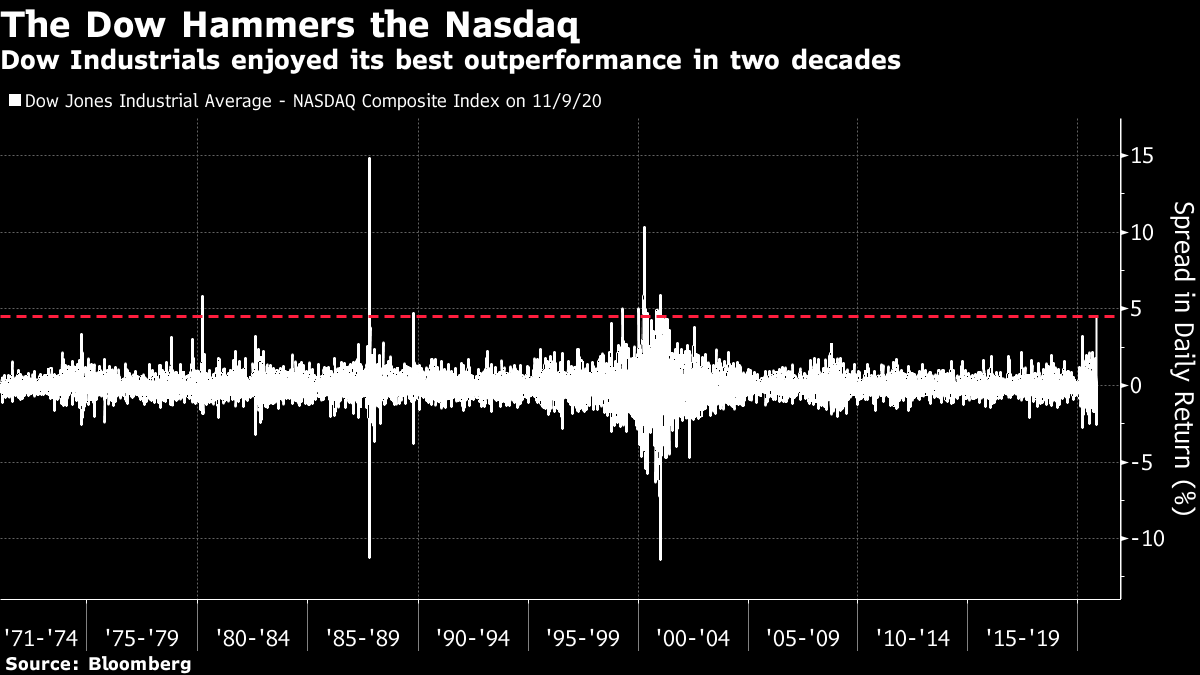

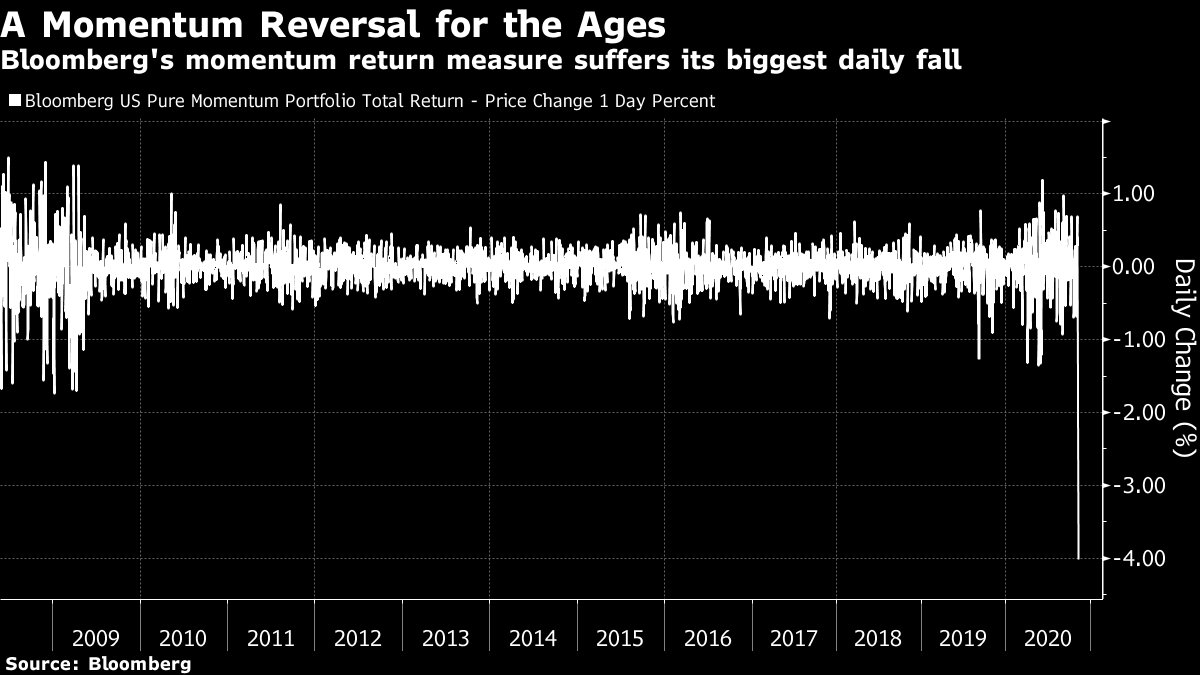

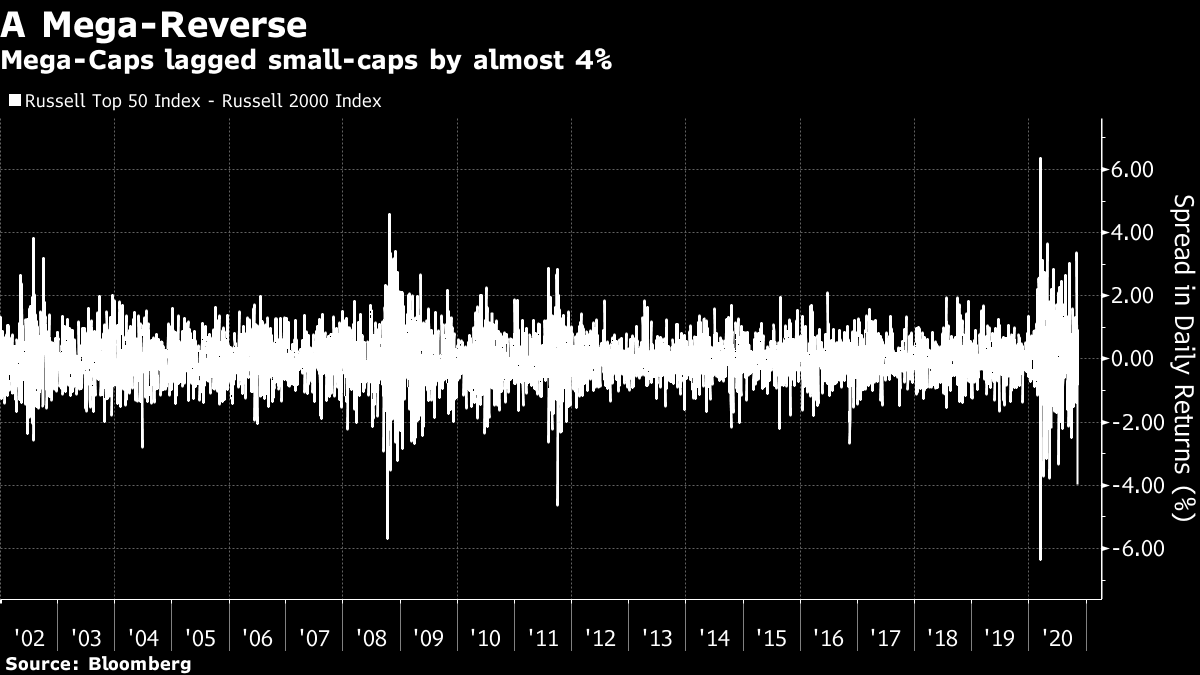

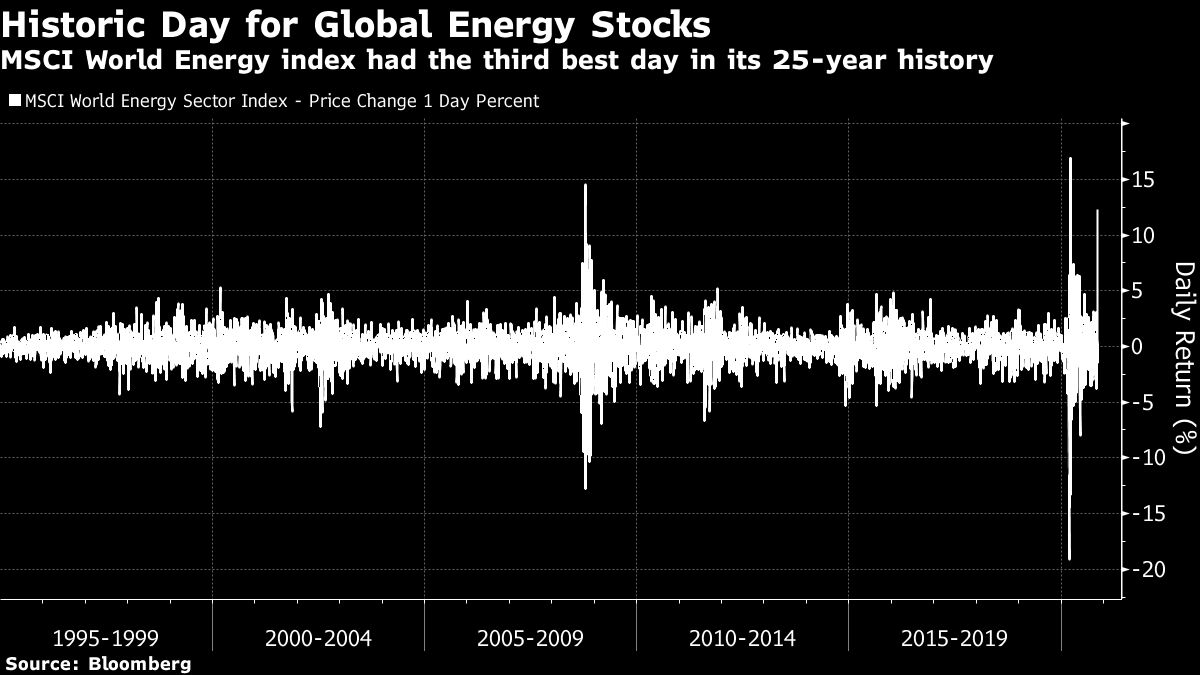

A Shot in the ArmMarkets received a shot in the arm Monday from Pfizer Inc. and its encouraging Stage III tests on a Covid-19 vaccine. As a result, the S&P 500, the MSCI World and the MSCI All-World indexes all rose to records. But that misses the point of the impact. The news triggered the biggest single-day market rotation I've witnessed in the 30 years since I started covering markets. I'll return to the vaccine and whether it really merited this reaction below. For now I want to illustrate, with bountiful charts, just how extreme a rotation this was. That isn't just because the test was big (and undeniably good) news; it's also because of the market's state when the news broke. All year long, stocks have been led by the outsize internet platform groups known as the FANGs. We know they are very strong and profitable companies; but they have also benefited from the perception that they are Covid-19 insurance. They can prosper even amid a pandemic, and have thus accumulated buyers on the perception that they have become defensive. Thus it was that on a great day for markets, the NYSE Fang+ index, which had been on the verge of a record, actually fell:  Relative to the average stock, as represented by the equal-weighted version of the S&P 500, the FANGs' underperformance was epic. They lagged the average stock by almost eight percentage points on the day. That was the most since the inception of the index, at about the point that the FANG acronym took hold, in 2015:  For another perspective, look at the EKG-style read-out of the relative performance of the Dow Industrials and the Nasdaq Composite. Both are flawed indexes, but both continue to frame much public perception of the markets. The Nasdaq is much more weighted toward technology, and includes all the FANGs. Monday saw the Dow's biggest outperformance of the Nasdaq since the bursting of the internet bubble in 2000. Other than that, the only times the Dow managed to beat the tech-heavy index by this much were on days when both were down, most dramatically during the Black Monday crash of 1987. If there is another example of a rotation this extreme on the back of good news, I cannot think of it:  In technical terms, the clearest expression of the violence of the turnaround comes from tracking the performance of stocks that have had the greatest positive momentum, relative to the market. Bloomberg's measure of the pure momentum factor in the U.S. stock market (the FTW function on the terminal), shows that momentum dropped 4% Monday. Since Bloomberg started tracking daily moves in 2008, it had never before fallen as much as 2%.  This could be alarming, give that many quantitative funds leverage up to bet on momentum. In recent months, a paired bet to go long momentum while shorting value stocks (chosen for their cheapness) has worked well. MSCI indexes show that this was a day when that strategy would have worked very badly:  So for many quant managers, this rotation will have felt a lot like the financial equivalent of stepping on a rake and having its handle hit you in the face. Sudden reversals like this have in the past caused serious market dislocations. We don't yet know if this has left any funds in trouble; this should grow clearer over the days ahead. Meanwhile, growth managers, who have done brilliantly for a while by betting on a factor perceived to be scarce, have also suffered a sharp reversal compared to value. All their outperformance of the last four months has been undone — although value still has the potential for a lot more strong performance if this rotation continues:  The same dynamic played out in other ways. Mega-caps, represented by the Russell Top 50 index, lagged the Russell 2000 index of smaller companies in the U.S. by almost 4 percentage points — the first time this has happened outside of major market crises:  Meanwhile, the rotation also played out in terms of industrial sectors. Bank stocks surged globally, while the previously bombed out energy sector enjoyed by far its best day ever, outside of two days when it rebounded during the historic crises of 2008 and March this year. This is the daily performance of the MSCI World Energy index since inception in 1995:  To be clear, a rotation this emphatic couldn't happen unless the market was unbalanced and too many chips had been put in the same place. It is a measure of extreme positioning that was already visible in the extraordinary performance of the FANGs. But the strength of the rotation also owes much to the fact that global markets were already shifting toward gradual reflation and economic growth. Plainly, if an effective vaccine can arrive sooner rather than later, it will be much easier for that scenario to happen. One of the most important yardsticks of economic optimism, the Treasury yield curve, was already beginning to trend upward. After Monday's action, it is its steepest in almost three years. This isn't consistent with a big bet on the safety of large and defensive stocks, but the vaccine news was needed as a catalyst for the rotation to come to stocks:  Another vintage measure of optimism about growth, the relative performance of industrial and precious metals, had also shown clear signs of perking up in recent months — a natural reaction to the signs of a strong revival in China, which dominates demand for copper and iron ore. The ratio is now above its 200-day moving average for the first time since early last year:  So this was an extraordinary rotation, and at first glance an overreaction to the news on the vaccine, which still leaves many questions unanswered. But the shift does make more sense when we grasp first that positioning was extreme, and second that there was already evidence it was time for stocks to move toward more of a reflationary position. And on to the VaccineNow for another question: Is the news from Pfizer really worthy of causing a big shift in the market? The answer is a guarded "yes"; the news improves the chances of economic growth compared to what had been expected. As Bloomberg Opinion's Max Nisen explains here, the key point is that the evidence for the vaccine's effectiveness is truly robust: Trials like Pfizer's compare the number of confirmed Covid cases among those who get the vaccine to those that take a placebo. The initial plan was to analyze the data after just 32 cases. But after discussions with the Food and Drug Administration, the companies decided to wait until there were 94. Their patience only modestly delayed results and makes it far easier to trust in the vaccine's considerable promise. Data collection will continue; the FDA requires at least two months of safety follow-up from most participants before considering an emergency use authorization. That data should be available later this month. Absent surprising side effects, quick authorization is more than likely. After all, the agency's bar for efficacy is just 50%.

Certainty isn't possible. It never is. But this statistical evidence is about as good as we could hope for at this point. We still need to know that it is safe, which requires waiting two months from injection to see if there are harmful side-effects (the next stop, coming soon, will be the release of results on safety). There are other important areas to explore, such as its impact in thwarting serious Covid-19 cases, and the effects on people in different age groups. It's also necessary to check whether subjects who avoided infection happened to be more responsible than the norm, wearing masks and avoiding crowds; although with larger tests this should be avoided. Then there is the issue of how long immunity can last. This may be a vaccine that we need each year, like flu shots. But the news is good. The fact that this vaccine has been shown so clearly to boost your immunity should also help in the critical next challenge of persuading people to take it. There are however, some key problems with the Pfizer/BioNTech SE vaccine candidate. In particular, it presents greater logistical challenges because it requires two shots rather than one; and it needs to be stored in extremely cold, freezing conditions. Of rival candidates, the one being developed by Oxford University and AstraZeneca Plc appears to be the most interesting, according to Jo Walton, managing director of the European pharma team at Credit Suisse Group AG. It doesn't need to be kept in a freezer, and would require only one shot. It should also be relatively easy to scale up, and is based on a different technology, so success would show that Covid can be countered in multiple ways. Successful trials for the Oxford vaccine would be great news, while a disappointment would be a major blow. The more candidates that prove successful, the more capacity there will be to produce them quickly, and the sooner the world can return to living more or less as normal. It is also important to recognize the limits. The vaccines haven't been made yet, and will take time to distribute. There is no way that the Pfizer/BioNTech candidate, or any other, will have vaccinated anyone in time to save them from the current outbreak. It won't be available during the northern hemisphere's winter, and so it will be necessary for people to continue to take evasive action that might well put a brake on economic growth. In what could be very bad for morale, this vaccine cannot arrive in time to save Thanksgiving, or even Christmas, for those who were hoping to travel long distances. Large tracts of the American population, and of others, are suspicious of vaccines. And take-up will need to be global to avoid a persistent reservoir of the virus that could stage a resurgence. The logistical challenges of vaccinating people in India or in sub-Saharan Africa are that much greater. All else equal, this brings forward the date when Covid-19 and the economic disruption can be put behind us. Any forecast should be shaded a little more optimistically now than it was 24 hours ago. But this isn't the end of the pandemic. The fact that this news caused such a market reaction reveals more about the market than about the vaccine. Survival TipsFirst of all, at the risk of stating the obvious, we all need to put up with wearing masks, particularly when indoors with groups of people, for many months more. It's time for more patience. Meanwhile, if you want a song to commemorate what happened in markets on Monday, try You Spin Me Around by Dead and Alive, or Twist and Shout by the Beatles. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment