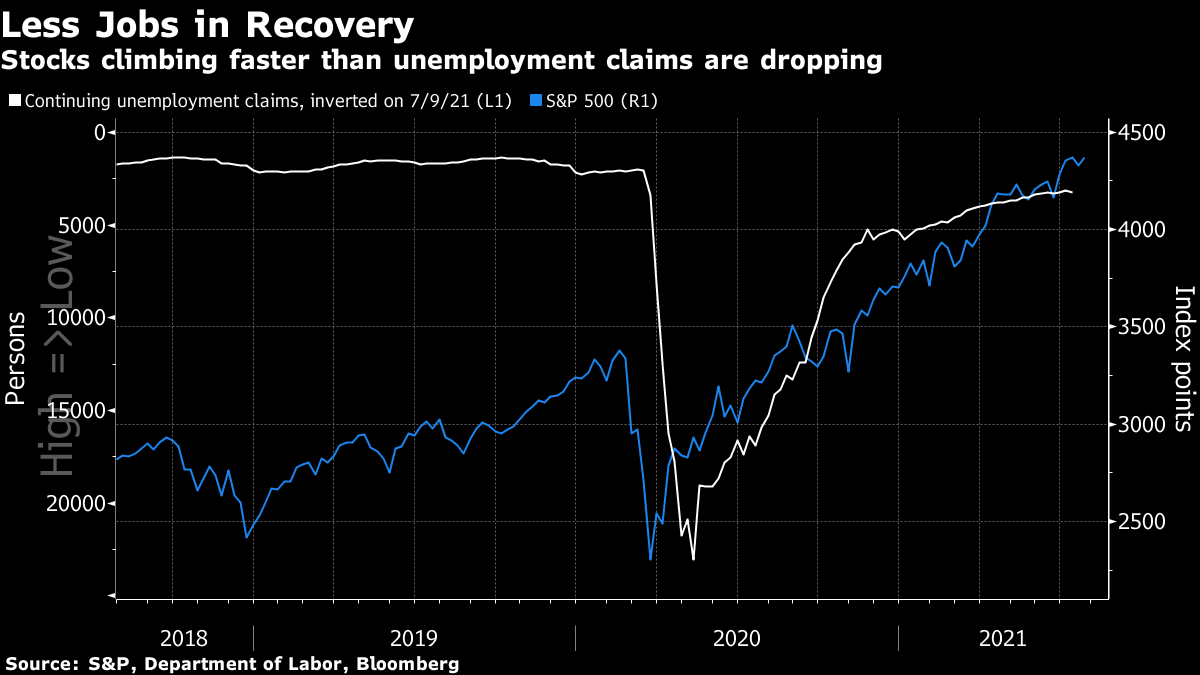

| Good morning. A giant private equity fund is in the making, the ECB changed its guidance, vaccine misinformation threatens the U.S. recovery and a clash over the Northern Ireland Protocol is brewing. Here's what's moving markets. The largest-ever private equity pool is in the works, with Carlyle Group looking to raise as much as $27 billion for its latest flagship fund. A lack of yield is playing into the hands of funds investing in unlisted securities or taking companies private as investors seek returns in alternative assets. The race for scale in the industry is intensifying: Hellman & Friedman this month raised $24.4 billion, near Blackstone's $26 billion record from 2019. The European Central Bank tweaked its guidance on Thursday, allowing it to keep rates lower for longer and extend bond purchases. This was the first policy meeting since the ECB lifted its inflation target to 2%. President Christine Lagarde says the ECB has learned from history and won't tighten early. Divergences among central banks are becoming more apparent: the Federal Reserve and the Bank of England, for instance, are inching toward paring stimulus. Unproven claims about alleged side-effects of coronavirus shots are causing vaccine hesitancy in the U.S., threatening to prolong the health crisis. Cases are rising in the world's largest economy, especially in areas with low vaccination rates, raising concerns about the rebound in travel and economic activity. President Joe Biden has urged Facebook to tackle misinformation and encouraged more Americans to get inoculations. The post-Brexit relationship between the U.K. and the EU is set to be tested once again over the Northern Ireland Protocol on customs checks and procedures. The European Commission is planning to file a "reasoned opinion" on what it sees as U.K. breaches of the protocol, which Britain says is causing trade disruption between Northern Ireland and the rest of the U.K. This comes as the EU has refused to renegotiate this part of the Brexit deal. European stock index futures point to another positive start, ending a week that featured generally strong corporate profits and stimulus support. Preliminary PMI figures for July are due, with economists expecting the euro area composite reading to rise further. The U.K. composite number is seen lower compared to June due to projected moderation both in manufacturing and services activity. In corporate earnings, telecoms giant Vodafone will publish a trading update. This is what's caught our eye over the past 24 hours. Dip-buyers almost erased the slide in equities that broke out as concerns increased about the global resurgence in the pandemic. The highly infectious delta variant is still driving lockdowns in Australia, South Korea and elsewhere, but investors are doing their best to put those fears behind them. It's possible the virus surge simply provided an excuse for some who were fretting that record-highs in stocks might be harder to justify amid mixed economic signs. While the inflation conundrum has sucked up most of the oxygen, labor markets could be of greater concern. Total employment remains well shy of pre-Covid levels in the U.S., Europe, U.K. and Japan -- and the gap is even wider to where jobs would have been without the pandemic. The latest U.S. data underscores the potential that the recovery will stall as employment gains slow. If that trend persists, equities may struggle to keep marching higher.  Garfield Reynolds is a markets reporter and editor for Bloomberg News in Sydney Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment