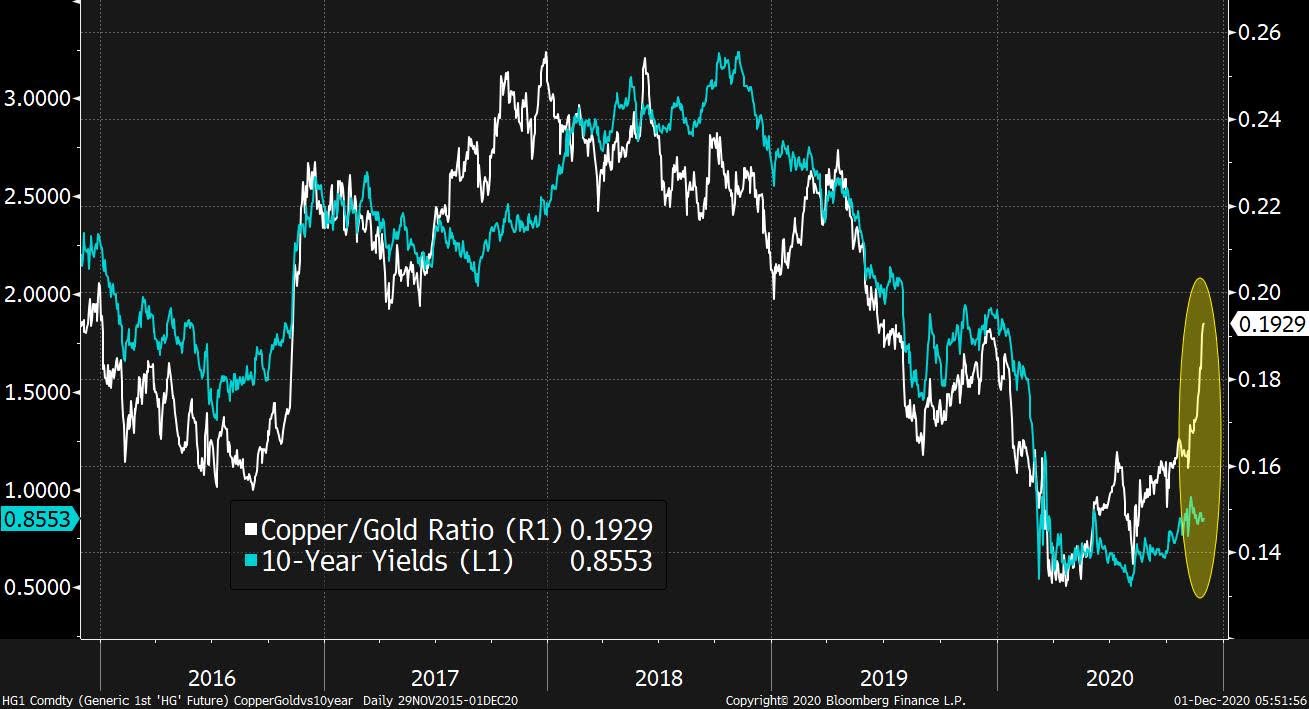

| More vaccine progress, Powell and Mnuchin testify, and OPEC+ talks delayed. Coming soonPfizer Inc. and partner BioNTech SE sought regulatory clearance for their Covid-19 vaccine in Europe, following a similar move from Moderna Inc. yesterday. This puts the vaccines on track for approval before the end of the year. Vice President Mike Pence signaled a swift response from U.S. regulators, saying that distribution of a vaccine could begin as early as the third week in December. Separately, there is new evidence that Covid-19 was in the U.S. earlier than previously recognized with a study finding infections in blood samples collected in late 2019. Powell testimonyFed Chair Jerome Powell's prepared testimony released ahead of his appearance in front of the Senate Banking Committee this morning show him in classic economist mode. On the one hand, he welcomes the rapid development of the vaccine, while on the other hand he warns that the current surge in Covid cases in the U.S. could prove challenging in the coming months. Treasury Secretary Steven Mnuchin will also appear before the committee today and will likely be questioned about the recent spat between his department and the Fed. No dealDespite a pre-meeting meeting of ministers on Sunday and a meeting of OPEC members yesterday there still is no consensus among members of the cartel and its allies over production levels once the current curbs expire in January. This has meant that today's planned OPEC+ gathering to finalize a deal has been postponed until Thursday to give more time to find a compromise. While the crude market is no stranger to long and difficult OPEC meetings, the impasse is unsettling traders, with oil having another volatile session today as futures swing between gains and losses. Markets riseGlobal equity traders are starting the month on a positive note with strong factory data from Asia adding to vaccine optimism. Overnight the MSCI Asia Pacific Index rose 1% while Japan's Topix index closed 0.8% higher. In Europe, the Stoxx 600 Index had gained 0.8% by 5:55 a.m. Eastern Time with miners and banks among the strongest performers. S&P 500 futures pointed to plenty of green at the open, the 10-year Treasury yield was at 0.837% and gold regained some ground. Coming up...Third-quarter GDP for Canada is at 8:30 a.m. with economists expecting annualized growth to be close to 50%. November Markit manufacturing PMI for the U.S. is at 9:45 a.m. Autosales data for November is published today. At 10:00 a.m., Powell and Mnuchin appear before the Senate Banking Committee. Fed Governor Lael Brainard, San Francisco Fed President Mary Daly and Chicago Fed President Charles Evans speak later. Salesforce.com Inc. is among the companies reporting results. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningThere's a pretty longstanding relationship between the yield on 10-year U.S. Treasuries and the ratio of copper prices to gold. When the global economy is gathering steam, and people feel more optimistic about an industrial recovery, the price of copper goes up relative to gold, as people desire to hold industrial metals as opposed to precious metals that don't benefit from the boom. Meanwhile in such environments, there's less demand to hold safe-haven Treasuries, as the rebound can (typically) be expected to push rates higher (all things being equal).

And yet over the last several months we've seen a break in this link, with the copper-gold ratio soaring back to pre-crisis levels while the 10-year yield remains stuck near all-time lows, having barely bounced off this year's bottom. There's good reason to think that what's happening in this chart is a demonstration of the Fed's power and the effectiveness of its new framework. Remember earlier this year the Fed gave two clear messages about how it would no longer be doing business as usual. First it said that it would aim for inflation to average 2% over multiple years, essentially indicating that it would not be inclined to hike rates unless there was evidence that the rise in inflation would be sustained in some way. It also said that it would not hike rates again until we got back to some level of full employment. Basically, in the past the Fed hiked early, before hitting its goals in order to pre-empt overheating. In this expansion the Fed will be patient.  So back in the day the signals that would drive the copper-gold ratio higher (industrial recovery, burgeoning investor confidence etc.) would also be seen as signals that would prompt the Fed to consider hiking -- driving rates higher over time. But the Fed has already said that there's almost nothing that can happen in the short-term that would prompt a rate hike. It was back this summer that Powell said the Fed wasn't even thinking about thinking about hiking rates.

And so we see this relationship breaking down, where the factors driving copper higher relative to gold are not enough to really put rate hikes on the table, causing the 10-year yield to hang out at rock bottom levels, even as numerous other things in the market point to a surge in optimism. Joe Weisenthal is an editor at Bloomberg. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment