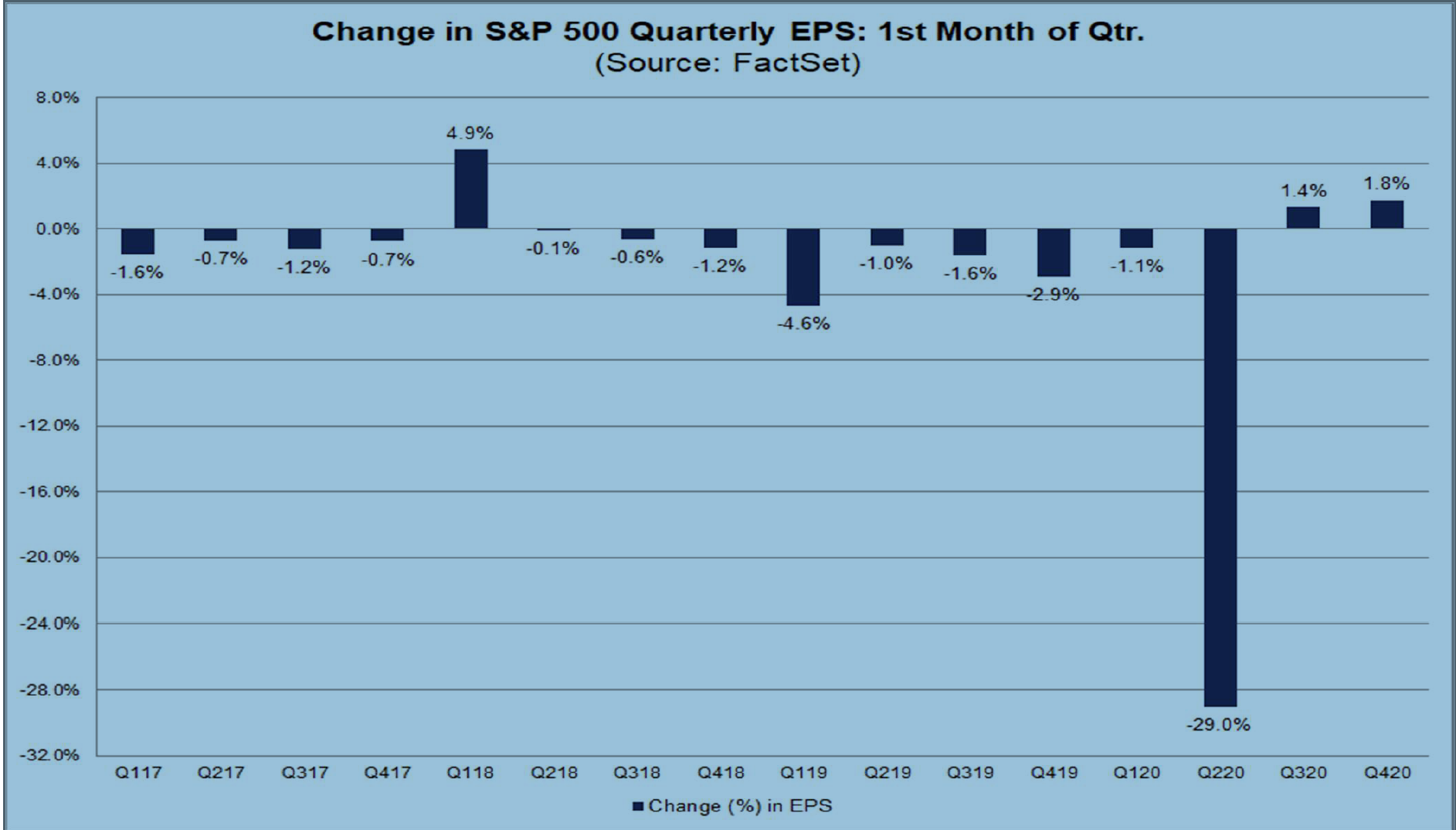

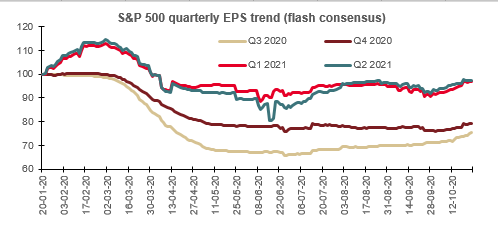

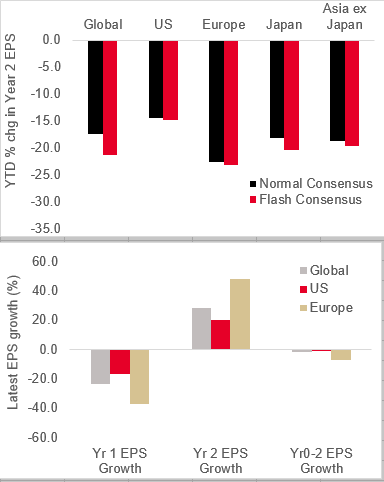

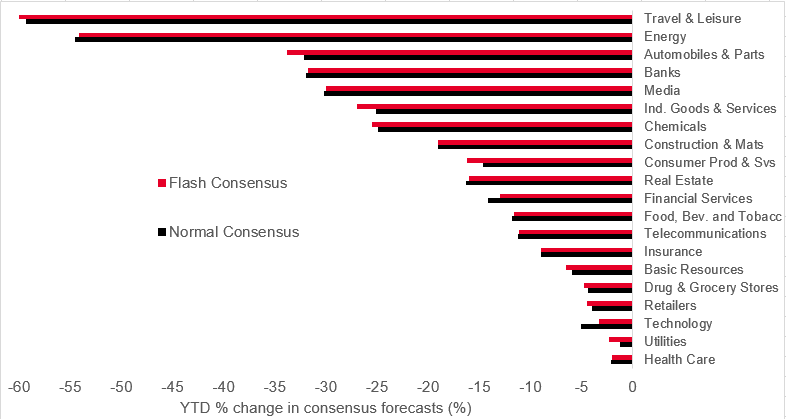

Strong LanguageThe third-quarter earnings season was one of the least exciting and impactful in recent corporate history, even though it broke records. Measured by companies' success in beating expectations that they have largely set for themselves, it tied for the best quarter since FactSet started tracking the metric in 2008. With 92% of S&P 500 companies having reported, a full 84% posted earnings per share that beat estimates. Congratulations to their investor relations departments. More impressively, companies spent October, the first month of the current quarter, gently talking expectations upward. This is very unusual. As the chart shows, this usually only happens when there is a major and discrete development, such as the corporate tax cut in the first quarter of 2018. Now it has happened two quarters in a row as Wall Street struggles to come to grips with the shock to activity administered by the pandemic. October was, according to FactSet's John Butters, the first time on record that expected earnings edged up in the first month of a quarter, yet the S&P 500 fell:  We all know the reasons. With such a dreadful economic mess, brokers didn't try too hard to model precise results, and companies didn't try too hard to guide them. The big earnings beat, the rise in forecasts, and the negative market reaction to them, can all be chalked up to October's twin preoccupations with the U.S. elections and the resurgent pandemic. It is distressing that this is all we can glean from earnings season. After all, investors in stocks are ultimately buying a share of corporate profits. Nothing should be more important, even amid pandemics and a U.S. election in which the loser refuses to leave. So let's try to wring something from it using first quantitative techniques (crunching the numbers) and then qualitative ones (reading what the executives have actually been saying). Andrew Lapthorne of Societe Generale SA keeps a regular spreadsheet of flash estimates — those most recently changed. These reveal that estimates for the first two quarters of next year for the S&P 500 are gently improving, which is better than the alternative — but there has been no great reassessment since midsummer:  Looked at geographically, estimates for next year are actually getting a little worse virtually everywhere, although this data won't yet incorporate any of the rising vaccine hopes. Base effects mean that next year will see great growth, particularly in Europe, though the change from 2019 to 2021 will be slightly negative. The halt to activity earlier this year will affect results for a while to come:  Lapthorne's data on next year's earnings for global stocks, split by sector, show little change in expectations in recent weeks. The overall shape is unsurprising, with travel and leisure still predicted to suffer a miserable 2021. Healthcare and utilities are viewed as being slightly more resilient even than technology; but at a global level, no sector has seen increased estimates since the beginning of this year:  There isn't a great amount of surplus optimism. When we try looking more qualitatively, however, things look a little brighter. Bankim Chadha and David Kostin, U.S. equity strategists at Deutsche Bank AG and Goldman Sachs Group Inc. respectively, perform the valuable public service of culling earnings calls for trends in what executives have been saying. In general, they are being more bullish than usual, or than they need to be. What follows are comments that caught my eye. The selection isn't scientific, but it's interesting. All are from on-the-record company earnings calls. First of all, Starbucks Inc., obviously grievously hurt by the initial lockdowns, had this to say: I could not be more pleased with our US sales recovery, which progress faster than we anticipated. In our final quarter of fiscal 2020 we finished the quarter with the comparable store sales decline of 4% for the month of September, a vast improvement from the approximately 65% decline we experienced at the depth of the pandemic only 5 months ago.

Logistics companies sounded bullish. This was from CSX Corp., a rail freight group: The consumer is still very, very strong. We expect a robust peak season around Thanksgiving time is usually when we see that e-commerce peak to Christmas time. We expect that to be very strong. Actually, it has been strong through the pandemic, just as people have been staying at and ordering stuff online, but we expect it to pick up even more robustly going forward as we approach Thanksgiving.

Meanwhile FedEx Corp., a huge logistics company, said: "The growth that we expected to see over a period of three to five years happened in a period of three to five months." If logistics companies can still be taken as economic bellwethers, and changing patterns in consumer demand do cloud this, they sound very positive. A number of consumer products groups trumpeted strong growth, and predicted that the shift toward eating more at home would "become a habit," in the words of McCormick & Co. This was from Clorox Co.: So up double digits behind strong consumer demand, and this is really about consumers staying home more and cooking more. So what we've heard is people are using more trash bags because they're generating more trash. So purchase frequency is up for Glad, in particular, and about 1/3 of households claimed to be using at least 1 full more — full bag of kitchen trash per week. And as people have told us, they continue to cook at home. In the future, we expect that to continue

There is also some quite old-fashioned bullishness about China. This is from Caterpillar Inc., another company often treated as a bellwether for manufacturing and international trade: In China, we expect our construction business to continue to be strong due to government spending on infrastructure and building activity. Based on what we see today, the strength in China should continue going into next year. We anticipate non-residential construction will remain subdued in North America in the fourth quarter as will machine sales for oil and gas-related activity.

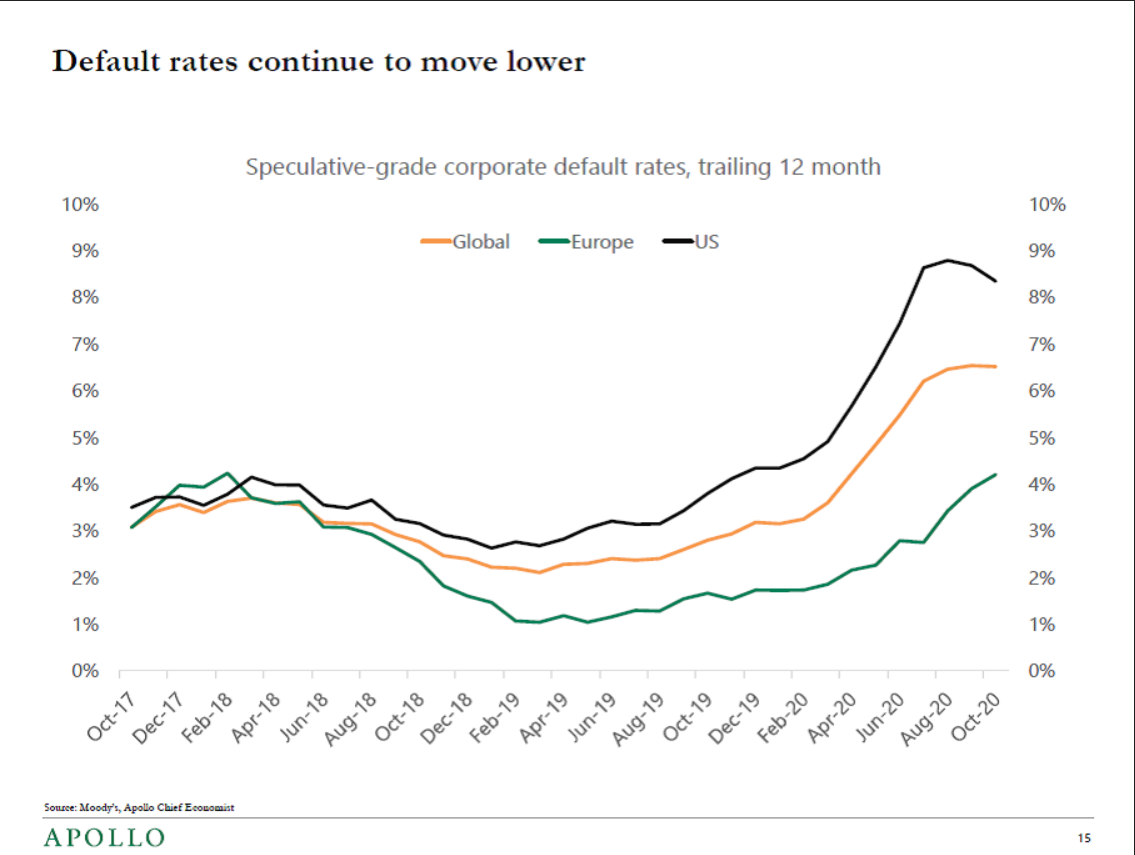

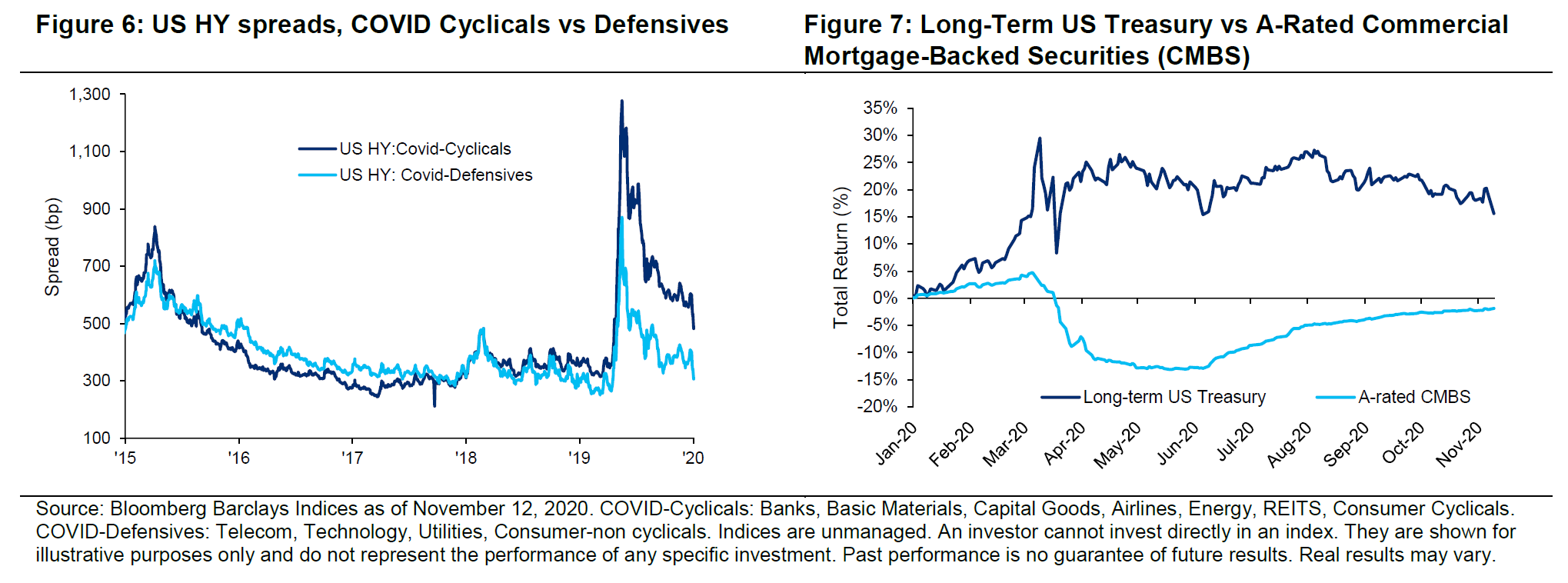

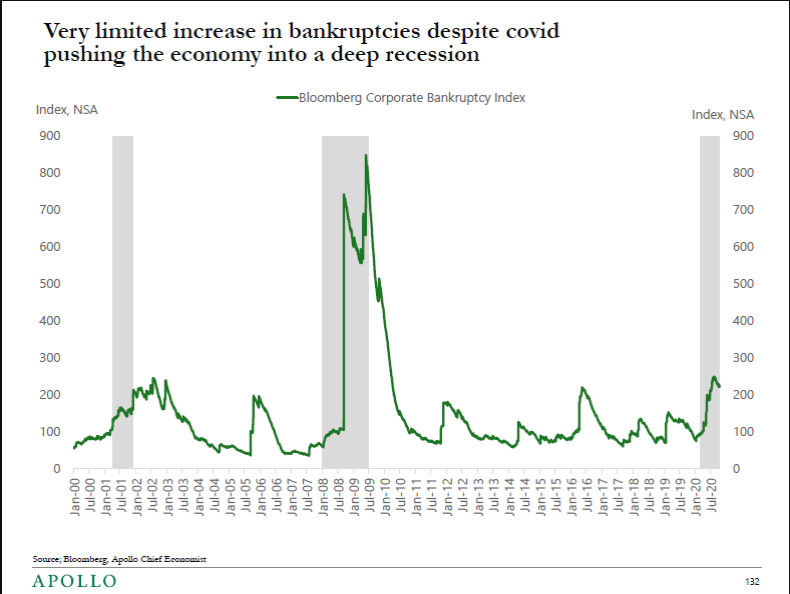

Consumer companies are also notably bullish on China. VF Corp., seller of branded clothing lines from The North Face to JanSport, said its growth was 19% for the quarter in mainland China, where its stores had been open throughout the period. To be clear, you would always expect executives to put the strongest spin that they can on their results. That's their job, and providing they don't lapse into untruths it's fine. But the strength of the language, when uncertainty remains so high, is meaningful. CFOs are naturally cautious types, who have dealt with a nightmare over the last eight months. They don't want to build up expectations that they cannot match. We should take their positivity at least somewhat positively. The underlying strength of earnings season helps to explain why the market has stayed as close to all-time highs as it has, despite lashings of political uncertainty and extreme valuations. The Solvency Crisis Still Hasn't HappenedArguably the greatest financial risk facing the world since lockdowns began in March has been a solvency crisis. A liquidity crisis was averted by the prompt provision of lots of money by central banks; but the fact remained that many companies weren't going to get the revenues they had reasonably been expecting. That led to the risk of a secondary solvency crisis as companies defaulted or went bankrupt, bringing down banks or financial institutions in their wake. So far, that hasn't happened. The following chart. from Torsten Slok of Apollo Management, shows the default rates on speculative-grade corporate bonds in Europe, the U.S. and globally. After rising alarmingly, U.S. default rates have declined slightly of late, while European defaults remain at a much lower level:  Another way to look at this is through credit spreads. Citi Private Bank divided high-yield bonds into "Covid cyclicals" (such as travel and leisure, which are worst affected) and "Covid defensives" (such as technology and consumer staples). Defensives, thus measured, are almost back to their tightest spreads, recorded before Covid struck, while even the cyclicals are now trading at lower spreads than they did five years ago, when worries about China were at a high. Even perceived risk for real estate, which suffers the considerable threat of unpaid rents, has returned almost to normal. The right-hand chart below shows how long-dated Treasuries have performed this year, compared to high-quality commercial mortgage-backed securities. Remarkably, the mortgage-backed bonds have erased almost all their losses for the year, again showing that concerns over a solvency crisis are much reduced:  The picture on bankruptcies is also much more positive than might have been expected. The Bloomberg Corporate Bankruptcy Index, which is based on both the number of bankruptcies of companies with at least $50 million in liabilities, and on the total amount of liabilities involved in the U.S, has also turned down slightly, and is nowhere the terrifying levels reached during the Global Financial Crisis:  If the pandemic's latest wave forces another serious interruption to economic activity before widespread vaccination can start, then a true insolvency crisis remains a risk. But it is reassuring that it has been averted until now, and that some of the markets closest to the problem are showing such relief. Survival TipsNothing matters more than the Covid-19 vaccine and when we will get it. If you're curious about who might receive Pfizer Inc.'s vaccine first if it's approved, then I invite you to join me today (Monday, Nov. 16) at 11:30 a.m. Eastern time in the U.S., for a livestreamed discussion on Twitter and Facebook with Bloomberg Opinion editor Sarah Green Carmichael. We will try to cover the full range of questions about vaccine ethics. Tune in here and comment with questions — we'll do our best to answer them in real time. For some reading in the meantime, try this, and this, and this. Most importantly, read this ambitious set of recommendations by a group of medics including some people who will be part of the Biden coronavirus task force. Getting the vaccine into our arms is going to be a huge logistical challenge. Many hard choices will need to be made. Can we all muster enough shared humanity to debate calmly how best this can be done? Given the experience of the pandemic so far, the prospects don't look good, but we will do our best to help find a way through the moral maze. Please join me and Sarah, and have a great week. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment