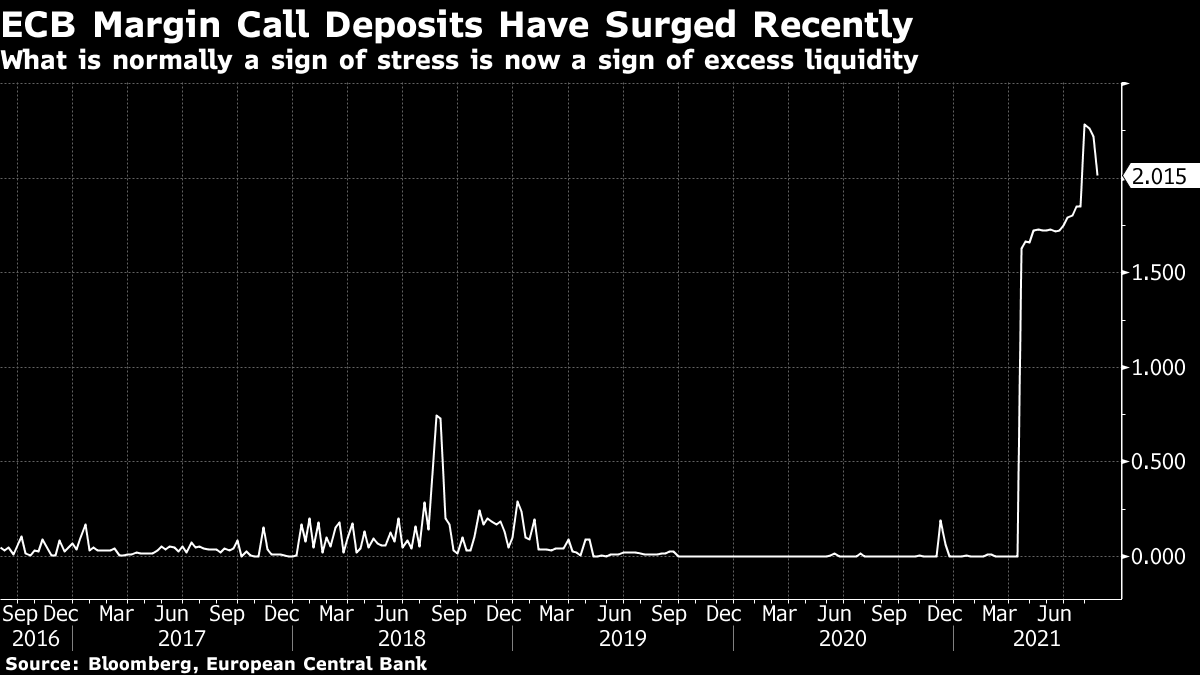

| Ida hits Louisiana, signs of slowing U.S. economy, and delta's resilience. There was an almost total loss of electric power in New Orleans as Hurricane Ida hit Louisiana with record-tying 150-mile-per-hour winds. The storm surge has caused the Mississippi to flow in reverse as vast quantities of sea water are forced ashore. Authorities remain confident that defenses which were upgraded in the wake of Hurricane Katrina will hold. U.S. gasoline prices jumped as operations at key refineries were suspended, while the price of crude is falling today as rigs in the area seem to have escaped significant damage. Federal Reserve Chair Jerome Powell said on Friday that while the bank could begin to reduce its monthly bond purchases this year, it would be in no hurry to hike rates. His comments came as there are increasing signs that the pace of the U.S. recovery is slowing as consumers put off spending and businesses delay plans for a return to normal operations. This week economists will be looking to Friday's payrolls report for a guide as to whether there is any slowdown, with early estimates suggesting 750,000 new positions added in August. The resilience of the delta variant of Covid-19 continues to cause problems around the world. Australia notched a fresh daily record for infections while New Zealand extended a lockdown in Auckland. In the U.S., public health advisors are meeting today to discuss booster shots as the White House continues to push for a Sept. 20 rollout. In some Southern sates hospitals are running low on oxygen as the region struggles with a high number of cases. Global equities are getting the week off to a fairly sedate start after Powell's much-anticipated speech failed to produce any fireworks. Overnight the MSCI Asia Pacific Index added 1.0% while Japan's Topix index closed 1.1% higher as tech shares in the region rose. In Europe the Stoxx 600 Index was 0.1% higher at 5:50 a.m. Eastern Time, with volumes low in the region as London is closed for a holiday. S&P 5o0 futures pointed to a small gain at the open, the 10-year Treasury yield finished the Asia session at 1.297% and gold slipped. U.S. pending home sales data for July is at 10:00 a.m. with the August Dallas Fed manufacturing survey at 10:30 a.m. President Joe Biden meets Ukrainian President Volodymyr Zelensky at the White House. Zoom Video Communications Inc., Nordson Corp. and Catalent Inc. are among the companies reporting results. Here's what caught our eye over the weekend. There is no doubt that financial markets these days are awash with liquidity as years of central bank support have added to the massive stock of cash globally. The main way policy makers have pushed all this into the system is through asset purchases, with central bank balance sheets expanding hugely in the past decade. But increasingly there are signs that they are either running out of things to buy, or running out of demand for cash. Nowhere is this clearer than at the European Central Bank where strange things are starting to happen at its liquidity operations. While the bank's asset purchases get much of the attention, its liquidity-providing operations have always been the backbone of monetary policy. The Targeted Longer Term Refinancing Operations currently provide more than 2.2 trillion euros of cash to the region's banks. Demand at the regular Longer Term Liquidity Operations, which provide money for three months has completely evaporated, with the July 1 scheme only attracting 3 million euros from one bidder. Even more unusually, banks are so flush with liquidity, they are now giving the ECB cash as collateral for the loans they receive. Yes, you read that correctly. Banks have borrowed money from the ECB -- and given the ECB the money back as collateral for the loan. We can see this in data provided by the weekly financial statement, which has a line item called "deposits related to margin calls." In any other time, an increase in this line item would be a sign of severe stress, as it would mean the collateral banks had posted with the ECB to secure their lending had fallen so much in value, the ECB has made a margin call -- think Greek sovereign bonds circa 2011. What the current rise is pointing to, though, is banks having nothing else to do with the cash, and by using it as security for the loan they get a handy interest rate income on the difference between the deposit rate of minus 0.5% and a TLTRO rate of potentially minus 1%. It also means that banks -- by giving the cash straight back to the ECB without doing anything else with it -- are effectively sterilizing a proportion of total liquidity the central bank provides. Monthly balance sheet data shows that the Bundesbank accounts for all of this "margin call" cash. It will be worth watching to see if this number disappears at the end of September when banks are allowed to start making early repayments on the cash they borrowed under TLTROs in 2019 and 2020. Follow Bloomberg's Lorcan Roche Kelly on Twitter at @LorcanRK Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment