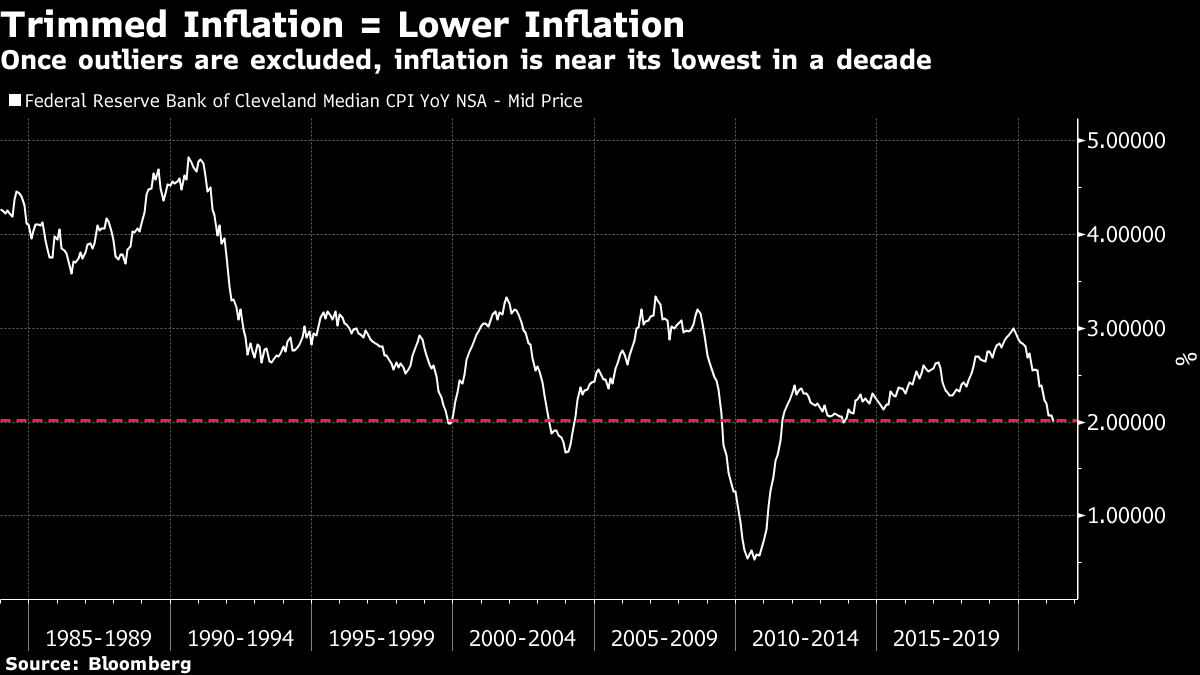

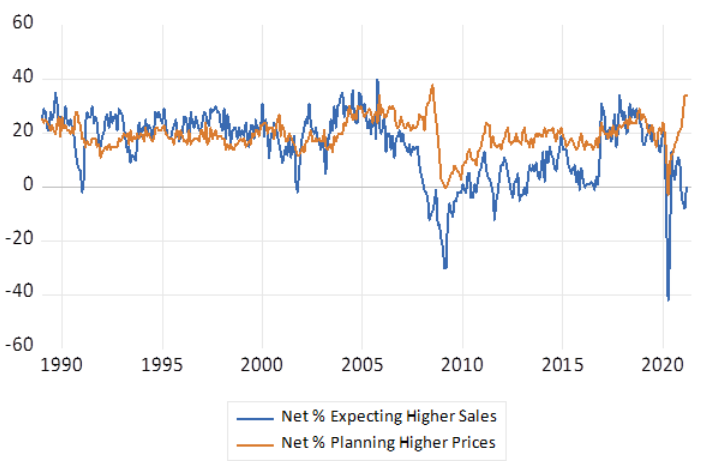

Inflation SightingsThe Reflation Trade enjoyed an exciting rendezvous with the facts on Tuesday. For months, the bond market has shifted to signal coming reflation. Everyone knows that the headline number will look bad for the next few months, because oil prices dropped precipitately a year ago; the question is whether a rare combination of massive fiscal stimulus and a strenuously easy monetary policy can at last jolt the U.S. and the rest of the world into an inflationary psychology. Of its nature, an inflation spiral takes a while to take hold. No data published Tuesday could possibly prove one way or another whether we will have inflation well above the Federal Reserve's upper limit of 3% in a few years' time. But all new data provide more evidence on the direction in which we are heading. And the release of the U.S. consumer price inflation data was all lined up to be a big moment. In the event, the headline rate came in "hot" at 2.6%, above expectation. That would naturally mean higher bond yields, as investors acted to protect themselves against higher inflation and interest rates ahead. Early in the European session, the benchmark 10-year Treasury yield briefly brushed the landmark of 1.7%, as traders braced for a spike higher. So, of course, exactly the opposite occurred. The following screen grab from the Bloomberg terminal shows what happened during the day. I've ringed the key events:  After hitting 1.7%, the next key event came at 7 a.m., when news that the Johnson & Johnson vaccine rollout had been paused by the Food & Drug Administration, following evidence that it might cause the same rare blood clot condition that interrupted delivery of the AstraZeneca Plc vaccine in Europe. Obviously a big deal, as it raises the risk that the pandemic could drag on longer than expected, the news prompted people to buy bonds and push down their yield. That move was swiftly reversed as traders positioned themselves for the possibility of a big upside surprise in the inflation number. The data when they arrived weren't enough to counteract the vaccine news, so the 10-year yield dropped steadily further. Not even a steady drip of reassurances from officials that the Johnson & Johnson delay would last days rather than weeks altered the direction of travel. Then at 1 p.m. came the day's key development as far as the bond market was concerned; news that the latest auction of long-dated Treasury bonds had been a success, revealing robust demand even with yields still very low. By the end of the New York day, the 10-year yield was threatening to drop through 1.6%, barely 12 hours after it had touched 1.7%. At its core, this tells us that the market now works on the assumption that the reflation trade has come as far as it needs to for now, if not a little too far. A high inflation number had already been priced in. By many sensible measures, the reflation trade has been on pause in the bond market for the best part of a month. To cite the most relevant measure, expectations for inflation for the next five years, and for the five years after that, have settled down. This market critically sees inflation as averaging only a little over 2.5% over the next five years, and then falling back over the following five. In other words, it is positioned for reasonably healthy reflation, but not for a major regime shift toward inflation:  Now, for a tour of the day's inflation sightings. There's plenty of new evidence. CPI The headline rate can be largely disregarded, as it is predictably high due to moves in the oil price. The core rate, excluding oil and food, is the one that matters most to the Fed, and where a true return to inflation psychology should show up. And core inflation is barely back into its standard range since the deflationary shock of the financial crisis a decade ago. It remains safely below the Fed's 2% target:  uq Another form of core inflation, increasingly closely watched, is the "trimmed median," in which the outlying highest rising and falling prices that go into the index are excluded. This index, compiled by the Cleveland Fed, actually suggests that core inflation is actively decreasing, and bang in line with the target of 2%:  There is nothing untoward here. The View From Small Business Tuesday morning also saw publication of the monthly survey of small business owners by the National Federation of Independent Business. This is a long-lasting survey that has been a good economic leading indicator over the years, although polarized politics may have begun to affect it, with a big jump in optimism following the election of Donald Trump, and a fall in optimism after Joe Biden's victory, which did not show up in other surveys. But on the face of it, the proportion saying that they were planning higher prices, the highest since immediately before the financial crisis, suggests significant inflationary pressure:  There are arguments against worrying about this, however, from TS Lombard's U.S. economist Steve Blitz. He points out that the survey's prediction of higher prices should be set against a distinctly bearish prediction on future sales:

He suggests that the survey as a whole should even be taken as evidence of the lack of "cost-push" inflation, because small business executives are effectively predicting that they won't be able to pass on prices to their customers. They aren't expecting great profits, and say they are having a hard time finding people to hire. Blitz suggests they are finding hiring difficult because they are also finding it difficult to afford the wages needed to attract people: So, where are small businesses? They say that want to hire even though sales and earnings expectations are muted at best. Taking them at their word on hiring, they are having a hard time at finding people and we suspect it is the wages being offered given their business outlook. If anything, this tells me that margin pressures remain, are anticipated to remain, and this also means inflation is not in the offing. Nor is there an expectation for the kind of growth the equity market implies and the Fed and most forecasters are expecting. This does not mean small business will be right, it does mean that people need to relax about taking price hikes due to shortages, etc, and translating this into an inflation story – this would be news to Main St.

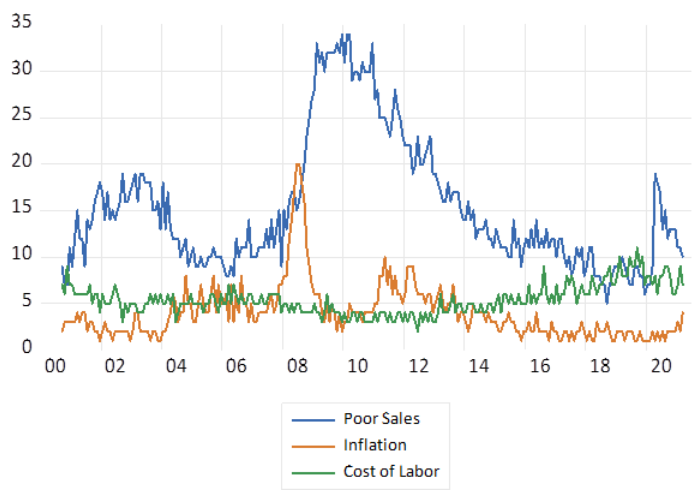

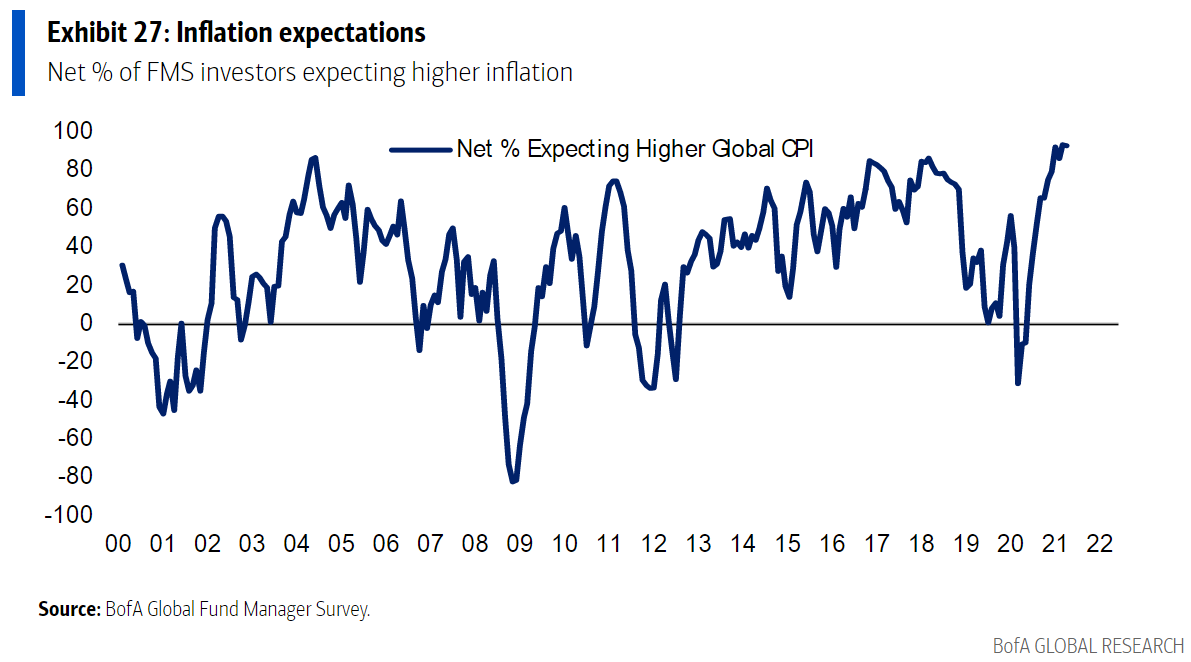

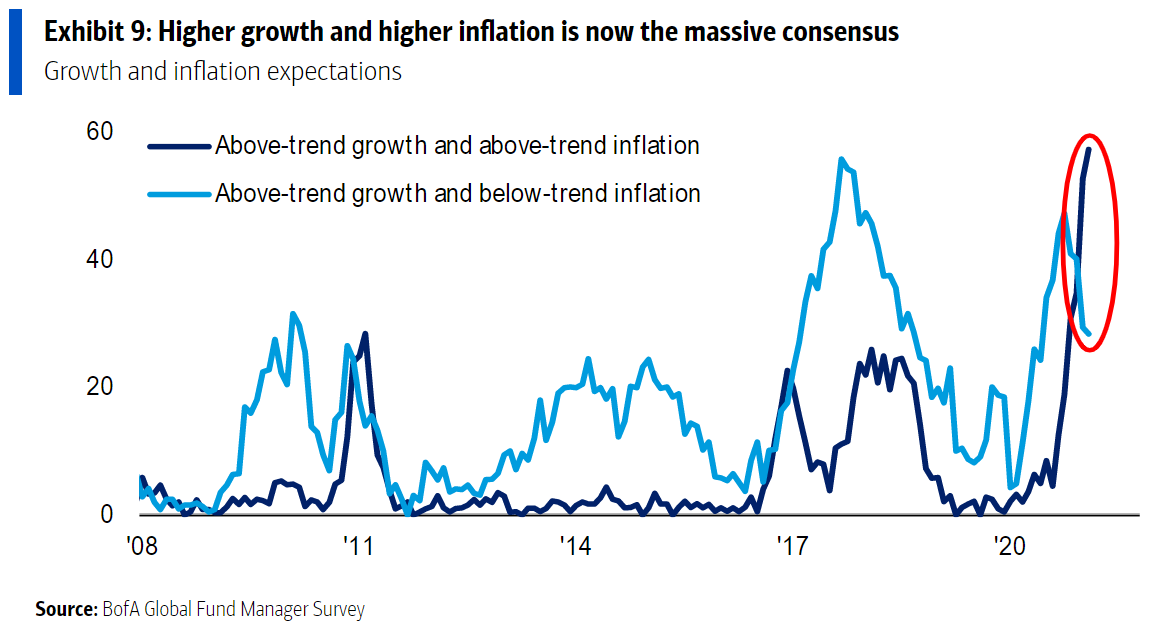

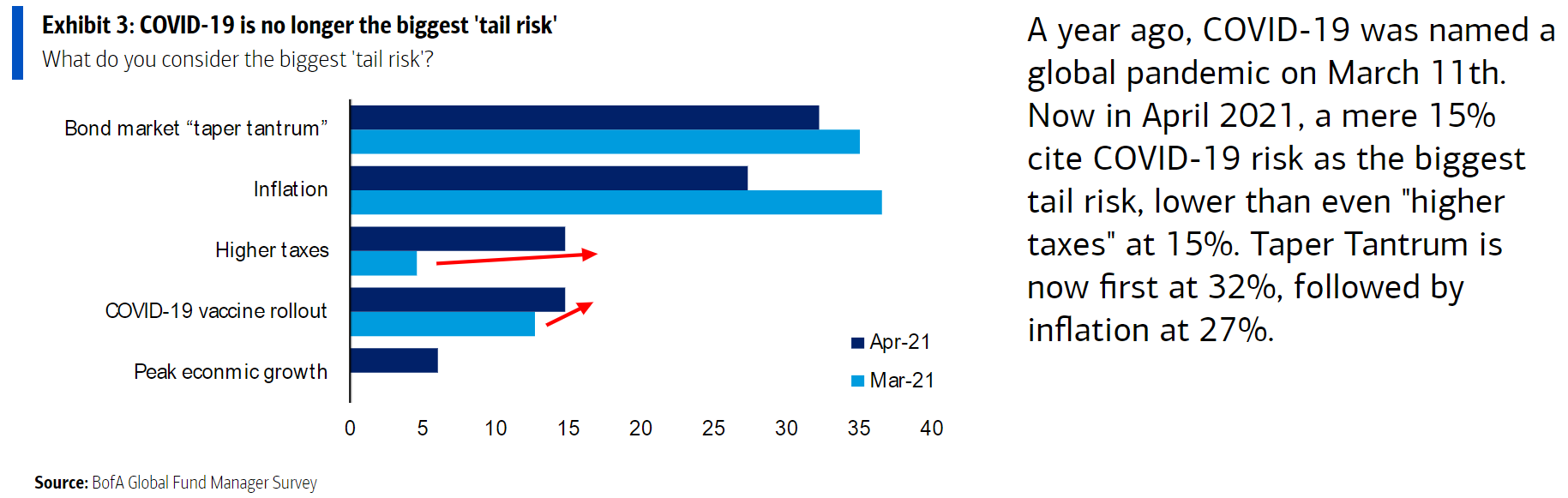

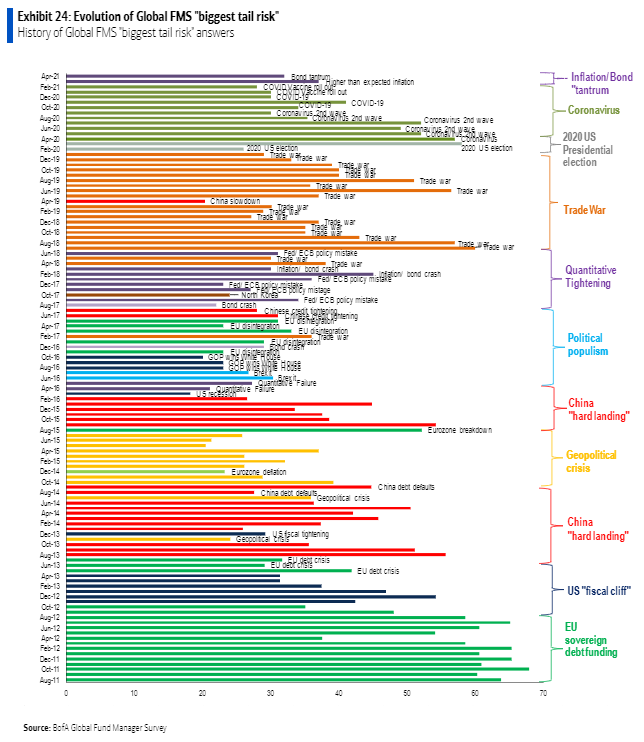

As a clinching argument, he draws attention to the NFIB's survey of executives' single greatest concerns. Inflation still lags poor sales and the cost of labor. Inflation is rising as a concern, yes, but from a very low level:  To emphasize that small businesses, despite their politics, aren't as worried by a return to 1980s inflation psychology as traders in financial markets are, look at the numbers going back to 1985:  Despite initial appearances, there is no inflation scare among small businesses. The View From Investors Tuesday also saw publication of the monthly BofA Securities Fund Manager Survey, a closely watched and detailed report on what "real money" regulated investors are thinking. Unlike small businesses, pension and mutual fund managers seem convinced: The proportion expecting higher global inflation is at a record for this century:  Not only this but the proportion expecting above-average growth combined with above-average inflation (the classic "reflation trade") is the highest since a question about it was first included in the survey in 2008:  Only very briefly had such a forecast previously exceeded a belief in below-trend inflation. Whether or not we have a clear shift toward an inflationary psychology in the population at large, we plainly have just such a shift in the investment world. Those convinced that this will be another inflationary false alarm should have the opportunity to make some money. The BofA survey also helps to explain how the successful bond auction seemed to blot out the news on inflation and on vaccines. Asked what they considered the greatest "tail risk" facing them, a majority named a bond market "taper tantrum" — a sharp rise in yields once the Fed moves to tighten policy — with inflation itself coming in second. The successful auction confirmed that a tantrum isn't in the offing, at least for now, and so it shouldn't be a surprise that it prompted plenty of people to buy bonds. Meanwhile, it is remarkable how many investors have moved on to worry about the risks of overheating after the pandemic, rather than about the pandemic itself:  To understand just how new and different the investor psychology is, look at the evolution of the "greatest tail risk" over the decade that the question has been included in the survey. Until now, all the most scary tail risks have involved something bad. For the first time since the global financial crisis, investors are now primarily worried about what happens if they get too much of something good:  This is all good evidence that the reflation trade has been taken too far too fast, so it's no surprise that the market took a step back from that trade after the inflation numbers.

None of this means that we shouldn't prepare for a new inflationary paradigm. There is still good reason to expect such a thing. Fiscal and monetary policy are directly aimed at making this happen. But they can't make it happen immediately, and plenty of deflationary pressures remain. Until we get more evidence, the reflation trade has come far enough.

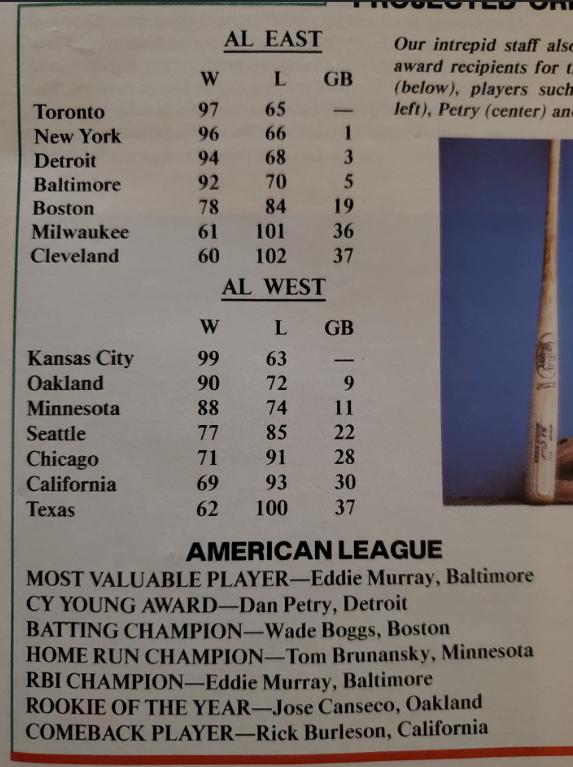

Survival TipsHere's one: Check your work to make sure you haven't made any absent-minded mistakes before putting it in an email and sending it to thousands of people. Yesterday's survival tip was about an actor and beatboxer called Mike Warburton. Make that Mike Winslow. Mike Warburton was the name of the gentleman whose tweet about Mike Winslow went viral, and brought a remarkable performance to my attention. My apology to both Mike Ws. One other survival tip is to take refuge in sport. Time and perspective can heal any number of wounds. Baseball season is back. Despite bad weather and tiny pandemic-riven crowds, and some rule changes that seem utterly crass, it continues to cast a spell. It's the continuity of the sport, and the slowness of its rhythm over an individual game or a whole 162-game season that makes it so seductive. A week can change everything. My Red Sox started off the season by losing three straight at home. They've won seven in a row since, and hope reigns. The passage of decades can also change things. Last week, one of my neighbors had a clear-out, and jettisoned a copy of the Sports Illustrated magazine preview of the 1986 baseball season, with the great Wade Boggs on the cover:  I was lucky enough to notice it in the recycling pile. The year 1986 was my first full season of baseball fandom when I was a student working a summer job in Boston, and an exciting one for the Red Sox. Those of you who follow baseball will know how it ended. Those who don't can Google it; it's just too painful to recount the way the Red Sox lost at the last gasp in one of history's greatest ever sporting collapses. However, they did win their own league comfortably, for the first time in more than a decade, and produced both the batting champion (Boggs) and also the Cy Young Award-winner for best pitcher, which went to a youngster named Roger Clemens. As history focuses on how the Red Sox failed at the last, it was a delight to be reminded that absolutely nobody had seen them coming. Here are the Sports Illustrated predictions:  Despite low expectations, the Red Sox won the American League. They shocked the world and made fools of the pundits. What a great season 1986 was. That is the way I will look at it from now on. Believe that and you'll believe anything. But if you still have piles of ancient magazines, you might want to have a quick read through before taking them to recycling. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment