On Goalkeepers, Activity Bias and EmbarrassmentYou never know what will interest the readership. Summer is here, the markets appear already to be becalmed again after a brief spurt of excitement over the Federal Reserve, and the European soccer championships have finished their opening stage. And goalkeepers are in the news. Last week, I suggested that this goal, scored past Scotland's David Marshall, might go down as the most embarrassing conceded by a goalie in the tournament. I already stand corrected. That prize should instead go to this, scored (into his own net) by Slovakia's Martin Dubravka. It's hard, after watching it many times, even to work out what he was trying to do. Meanwhile, much of the readership seems to want to discuss goalkeeping. How does this job matter to Points of Return readers? Behavioral finance has unraveled the importance of "activity bias" — the feeling that it is better to do something, rather than nothing. In a crisis, this can lead to disaster, as people sell at the bottom. Churning a portfolio generally incurs extra costs without generating any extra return. But it still seems better than just staying put and doing nothing. One of the classic studies of activity bias relates to goalies in soccer. When trying to save a penalty, they generally dive one way or another, thus making it that much easier for the striker to score just by kicking the ball straight through the middle. But standing still and watching the ball hit the corner of the net is felt to be more embarrassing than diving dramatically while the ball goes right where you were just standing. Back in 2008, a report by a group of Israeli psychologists, summarized here, revealed that goalkeepers suffered from activity bias. In a sample of 286 penalty kicks, they were found to dive 94% of the time, even though the statistically optimal approach would be to stay put. There are arguments against this. Soccer players adapt, much as markets do. Once the word was out among strikers that it might make sense just to bash the ball forward, so goalies grasped that it would be a good idea to stay in the middle every once in a while. Thus an anomaly was corrected. Research published by The Economist looking at 434 penalty kicks taken in World Cup and European Championship games shows that kicks taken low and to the center (the kind designed to take advantage of the goalie's activity bias) were the most likely to be saved. Despite this, strikers tried such kicks 10% of the time.

Forwards had adapted, but so had goalkeepers. And strikers also had to contend with the desire to avoid embarrassment. For every masterly straight penalty by Antonin Panenka or Zinedine Zidane, there is an attempt that goes embarrassingly wrong, as most famously happened to England great Gary Lineker when he tried it in a penalty that would have given him a share of the all-time scoring record for England. He never scored an international goal again. Once the strategy of kicking the ball straight ahead was out there, the downsides for strikers also steadily became apparent, along with the need for goalies to adapt.

That is what investors try to do all the time. The dilemmas for goalkeepers and forwards are very similar to the dilemmas for investors contemplating new strategies. Regular correspondent Dec Mullarkey, who heads Sun Life Capital Management in Wellesley, Massachusetts, made this point: If the goalkeeper adopts standing in the middle as their default then the strategy is no longer effective. The option that the keeper randomly shifts complicates it for the kicker and heightens the risk they will make an error. Which somewhat circles back to the Efficient Markets paradox. If every market agent is furiously looking for mispricing opportunities then there is no value for you to get active as the market fully reflects all information. In fact you save the costs of research and do better. But if everyone becomes a free rider and no one is rigorously vetting prices there is a massive advantage to actively researching.

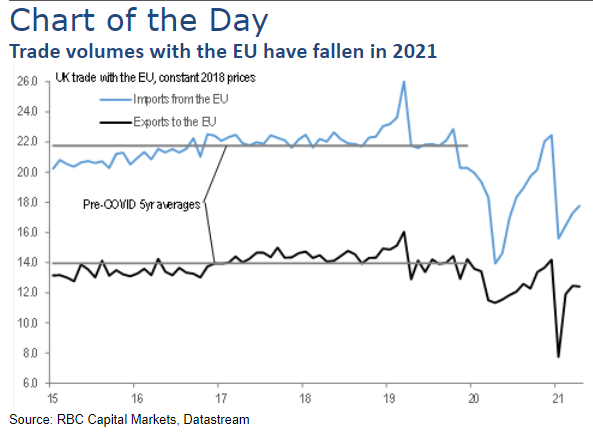

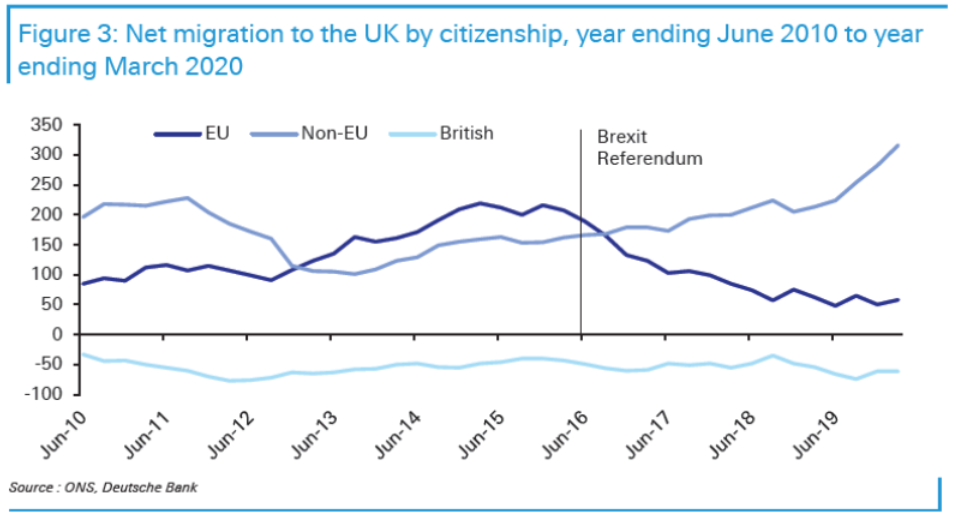

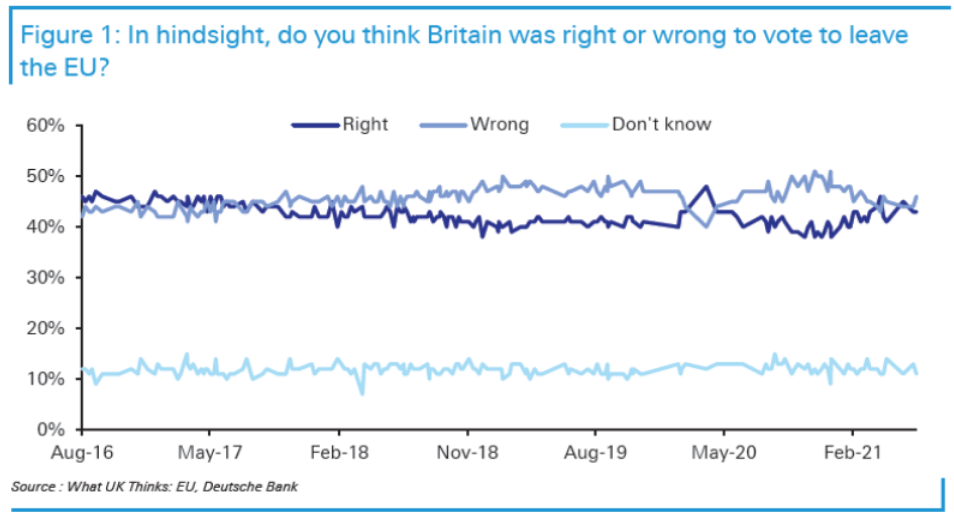

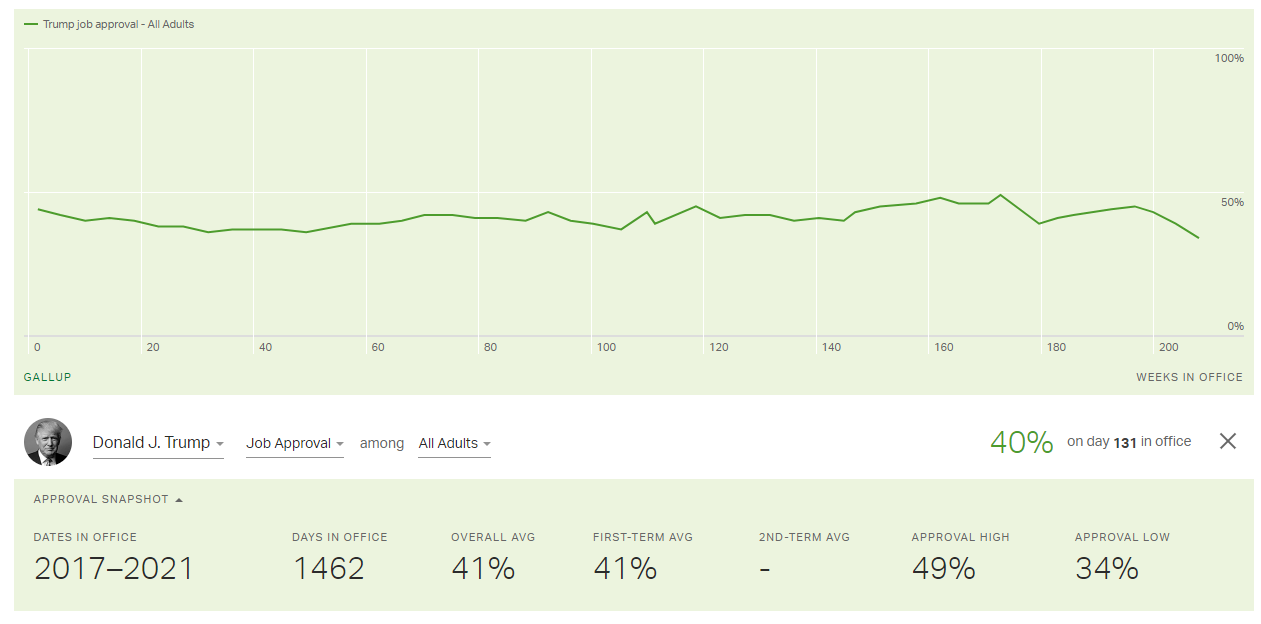

This is what might be called the "peak passive" argument. At some point, logic dictates that so much money will be invested passively there will be a huge advantage for those who try to spot anomalies. The phrase "peak passive" cropped up in the literature a few years ago, and logically it will come at some point. But exactly where remains a matter of conjecture, not susceptible to empirical research; I've heard suggestions that it's already here, along with theories that 90% of assets could be run passively and we would still have adequate price discovery. This leads to another risk, which is narrative fallacy. We think in terms of stories, and we hold on dearly to those that appeal to us and have a moral of which we approve. Peak passive is a story that many people badly want to believe. That doesn't make it so. Similarly, the narrative of inactive goalies is appealing, because many of us enjoy watching or playing football, and this gives us a chance to apply it to the rest of life. But it isn't that simple. The story is a warning to us not to act just to avoid embarrassment — but the appalling fate of Marshall and Dubravka (just take a look at the memes that are already spreading about them) reminds us that there are few things we want to avoid more. It doesn't suggest that there is a great argument for masterly inactivity. Rather, there is a great argument for studying how others behave in a competitive environment, spotting patterns in their behavior, and adjusting accordingly. It isn't the perfect fable it at first appears. But on a hot summer's day, with an England vs. Germany knock-out game at Wembley once again looming, it fits the bias of some investment newsletter-writer to write about football, rather than investment. And I think I've got away with it. Masterly inactivity rules again! Brexit's AnniversaryAs trailed yesterday, this has been the fifth anniversary of the U.K.'s Brexit referendum. As I type this, it is exactly five years since I spent one of the more eventful evenings of my professional life in a New York newsroom trying to cover both the electoral earthquake at home and the extraordinary moves in foreign exchange trading in Manhattan. The market reaction so far, as covered yesterday, has been a calm and straightforward downgrade of the U.K.; not a disaster, but also nothing that suggests that people with money at stake think that Britain is going to be better off for leaving the European single market. As for the question of whether the country will change, for better or worse, it is still far too early to say. The U.K. only left its old trading agreement with the European Union at the beginning of this year, and the effects of the pandemic have likely swamped any effects from the change in trading status. However, Adam Cole, foreign exchange strategist at RBC Capital Markets in London, offers this chart of trade between the EU and the U.K., and it does show volumes that are still below the five-year pre-Covid average. There's still a lot of noise, but it doesn't look good so far:  Judging by the campaign, immigration was a more important issue than trade rules. On this, Jim Reid of Deutsche Bank AG offers this chart, showing there have already been significant changes, with a sharp drop in immigration from the EU. The mere prospect of Brexit seems to have been enough to deter EU nationals from coming to work in the U.K. However, those immigrants have been replaced, almost on a one for one basis, by people from elsewhere. For those who wanted lower net total migration, leaving the EU doesn't look to have been a panacea thus far:  It will be a while before there is any clear judgment. As for public opinion, what is remarkable is how little it has changed, and how closely matched the pro-and anti-Brexit camps remain (just as the referendum itself was very close). Here is Reid's chart of polling on the Brexit question since the referendum:  It is almost chilling that so few people have changed their mind. After a general election, people are often willing to decide that the party they voted for doesn't deserve their approval. In the specific, divisive case of Brexit, the number of Britons adjusting their view was tiny, even though they were deluged with new information and commentary about it for five years. This looks very similar to the way public opinion moved after the other great populist electoral revolt of 2016, the election of Donald Trump. Here is Gallup's chart of his approval rating throughout his term:  Despite four years of high political drama, very few people ever changed their minds about him. Throughout his term in office, the nation was split almost 50/50, just as has happened to the British with Brexit. 'Twas not ever thus. Gallup's nifty site allows comparisons with earlier presidents, and none of the post-war presidents have an approval line quite as horizontal as Trump's was.

It's hard to see that either of the great electoral surprises of 2016 have had either the positive or negative consequences that were predicted for them, at least in hard economic numbers. But the sense of deep and fixed polarization was real, and it has persisted. That does tend to make any given political risk out there that much greater.

Survival TipsSome soccer-related reading. For readers who weren't brought up on soccer, I recommend Football Against the Enemy, by my former colleague Simon Kuper — it's a record of his journey around the world watching soccer in dozens of countries; Futebol by Alex Bellos, on the phenomenon of soccer in Brazil; and Fever Pitch by Nick Hornby, a memoir of his love affair with Arsenal, which revolutionized sports writing. It's wonderful reading even if you dislike Arsenal. All three books can be read like a novel, in a hammock. For those who were brought up on football, I recommend And Gazza Misses the Final by Rob Smyth and Scott Murray, a compendium of historic matches that they watched and live-blogged in real time. If you like football, it's the literary equivalent of a large slice of cheesecake washed down with a pina colada. Decadent. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment