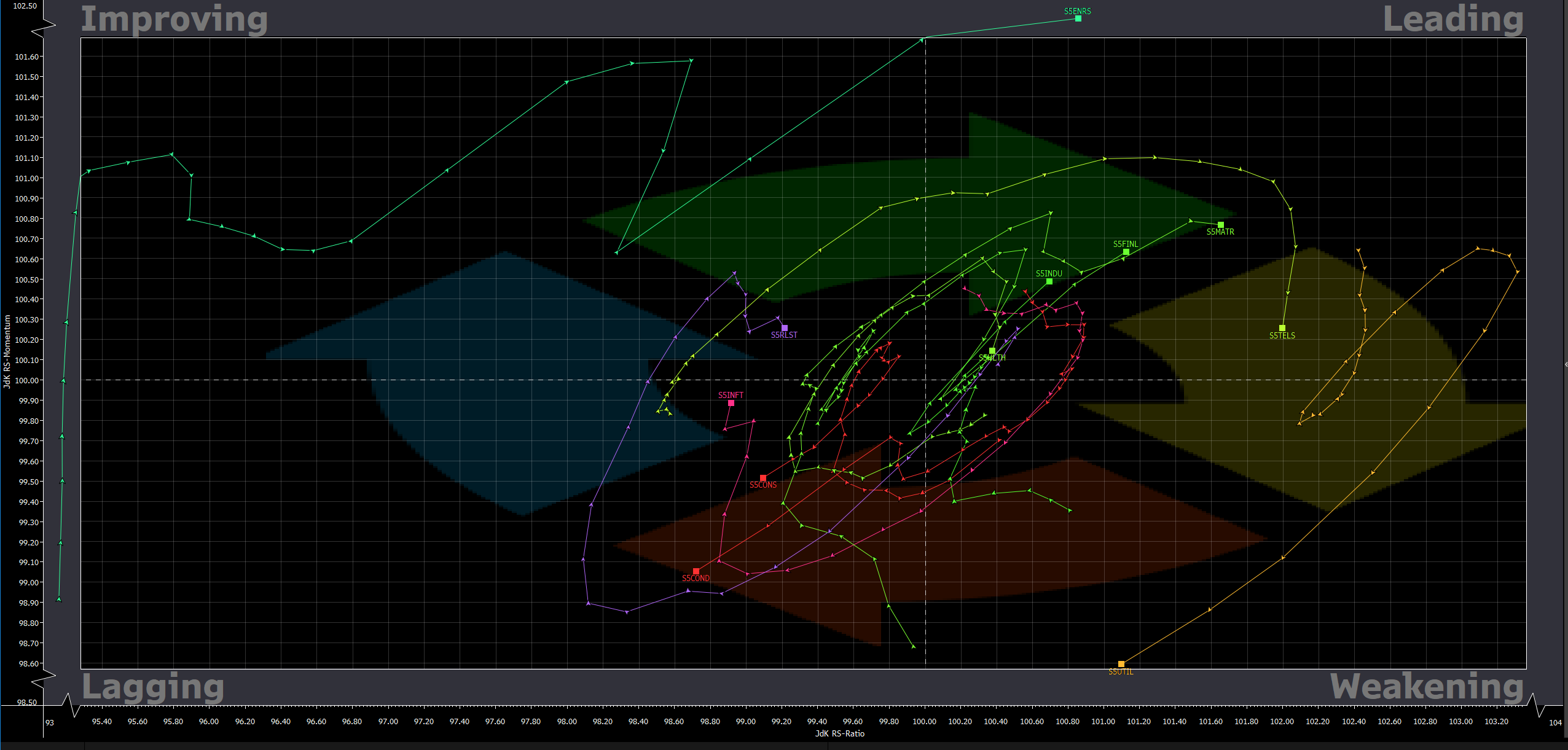

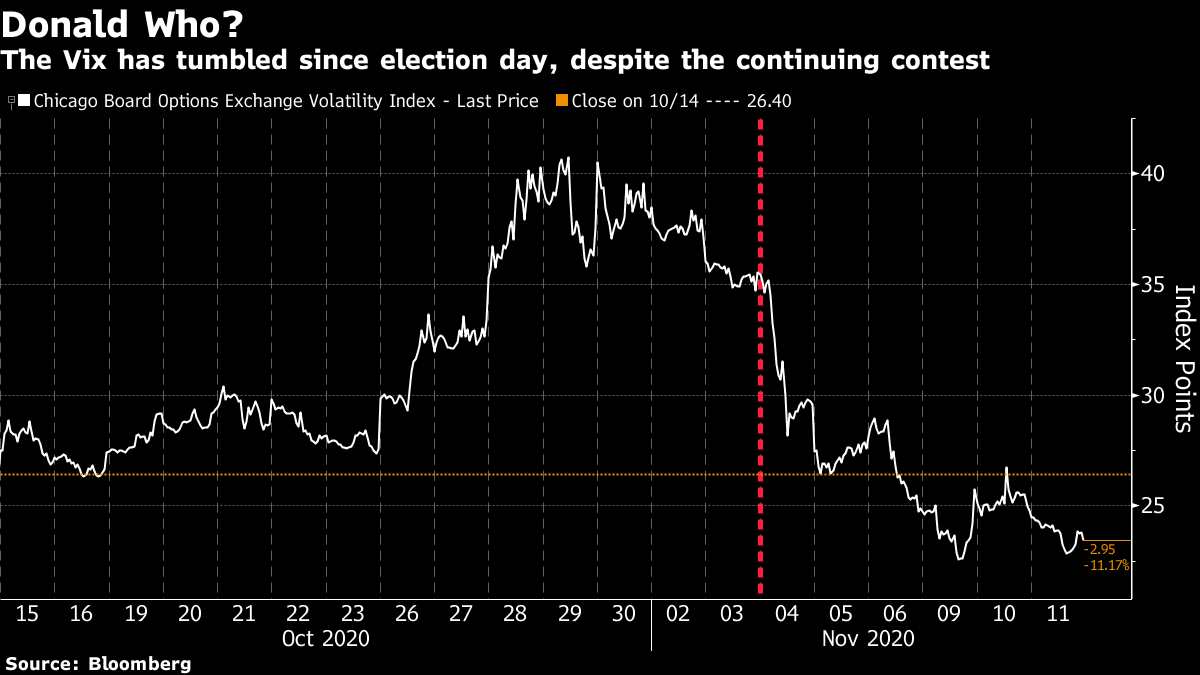

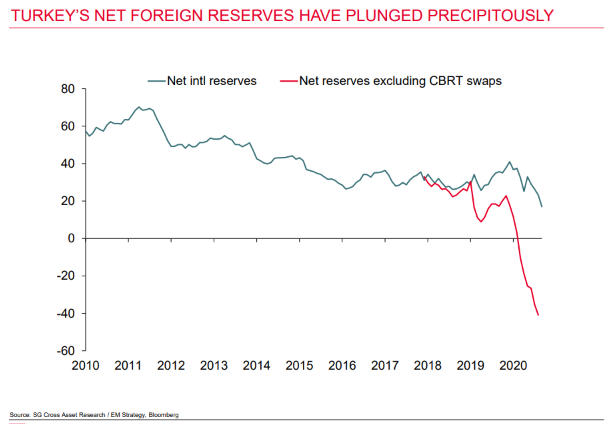

| To get John Authers' newsletter delivered directly to your inbox, sign up here. Balancing the BooksAnother positive landmark for world markets arrived Wednesday, one that seemed scarcely possible a few months ago. As of now, global stocks excluding the U.S. are in positive territory for 2020. The U.S. market has stalled with gains for the year at 10%, just below a peak set two months ago. Now the rest of the world is closing the gap, helped by the positive news on the Pfizer/BioNTech vaccine:  This is happening even as a third wave of the coronavirus hits the U.S., and a second wave hits western Europe. Neither is as deadly as the first, and neither has led to the almost complete cessation of economic activity seen this spring. But it is still remarkable to see these landmarks reached. At the beginning of this year, nobody had even heard of Covid-19. With the pandemic still raging, somehow investors are sufficiently assured about future prospects that they are prepared to take stocks higher than at that innocent time 10 months ago. How much further they can go is another issue. Technology stocks bounced back a little in Wednesday trading, but not enough to alter the picture that investors are steadily taking profits in the FANG internet platform companies and buying stocks in the rest of the U.S., and elsewhere in the world. The FANGs and their assured profitability are perceived to offer some Covid insurance, but investors no longer think it is worth paying so much for that protection. This is how the NYSE Fang+ index has performed this year relative to the equal-weighted S&P 500 index, representing the average large U.S. stock:  It is just faintly possible at this point to see the outline of a positive resolution to the financial crisis sparked by the pandemic. If (still a very big if) the latest news does lead to the successful vaccination of a large part of the world's population by about the middle of next year, then economies might begin to benefit from pent-up demand. Meanwhile, it is possible that markets can edge their way back from the extreme side-effects of the desperation measures that central banks took last spring. Maybe, just maybe, it will be possible to sell down the FANG stocks that people bought as insurance without causing an all-out burst bubble. That money can then flow into the many companies that are still languishing. The net result would be a stock market that goes sideways for a long time. And if anyone wants to complain about that, with equities up in a year that has seen the worst global pandemic in a century, they can shut up. There are plenty of things that could still go wrong. The vaccine needs to get to people, and the world economy needs to keep above stall speed during what could be a dark winter. The economy needs to revive in time to save the many businesses, particularly in real estate, that appear to be at risk of default. But at least some version of a positive outcome is becoming visible. The first stage, a massive rotation of stocks away from defensive sectors and toward those that would benefit from growth, is already under way. I've neglected over the last few days to mention that Bloomberg terminal users can track stock market rotations using the Relative Rotations Graph, or RRG, function. This graph of beauty shows what has happened to the main 11 industrial sectors within the S&P 500 over the last 30 trading days:  Another glimpse of returning normality comes from Jerome Powell, chairman of the Federal Reserve, who will be speaking at a European Central Bank conference on the future of central banking Thursday. It matters what he says. Bond yields in the U.S. remain very low, but they have risen enough of late to tighten financial conditions. Is he going to be comfortable with that? Markets don't appear wholly convinced that the Fed means what it says about letting the economy run hot until inflation exceeds 2% on average for a while. Does that mean that Powell will jawbone rates lower? The mere fact that such a question seems relevant, and that a central banker might be able to make things happen with mere words rather than desperation measures, is a sign of reassurance. Let's hope it is justified. PoliticsPresident Donald Trump has long set great store by the judgment of the stock market, and found validation in it. This week, it hasn't returned the compliment. Instead, it has done what the president seems to fear most, and ignored him. Approaching the election, mountains of investment research went into analysis of what would happen in the event of a contested election, in which Trump lost but refused to accept the result. There was general agreement that this was a nightmare scenario. The old cliche is true, that markets hate nothing like uncertainty. We appear to be in the presence of the nightmare scenario. The polls were wrong to predict a Biden landslide, his victory hinged on narrow margins in a series of states, and the president has refused to accept defeat. The great majority of elected Republicans are with him, and so are the many millions egging him on via social media. Trump has mobilized the Department of Justice to help and has also — ominously in the eyes of liberals — fired his Secretary of Defense. This is already having repercussions as the administration is refusing to release the funds that would allow Joe Biden to move on with planning his transition, as set out by law. His refusal to concede has been headline news across U.S media. The markets couldn't care less, though. Stocks are up since the election, and so are bond yields. Equity market volatility, as measured by the VIX index, has fallen almost without interruption since election day:  The only reasonable explanation is that the markets don't take Trump's effort to deny reality seriously. He has produced no evidence thus far, and needs to prove a conspiracy across several states, involving both Democratic and Republican officials, that led to tens of thousands of illegitimate votes being counted. So, as far the steely-eyed investors on Wall Street are concerned, he can be ignored. Trump should take heed of the markets. Meanwhile, investors might want to look at the effect his refusal to stand down is having on the emotions and opinions of Americans, some 70 million of whom voted for him. This may be a little too early to relax their guard. Turkish DelightAmid the drama over Trump's refusal to stand down, one of the world leaders on whom he appeared to model himself, President Recep Tayyip Erdogan of Turkey, appears to have exercised quite a retreat in the face of opposition from the global capital markets. It could be a turning point for the country, and may turn out to be an important battle won for the principle of central bank independence. As much of the world watched the U.S., Turkey announced the firing of its central bank governor Saturday, and then the finance minister proffered his resignation Sunday. The finance minister also happened to be Erdogan's son-in-law. These dramatic events, in a country where the president had persistently overruled the monetary authority, appeared briefly to prefigure chaos. Instead, they led to a remarkable recovery for the lira:  To fill in more of the back story, Erdogan dislikes raising interest rates to defend the currency, because he believes that higher rates lead to higher inflation. (Few economists agree with him.) The lira has been steadily depreciating for a decade. When it last came under intense pressure, in 2018, the central bank restored order by hiking rates above 20%. This time, as pressure mounted, it refused to do so:  The predictable result was a grievous run on foreign reserves, as illustrated in this chart from Societe Generale SA. Traders knew that Turkey was running out of money, and so the pressure on the lira became extreme entering the weekend:  This week, Erdogan has accepted his son-in-law's resignation. More importantly, he then delivered a speech Wednesday in which he said he supported "every" central bank policy that might be needed to achieve price stability, and that Turkey might have to take "bitter pills." Currency markets, as the chart implies, took this to mean that he is now prepared to let his new central bank governor hike interest rates. Tatha Ghose, foreign exchange strategist for Commerzbank AG, expressed the significance thusly: "We view this as the equivalent of Erdogan implementing his own IMF bailout for Turkey." That seems to be right. This is the point in a devaluation drama when an embattled president has to ask the IMF for help. Rather than that ultimate humiliation, Erdogan is opting for a slightly less embarrassing change of course. It remains unclear why it was necessary to replace the central bank governor to do this. But the principle seems to have been established that even the most autocratic of populist leaders cannot say no to the international markets, and has to allow his central bank some independence. Survival TipsI have written this on Nov. 11, Armistice Day in Britain and Veterans' Day in the U.S. From where I sit overlooking the Hudson River, I can watch a giant American flag hanging in the day's honor from the George Washington suspension bridge, under which all traffic must pass as it enters New York City. I'm lucky enough never to have fought in a war, and young enough to have avoided compulsory military service. But we all as humans share the same thoughts of the heroism, pain and loss of those who have fought. Nothing from popular culture sums up the futility and tragedy of war better than the final scene from Blackadder Goes Fourth, a sitcom set in the trenches of the First World War. It's regarded as one of the greatest moments of British television, and if you've never see it, you should. From higher culture, I think the greatest music to come out of the First World War was Benjamin Britten's War Requiem, which premiered at the opening of Coventry Cathedral after the ancient cathedral in its place had been destroyed in a German bombing raid during the Second World War. This is a film of Britten himself conducting it. This is a more modern version with better sound, conducted by John Eliot Gardiner. That requiem is a setting of the poetry of Wilfred Owen, the poet who was killed in battle less than 24 hours before the Armistice came on the eleventh hour of Nov. 11, 1918. One of them is the deeply moving Anthem for Doomed Youth: What passing bells for these who die as cattle?

Only the monstrous anger of the guns.

Only the stuttering rifles' rapid rattle

Can patter out their hasty orisons

No mockeries for them from prayers or bells,

Nor any voice of mourning save the choirs, --

The shrill, demented choirs of wailing shells;

And bugles calling for them from sad shires.

What candles may be held to speed them at all?

Not in the hands of boys, but in their eyes

Shall shine the holy glimmers of good-byes.

The pallor of girls' brows shall be their pall;

Their flowers the tenderness of silent minds,

And each slow dusk a drawing-down of blinds.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close.

|

Post a Comment