|

Welcome to The Weekly Fix, the newsletter that's all for very enthusiastic debates on asset purchases. I'm cross-asset reporter Katie Greifeld.

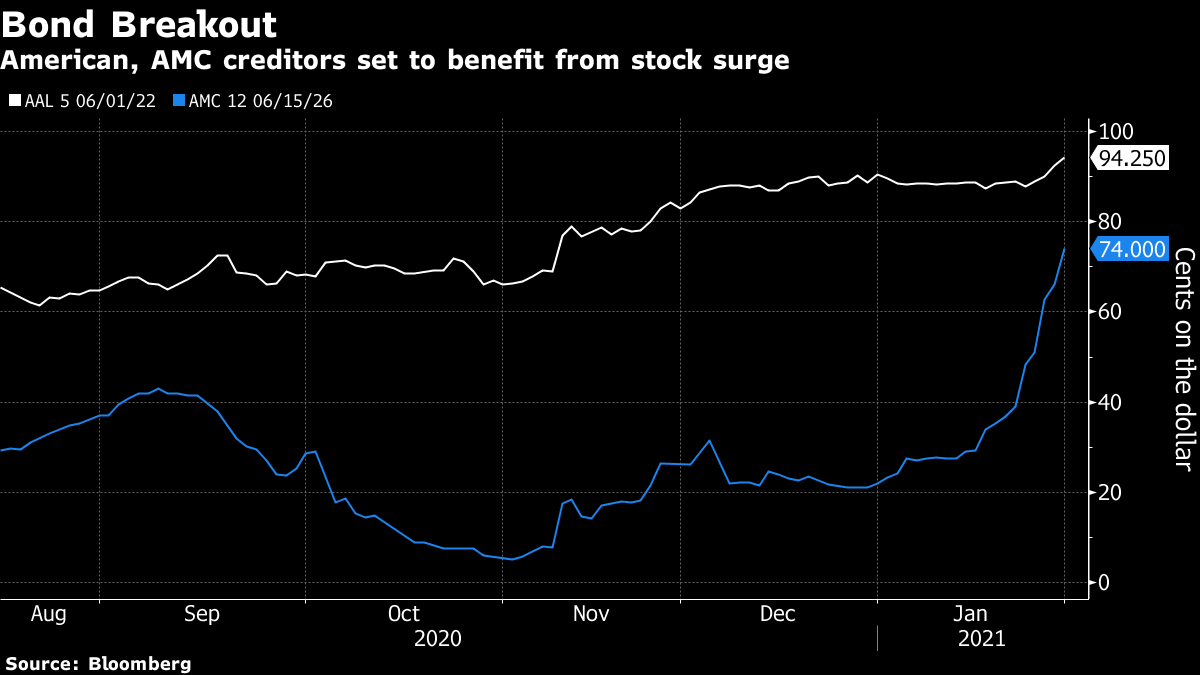

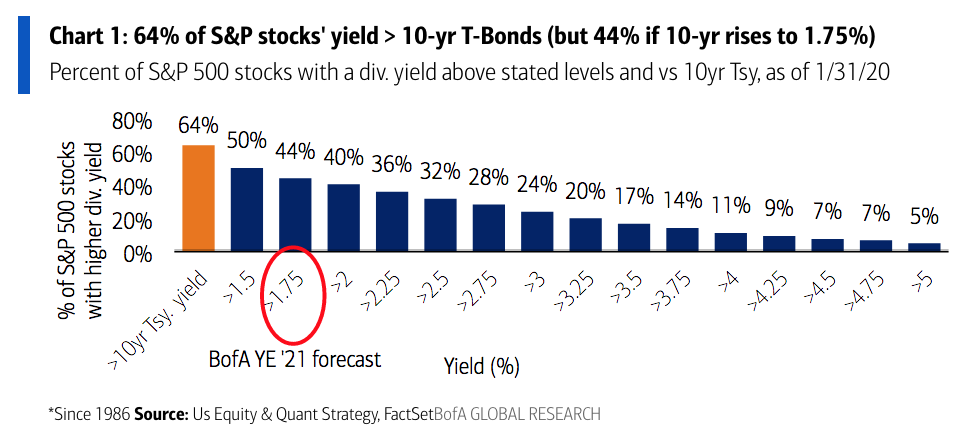

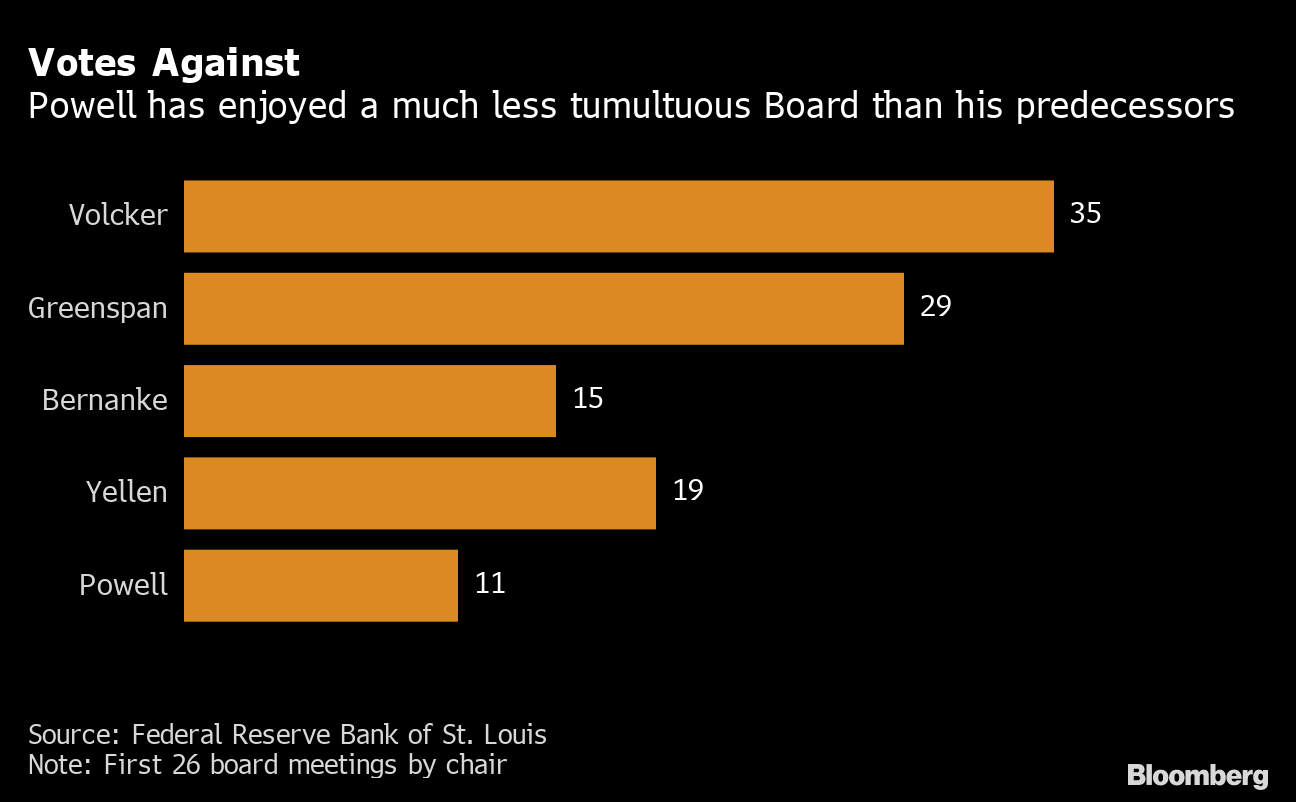

Staying AliveWe're well past peak "GameStop" -- last week's Saturday Night Live skit was the summit -- but if you'll indulge me, the WallStreetBets day trading phenomenon created some fascinating ripples in the corporate bond market. While it's tempting to view the past few weeks as a sideshow isolated to the equity markets, those meme stock moonshots translated into real-world impacts on the capital structures for some of the companies caught in the fray. AMC Entertainment Holdings Inc. is perhaps the most dramatic example. In their quest to crush short-sellers, Reddit traders bid up AMC shares by over 525% in January, pushing prices as high as $20 on an intraday basis. That was a magic number for the likes of private equity firm Silver Lake Management, which converted $600 million of the struggling theater chain's 2.95% bonds to equity at a price of $13.51 a share. While that resulted in a tidy payout to the tune of $113 million for Silver Lake, it also erases a sizeable chunk of debt from the struggling cinema company's balance sheet. And that's not all -- AMC was able to raise roughly $300 million last week through an at-the-market equity program, which essentially allows companies to issue additional shares at market prices. That's huge news for AMC, which has suffered massively after the pandemic forced theaters to shut in the firm's major markets. The fresh funds should help AMC avoid the dreaded "zombie" status -- when a company isn't able to generate enough revenue to cover its interest expenses.  "By lowering your debt-to-earnings ratio, it opens up the funding window at more reasonable prices going forward, because all these companies are going to have to refinance anyway," said Chris White, chief executive officer of BondCliQ, a market data system for U.S. corporate bonds, in an interview. "The equity trading at $1,000 per share, for AMC, that doesn't change their prospects much. But if you look at how they're structured from a debt standpoint, if it helps their debt-to-earnings ratio that their stock is trading at this level because people can convert out, now there's actually a tangible benefit to the Reddit phenomenon for AMC." It's not just AMC. SunPower Corp.'s convertible 4% notes due in 2023 skyrocketed as the company's shares shot over 110% higher in January (they've since fallen over 25% so far this month). Meanwhile, American Airlines Group Inc. -- another company rocked by the pandemic -- plans to sell as much as $1.1 billion of stock, also through an at-the-market program. Interestingly, there hasn't been much action (from a fixed-income standpoint) in the company at the eye of the Reddit storm. Rather, GameStop's 10% notes due 2023 have traded close to par throughout the last few weeks. That's because unlike AMC, the perception of whether the video game retailer will be able to pay off its debt hasn't changed, White said. "The real story on what's going on with any company is being told in the debt markets," White said. "What this Reddit phenomenon is doing is clearly articulating that a company's equity can be decoupled from the company itself." Hedging on the CheapBeyond the shores of AMC island, the sea of corporate credit has been remarkably calm. While the Cboe Volatility Index -- known as the VIX -- is stuck at stubbornly high levels, high-grade and high-yield fear gauges have barely budged in 2021, despite the single-name hysteria. There are a few interesting quirks at the heart of both markets which explain why. While equities have been overrun by retail traders in some respects -- take a look at options markets and penny stocks -- corporate debt remains largely outside of the individual investor's grasp (It's worth noting that zero-fee platform Robinhood, where traders can gallivant in stocks, options, gold and crypto, doesn't allow fixed-income trading). Exchange-traded funds such as the iShares iBoxx $ Investment Grade Corporate Bond ETF (ticker LQD) offer an entry point, but to a broad swath of bonds rather than a single name. Additionally, while the WallStreetBets crowd targeted companies with high levels of short interest to force a squeeze, betting against corporate debt isn't as straightforward. For one thing, funding a short position against a company's bonds for an extended period of time is an expensive proposition, said BondCliQ's White. Additionally, it may be tricky to even find bonds to short, points out Hirtle Callaghan & Co.'s Mark Hamilton. "You can do it, credit hedge funds do it, but it's not as widespread and it's not something that's going to make the papers in the same way," said Hamilton, the firm's chief investment officer, in an interview. "I wouldn't say it's as readily available as shorting is in equities, because there's typically a significant amount of the bonds locked away by long-term holders."  That placidity in credit markets -- particularly in junk bonds -- has created an opportunity for investors to pick up cheap hedges, in the eyes of Tallbacken Capital Advisors LLC's Michael Purves. Bloomberg data going back to 2015 show that the ratio of the Cboe High Yield Corporate Bond ETF Volatility Index to the VIX is near historically low levels. Given that implied volatility feeds into option pricing, that means that credit markets offer relatively inexpensive protection, according to Purves. That dynamic creates "a good opportunity to find some protection for long credit positions and/or a pan-asset de-risking," Purves wrote in a recent note. There Is (Maybe) an AlternativeA common refrain in markets is that with global rates so low, investors are being pushed into riskier securities, such as stocks -- the "there is no alternative" attitude. The yield-seeking behavior that environment fosters is often blamed for inflating asset bubbles. However, Bank of America thinks the end of TINA may be in sight. Currently, over 60% of the stocks in the S&P 500 carry a dividend yield higher than the 10-year Treasury yield, which is around 1.13%. Should benchmark rates climb to 1.75% by year end -- Bank of America's current house view -- that total would drop to 44%, making the bullish TINA mantra for stocks "less compelling," the analysts wrote.  Bloomberg Bloomberg "A move higher in rates, forecast by our rates team, would likely be most painful for themes that have thrived over the last few decades," wrote Bank of America strategists led by Savita Subramanian in a note Thursday. "Both ends of the equity duration spectrum are at risk: long duration growth stocks that benefited from a falling discount rate could suffer a reversal of fortune. And short duration high-coupon stocks with no room to raise dividends would pale relative to bond income." Judging by ETF flows this year, it doesn't look like investors are seriously prepping for that possibility yet. Nearly $41 billion has poured into U.S. equity ETFs so far in 2020, outpacing inflows of roughly $24 billion into fixed-income funds, data compiled by Bloomberg show. Still, it's worth noting that the reflation trade picked up further steam this week. Five-year breakeven inflation rates hit the highest level since 2013, while the 5s30s Treasury yield curve climbed to the steepest since 2015. The long-bond selloff was fueled in part by the U.S. Treasury keeping next week's refunding at a record size. The Bank of England delivered another bump Thursday, with an assurance that the U.K. economy is heading for a rapid rebound. While the Federal Reserve seems to have successfully convinced markets that interest rates aren't moving for the foreseeable future, what a roiling reflation trade means for the future of its asset purchases is an open question. Though some officials have discussed the idea of a 2021 taper, Fed chair Jerome Powell reiterated last week that "the whole focus on exit is premature."  As Bloomberg News reported this week, Powell has enjoyed fewer dissents from Board members than his predecessors. But that tranquility may not last. Last week, Dallas Fed President Robert Kaplan said he expected "very enthusiastic debates" about scaling back asset purchases. "I think they're going to have a very difficult time holding the very accommodative line over the course of this year," said Mark Cabana, head of U.S. interest rates strategy at Bank of America, in a Bloomberg Television interview. "As growth picks up, supported by fiscal policy, it's going to be increasingly difficult for the Fed to keep saying that it's appropriate to keep the asset purchases." Bonus PointsTreasury Department says U.S. market infrastructure was ``resilient'' during Reddit frenzy Long before GameStop, there was Piggly Wiggly Welsh sheepdog Kim sells for world record £27,100 |

Post a Comment