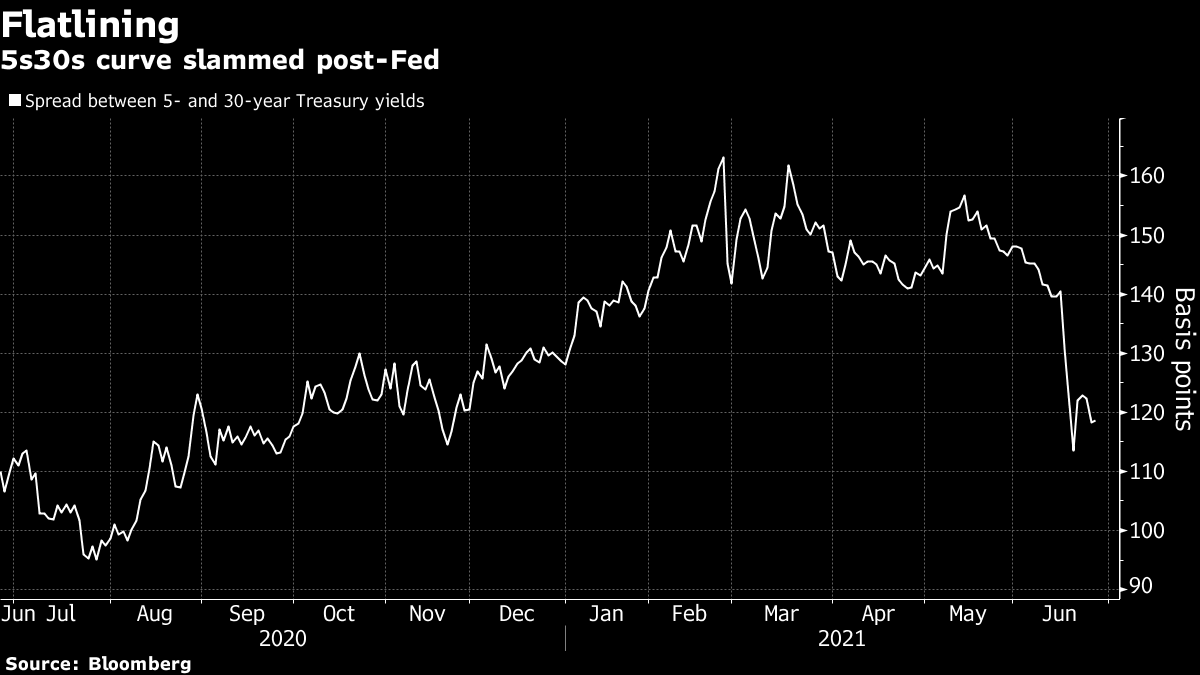

| Biden's next challenge, inflation debate and data, and vaccine push continues. Deal President Joe Biden announced an agreement on infrastructure spending of $579 billion with a group of bipartisan senators. The package, a carve-out from Biden's $2.25 trillion American Jobs Plan unveiled in March, is heavy on road upgrades, with rail also a winner — getting more spending than broadband. While the plan will still face opposition in Congress, the big prize for Democrats will be to get the rest of Biden's spending plans through under budget reconciliation procedures that would not require Republican support. Inflation debateIt's already been a very, very busy week for comments from Fed policy makers. The one thing that is becoming increasingly clear is that officials are split. Those such as Chair Jerome Powell believe inflation will head back towards target in 2022; others view Fed action next year as necessary. This morning's PCE deflator — the Fed's preferred measure of inflation — may show a pick-up to 3.9%. After that data is out we will get the thoughts of Minneapolis Fed President Neel Kashkari, Cleveland Fed President Loretta Mester, Boston Fed President Eric Rosengren and New York Fed President John Williams who speak at various events. Vaccine Big banks are keeping the pressure on their employees to get vaccinated, with JPMorgan Chase & Co. asking staff with client-facing roles in Hong Kong to have at least one shot by June 30. In Europe, the leaders of Germany and France expressed alarm that tourism-dependent countries like Greece are accepting visitors that have been vaccinated with non-EU approved doses such as the Sputnik shot. More than half a million Sydney residents are in lockdown for a week after an outbreak of the delta variant there. Biden warned of the risks that strain poses as he urged more Americans to get vaccinated. Markets riseGlobal equity markets are generally having a quiet end to the week, with Wall Street banks rising in pre-market trading as their passing of the Fed stress test paves the way for dividend payouts. Overnight the MSCI Asia Pacific Index rose 0.9% while Japan's Topix index closed 0.8% higher. In Europe the Stoxx 600 Index was broadly unchanged at 5:50 a.m. Eastern Time as travel stocks were hit by EU leaders' comments. S&P 500 futures pointed to a small move higher at the open, the 10-year Treasury yield was at 1.494%, oil held above $73 a barrel and gold gained. Coming up... U.S. personal income and spending data for May is at 8:30 a.m., with incomes expected to decline due to the end of stimulus payments. University of Michigan sentiment for June is at 10:00 a.m. The latest baker Hughes rig count is at 1:00 p.m. Paychex Inc. and CarMax Inc. are among the companies reporting results. What we've been readingHere's what caught our eye over the last 24 hours. And finally, here's what Katie's interested in this morningTraders are still grappling with existential questions about the Federal Reserve's path forward after last week's dot-plot bombshell—a task made no easier by an absolute parade of Fed speakers over the past few days. Case in point: New York Fed President John Williams told Bloomberg Television on Tuesday that liftoff is "still way off in the future" and the central bank isn't close to tapering bond buying. The following day, Atlanta Fed president Raphael Bostic said the taper decision may come in the next few months and he expects the Fed to first hike rates in late 2022. Chair Jerome Powell himself weighed in, telling Congress that the central bank will wait for "actual evidence of actual inflation" before lifting rates. The back-and-forth is hammer-locking both stocks and bonds. Benchmark 10-year Treasury yields are practically unchanged from pre-meeting levels around 1.49%, despite swinging in a 24-basis-point range. The S&P 500 has drifted about 0.5% higher, after sliding as much as 2%. Meanwhile, analysts are of two minds when it comes to navigating the Treasury market. Rates strategists from TD Securities and Bank of America both characterized last week's Fed meeting and updated dot plot projections as a "hawkish pivot" in research notes this week. However, the two banks took opposite ends of the trade.  TD's Priya Misra and Gennadiy Goldberg recommend wagering that the five- to 30-year yield curve will re-steepen from here, arguing that last week's dramatic flattening "looks extreme and was likely driven by a positioning washout." They initiated the paper trade at 121 basis points, with a target of 150. On the other side is Bank of America, where analysts led by Mark Cabana posit that the 5s30s curve will continue to compress from here, albeit at a "more gradual pace." Underpinning that view is the belief that improving economic data will hit the belly the hardest as traders price in a less-accommodative Fed. As they exit the five-year segment, that yield rises in a bear-flattening move. Judging by this week's trade, it's still a line-ball call. This stretch of the curve is sitting almost smack bang in the mid-point of this week's high and low, at 118 basis points—though it's well shy of its pre-Fed levels above 140. Follow Bloomberg's Katie Greifeld on Twitter at @kgreifeld

Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment