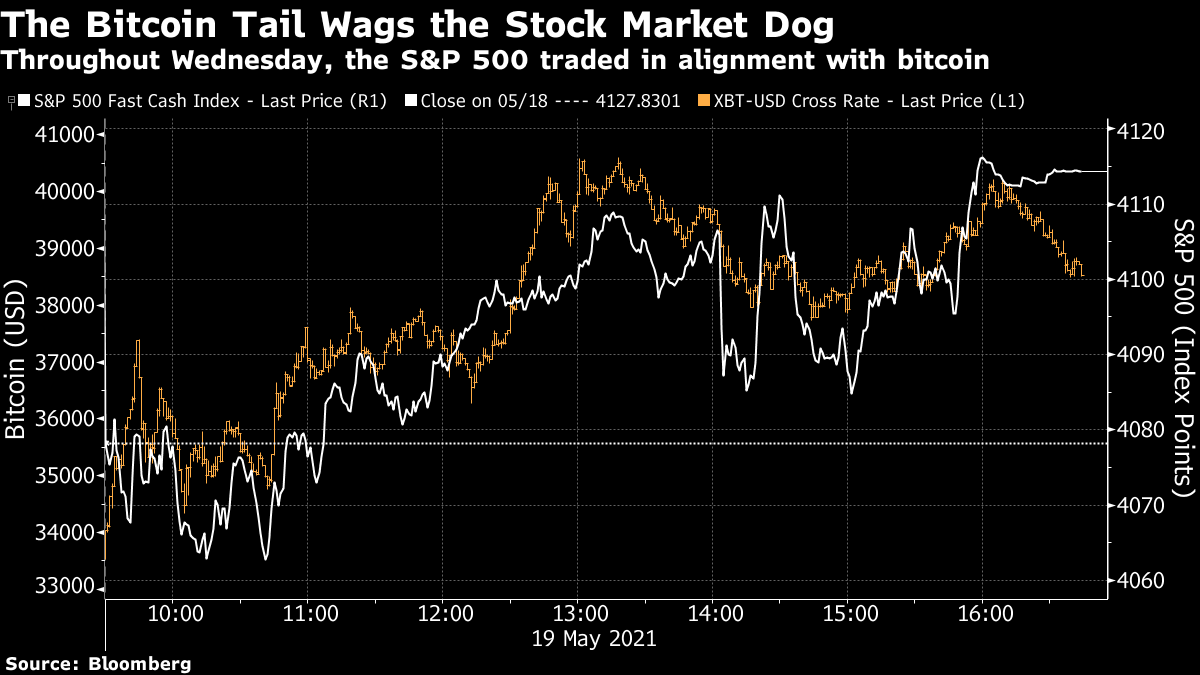

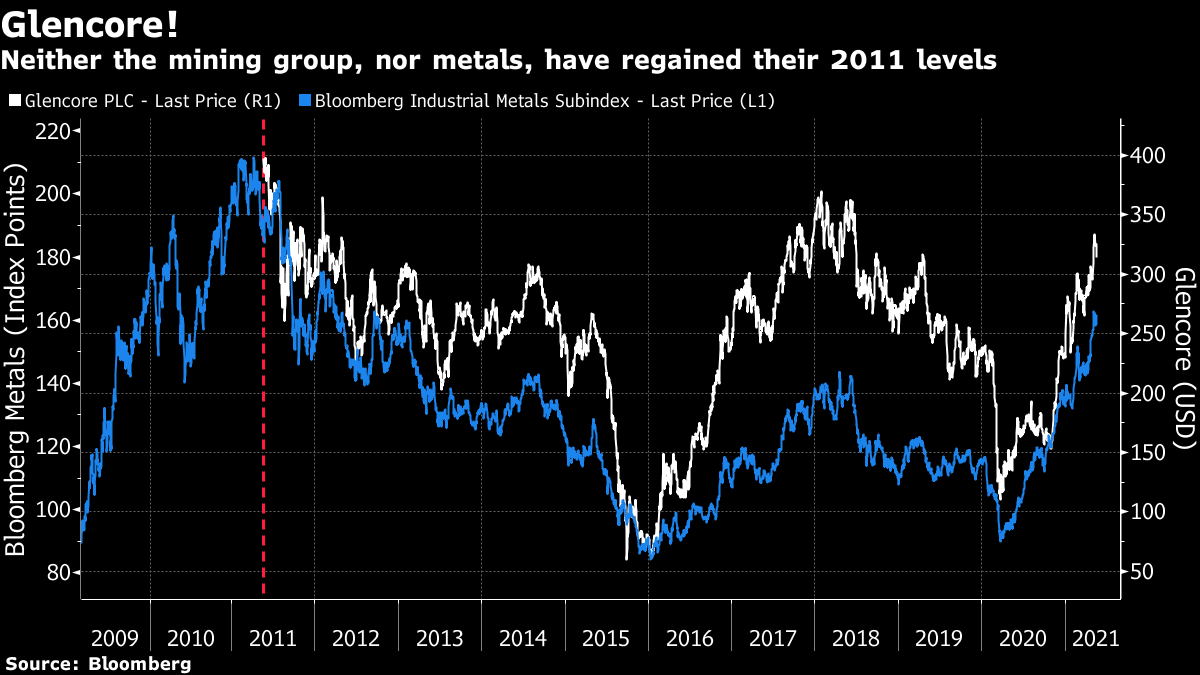

Bitcoin Goes a Bit CrazyFiat currencies are never this exciting. Bitcoin set its most recent high, of just under $65,000, on April 14. After that it had steadily given ground, and that became a headlong crash in the early hours of Wednesday morning. By 9 a.m. New York time, bitcoin hit $30,016 — a fall of almost 54% in five weeks. Over the next four hours, it rallied almost 36%. At the time of writing, the price is $39,000. It was quite a ride:  When I tweeted a version of this chart, with the accompanying comments that it was too soon to say that a bubble had burst, and that nobody in their right mind would denominate a transaction in bitcoin while it was this volatile (one of the less controversial things I've ever said), I attracted a fresh flood of righteous anger. You can see it all here. Bitcoin is still blessed, or plagued, with believers rather than investors. There are lots of great arguments for bitcoin, and even more for the blockchain technology on which it is based. While it inspires cultish devotion, however, it is difficult to analyze as an investable asset. That's a shame, because this was one day when the crypto world appeared to be the tail that wagged the stock market dog. The S&P 500 sold off sharply at the open, as traders looked at the bloodbath in cryptocurrencies overnight, and then spent most of the day regaining ground as bitcoin staged its own spectacular rebound. It did this even after the somewhat hawkish minutes from the last Federal Open Market Committee meeting, which I'll come to later, gave another reason to sell stocks:  Naturally, this has lots to do with emotion, and in particular with Elon Musk. But even if we take Musk's hype and the excitement he generated into account, nothing happened in the early hours of Wednesday to justify such a huge selloff and rally. And while waves of emotion happen in markets all the time, they are seldom this powerful or as swift. So, how to explain what has happened? Could it have been predicted? And can we predict anything for the future? Curse of the IPOThere was one surefire clue that something like this was going to happen. Throughout history, initial public offerings have taken place at peaks of confidence. When the owners of a big private company think market conditions are as good as they are going to get, they will go public. And as they know what they are doing, the rest of us should take the hint. Coinbase Global Inc., the biggest intermediary in the cryptocurrency space, listed last month at almost the exact top for bitcoin. This chart shows what has happened to the stock and the cryptocurrency since then:  I'm not saying that backers of Coinbase had any inside information, just that they understood conditions were as good as they were going to get. For previous examples of the Curse of the IPO, see what happened when giant mining group Glencore Plc decided to go public in the spring of 2011. The Bloomberg industrial metals index topped out a week before the offering. Remarkably, neither metals prices nor Glencore shares have returned to their levels on IPO day in the decade since:  For another example, try Blackstone Group, which arguably did more than anyone else to develop the concept of private equity. Such buyout firms are aided by lofty price-earnings multiples on stocks, and cheap debt. Somehow, Blackstone went public in the summer of 2007, right on the eve of the global financial crisis. Anyone who bought the stock at IPO, or the S&P 500 at the same time, would have had to wait until 2013 to show any significant capital gain:  The Elon Musk show was more entertaining, and his arguments against bitcoin on environmental grounds are valid — although he should have been perfectly aware of these problems before he started plugging cryptocurrencies. But we shouldn't have taken our eyes off the Coinbase show. The Curse of the IPO will not be denied. Bracing for RegulationIf the Coinbase IPO was a good "tell" that bitcoin was ready for one of its periodic steep falls, it didn't give a good cue for Wednesday's flash crash. Regulators did. Bitcoin generates much of its excitement precisely because it is an alternative to fiat currencies. Like gold, it might be able to hold its value, impervious to the actions of governments. The problem is that governmental fiat can destroy currencies as well as create them. Governments hold a monopoly on issuing currency, and would understandably be loath to lose it. This is one of the most serious "bear" points against bitcoin, and it got a lot of new support in the hours before the flash crash. From China came the news that payment and credit organizations were to be blocked from accepting bitcoin. In the U.S., the new comptroller of the currency at the Treasury Department — succeeding a man recruited by the Trump administration from Coinbase, of all places — announced a review of crypto regulation policy. Michael Hsu, the acting comptroller, said: "At the OCC, the focus has been on encouraging responsible innovation. For instance, we created an Office of Innovation, updated the framework for chartering national banks and trust companies, and interpreted crypto custody services as part of the business of banking. I have asked staff to review these actions."

