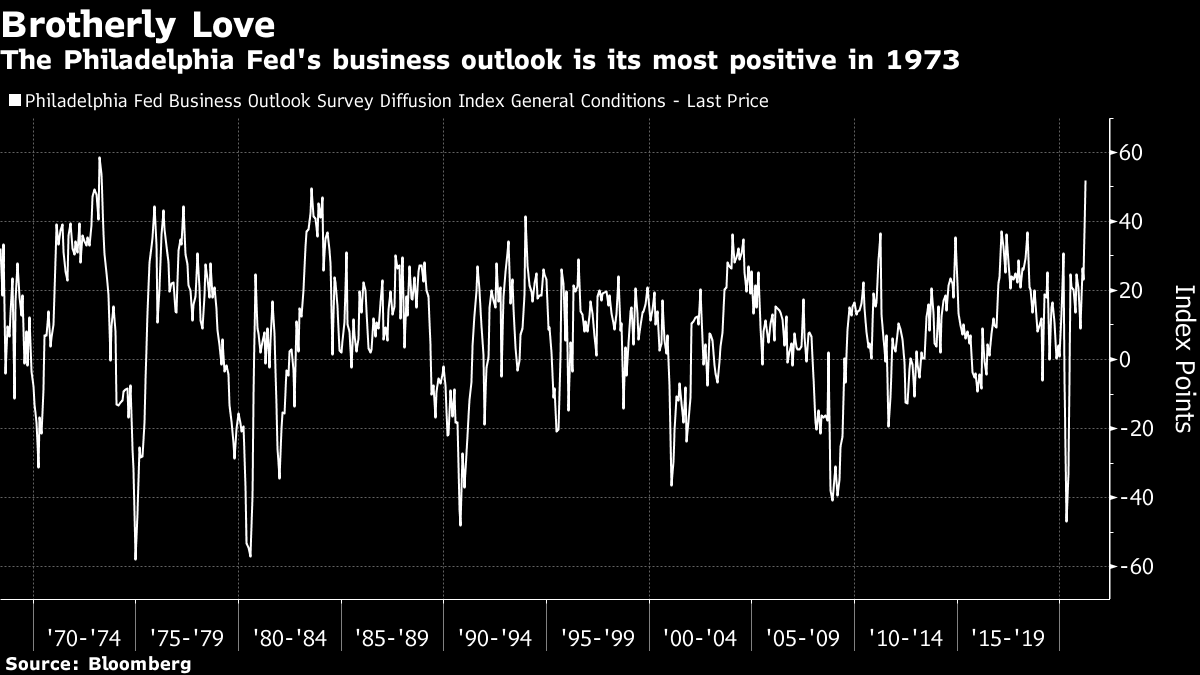

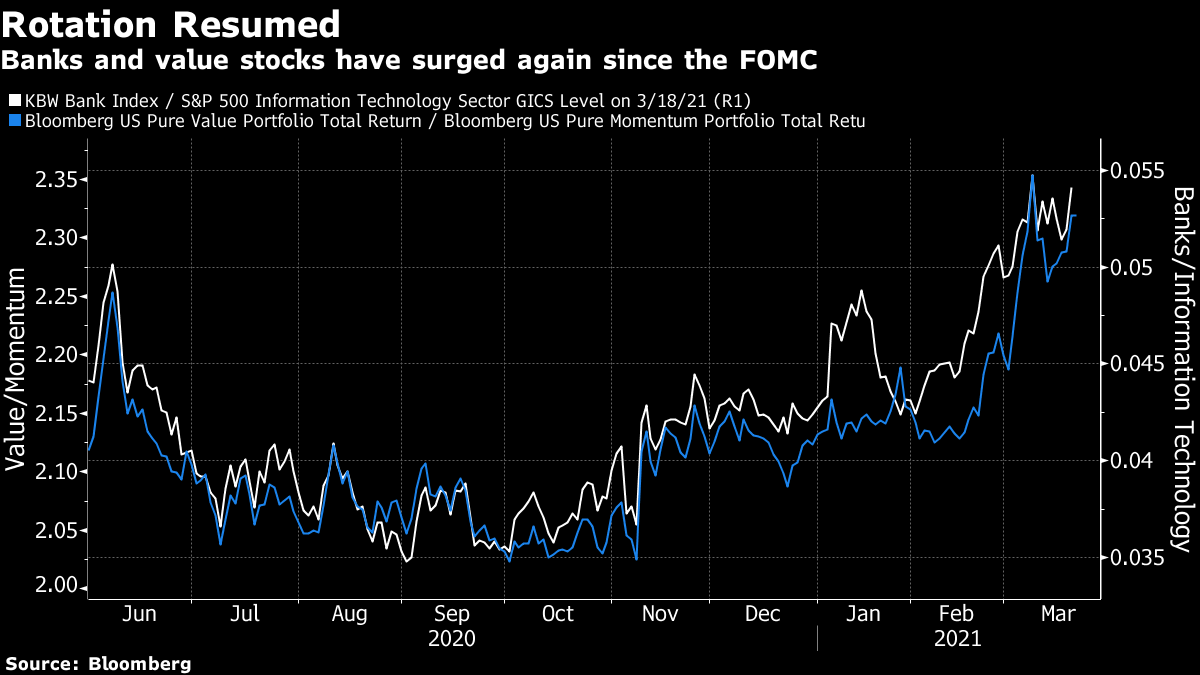

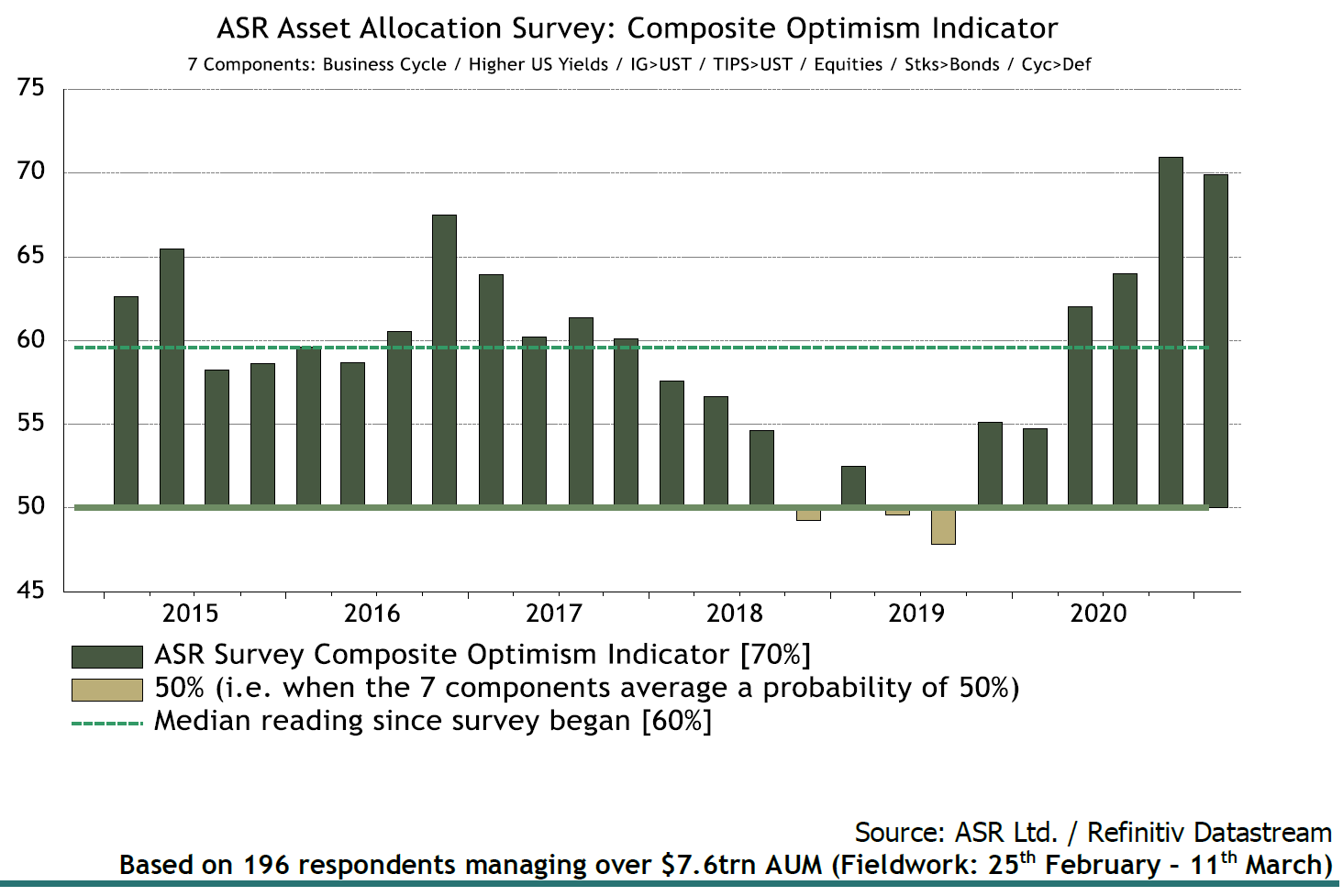

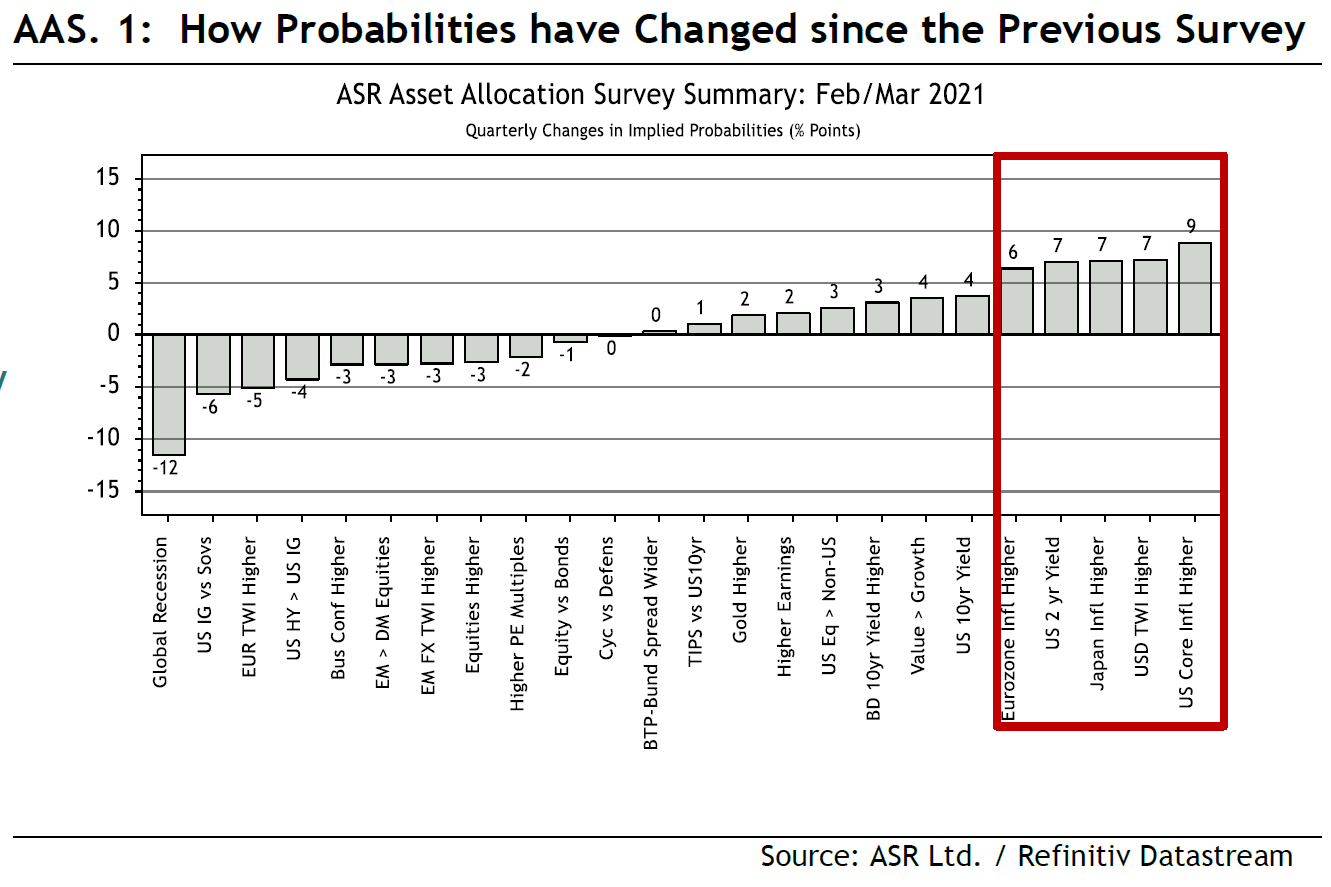

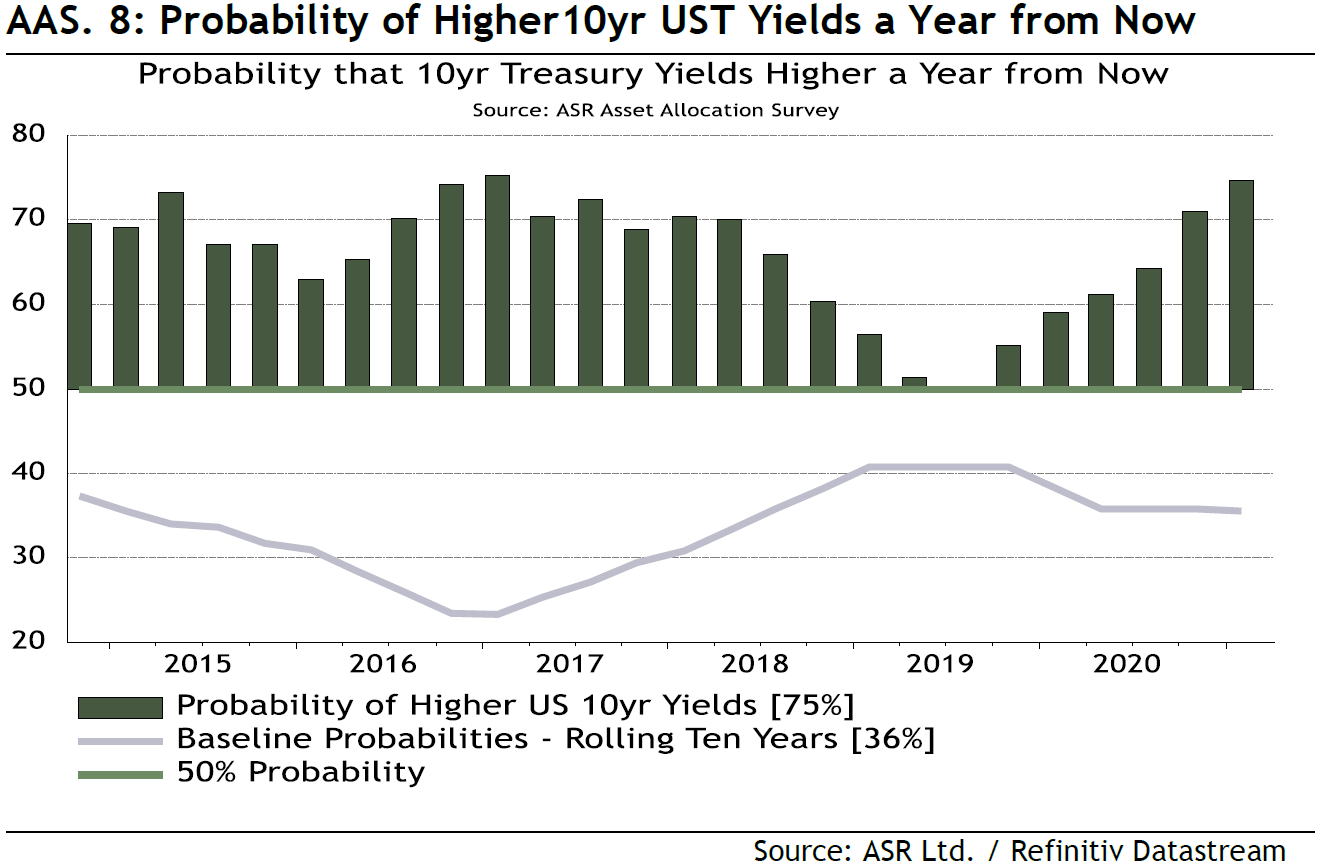

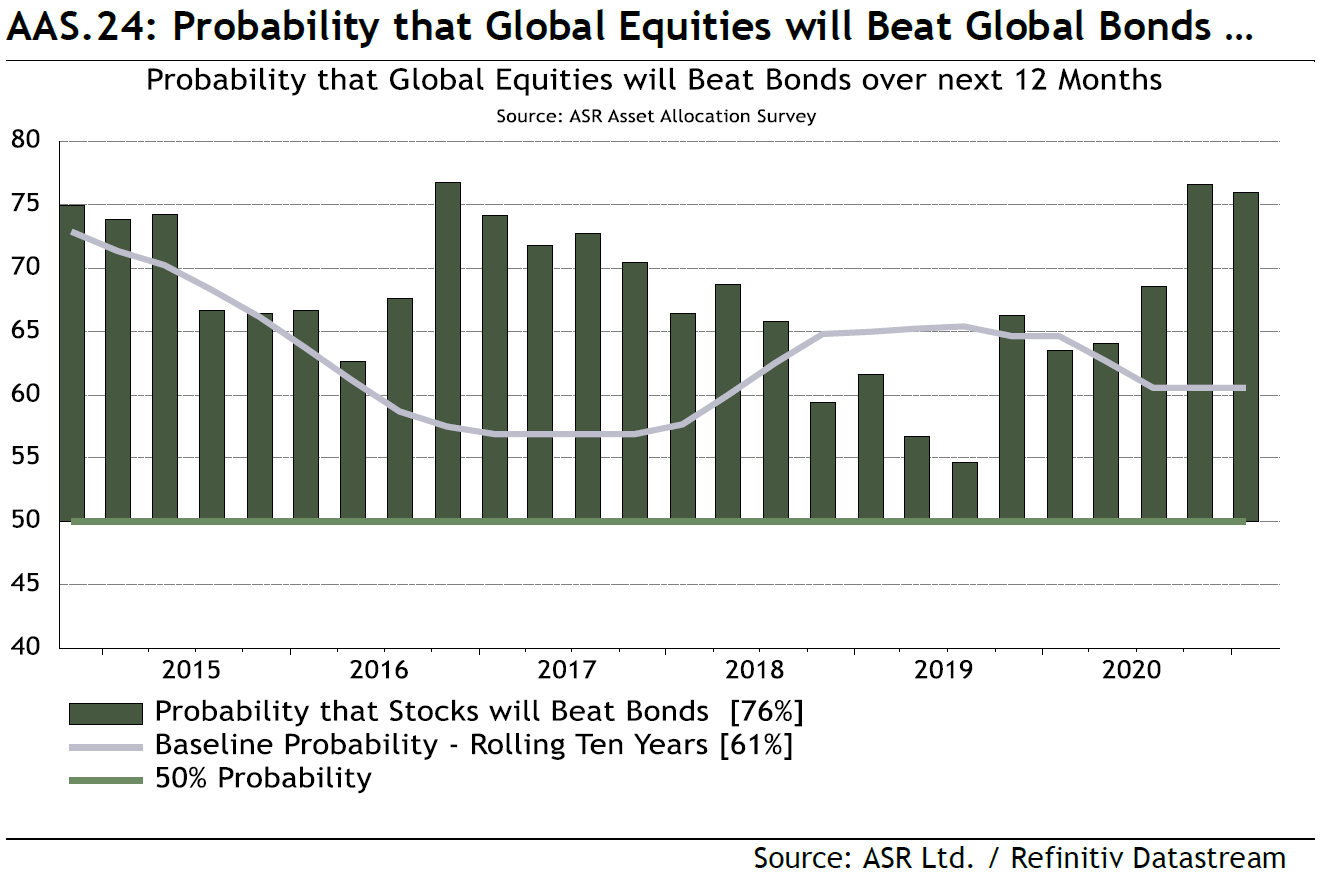

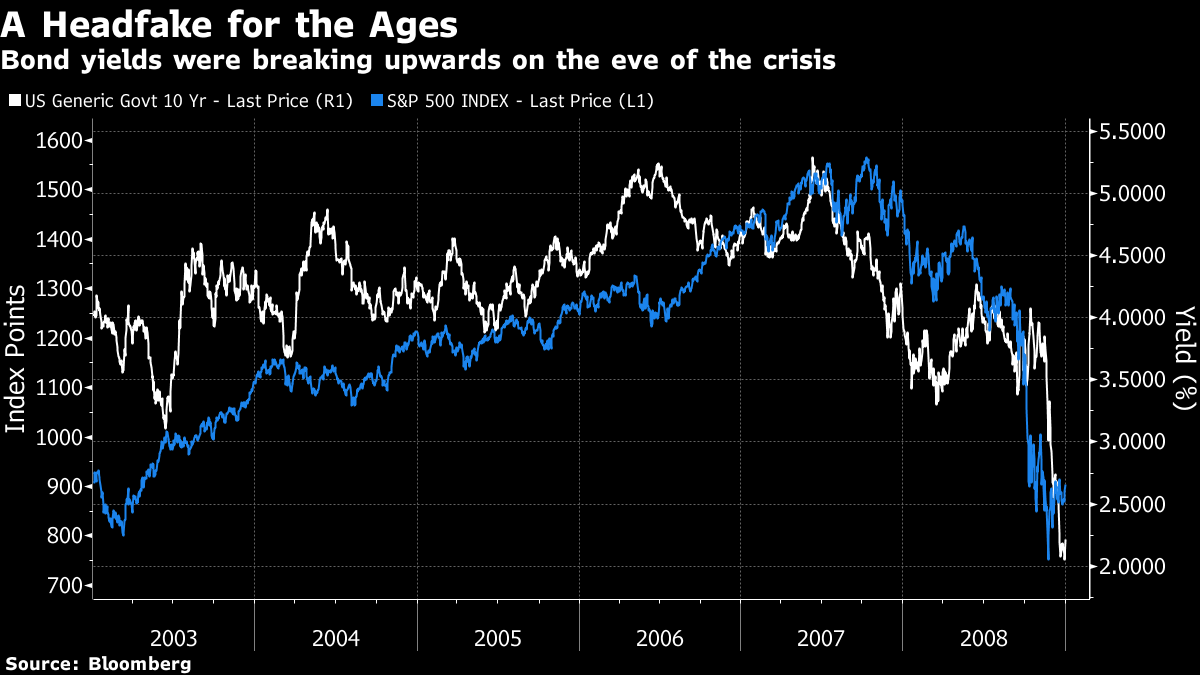

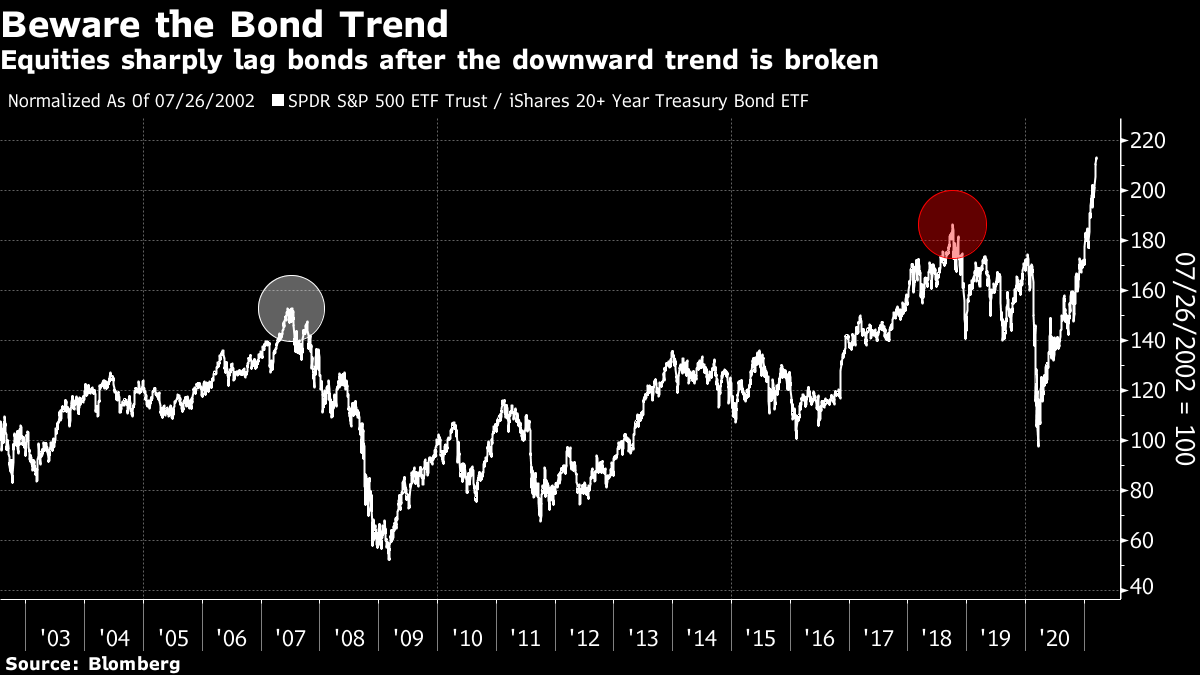

Animal MagicIt is time to take refuge once more in the animal kingdom. To try to explain what is happening in bonds, and the effect it could have on other markets, I will summon two characters from the summer of 2007. That was the period when the coming financial crisis became evident, and when equities were the last to grasp it. First, there is Wile E. Coyote, the character from the old Road Runner cartoons. He is capable of running off a cliff and continuing to run on thin air. It is only when he stops and looks down that he falls. Second, there is Jeremy Grantham's brontosaurus, the dinosaur invoked by the founder of GMO in the summer of 2007 to explain why equities were still at all-time highs as all hell broke out in the mortgage market. Stock markets were like a brontosaurus, he said; when they were bitten on the tail, it took ages for this information to make its way to the brain. These are the kinds of narratives that can help us to understand why markets behave the way they do. The story from Thursday, after a startlingly dovish statement from the Federal Reserve, was clear enough. The spread of 10-year over two-year Treasury bond yields passed another landmark, briefly topping 160 basis points. Meanwhile, the 10-year yield itself topped 1.7% for the first time since last year's Covid shutdown. Investors are evidently prepared to believe the Fed when it says that it will leave interest rates low come what may, and let the economy run "hot." This buoyant narrative was strengthened by another helping of strikingly hot data. The Philadelphia Fed's survey of the business outlook rendered its most positive result since 1973:  Within the stock market, the implications of further reflation were clear, and the rotation away from the safe stocks that did well last year, and toward value stocks and banks, resumed after a few days of consolidation. Banks sharply outperformed tech companies, while value beat momentum, as measured by Bloomberg:  Investors are almost frighteningly unified in their conviction that reflation is coming. This was the outcome of the latest asset allocation survey carried out by Absolute Strategy Research Ltd. of London, based on regular interviews with a panel of money managers responsible for more than $7.5 trillion in assets between them:  Their optimism is based on unshakeable confidence that inflation is at last going to stage a return, while a recession is avoided. Views of the probabilities in the three months since the last survey have moved almost uniformly to support a reflationary narrative:  This means that bond yields will be higher in a year's time. Certainty on this has never been higher:  But higher rates won't get in the way of a continuing rebound in global corporate earnings, which will buoy stock markets. Again, confidence is strong, and growing:  Put these together, and you have great conviction that stocks will beat bonds for the next year. Worries that higher bond yields could derail the rally in equities haven't, for the most part, shaken the confidence of asset allocators:  So the narrative on which the markets are running is clear and to an extent self-reinforcing. Market perceptions of reality have the power to change reality — a concept that George Soros labels reflexivity. Could this all add up to an epic "head fake," to borrow the phrase of one of my Twitter interlocutors? After darting in one direction, will we end up heading in the other? It's certainly possible, but even if this happens it would be inaccurate, I think, to call this a head fake. Rather, a shift back would mark the moment when investors acted like Wile E. Coyote or the brontosaurus, and finally grasped that the data didn't support the narrative, and that the rise in bond yields was going to bring down the stock market. We are going through a process where a narrative is tested against the market. If we reverse, it will come at the moment when that narrative can no longer create its own reality, and instead has to succumb to it. For an example, let me point to a little remembered scare in the bond market, when the 10-year Treasury yield briefly shocked traders by exceeding 5%, back in the summer of 2007. That prompted much analysis about the possibility of a new world where steadily falling yields were replaced with a rising trend. What instead happened was that investors looked at what yields so high would mean for the increasingly over-extended financial architecture, and took fright. Money exited risky credit and flowed into government bonds, whose yields shot downward. With the problems in credit now impossible for anyone to ignore, stocks wobbled after reaching a high and then made their epic descent of 2008:  Why was that particular rise in bond yields so scary? As the chart above shows, they had been almost as elevated at one point about a year earlier, in 2006. The main answer is that bond traders had come to rely on the downward trend in the 10-year Treasury yield, which had persisted ever since Paul Volcker crushed inflationary psychology in the early 1980s. A trend line joining the 10-year yield's high points in the years following formed an almost perfect straight line. The summer of 2007 saw that trend line broken for the first time (it's just visible on the chart below), and many financial engineers suddenly had to confront the possibility of a world in which long-term rates didn't float downward forever. The idea was appalling, and bond yields swiftly resumed their downward progress:  The eagle-eyed will see that that trend line was broken a second time, in the first week of October 2018, coincidentally on my first day at work at Bloomberg. On that occasion, yields were rising as the Fed tried to normalize rates, and to convince the markets that it would continue doing so. The effect on the relationship between stocks and bonds was instant. The chart below shows their relative performance, as proxied by the SPY and TLT ETFs, which respectively track the S&P 500 and Treasury bonds of more than 20 years. The points at which the long-term downward trend in bond yields was breached are both circled. In both cases, the point when investors finally confronted the notion that yields would move much higher overlapped exactly with the point when stocks started to underperform. This was true even though bond prices started to fall:  On both those occasions, the rise in yields tested investors' confidence that stocks could withstand a more normal world with higher rates, and found that no such confidence existed. Now, higher yields and the steepening in the yield curve suggests that another such test is under way. Going by past experience, the 10-year yield can rise to about 2.8% (where the long-term trend line is at present) before this moment of truth. So investors eat, drink, buy into the reflation trade and make merry, on the assumption that the bond market is still lenient enough that there is a way to go before it will bring equities down. Put differently, there is plenty of evidence of bubble-like enthusiasm at the margins of the stock market. The current scenario implies that financial conditions are still loose enough for a bubble to expand much further before it gets punctured by its own contradictions. How much does all of this jibe with the likely future of the economy? Broadly, there are three plausible scenarios. One is that after receiving a few jolts of energy as we recover from Covid-19, the developed world economy returns to its old customary state, with minimal inflation, slow growth, and presumably yet more inequality. The deflationary forces remain insuperable. The second is the scenario that the Fed is hoping for; that after another two or three years with the foot firmly on the monetary accelerator, and with help this time from helicopter-aided fiscal policy, we at last move into a world where inflation tends to be somewhere north of 2%, and interest rates tend to be positive, while growth helps even out some of the injustices that have taken root over the last few decades. The third suggests that we move into a full-blown inflationary cycle. Just as inflation reached a point that could no longer be tolerated four decades ago, so weak growth and inequality can no longer be tolerated now; and so we steadily move into a world of inflation. In practice, it will be hard to tell between the first and the second for many months yet. There is a high likelihood of a transitory phase of inflation, at the very least, as we emerge from the pandemic. So both the first two scenarios remain alive for about a year. Meanwhile, the prospects for the second and third are hard to distinguish from where we stand now. It's difficult to fine-tune an economy so that it comes in exactly on target. Just ask any communist planner. It took at least a decade for the policy mistakes that created the Great Inflation to bring the world to a pivot point, probably longer. It's a fair bet that any move to a new regime would also take a while, with a few years of what felt like a healthy new norm followed by a more worrying descent into higher inflation. A look at real yields shows that the market is alive to this. Five-year real yields have continued to fall this year, showing great confidence that a dovish Fed and relatively controlled inflation are around for a while yet. But 10-year real yields have risen, suggesting the market sees a concrete difference between likely outcomes in the near future and a few years down the road.  To be clear, with real yields still negative, it isn't as though the bond market is signaling any great level of concern about inflation. But the progress of the 10-year real yield will be a critical measure to watch. As for the stock market, which stays aloft while bond yields are rising inexorably, we can all hope that the brontosaurus still doesn't get the message, and that the coyote doesn't look down. Survival TipsAfter my collection of "miserable day" songs yesterday, I've had plenty of suggestions for happy day songs. So try Day Is Done by Peter, Paul and Mary, Oh Happy Day by the Edwin Hawkins Singers, Beautiful Day by U2, Days by the Kinks, In-Between Days by The Cure, and Good Day Sunshine by the Beatles. = Pride of place has to go to Bill Withers' Lovely Day, one of the all-time greatest feel-good songs. I've offered it before, but it's worth listening to again and again. Please spend some time looking through a copy of Reminiscences of a Stock Operator by Edwin Lefevre this weekend — it's the subject of our next book club live blog on Wednesday next week. And have a great weekend. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment