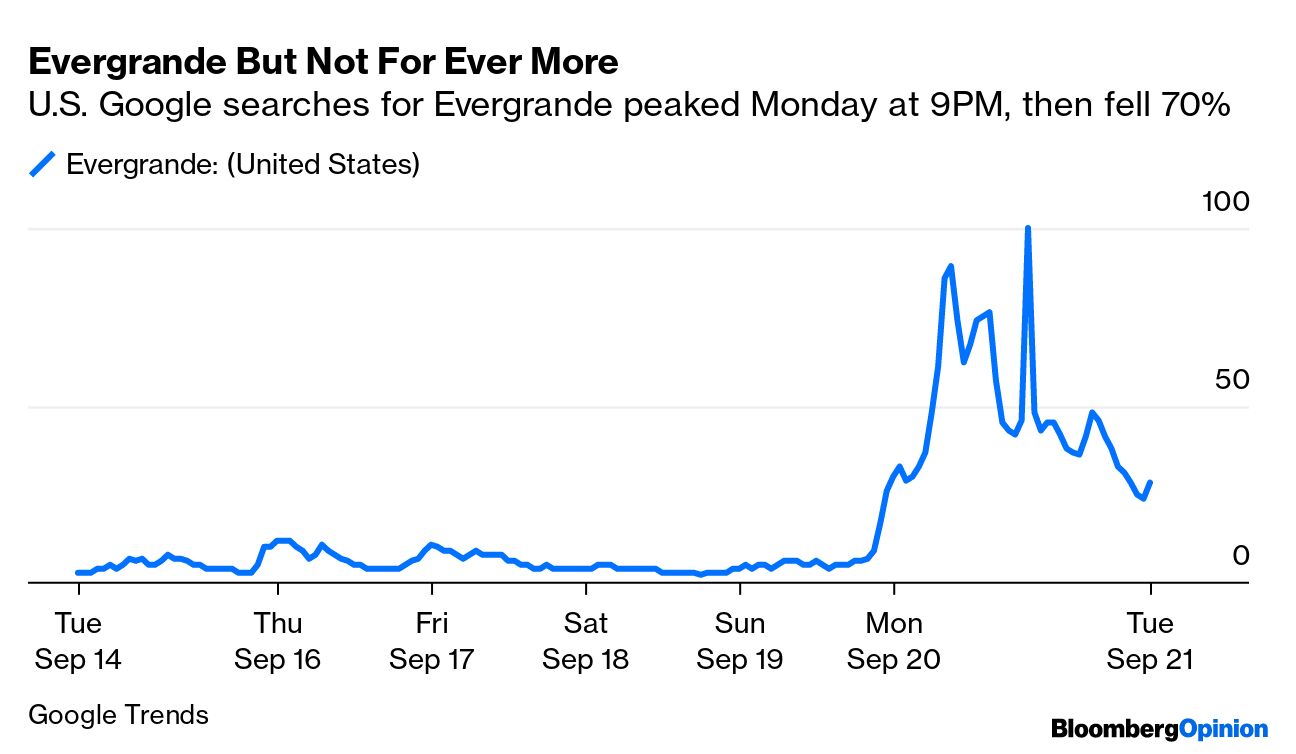

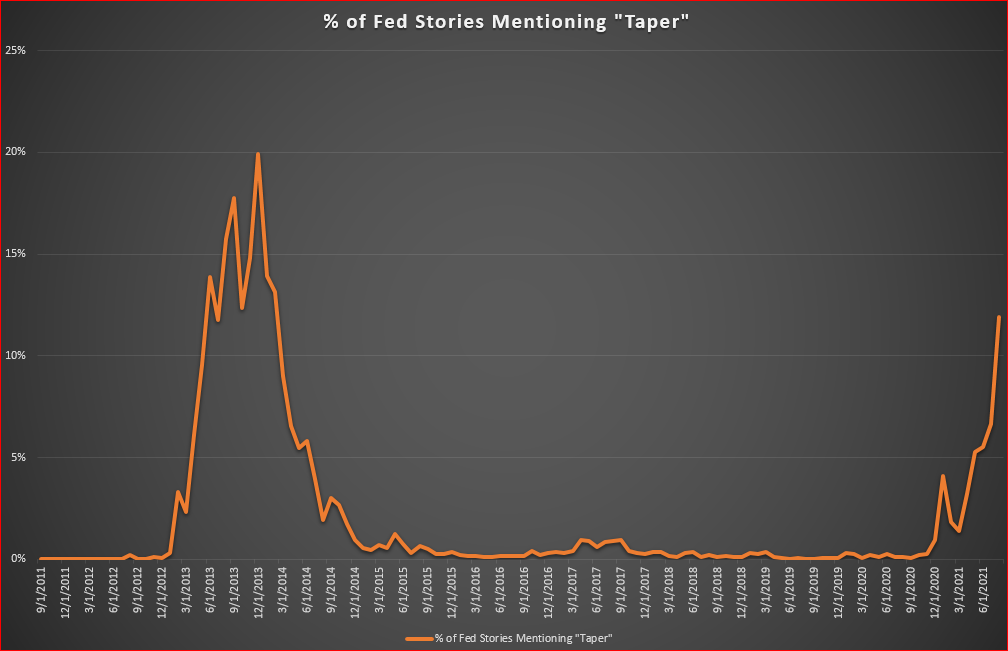

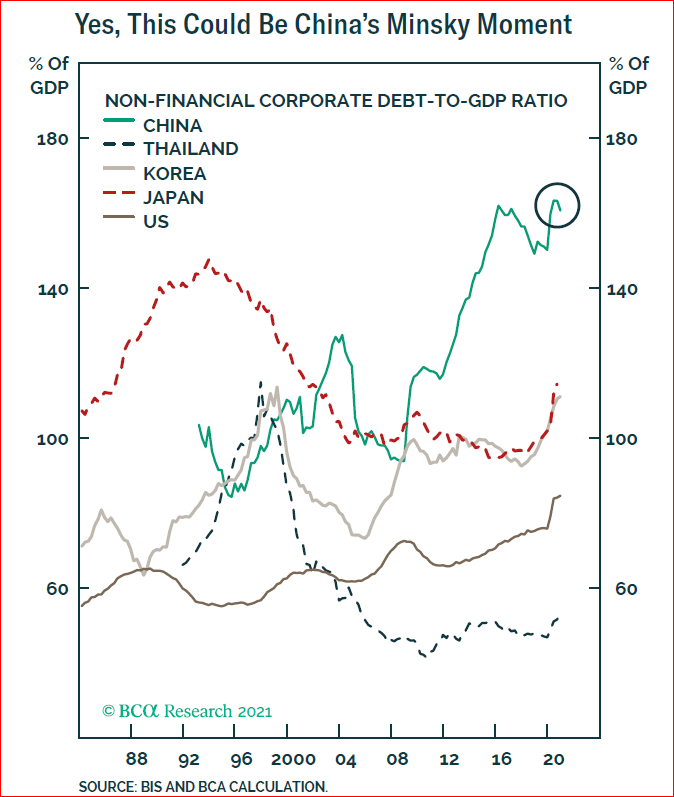

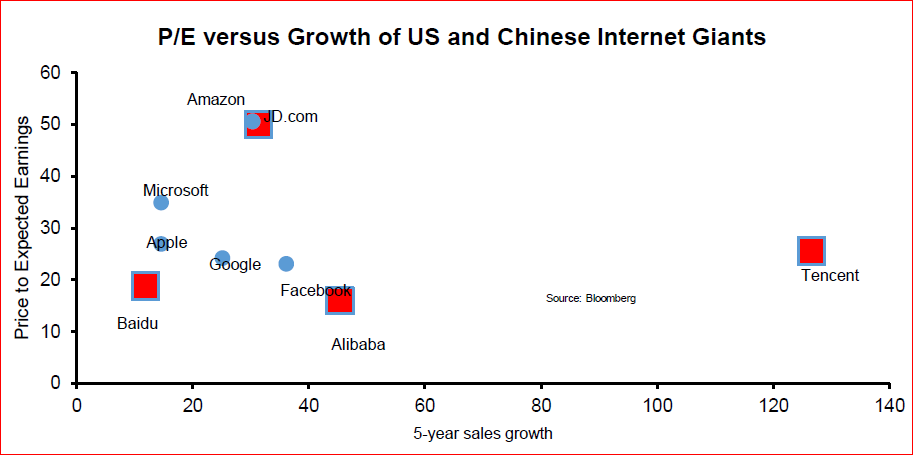

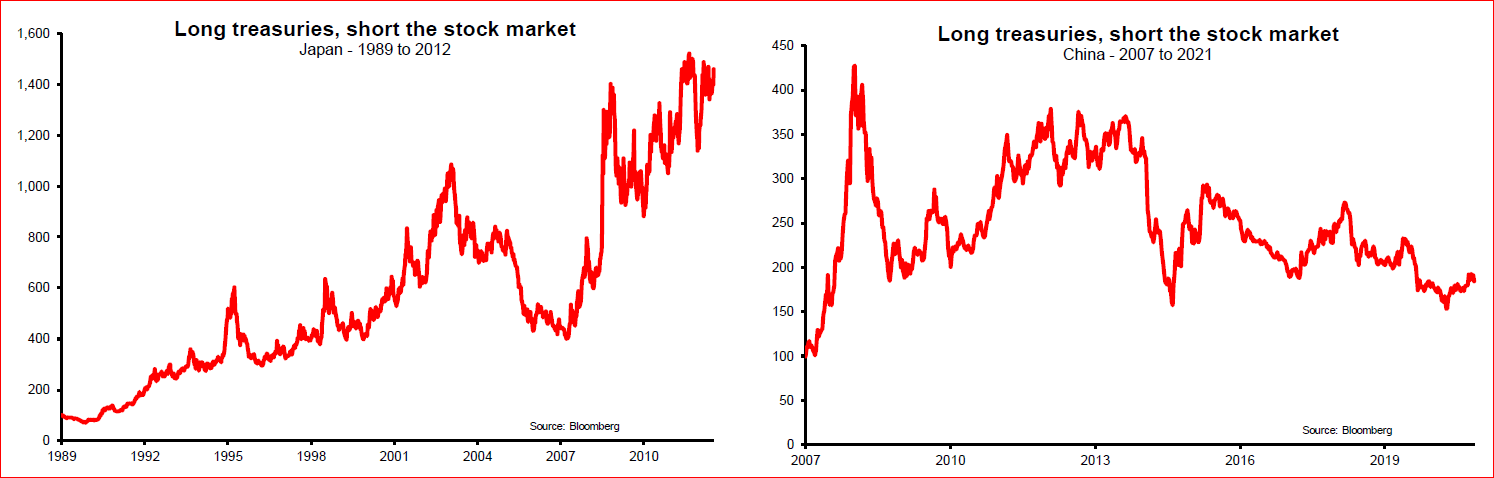

| The Evergrande panic isn't everlong. After Monday's selloff, which teetered on the brink of panic, stock markets pulled themselves together across the world. Meanwhile, investors appeared to believe that they had brought themselves up to speed on the troubles of China Evergrande Group, the country's second-largest property developer. Google Trends shows that searches for the word "Evergrande" in the U.S. suddenly took off on Monday morning (even though the situation had been coming to a boil for weeks if not months). After activity peaked at 9 p.m. on the Eastern seaboard, it fell off sharply Tuesday:  Many other things are going on, not least a general election just across the border in Canada, and plenty of intrigue on Capitol Hill. It's understandable for investors to try to avoid extreme positioning on the eve of a Federal Open Market Committee meeting that will bring the taper back into the conversation. Mentions of "taper" in Bloomberg are rising in just the way we would expect if support were to begin to come off at the end of this year, just as it did at the end of 2013:  But if we look at a chart of the Chicago Board Options Exchange Volatility Index, or VIX, over the last week, the similarity with the Google search history is obvious. It could be a coincidence, and this doesn't prove cause and effect. But it seems a fair base assumption that the ebbs and flows of worry about Evergrande have been driving sentiment in the U.S. stock market:  Why such concern about an issue that is a long way away? Reams of research (to which I contributed Monday) have asserted in the last two days that Evergrande won't be China's "Lehman Moment." In other words, investors are confident that a default or bankruptcy couldn't trigger a crisis on the scale of the disaster that followed the Lehman Brothers collapse in 2008. The fact that so many addressed this question does, however, show that the question is reasonable. As BCA Research Inc. shows, non-financial corporate debt in China is now on an even bigger scale than Japanese corporate debt before its economy ground into crisis in the 1990s. This chart also provocatively draws comparisons with the peak in debt for South Korea and Thailand in the late 