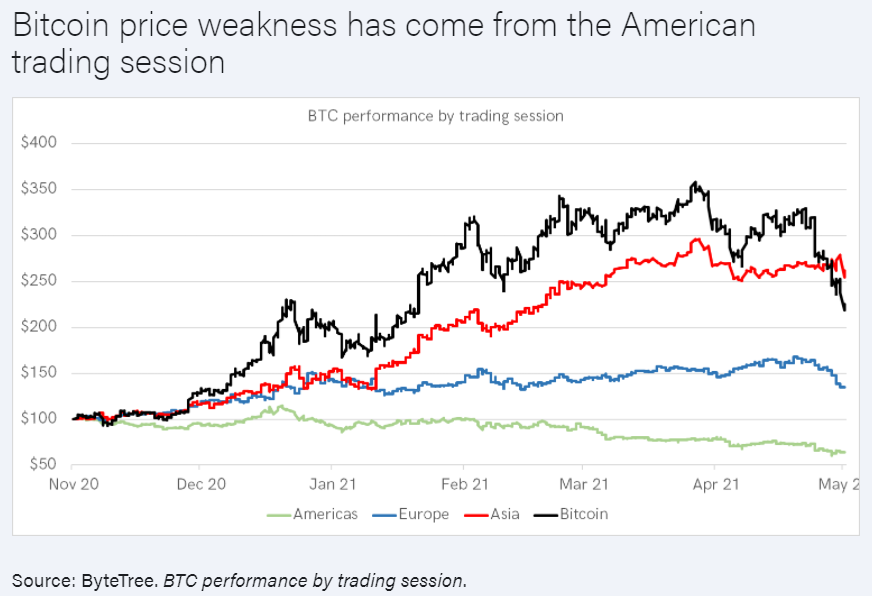

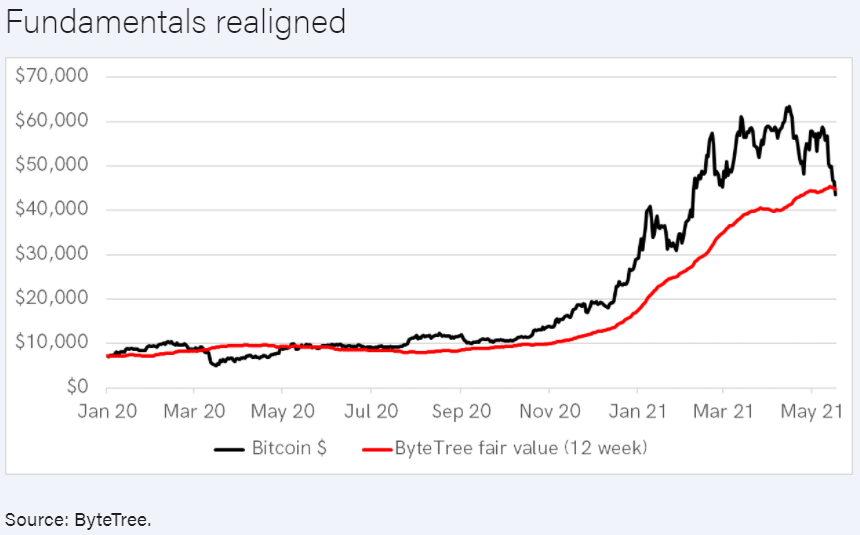

This is far from a declaration of war, and he made clear his belief that financial technology companies had a future. But any sign that the lenient regime currently in place might be changed was unwelcome for bitcoin investors. It isn't a coincidence that the extreme selling started after the Chinese news, however. The following chart, produced by Charlie Morris of ByteTree Asset Management Ltd. in London, breaks down bitcoin's trading patterns into the hours when activity is typically dominated by Asia, Europe, and North America. We don't know exactly who is selling when, but time zones give a good idea:  Asia, in red, appeared to have led buying of bitcoin in recent months, while American sessions saw net selling. It shouldn't be surprising that a bad news item in Asian hours prompted a flash crash. The Ghost in the MachineAre there any fundamentals we can use to work out a fair value for bitcoin? Morris has attempted this heroic task, and produced some interesting measures. Assuming its value is as a network and that more users make it more valuable, Morris produced a set of criteria for fair value in 2013, which he hasn't changed. Remarkably, that model gives a fair value at this moment of about $40,000. So it looks a little bit like a normal market in which an asset gets overhyped, falls and then overshoots, prompting buyers to come in. It is ridiculous to try to account for all of the sensational volatility around bitcoin in terms of a rational hunt for fair value, but there it is:  As an alternative, Morris looked at global transaction fees generated by bitcoin. In general, the system still has limits on capacity, and when more people are transacting, fees will go up to keep the volume manageable. (Another indication, incidentally, that while the mathematics and conception of bitcoin are extraordinary, there are plenty of technical kinks before this can be a mainstream currency.) Transaction fees saw a big spike as bitcoin was reaching its peak, and then tumbled. So maybe this is another measure that people can use to gauge the future progress of an asset that has no intrinsic value and produces no income yield:  If there are tentative ways to measure the technicals, there are also tentative ways to measure the emotion that undeniably drives much trading in bitcoin. Peter Atwater, who analyses social moods that influence investment patterns for Financial Insyghts, suggests that the falling out between Musk and Dave Portnoy of Barstool Sports Inc., another of the biggest bitcoin backers, was a tell that the top was near. "On the way up, there's enough money for everyone that the revolutionaries don't go after each other. To me, the Portnoy-Musk dispute introduced a sense of finiteness — now, in order for one to win, the other had to lose." Then, of course, there was Musk's appearance on Saturday Night Live; an event that gobbled publicity for weeks, and showed that the bitcoin phenomenon had passed beyond markets. If ever there was a moment to mark an emotional peak, this was it. That came with a proliferation of videos on YouTube telling people how to create their own crypto-coins. Whatever the merits of bitcoin itself, the signs that it had taken on some disreputable hangers-on were clear. When money is seen as that easy to make, it is never a good sign. But was this the top of the bubble? It might be, but it probably isn't. Bitcoin has formed at least three classic bubbles already in its brief history. Each time it has crashed by 80% or more, and then revived after a few years. If we compare bitcoin starting a year before its recent peak to the 12 months before its last high in December 2017, we see that this dose of mania seems to have calmed down much earlier — and after the last apparent burst bubble it was still able to regroup and set a new high:  Where does this leave us? My best guess, looking at what metrics are available, is that another surge in cryptocurrency assets has peaked and that it will probably be a while before the high from last month is revisited. Given bitcoin's ability to pick itself up and start again, demonstrated several times now, it is way too soon to say that this is a burst bubble. Whether it really establishes itself as a part, or even an essential part, of the global financial system will depend on how many people use it, and how tolerant central bankers are of that. While bitcoin continues to develop, it will be worth as much as someone is prepared to pay for it. The digital currency's fortunes are likely to remain tied to risk appetite in society at large; whatever direction bitcoin goes in, we can expect other risk assets to go the same way. A Case of MentionitisIn the beginning stages of a relationship, or any stages of an illicit relationship, it's hard to avoid "mentionitis," which the Lexico online dictionary defines as "a tendency towards repeatedly or habitually mentioning something, especially the name of a person one is attracted to or infatuated with, regardless of its relevance to the topic of conversation." Bridget Jones once noticed that her boyfriend suffered from it. Now, it appears that members of the Federal Open Markets Committee have come down with their own case. They are supposed not even to be thinking about thinking about tapering asset purchases, and to be secure in their confidence that the current bout of inflation is only transitory. But the minutes of their latest meeting, released Wednesday, suggest they are already seriously afflicted by mentionitis. This new sentence appeared: "A number of participants suggested that if the economy continued to make rapid progress toward the Committee's goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases."

That counts as thinking about thinking about tapering asset purchases. Then Steve Blitz, chief U.S. economist of TS Lombard, pointed out that this sentence in the previous minutes had mysteriously disappeared: "Most participants noted that they viewed the risks to the outlook for inflation as broadly balanced . . . Several participants commented that the factors that had contributed to low inflation during the previous expansion could again exert more downward pressure on inflation than expected."

Blitz noted that the following sentences had been inserted: "A number of participants remarked that supply chain bottle-necks and input shortages may not be resolved quickly and, if so, these factors could put upward pressure on prices beyond this year."". . . a couple of participants commented on the risks of inflation pressures building up to unwelcome levels before they become sufficiently evident to induce a policy reaction."

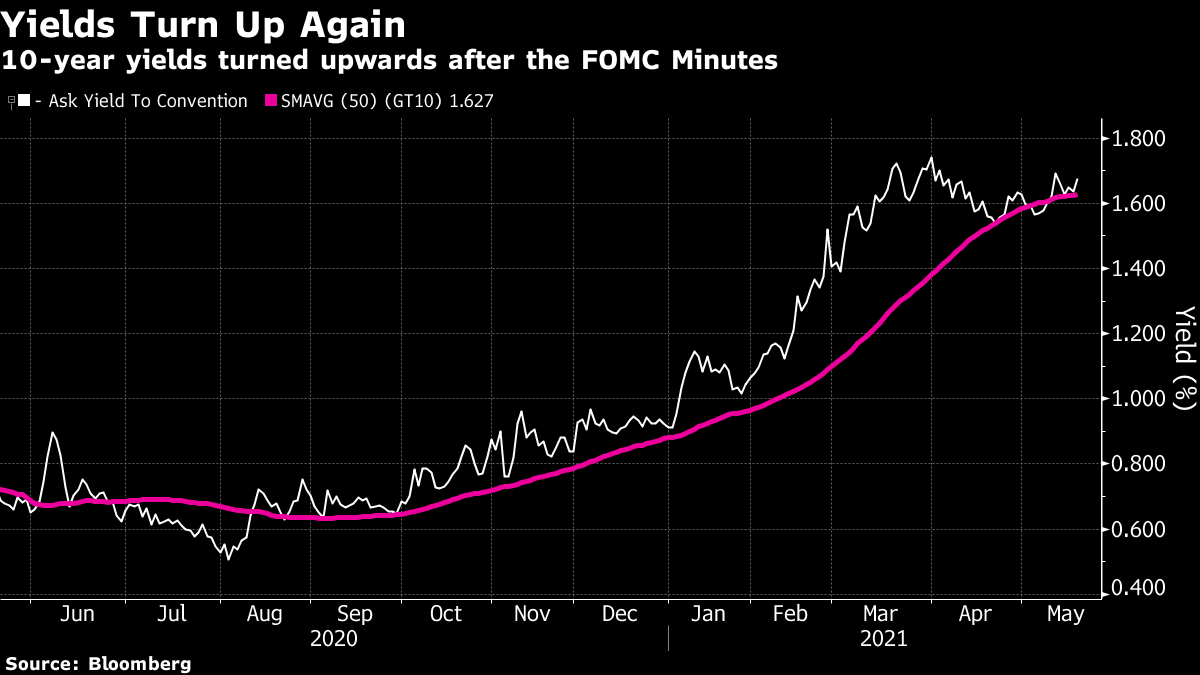

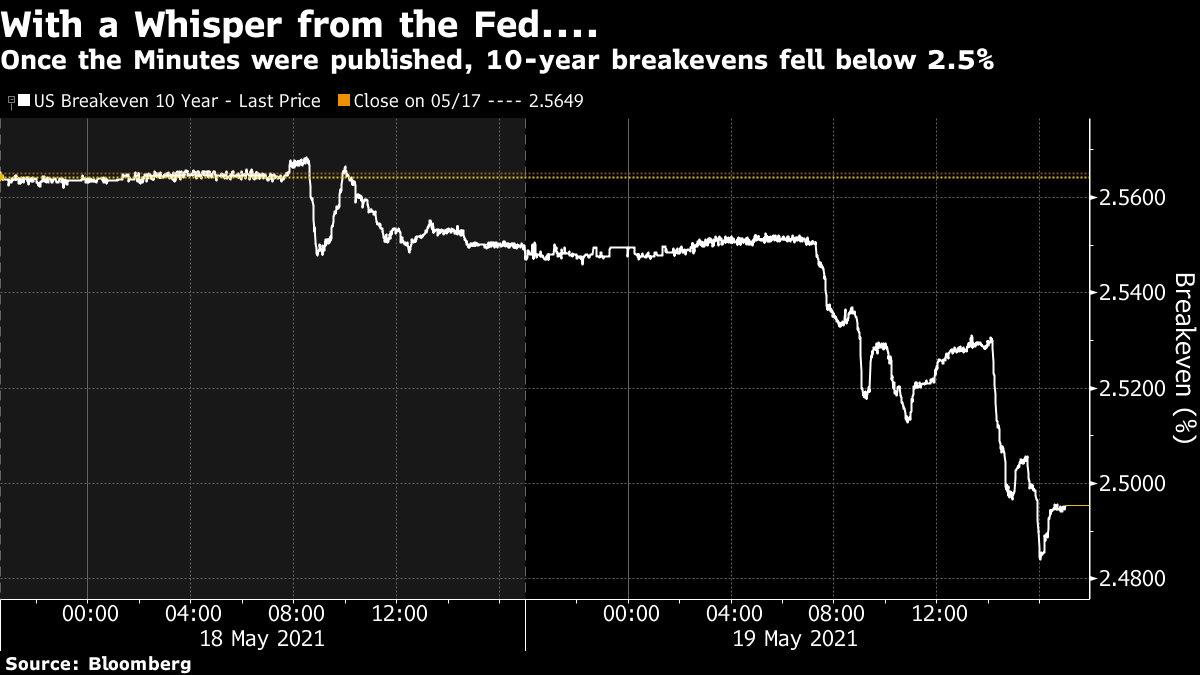

In Bridget Jones terms, if Fed governors were to be asked directly if they were flirting with a taper, they would blush, look downwards, and deny all interest. But it's obvious how they feel. The ever-so-gentle move to prepare financial markets for conditions that are ever-so-slightly less friendly has at last begun. Stock markets, like a distracted boyfriend, were enthralled by the crypto-drama. But the bond market plainly got the message. Yields had gently started to descend in the last few weeks, with the 10-year yield briefly dropping below its 50-day moving average. It's not back to its high, but the Fed said enough to nudge it up, and keep the prevailing trend upward:  If the Fed is at least thinking about thinking about tapering, that reduces the risk that inflation is allowed to get out of control, which of late has begun to loom as the biggest tail risk. As this two-day chart of the 10-year bond market inflation breakeven shows, publication of the minutes at 2 p.m. was enough to bring inflation forecasts below the disquieting (for the Fed) level of 2.5%:  All it needed was a not so careless whisper from the Fed, and the markets got the message. Whenever you thought tapering would start before, it's best to bring that date forward by one FOMC meeting. Survival TipsAfter recommending caffeine yesterday, which wasn't very socially responsible of me, I can now offer a new healthy option. Yesterday, Bloomberg employees were told they could walk the office unmasked (if we were fully vaccinated). Today, came the ultimate boost to morale — the reappearance of fancy vats of iced water, infused with pineapple, lemon, or lime. I have to thank my colleague Sonali Basak for this photo:  Boy, does this make a difference to morale! It also provides yet another reason to come into the office. There is of course no reason why you can't infuse some iced water with some fruit at home and drink it. But having it there, all ready for you, feels like a treat and a privilege, particularly after the aridity of the last year. Small gestures of return to normality can make a big difference. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment