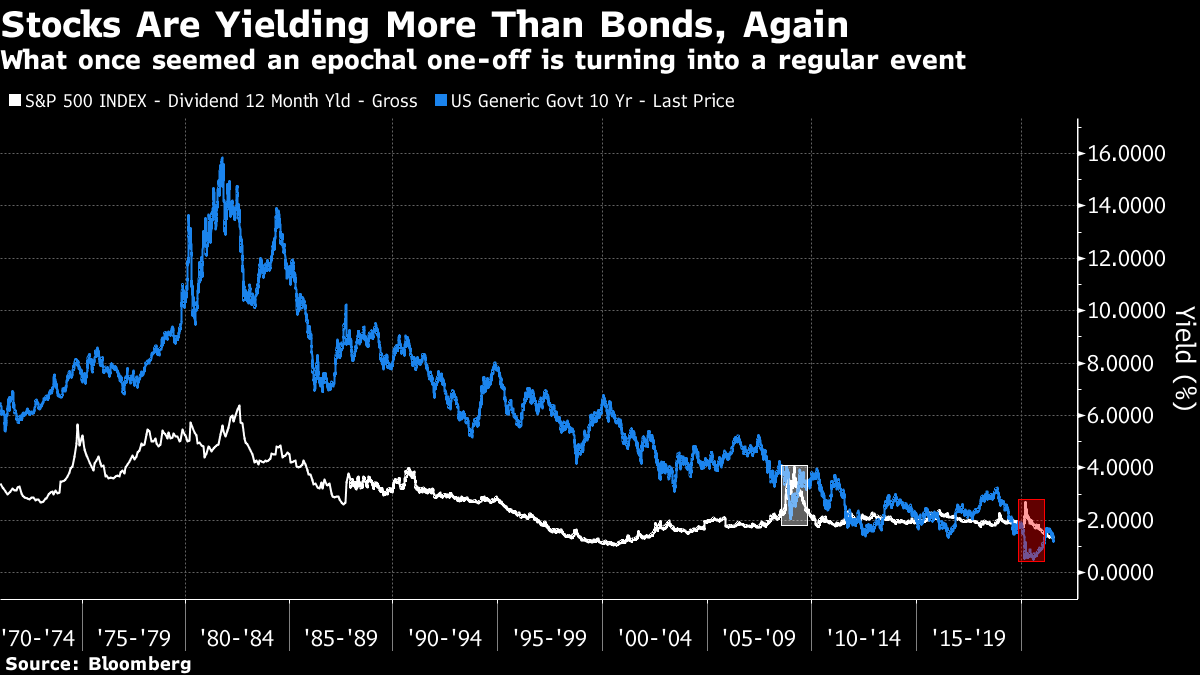

| When I tried to go through the different ways to value stocks yesterday, I omitted the simplest of all: dividend yield. At least it's easy to measure, with no controversy, and it allows for a simple comparison with bonds. Look at the cash yields available, ignore all possible future risks, and buy whichever pays more. Amazingly, if you follow this rule now, that means purchasing stocks. For more than half a century, 10-year Treasury yields exceeded dividend yields on the S&P 500. That was because stocks offered the possibility of growth, and bonds didn't. Therefore, the logic went for many years, stocks would of course have lower yields. Then, in early 2009, that reversed. It brought much speculation that the "cult of the equity" was over, amid deep disillusion. That turned out to be a fantastic signal to buy stocks. In the decade since, however, buying of bonds has been so heavy that the spread of fixed-income over dividend yields has never returned to anything like what we previously regarded as "normal." The lines crossed a few more times, and then last March, dividend yields again soared far ahead of bond yields. The two incidents are marked on the chart:  Is there any way to turn this into a timing strategy in real time? It turns out that there was. There have only been two occasions when dividend yields rose more than a percentage point above bond yields. Both times, once the spread turned, there were no second thoughts. The spreads swiftly tightened and soon reversed. The points when the spread reached its widest and then started to narrow are circled in the chart. Wait a week to make sure the spread was really reversing, then buy stocks while shorting bonds, and you would have done fantastically both times. In 2009, there was a 68% return over the next 12 months, while last year the 12-month return was a scarcely believable 94%. To be clear, in both cases this assumes waiting until a week after the widest spread before buying:  The problem with this crude but simple measure is that while it's effective, it's only flagged two buying opportunities in the last 70 years. Both came at the end of extreme stock-market selloffs, when fear was rampant and had utterly overcome greed. Such moments don't come around often. Now we come to the awkward part. As of this moment, dividend yields have overtaken bond yields once more. Last year and in early 2009, this was a moment driven by a historic collapse in share prices and a wave of risk aversion. This time around, it's happened just as the U.S. stock market is setting yet more all-time highs. Despite this, equities are currently paying a yield in cold hard cash that is slightly higher than what you can get from bonds. To be clear, the current spread is nothing like the big excess in favor of dividend yields in the historic circumstances of 2009 and 2020. But it does suggest something very strange is afoot. Back in 2012, dividend yields crept back up above bond yields again, prompting some suggestions that a new cult of the equity was at hand, and other claims that capitalism itself had been called into question. The former turned out to be more accurate. This time around, it's hard to imagine that another historic stocks rally is ahead of us (famous last words); once more, with intervention helping to hold bond yields so low, it appears that capitalism is being called into question. Earnings season is with us again. It looks likely to provide another "beat" compared to expectations that doesn't push the market far upward on its own. More importantly, it could tell us a lot about a couple of key trends in global markets. First, inevitably, there is inflation. Companies are talking about it a lot in earnings calls, and are providing much evidence for the notion that real inflationary dynamics are building.

Analysts will doubtless dredge these calls using machine learning, and give lots of precisely quantified measures of inflationary pressure. For now, I will offer some chunky straight quotes. The following were all cited in the latest earnings note from BofA Securities Inc.'s Savita Subramanian:

Fastenal Co (Industrials): "Price actions to-date have largely matched cost increases. There's a ton of inflation going on. There's inflation because of disruption and shipping" "The marketplace is still receptive to price actions and the tools and processes we have developed have been effective. Even so, given the rate of inflation, maintaining price cost parity will be a bigger challenge in the third quarter." Conagra Brands Inc. (Staples): "We expect the negative impact of the cost inflation to hit our financials before the beneficial impact of our responsive actions, including our pricing. This timing mismatch is expected to be particularly impactful in (fiscal) H1 and, more specifically, in (fiscal) Q1. The resulting pressure on our first half margins impact our full year profit […] Although the substantial increase in inflation over the last few months has negatively impacted our profit guidance for the (fiscal) year, we remain confident in the underlying strength of the business..." "When we initially gave our fiscal 2022 targets at our Investor Day in April of 2019, our models assumed an annual inflation rate of around 3%. At the time of our third quarter call, in April of 2021, we expected fiscal 2022 inflation to come in at twice that level around 6% […] We now currently expect fiscal 2022 inflation to come in around 9%." McCormick & Co Inc. (Staples): "We're seeing broad-based inflation across our various commodities, packaging materials and transportation costs. To offset rising costs, we are raising prices where appropriate, but usually there is a lag time associated with pricing, particularly with how quickly costs are escalating. And therefore, most of our actions won't go into effect until late 2021." PepsiCo Inc. (Staples): "We're seeing inflation in our business across many of our raw ingredients and some of our inputs in labor and freight and everything else. So, we operate in the same context. We feel quite comfortable or confident that through a combination of net revenue management initiatives and increased productivity, we can navigate this." Cintas Corp. (Industrials): "While some inflationary pressures increased certain costs, these were more than offset by increased revenue from businesses reopening or increasing capacity as COVID-19 case counts fell and restrictions on businesses were reduced."

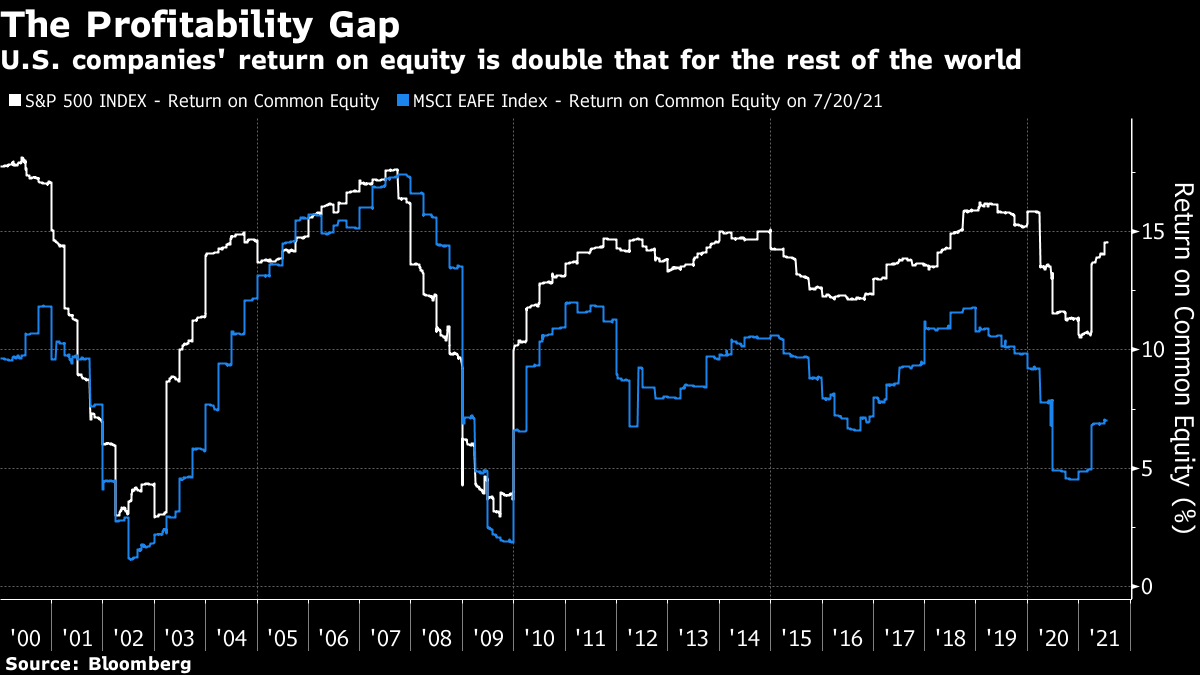

Bloomberg News also reported this bleak assessment from PPG Industries Inc.: "This inflation cycle is much higher than anyone anticipated and we're continuing on a business by business basis, working to secure further selling price increases"

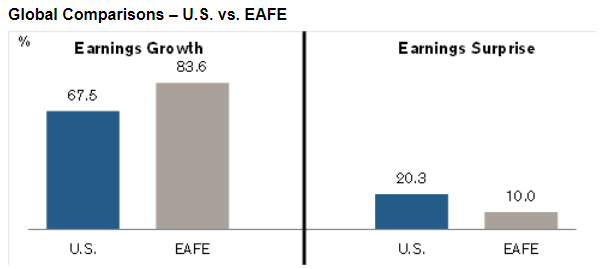

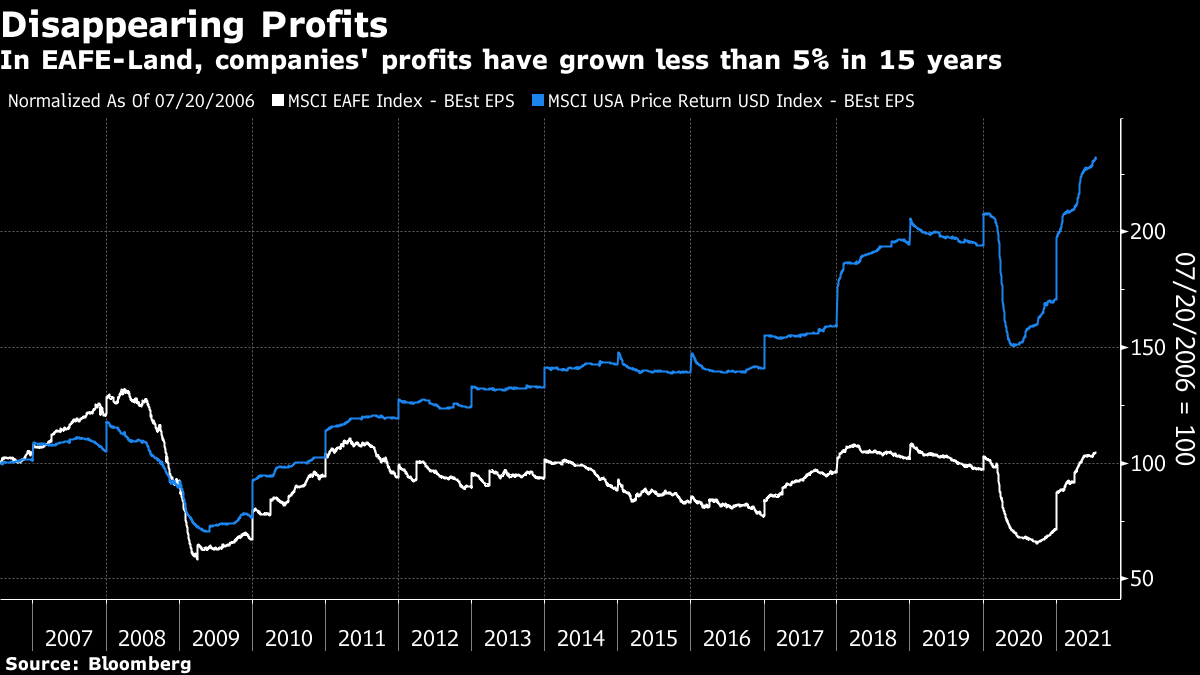

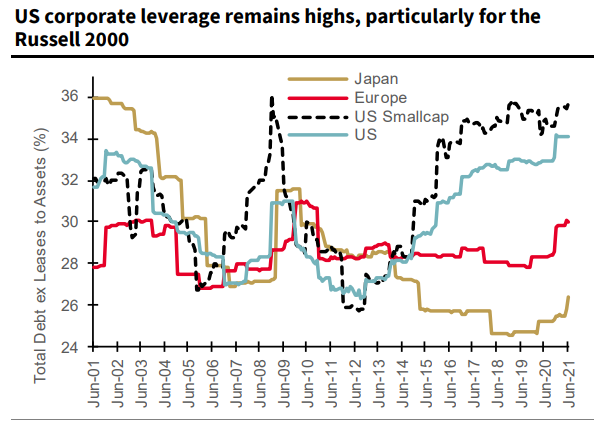

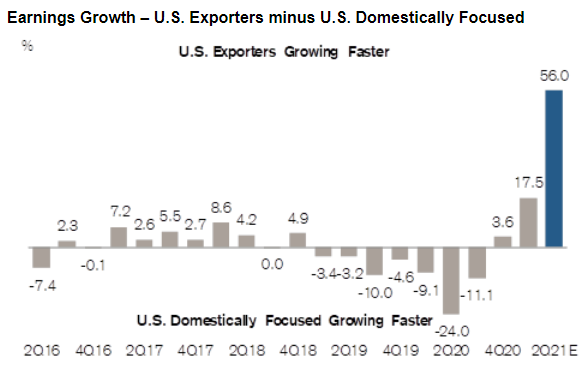

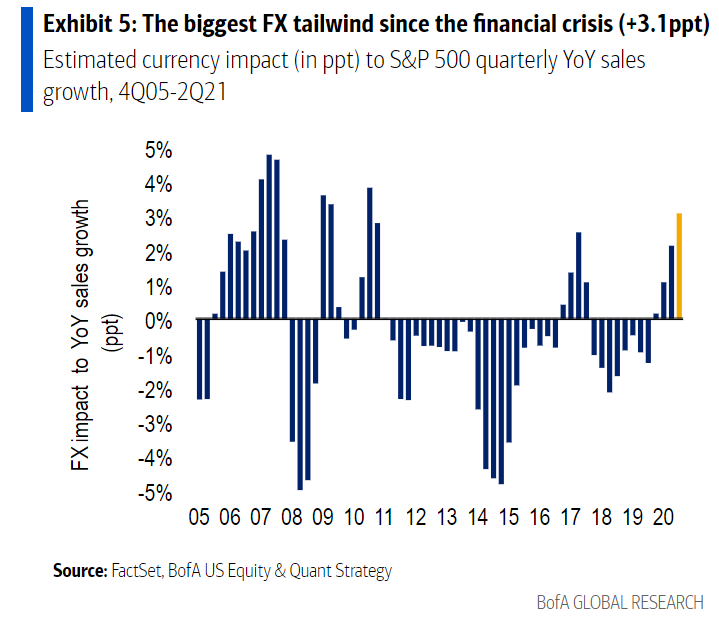

Executives are contending, for the most part, that they can still deal with this, as far as their shareholders are concerned. That is another way of saying that they are confident they can get their customers to pay more. When it comes to stockpicking, companies that can demonstrate pricing power (which Warren Buffett might call those with "wide economic moats") should do relatively well. Any doubt that a company will be able to pass on higher prices will be punished. When it comes to the macro-economy, anecdotal evidence so far suggests there is higher inflation in the pipeline than executives who rely on specific markets and supply chains had expected. What we discover about cost pressure (or the lack of it) this results season could well be more important for markets in the long run than the earnings themselves. The other big theme of this earnings season could be globalization. The expectation seems to be almost universal that more profit growth is going to come from countries outside the U.S. This is true both for non-U.S. businesses, and for American companies deriving earnings internationally. Oil's rebound has much to do with this. U.S. companies doing most of their business overseas include big energy groups whose profits and sales are going to be a lot higher than 12 months earlier. What is more intriguing is the projected improvement for non-U.S. companies. These figures are from Credit Suisse Group AG's U.S. equity strategist Jonathan Golub, and show both expected earnings growth, and surprises compared to expectations to date:  The percentage growth numbers are enormous. Nobody should extrapolate them into the future. The main reason for the disparity is that the U.S. started reopening earlier than most other developed countries, so second-quarter 2020 earnings weren't quite as spectacularly depressed. However, if we look to the longer term, we see a deep-seated trend. The following chart shows Bloomberg's projected earnings per share for MSCI's Europe, Australasia and Far East index, and its U.S. index (which is very similar to the S&P 500). Both are rebased to start 15 years ago. In that time, U.S. earnings have comfortably more than doubled, and EAFE earnings are basically flat:  The single biggest reason is that the global financial crisis carried on much longer in EAFE-land, thanks to the EU sovereign debt mess. That shows up in one of the critical reasons for U.S. companies' superior profits, which is that they have made massively more use of leverage. The following chart, from Andrew Lapthorne of Societe Generale SA, shows debt as a proportion of assets for Japan, Europe, the U.S. and the Russell 2000 index going back to 2001:  American companies are far more heavily levered now, but this has only been true for the last seven years or so — a period in which they have enjoyed the benefits of a healthy banking system and a credit market that showers money on them. More debt also helps boost profitability as measured by return on equity. Here again, American companies showed no particular advantage in the years leading up to the GFC, and suffered equally in 2008 and 2009. But they have opened up a wide gap since then:  Leverage doesn't explain everything. Numbers like this will feed into the intensifying U.S. debate over competition policy. If industries have been allowed to grow over-concentrated, and the FANG internet platforms have been allowed to establish well-defended monopolies, then that would show up in improved returns on equity. That still raises the issue of why EAFE companies make only half the ROE that American companies do. Plenty of them also have well-fortified competitive positions. To the extent that the issue is the sluggishness of their home economies, current expectations suggest that the world beyond the U.S. is about to become a happier hunting ground. One factor in the rebound of the last 12 months has been to improve the fortunes of U.S. exporters (led by energy). The market, according to Golub of Credit Suisse, is braced for exporters to have a historically fantastic quarter compared to domestically focused companies:  Another factor helped exporters in the second quarter: The dollar was substantially weaker than a year earlier, automatically flattering any overseas profits. U.S. exporters have had serious currency headwinds for most of the post-crisis period. In the second quarter, the dollar helped them more than at any time in a decade, as this chart from BofA's Subramanian shows:  The dollar's shift should ensure that U.S. companies carry on looking better than the rest of the world. The continued generosity of U.S. credit markets does them no harm for the time being either. But the critical questions concern what the non-U.S. corporate sector can do to raise profits and profitability. In an increasingly globalized system, the advantages have increasingly accrued to American companies. How long can it go on? I'm getting more musical tips from readers these days, which is great for the soul. To start with, I've offered a couple of women singing Led Zeppelin already, including Alison Krauss and the wonderful Jess Greenberg. Now try Zepparella playing When the Levee Breaks or my personal favorite Zeppelin track, Immigrant Song. They're extraordinary. The yodeling at the beginning sounds even better when a woman sings it. Shifting to jazz, for a very different take on It Ain't Necessarily So that uses it as a theme for many extemporized variations try this version by Herbie Mann at the Village Gate, or for a clear and very trad jazz telling of the tale of St James Infirmary, try Danny Barker.

Finally, Apple Music has been prompting me again. One of my favorite Waterboys songs is Island Man; it's short, it's a paean of praise to the British Isles (even though it starts with a didgeridoo), and it's fun.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment