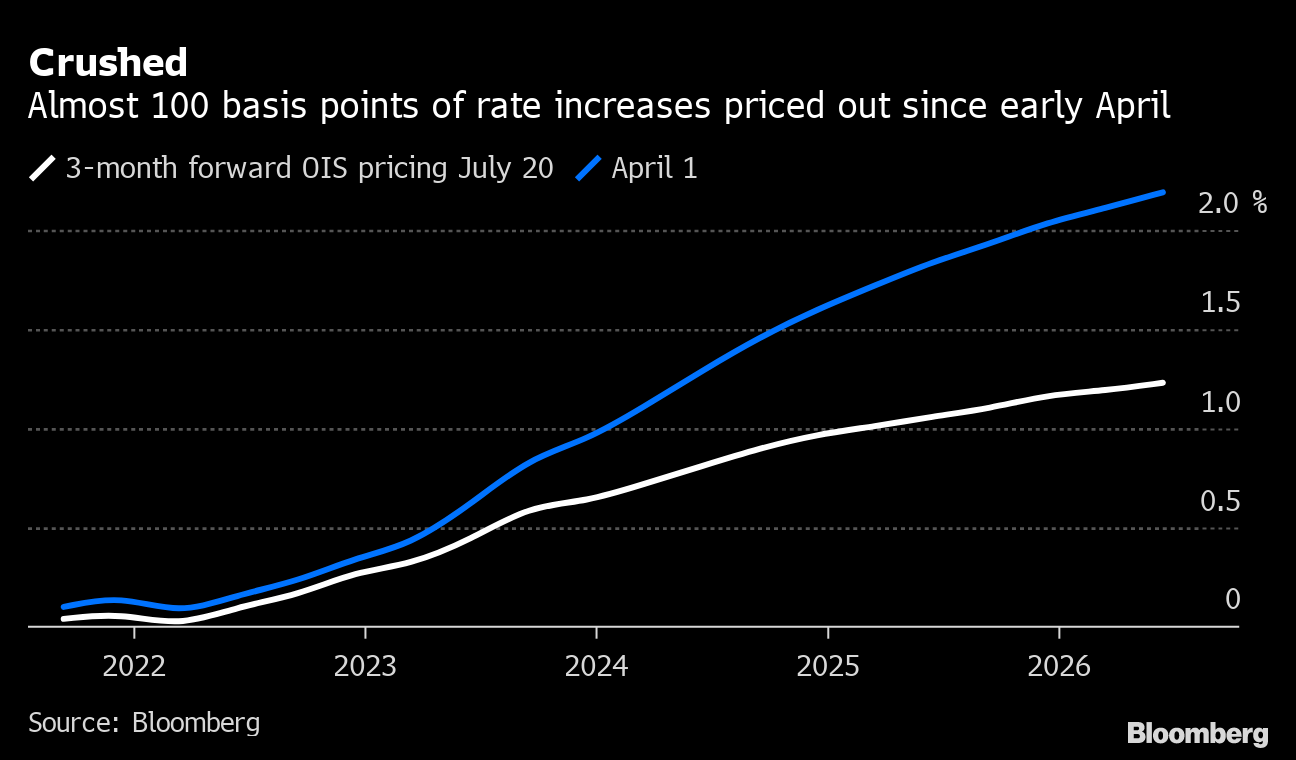

| Some say if you print it out, the words will disappear, and if you read it aloud in the mirror you see where stocks will close in the third quarter. All I know is, it's called The Weekly Fix. I'm Stephen Spratt from the FX/Rates team in Hong Kong. It's not nice being wrong. But what about when you're kind of right but still wrong. Then, what about if it costs you money being wrong. Well, that's been happening a lot in Treasury markets over the past two months. This week was another volatile one:  An uptick in global coronavirus cases and fears this could morph into lock-downs lit the fuse for another big week of bond volatility. Benchmark 10-year yields fell to just 1.13% at one stage, in what was the largest one-day drop in almost five months. That's tough to digest when there was no major data related to the main drivers of bonds -- the growth and inflation outlooks -- which are both on a strong path. For instance, the Federal Reserve Bank of Atlanta's GDPNow index is forecasting growth of more than 7.5% for the second quarter. Even Federal Reserve officials were quiet. They're observing a black-out period ahead of next week's meeting, so they can't talk publicly on policy. Though, you can count on certain officials rushing to the microphones as soon as it ends, in what has to be the least camera-shy Fed ever. Strategists are pulling their hair out as they've mostly been recommending shorting bonds -- betting on yields to rise -- as all of their fair value models say this is what should happen. These models are based on fundamentals, so they plug in their growth and inflation expectations, the Federal Reserve outlook and some other bits and bobs, and it spits out a number. They compare that number to yield levels. For example, Analyst A says benchmark yields have a fair value of 1.70%, and the market is at 1.40%, you should sell bonds. But none of that mattered on Monday, when bond yields dropped as much as 12 basis points to hit the lowest levels since February. Positioning -- specifically, short positioning -- and other technical factors were king, not fundamentals. It wasn't just Analyst A saying sell bonds, it has been almost everyone. And when participants are all scrambling to buy back shorts, the price or the fair value doesn't really matter. Interest-rate swap markets have now priced out close to 100 basis points of hikes since early April -- that's a big change, when there was only just over twice that priced in to start with. The level of yields looked so extreme it briefly began to raise the question of IF -- not when -- the Federal Reserve would ever raise rates. Does that sound right? Probably not.  When things get volatile, liquidity tends to worsen as investors dial back risk-taking activity. Less liquidity means it gets a bit more difficult to trade and when you do trade, the market impact can be greater than usual, which leads to directional moves being more extreme. The good folks at JPMorgan Chase & Co. reckon conditions have worsened back to levels seen in late February -- when a pretty big sell-off gripped Treasury markets -- and it's highly likely this has exacerbated the latest move. For me, I'm talking. I speak to a bunch of different traders and one regular frustration is a legacy beef with analysts. The main reason for this is, analysts have calls, but no skin in the game. You can have diamond hands when it's all just paper trading. But that's the analyst's job: provide some rigorous analysis -- like the fair value models described above -- give fresh ideas, inspiration and some trades that might work. But that doesn't calm down some traders and that's because when they're wrong, money, jobs and bonuses can be lost. When analysts are wrong, they can explain why, engage in some mental gymnastics and then move on. "Must be nice," one rates trader in Asia once quipped to me, when a bank strategist flipped a long held view on the Fed's reverse repo facility. Markets are humbling for everyone sometimes. Everyone. There are tons of Wall Street banks with particularly unfortunate calls on Treasuries, European bonds and global interest rates so far this quarter. Even those who've eventually been right have had to ride out such deeply loss-making moments that it would make the most seasoned risk manager balk. Let's turn finally to leverage, which is at the heart of most crashes. Archegos, Long Term Capital Management, Great Financial Crisis of 2008, even the 2008 Honda I bought on finance after I got my first job out of school. And that's why people take it so seriously. This week, a group of banks in Hong Kong looked at the world's most indebted real-estate developer and blinked. They stopped providing mortgages to buyers of the China Evergrande's unfinished residential properties in the region. While the Hong Kong market is tiny for the group, the message was heard everywhere. Last month, Bloomberg also reported that several large Chinese banks were looking to cut lending to the group. China Evergrande stock has tanked some 20% this week, hitting the lowest levels since 2017 as fears of a default begin to bite, stoking concerns about financial contagion. The firm's dollar bonds hit record lows too. It had $302 billion in liabilities last year, and has been trying to make amends by offloading assets and cutting back debt as well as offering blitz sales discounts on new units. One to watch. Billionaires like zero gravity Less IPO more IP'Doh! ECB's last hiker says beware The Olympics is good for fried chicken |

Post a Comment