1990s, on the eve of the Asian crisis. If mishandled, it isn't alarmist to raise the question of a potential Lehman-scale crisis in China:  Without repeating all the arguments from earlier in the week, it looks as though the Chinese authorities are determined to ensure some form of orderly workout, and also as though they have the ability to avoid disaster. Evergrande's problems were in many ways triggered by last year's regulatory crackdown on developers' leverage. So the chances are slim of a disorderly bankruptcy a la Lehman, which takes the market by surprise. None of this is a counsel for complacency. Evergrande is in a serious mess. But people with the tools to clean up the mess are on the case. This is what you might call the "upside" of the Chinese government's increasing willingness to intervene in the private sector. It makes a debt crisis less likely. But a heavy-handed government is a double-edged sword. The downside is that the government reserves the right to get in the way of a company making a profit, or to grab returns that shareholders might have expected were coming to them. State planning might well have the tools to avert an all-out debt crisis; sad experience over many decades suggests that it is a lot less effective at spurring consistent and strong economic growth. Communist planners want their economy to grow, and have no desire to spark a crisis. To an extent, their interests are aligned with those of private sector investors. But that alignment is far from perfect. Evergrande also highlights another long-lasting issue with the Chinese growth of the last generation. Countries have grown like this in the past, but never without suffering some major crises along the way. This was true of Britain during the Industrial Revolution and Gilded Age America, and more recently the BCA chart above shows how debt-fueled expansions in Japan and the Tiger economies reached a moment of crisis. Government intervention in China has, so far, averted a major crisis — but that has meant that the debt kept piling up, in a way that must logically slow down growth in the longer term. The factors of political interference, and the inevitability of interruptions after so much growth come together in the question of valuing Chinese assets: For several years around the global financial crisis, Chinese shares traded at a premium to the developed world, in terms of price-book multiple. That reflected belief in superior longer-term growth prospects, along with a belief that the Communist Party was communist in name only and could be trusted to provide enlightened stewardship of capitalism. Confidence in both propositions, particularly the second, was excessive. Chinese shares have traded at a discount to the MSCI World Index for almost a decade now, as confidence has been diluted. The major growth scare of 2015 saw the discount deepen. But in the last few months, a combination of the party's crackdown on the private sector and the growing problems with Evergrande have led Chinese stocks to trade at the biggest discount of the modern era:  Meanwhile, the link between China and the rest of the emerging world has been sundered. For all of this century, emerging markets traded in effect as though they were an extension of China. Commodity exporters in Latin America, and the companies that supplied China in the Asia-Pacific, all rose and fell with the country's fortunes. But the last few years have shaken that. China is now being traded very differently from the rest of the emerging market complex. First, China's management of the pandemic (even though it originated there) while other emerging countries were stricken drove massive outperformance. In the last few months, mounting alarm about the Communist Party's behavior, along with the developing Evergrande situation, has seen a massive correction. At this point, China's stock market has done scarcely any better than the rest of the emerging markets this century:  If belief in beneficent Marxist capitalist planners was always misplaced, it's still open to question whether the pendulum has moved too far. China is the only country other than the U.S. that hosts some seriously potent internet platform companies meriting comparison to the giant U.S. "FANG" stocks, such as Amazon.com Inc., Microsoft Corp., Apple Inc., and Alphabet Inc. Chinese companies like JD.com Inc., Alibaba Group Holding Ltd. or particularly Tencent Holdings Ltd. have enjoyed sales growth in the same stratosphere as the FANGs. But they don't command anything like the same multiple of earnings. This chart is from Vincent Deluard, investment strategist at Stonex Group Inc.:  Chinese politicians are keeping big internet groups on a tighter leash these days — but it's not as if their counterparts in the U.S. are free of political risks. While China's leaders want to maintain control, they don't want to kill off successful companies. Could the pendulum have moved too far? The issue of growth is more profound. At a certain point, Deluard points out, growth will inevitably slow down and it will pay investors to hold Treasuries while shorting the stock market. That was spectacularly true of Japan starting in 1990, after a massive speculative bubble. There is no such bubble at present in China, and Treasuries won't generate the returns they did in the 1990s. But if we start on the eve of the Chinese stock bubble of 2007, holding Treasuries while shorting Chinese stocks has worked for a while:  A Lehman event should be avoidable. But a big slowdown in broader growth is harder to avert, and Evergrande makes a slowdown look even more likely. Investors are braced for such a slowdown in China now. Depending on how Evergrande is handled, it may be necessary to price in a milder or more severe slowdown in the world's second-largest economy. That is its greatest significance. My list of great Canadians from yesterday wasn't meant to be exhaustive. Many have written in to point out some of the worst omissions. From the world of music, for example, I could/should have mentioned Joni Mitchell, Neil Young, Oscar Peterson, Alanis Morisette, Owen Pallett, and Drake. Ryan Gosling has shown us he can sing. I might even have mentioned Bryan Adams. But definitely not Justin Bieber. And Canada also provides a regular stream of great athletes for whom the Brits then take the credit. Following Lennox Lewis and Greg Rusedski, we now have Emma Raducanu, the young queen of women's tennis, who is British but was born in Toronto (and beat another Canadian in the final of the U.S. Open). So discerning is Raducanu that she has even named Bloomberg's own Tom Keene as one of her three ideal dinner dates (along with Michael Jordan and the Formula 1 driver Daniel Ricciardo, who will doubtless be delighted to be included in the same company as Tom). This is the kind of wonderful judgment we expect from Canadians. It's also very nice of the country to the Great North to stage a general election so uninteresting that the balance of power barely changed, the government didn't change, and the Canadian dollar barely ever wobbled. Which got me out of having to do some work on the Canadian financial markets, but did give me an excuse to look up a lot of great Canadian musicians. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment