| Tuesday was a day of excitement in markets. Our own Bloomberg News headline was: Markets Faced a Day of Superlatives as Wall of Worries Spread. But how much did it matter, and what does it tell us about the future? What, if anything, is there useful to know about it? It's a dilemma for investors and it's a dilemma for people like me who have to cover markets. I'm still smarting from a friendly (I think) note from a reader, in which he looked for the best analogy for this newsletter: I have rejected "calling a play by play for a ping pong match", and "speculating about the next moments weather", as well as "predicting the health of a forest by examining individual trees", none really fit. Yet I feel that you are mired in the data and not really capturing broad trends that would be useful to long term investors.

Ouch. I'm not sure this is totally fair, but it certainly pinpoints a problem. You can only get to the long term by surviving the short term, and in every day's noise there is some signal to be detected. But it's difficult to find that signal, and it's easy to fall into the trap of retro-fitting explanations to fit the way the market happened to behave. The fact that journalists have to find something to say every day constantly creates the temptation for exaggeration. And of course, it's easy to drown out any signal you find with all the noise. So, here is an attempt at some of the salient points from an undeniably dramatic day: - The main equity indexes still aren't as low as they were at the worst point on Monday last week, now known as "Evergrande Monday".

- The total drawdown, from peak to trough, isn't even 5%. This sell-off hasn't corrected much of anything.

- Bond yields, yield curves, and inflation breakevens have all risen sharply, but all remain within their ranges for the year.

- Where there does appear to be a break out is in the dollar — its highest since the successful vaccine trials were announced last November against both emerging market currencies, and the other major developed market currencies.

- Perhaps most importantly; this was an uncharacteristic day, of late, when stocks and bonds were sold at the same time. If you were hoping to use bonds as a "diversifier" to cushion the blow of falling stocks, they didn't work for you.

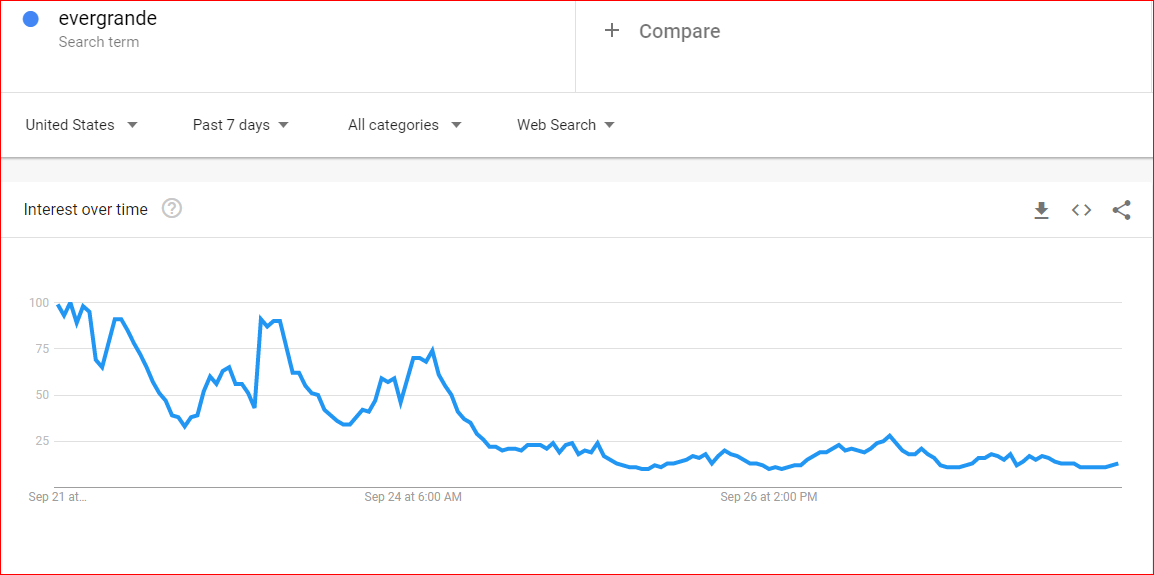

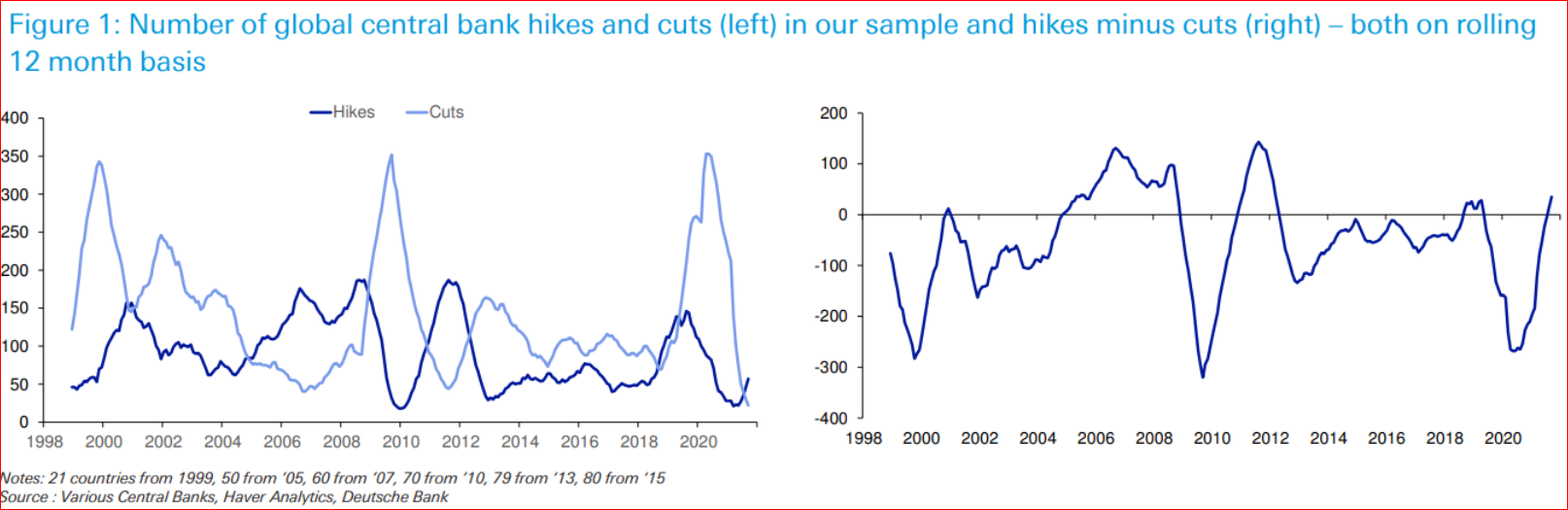

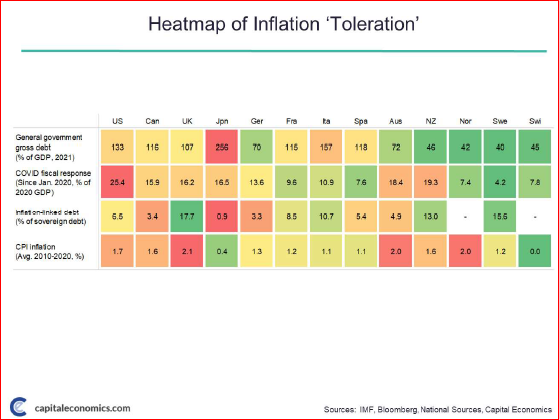

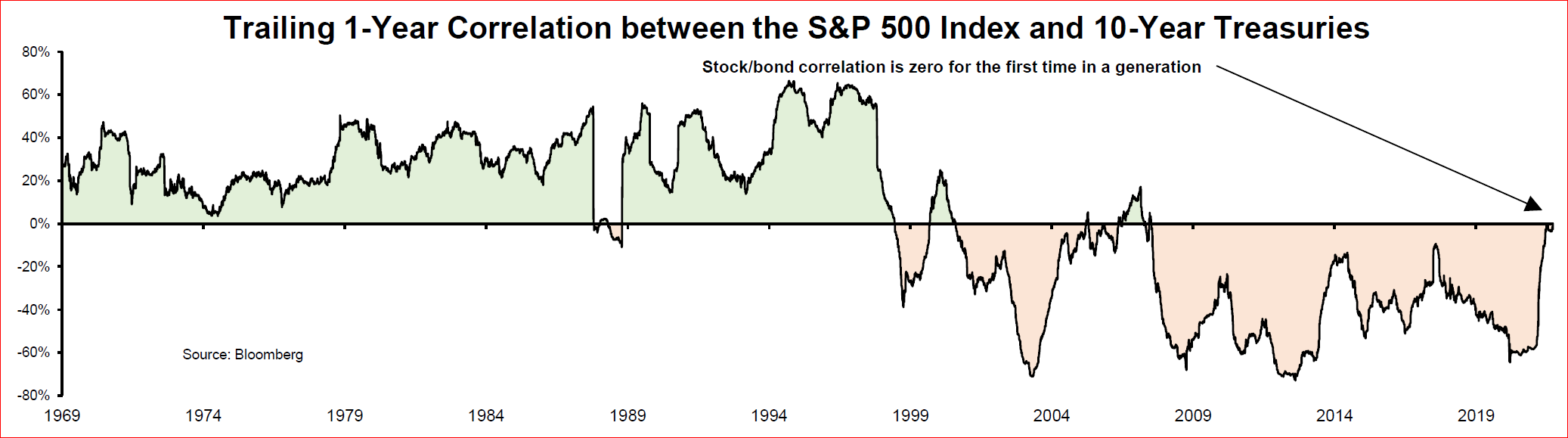

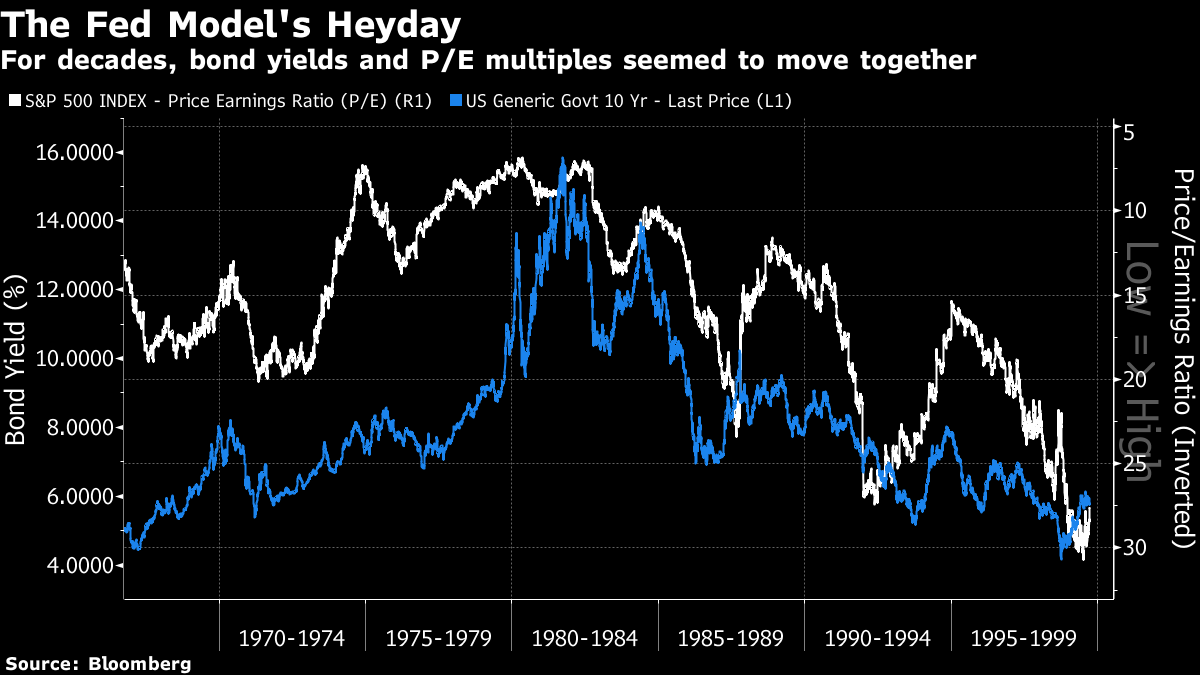

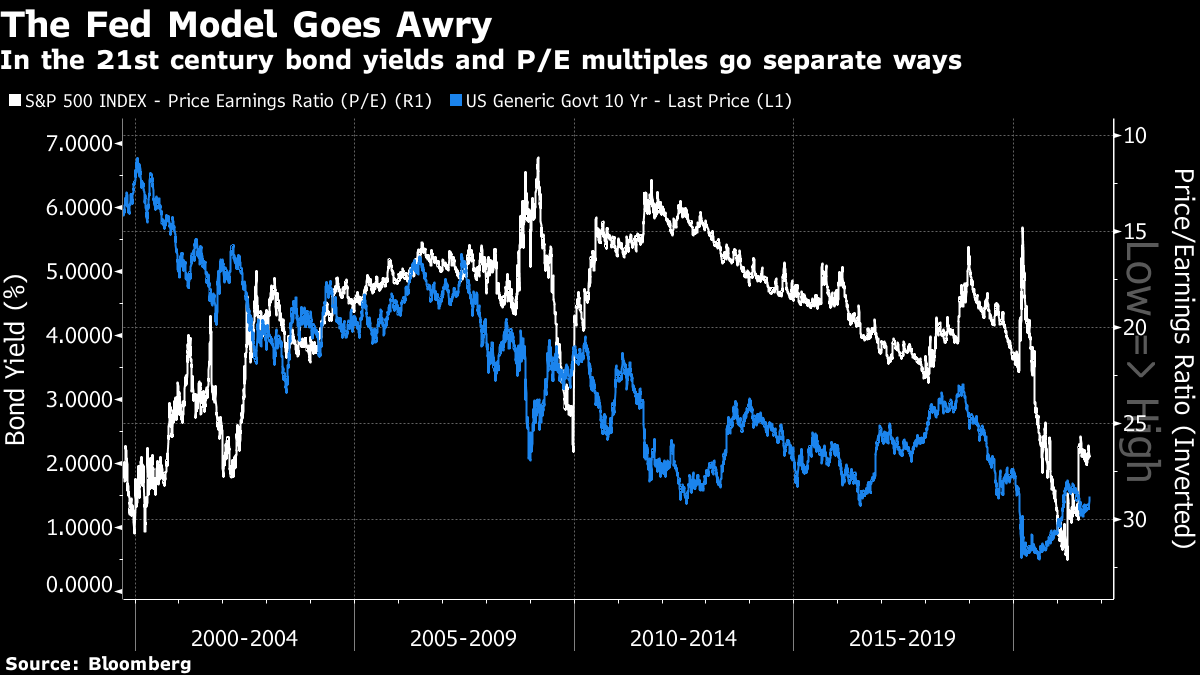

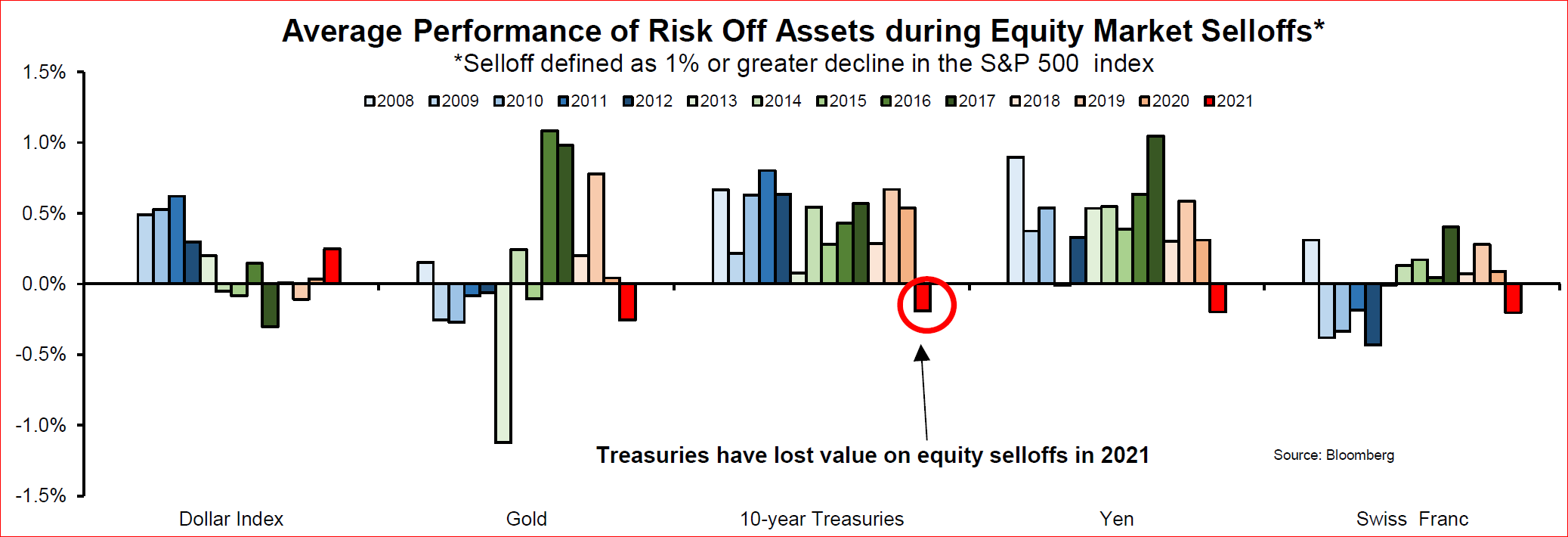

This wasn't a typical "risk-off" day, as we've come to think of them, in which money flows out of stocks and into bonds. The money flowing into the U.S. and out of the emerging complex shows concern about risk, but money is also flowing out of Treasuries. It's tempting to blame the machinations in Capitol Hill, where the president seems not to be exerting any control over the situation, and people on all sides are playing brinkmanship. Janet Yellen, the Treasury secretary, has now told us that the federal government will run out of the money it needs to service its debt on Oct. 18, which is uncomfortably close. On the face of it, that would explain a rise in bond yields. Except that in the first great debt ceiling crisis, just over a decade ago now, the exact opposite happened. The 10-year yield dropped to 3% from 3.5% in the months leading up to the Aug. 1 deadline for those talks in 2011. The debt ceiling was eventually raised, a few hours late, but then U.S. Treasury debt was downgraded by Standard & Poor's, the 10-year yield dropped all the way to 2% by the end of August, and fell further thereafter. When there was a perception of a serious risk, traders did what they usually do, and bought bonds (while selling stocks). This time around they are selling bonds. And frankly, if there really were thought to be a serious risk of a U.S. default within a matter of weeks, stocks would have sold off a lot more than they have. It's also tempting to blame the stricken Chinese property developer China Evergrande Group. Its commitments appear to be multiplying; Bloomberg News reported earlier this week that the company is the guarantor on $260 million of dollar-denominated debt which is due to mature at the beginning of next week. But traders seem to have lost interest in the situation. This is how Google Trends search interest in Evergrande has moved over the past week:  So if there is any signal to be extracted from any of this noise, I suggest it is about the intentions of central banks. Markets are waking up to the notion that central banks are starting to tighten monetary policy, and won't be as lenient as hoped. The dominant thesis these days is that Jerome Powell of the Federal Reserve wasn't really serious about "flexible average inflation targeting" when he announced the idea at Jackson Hole last year. The expressed intention was to allow inflation to run above 2% for a while, and stay accommodating as long as the Fed dared. But maybe he was only saying that because at that point there were still no vaccines, recovery was far from a given, and he needed to do something to build confidence that the Fed would be friendly, and that inflation would return. Now, with inflation running very hot indeed, the shift toward more hawkish policy is on. The following charts come from Deutsche Bank AG strategist Jim Reid, and show the balance between global central banks cutting and hiking within the last 12 months. Remarkably, central banks have been more aggressive in the last 12 months, on this metric, than at any time in almost a decade:  That would explain a desire to get out of both bonds and stocks. But why the move to the dollar? Capital Economics Ltd. of London suggests that this might have something to do with inflation tolerance. Countries with a lot of debt have an incentive to allow more inflation. Those that have spent a lot to get through Covid show themselves particularly willing to take the risk, and juice growth. And those who already have relatively high inflation also show more of a propensity to let it happen. That leads to the following heat map, which suggests the U.S. is the most obvious candidate to allow some inflation to take hold:  If any country is going to grow and allow some inflation in the process, it's probably the U.S. In the longer term, that suggests the potential for serious problems, if it succeeds too well and lets inflation take off. For the time being, the betting is that higher American tolerance for rising prices will translate into a longer period of permitting growth to run, but not into serious long-term structural inflation. While people believe that inflation won't be allowed to move out of control, maybe the shift higher in the dollar makes sense — but it's not an easy circle to square. The market's bad day may well have been little more than a random walk, in the greater scheme of things. There's a risk of being drawn into calling play-by-play on a ping pong game. But if investors want to focus on something, it should be that investors are latching on to the notion that central banks are beginning to end the party. And if there is one country where that could end in inflation, it's the U.S. If the price of both bonds and stocks go down together, how do you protect yourself? And, unfortunately, note that gold and its putative replacement bitcoin also fell Tuesday. It's a problem because throughout the post-crisis period nothing has worked as a better diversifier than bonds. And it's not new, although Tuesday's action was probably the most dramatic demonstration yet. For many decades, bonds and stocks were positively correlated (so yields would fall as stock prices rose). Then at the turn of the century that turned around as a succession of Fed presidents cut rates to help prop up asset prices. And now that strong negative correlation has also disappeared. This chart from Vincent Deluard, global macro strategist at StoneX Group Inc., illustrates what has happened beautifully:  This chart also shows us the reign of the Fed Model (the notion that price-earnings ratios and bond yields would follow each other, with lower yields permitting higher P/E multiples. It seemed so strong that Alan Greenspan himself seemed to be using it as a model. Hence the name:  This is what the same chart looks like, starting in 1999 and carrying on until today. There appeared to be a relationship at one point, but it changed utterly in the era of quantitative easing:  If we are returning to a world of higher bond yields and even higher inflation, asset allocation becomes more difficult. The problem is that nothing diversifies, in the last decade, as well as bonds. Throughout the post-crisis period, Treasuries have on average gone up on days when the S&P 500 has given up 1% or more. This isn't true of any of the other most obvious diversifying "hard currency" assets, such as the Swiss franc, the Japanese yen, the dollar index, or gold. The sad part, as Deluard demonstrates in this chart, is that this year Treasuries haven't done the job. Tuesday wasn't the first time this had happened:  Note also that the dollar has been the one successful diversifier this year (and was again Tuesday). That's not great news for emerging markets if the risk-off tone grows stronger. What might replace bonds as a diversifier? Deluard did some heroic research on this, but revealed what we might have expected: The assets that actually do well when the market goes down are risky. The most reliable candidates he could find, both of which have had long periods of poor performance in the last decade, were uranium and Japanese utilities. Both require a lot more due diligence than Treasury bonds. The bottom line: If we really are moving to a world where inflation is a genuine risk and central banks have to start behaving like they used to, risk management is going to get a lot tougher. Hope that helps. There are some things on which you can rely in life, and which provide lasting beauty. Lionel Messi fascinates me. It's sad in many ways to see him play for anyone other than Barcelona, but his first goal for Paris Saint-Germain (and for any club other than Barcelona) was a thing of beauty. I could watch this time and again. And if you have some time, read this early classic of statistical sports journalism. Rather like the physicist who proved that bees cannot fly, FiveThirtyEight proved seven years ago that Lionel Messi is impossible. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment