| Welcome to The Weekly Fix, the newsletter that wants popcorn with those March projections. ---Emily Barrett, cross-asset editor, Asia.

Tough Love

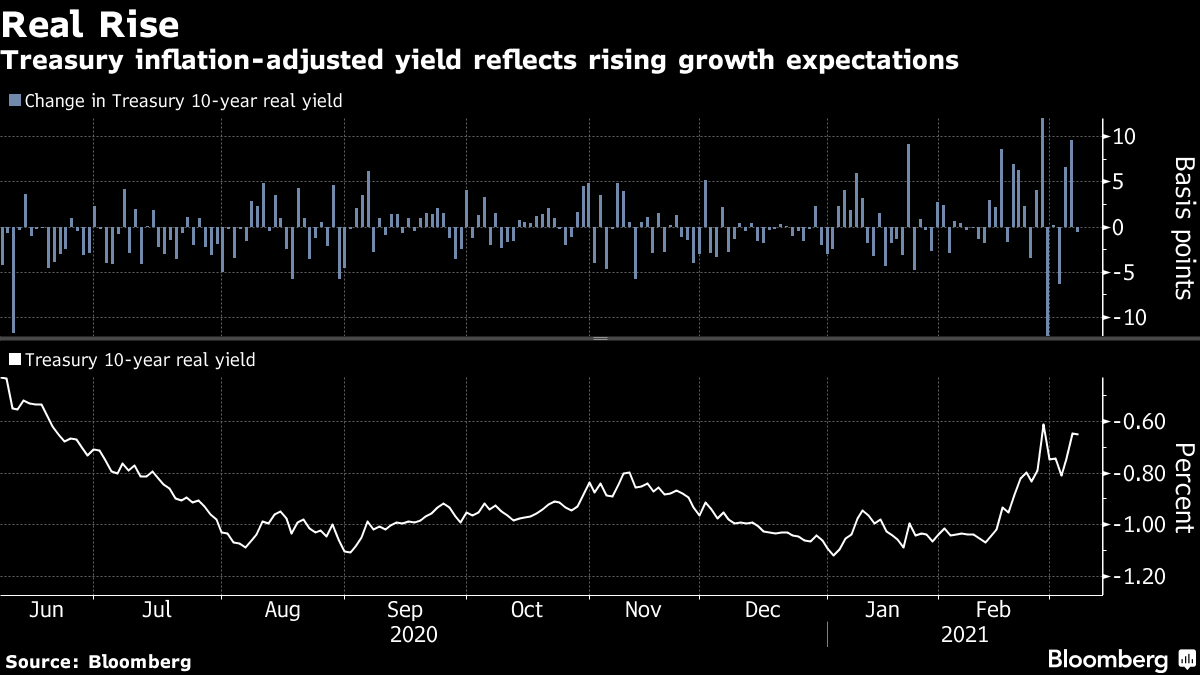

The market isn't used to hearing "no" from the Federal Reserve. But that's what it got this week, as Chairman Jerome Powell stuck doggedly to the script and gave no sign of an intention to rein back what's now a pretty substantial rise in yields. Now traders have a week of silence from the U.S. central bankers, who are observing the customary blackout ahead of their next policy meeting. What to do? The odds of an Operation Twist to buy more longer-dated bonds are looking slim. Yield curve control, a pipe dream. So the path of least resistance seems to be to drive benchmark rates higher. And that's what the market did in a renewed bout of selling following Powell's comments. Meanwhile, the Street continued revising forecasts for the 10-year yield. Goldman Sachs has bumped theirs up to 1.90% from 1.50% by year end, and TD Securities now sees it at 2%. More surprisingly, the market is pricing strong odds of a first rate hike by the end of next year. This seems pretty aggressive, but the main point is, traders really aren't sharing the Fed's caution on growth. That's clear from the recent jump in real yields, which are now around their highest since June (though still emphatically negative).

While the positioning for hikes looks overdone, a ratcheting-up of expectations seems in order. After all, the Fed's last assessment of the economic outlook and projections for interest rates (in which most policymakers saw no change through 2023) are now very stale. They're from December of last year -- before the Democrats' unexpected victories in the Georgia Senate races ostensibly cleared the way for larger spending packages. And before another $1.9 trillion in near-term aid or a follow-up infrastructure package looked possible. And also before much of the flurry of positive news on the vaccine rollouts, which have boosted morale, investment plans and risk appetite.  And in his speech Thursday, Powell seemed to have completed a pivot from talking about lift-off as determined by the path of the virus -- as he has in prior months -- to depending "entirely on the path of the economy." It's a risky juncture for the Fed. The updated economic projections are released with the policy decision on March 17, and they're likely to look more optimistic -- and so more hawkish to the market -- than they did in December. The trouble is if the market, having already front-run a stronger recovery, takes this as an endorsement to push yields higher and faster still. Turning the market's attention to how incoming data are shaping up relative to the Fed's more ambitious labor-market and inflation objectives is important. The Fed needs it not to preempt a fully-fledged recovery until the encouraging figures we've seen so far prove sustainable. Powell wants an economic upswing that lifts lower-income and marginalized Americans too, and an overeager rates adjustment could jeopardize that. Where Are We Now?Yields aren't at worrisome levels. The U.S. benchmark, at close to 1.60%, is only regaining the altitude it had just before Covid-19 was declared a pandemic. But the speed of the move -- more than a half percentage point year-to-date -- has unnerved markets, and Powell and his colleagues admit it's "caught" their eyes.

"Everyone was talking about low rates forever and suddenly they're caught wrong-footed," said Natixis chief economist Alicia Garcia-Herrero.

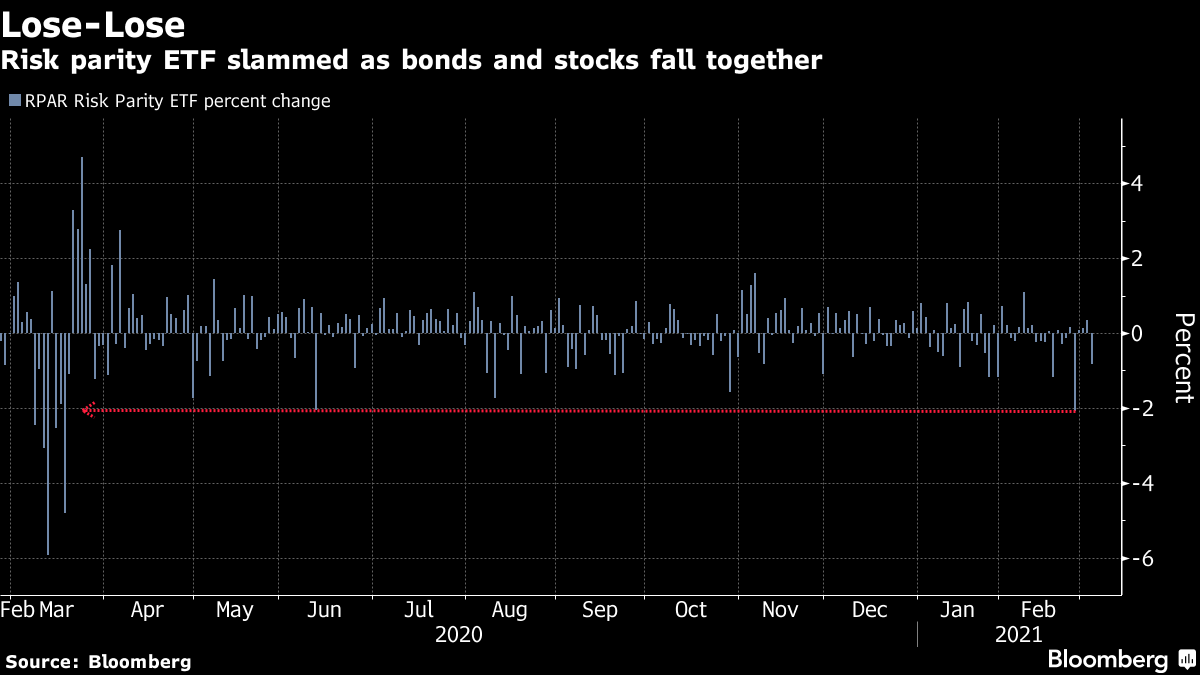

So everyone is now watching, in case what most people are still calling a "normalization" turns into a tantrum. In the U.S., the fallout beyond tech stocks hasn't been too dramatic. While the Nasdaq 100 is down almost 10% from its February high, the S&P 500 is still a way off this technical correction territory. The cost of protecting investment-grade corporate bonds from default is at a four-month high, though it's rising.  The dollar has advanced almost 2% this year, which in Garcia-Herrero's view is a subdued move given the talk of surging yields, which ought to drive waves of capital into the world's largest economy. That said, it could well be at a tipping point, cross-asset maven Cormac Mullen points out, thanks to an abundance of short positions -- the hangover from a weakening trend last year. A further gain in the greenback could send traders rushing to cover those bets, adding fuel to its rise. The view from outside the U.S. is getting a little more fraught, as local currency bonds across emerging markets have started to shed gains made in light of a brighter outlook for the global economy. Lisa Chua, emerging markets portfolio manager at Man GLG, told our rates reporter Ruth Carson that local bonds "have limited cushion left to absorb further increases in U.S. 10-year yields beyond current levels of around 1.5%." She sees a likelihood of a larger exodus as the benchmark approaches 2%.  And we may have hit a turning point in a long trend of declining government borrowing costs, as a string of sovereign debt sales globally showed investors stepping back or pushing for higher rates. The lowlight was arguably a disastrous auction of U.S. seven-year notes a week ago, which drew the weakest ratio of bids on record. Offerings from Indonesia to Japan and Germany have drawn tepid demand, and Mexico scrapped a sale.

All in all, these stirrings of bond vigilante-ism may complicate efforts to finance $14 trillion worth of fiscal stimulus globally. Though there was a silver lining in the sale that bucked the low-energy trend: Italy was swamped with orders for its inaugural green bond. Movers and ShakersCLSA Ltd. has lost more than half of its fixed income team that focuses on bond sales in Hong Kong after its Beijing parent tightened control over the brokerage Merrill Lynch Wealth Management is intensifying its focus on the Sunshine State. The firm has 20 teams that cater to ultra-high-net-worth individuals there, and plans to double that over the next few years Eric Lane, the co-head of Goldman Sachs Group Inc.'s asset-management business, is quitting the firm to join Chase Coleman's Tiger Global Management Bank of America Corp. named Moritz Westhoff its new head of U.S. Treasury trading after two senior bond traders left the company. One by one, most of the biggest U.S. banks pledged to avoid workforce reductions almost a year ago as coronavirus infections erupted in New York City. One by one, those vows have given way. Bridgewater Associates named Nir Bar Dea as a deputy chief executive officer, following last year's record loss at the $150 billion investment firm's flagship hedge fund.

Bonus PointsZoltan Pozsar takes the OddLots crew on a tour of the latest mess in the Treasury market  Ranking global Covid-19 responses. The Goldberg Variations, upside down |

Post a Comment