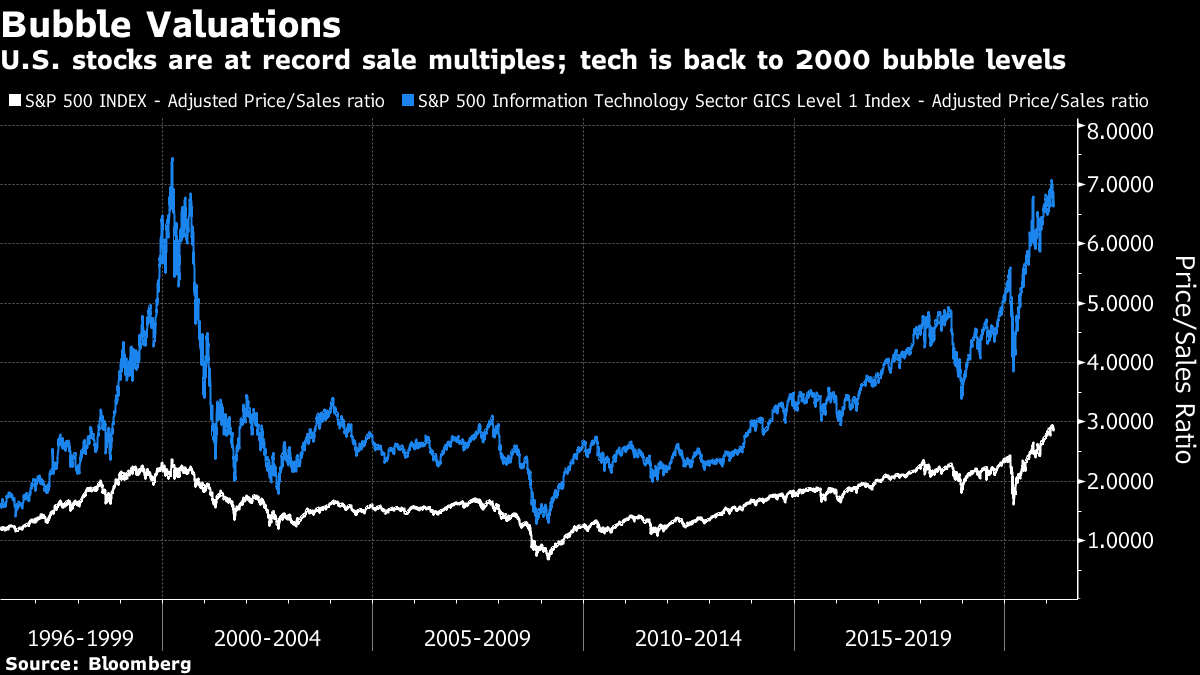

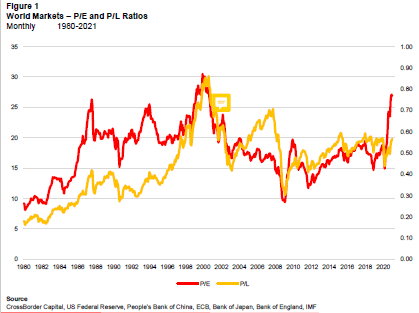

Back to BubblesA new month, and a new attitude to menacingly rising bond yields. Strong manufacturing data from the U.S. and western Europe, and a rebound for Treasury yields, didn't stand in the way of a rally in stocks. U.S. equity markets are almost back to all-time highs. GameStop Corp. shares rose again, as did the prices of bitcoin (up 14.4% from its Sunday low at the time of writing), and Tesla Inc. (up 6.5%). This renewed optimism may or may not persist. But it is worth returning to the debate that was consuming commentators until last week's reflation spasm: Is the U.S. stock market in a bubble? There is a difference between a bubble, which implies overextended and unsustainable valuations that can only be corrected by bursting, and an overvalued market. Stocks don't exist in a vacuum; other asset classes matter. And there is little case that there are true speculative bubbles outside the U.S. In the U.S., there is a case to answer. The following chart shows the price-sales multiple for the S&P 500 and for its information technology sector over the last 25 years. On this simple basis, the broad market is its most expensive ever, and the tech sector is almost as pricey as it was at the peak of the 2000 internet bubble:  l What reputable arguments are there against this? Perhaps the most important one comes from liquidity. There is a lot of it about, with broad measures of money growing as never before after central banks' response to the pandemic last year. Michael Howell of Crossborder Capital Ltd. in London argues that earnings and sales multiples don't work at a macro market level, even if they do for stockpickers. Howell points out that markets are frequently characterized by a dominant financial cycle, which, in turn, "is driven by shifts in liquidity and in investors' risk appetite." This leads to a search for a broad measure of liquidity; when prices are high compared to liquidity, that is a clue that risk appetite has become excessive. Here are his estimates for price-earnings (in red) and price-liquidity (in yellow) for world markets over the last four decades:  On this basis, the market looked as expensive in terms of liquidity in 2000 as it did in terms of earnings, while Howell's measure also produced a good warning that risk appetite was getting out of control before the global financial crisis eight years later. Now it suggests that global risk appetite is roughly back at the top of its range for the post-crisis decade but no more than that, even as earnings multiples suggest that the market is screeching toward a repeat of 2000. On this view, the danger at this point isn't of risk appetite bubbling over, but of liquidity being allowed to stop too quickly. The analysis confirms that central banks have a very tricky job ahead of them, which is completely in line with intuition after the extreme steps they took last year. But they don't need to worry about deflating a bubble in the equity market, at least at the global level. As for the concept of "global liquidity," it was originally developed at Salomon Brothers. Here is Howell's brief definition: It is 'global' because it covers 80 economies and includes cross-border flows, and it is 'liquidity', rather than the traditional, narrower measure of 'money supply' based on retail banks, because it extends to non-bank credit providers, such as so-called shadow banks. These rely on collateral and operate across the wholesale money markets.

His thesis is fascinating and there is obviously lots of room to argue over definitions, but there is plainly much merit in his basic point that this spike in price-equity ratios is more a response to an unprecedented gush of money than a classic case of animal spirits. Another convincing push back at the notion of the bubble comes from Ray Dalio, founder of Bridgewater Associates and one of the world's most powerful investors. Last week he published his own proprietary checklist of whether U.S. stocks were in a bubble. His bottom line: In brief, the aggregate bubble gauge is around the 77th percentile today for the US stock market overall. In the bubble of 2000 and the bubble of 1929 this aggregate gauge had a 100th percentile read.

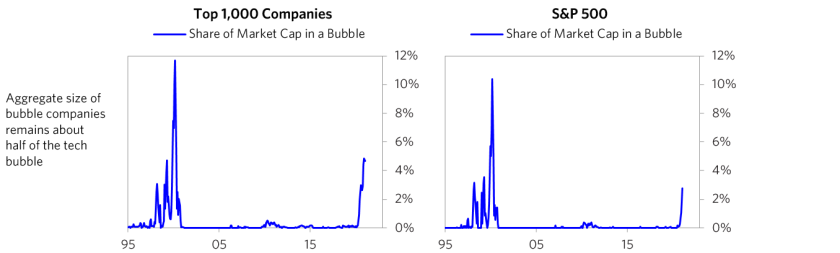

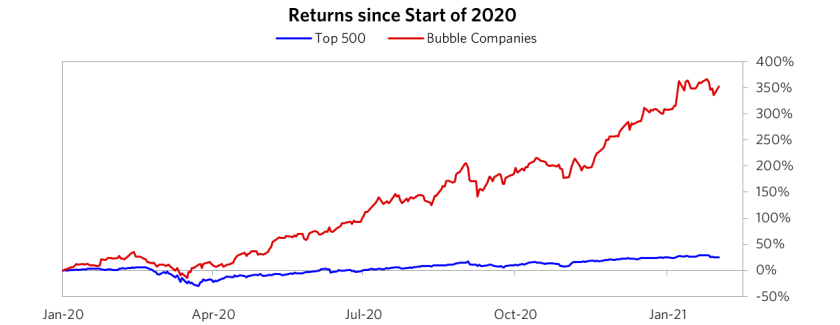

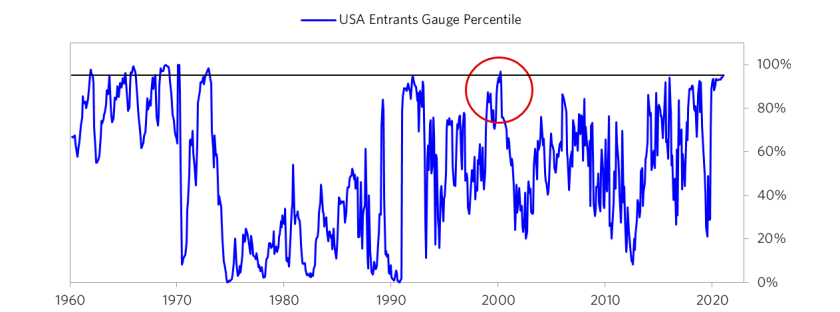

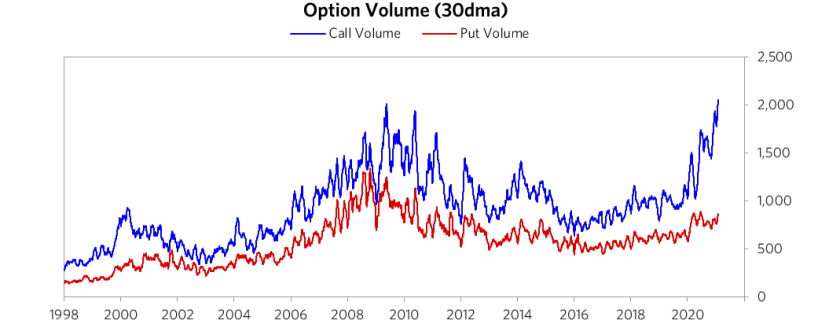

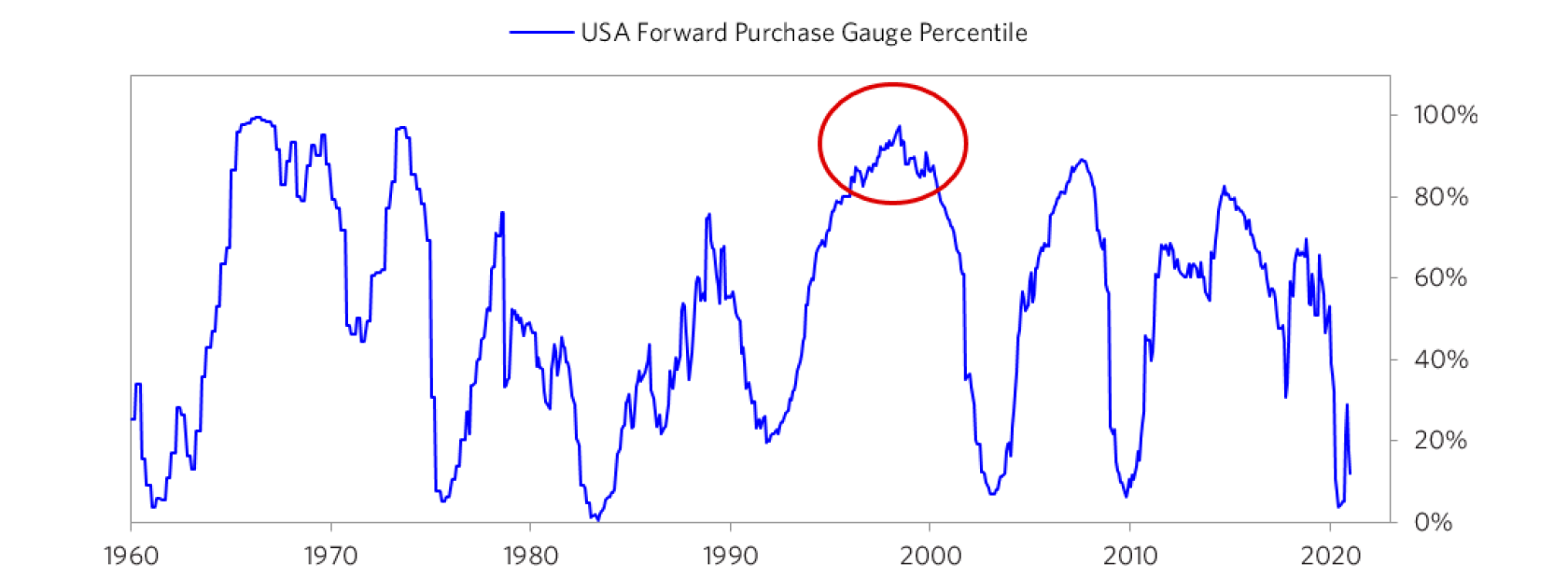

So by Dalio's reckoning, we have a somewhat expensive market, and not a historically great time to buy, but nothing that requires immediate action. That is for the market as a whole. He does look at individual companies, and comes up with a measure for how many are in a bubble: roughly half as many as at the top in 2000. There is something to worry about here, but nothing like as terrifying as 21 years ago:  This is how the companies Dalio classifies as bubble-icious have performed compared to the S&P 500 since the beginning of last year. Evidently, the monetary desperation tactics at the outset of the pandemic have much to do with the bubbles in tech:  Dalio doesn't go into all the details of how he comes up with his secret sauce, but he does show us what broad criteria look most scary, and which give greatest cause for relief. One measure is the number of new entrants to a market. The more there are, the more dangerously overblown conditions are. On this measure, last year's influx to discount broking has almost led us back to 2000:  Dalio also agrees with many other observers that the extreme interest in call options in individual stocks (used to bet that their share price will go up) is a danger signal, particularly when compared with interest in put options, which protect against prices falling:  However, Bridgewater doesn't see excessive leveraged activity outside the retail sector. The key measure that keeps his measure of bubble risk as low as it is concerns willingness to make forward purchases. Dalio explains this as follows: We apply this gauge to all markets and find it particularly helpful in commodity and real estate markets where forward purchases are most clear. In the equity markets we look at indicators like capital expenditure—whether businesses (and, to a lesser extent, the government) are investing a lot or a little in infrastructure, factories, etc. It reflects whether businesses are extrapolating current demand into strong demand growth going forward.

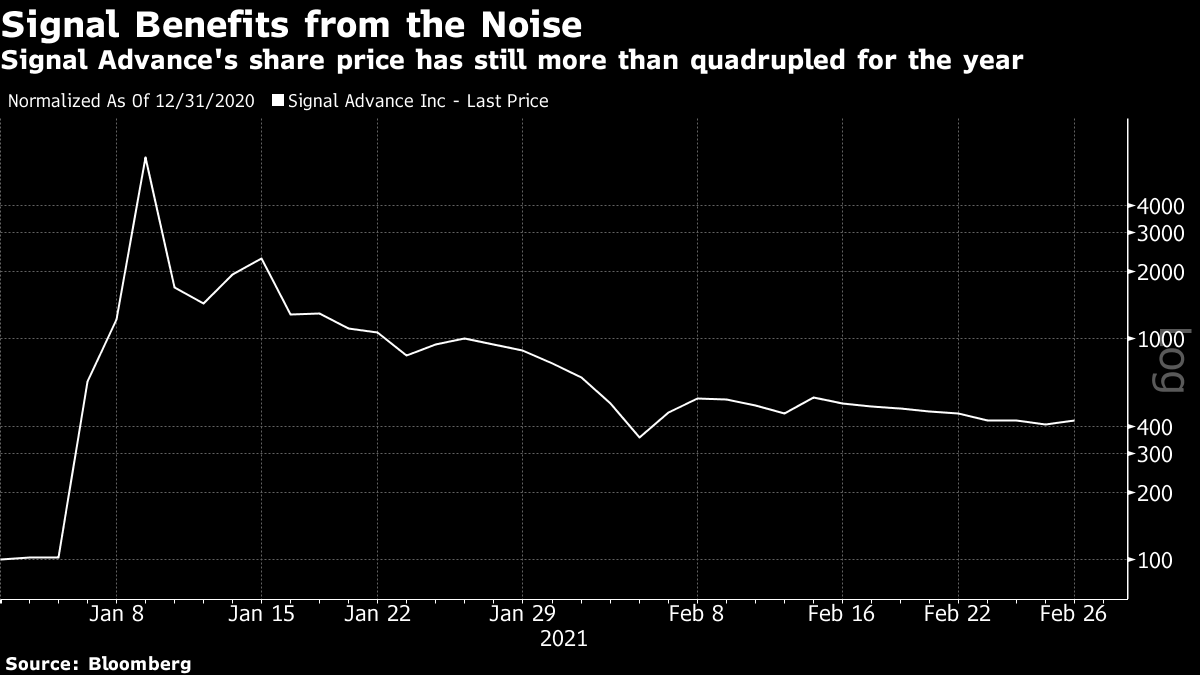

At present, relatively subdued levels of mergers and acquisitions, and of capital expenditures, suggest that people aren't relying on such strong demand growth into the future:  A major resurgence in such activity could easily bring Dalio's measure into bubble territory. As it is, his exhaustive quantitative techniques suggest that we have bubbles forming in the speculative end of technology, but that the reaction of the market as a whole to last year's splurge of liquidity isn't excessive. As with Howell's approach, that still leaves the nagging question of how we deal with an unprecedented gusher of money; but we aren't talking about a direct repeat of 1929 or 2000. "Irrational Exuberance" or "Stupidity"?One final measure of bubbliness is behavior. As Jeremy Grantham of GMO put it, when he warned that stock markets were in a new "bona fide" bubble, "crazy" behavior is the best indicator that a climax is approaching. There is plenty of bonkers behavior around. Some of it crosses the line from "irrational exuberance" (taking a good idea way too far) into stupidity. Exhibit a) is Signal Advance Inc., whose shares rocketed in January after Elon Musk tweeted a recommendation to switch to Signal, an unrelated communications app. That case of mistaken identity was cleared up a month ago. But anyone who happened to hold Signal Advance at the beginning of the year, before Musk's tweet, is still sitting on a 300% gain. The stock has quadrupled thanks to a momentary misunderstanding from six weeks ago, which the market hasn't bothered to correct:  This isn't over-exuberant so much as plain dumb. Meanwhile, on the subject of signals, another indicator that markets are growing distracted is that it is harder to tell the difference between signal and noise. Last week I commented that Cathie Wood, manager of the hugely successful Ark Investment Management, had managed to reverse a dip in Tesla's share price virtually single-handed with the announcement that she was buying shares. Here are two contrasting responses to that comment. One reader wrote: When someone with deep pockets buys a bunch of stock in a company, that isn't "noise." In fact, it's the very definition of "signal" in the markets. The only way it's noise is if the buyer hasn't done their research and is just investing capriciously, but that's unlikely to happen with a high-value purchase -- and certainly isn't the case with Cathy (sic) Woods (sic) and ARK Invest.

I think this is nonsense. The ARK Innovation ETF has been very successful. It's still not that big, and we know that Cathie Wood has been a committed buyer and fan of Tesla for a while. Her actions might count as a "signal" to a small group of devoted fans. It isn't a major market signal. I also received this comment: Prior to your column, I'd never heard of her. I know a few traders like myself, and most of us, perhaps by being in the much-maligned "Boomer" category, pay very little attention to what goes on in the financial media… We read, perhaps, 1 or 2 commentators, keep abreast of general news developments, and may have one dedicated market news source… My point being, that far from being deafened by Cathie Wodd's (sic) or anyone else's noise, we actually do much better by not being at all aware of such noise.

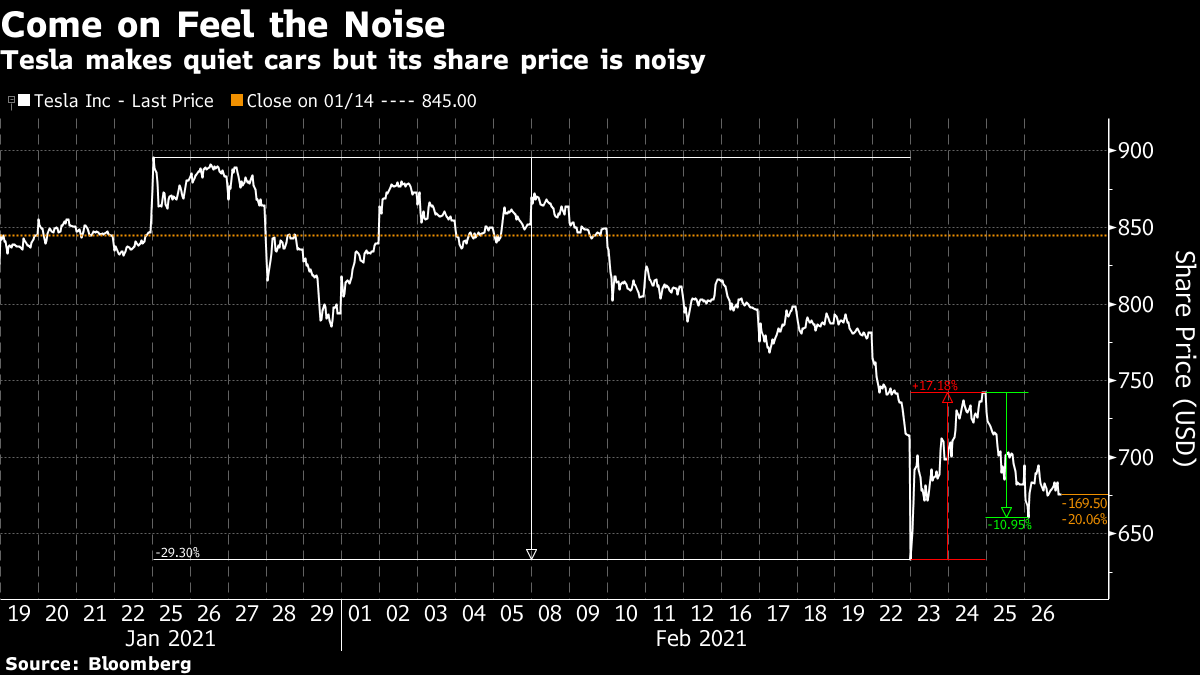

My sympathy is more with the "boomer." I also have great sympathy for Wood. My surname is often misspelt, which is irritating, but at least it's an unusual name. At hectic times like this, virtually everything about a stock like Tesla is "noise" and best tuned out. This is the stock's progress since it topped at close to $900 per share barely a month ago:  That is as noisy as it gets. And, to be clear, none of this is criticism of Wood herself. Her flagship fund's performance brooks no argument:  I still wouldn't want to be led by a fund that has recently enjoyed performance like that. Such performance can't be sustained, even if managers continue to make exemplary decisions. As a cautionary tale, I offer this chart of the rise and decline of the fund known for most of its life as the Legg Mason Value Trust. About 15 years ago, whole conferences would be given over to discussing the remarkable streak of its manager Bill Miller, who used a value style of investing to beat the S&P an incredible 15 years in a row. This makes him the Joe DiMaggio of fund managers; such consistency plainly showed great skill. However Miller, like Wood now, had a style that worked for the time in which he was operating. When the market turned against value stocks, it did so with a vengeance. Once the streak was broken in 2006, the portfolio suffered a staggering run of underperformance, lagging the S&P by 50%:  None of this meant that Miller wasn't a good manager. But market-beating like that requires a concentrated style. If you wanted to know good value stocks to buy, it was worth following him forever. If you wanted to know whether value would continue to outperform, not so much. Similarly, Cathie Wood is obviously an exceptionally talented tech growth investor. Her decisions don't tell us whether tech growth stocks will continue to outperform. There is something of a personality cult around her at present (which isn't her fault) and that suggests deeply irrational exuberance, if not outright stupidity, in a corner of the market. Survival TipsOK, something to raise the spirits. The Blues Brothers is streaming again. I was a bit too young for it when it came out, but what great fun, and what great evidence that Saturday Night Live really was better in the old days. This is Soul Man as performed on SNL; and this is Everybody Needs Someone to Love from the movie. I'd say it was the funniest rock and roll movie of all time — except of course for This Is Spinal Tap, which goes to 11. Anyone disagree? Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment