When Is a rotation a Rotation?One of the great things about Bloomberg is that we are free to speak our minds. Debate is encouraged. So I spent much of Tuesday in a lengthy Twitter debate with my colleague Kriti Gupta on the subject of whether what happened on global stock markets was a rotation. I argued yesterday that it was. Kriti argued Tuesday morning that it wasn't. Her opening salvos went as follows: Quick thing: a rotation must be sustained. Saying "investors are rotating into cyclicals"...they're not yet! They could be, but one day does not a rotation make. That phrase should be used in retrospect. While I'm at it -- June/September weren't rotations either despite it being called that at the time. Because if tech outperforms on virus risk in a few days again, you can't say we had a one or two-day rotation. That's not a rotation. That's trading!

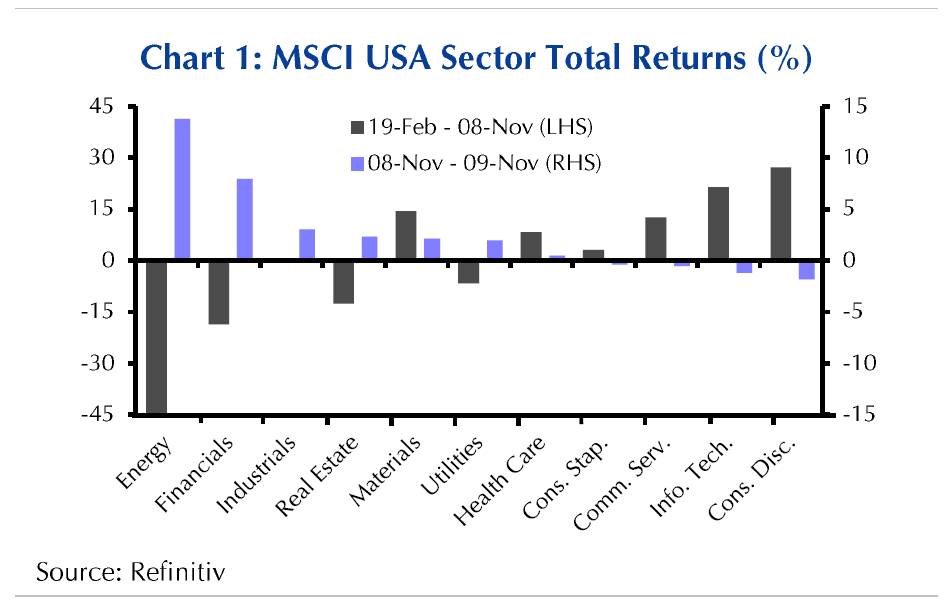

Most of our disagreement was definitional. I don't see another word to describe what happened in markets Monday. Here is Capital Economics' summary of how sectors performed before Monday, and on the day:

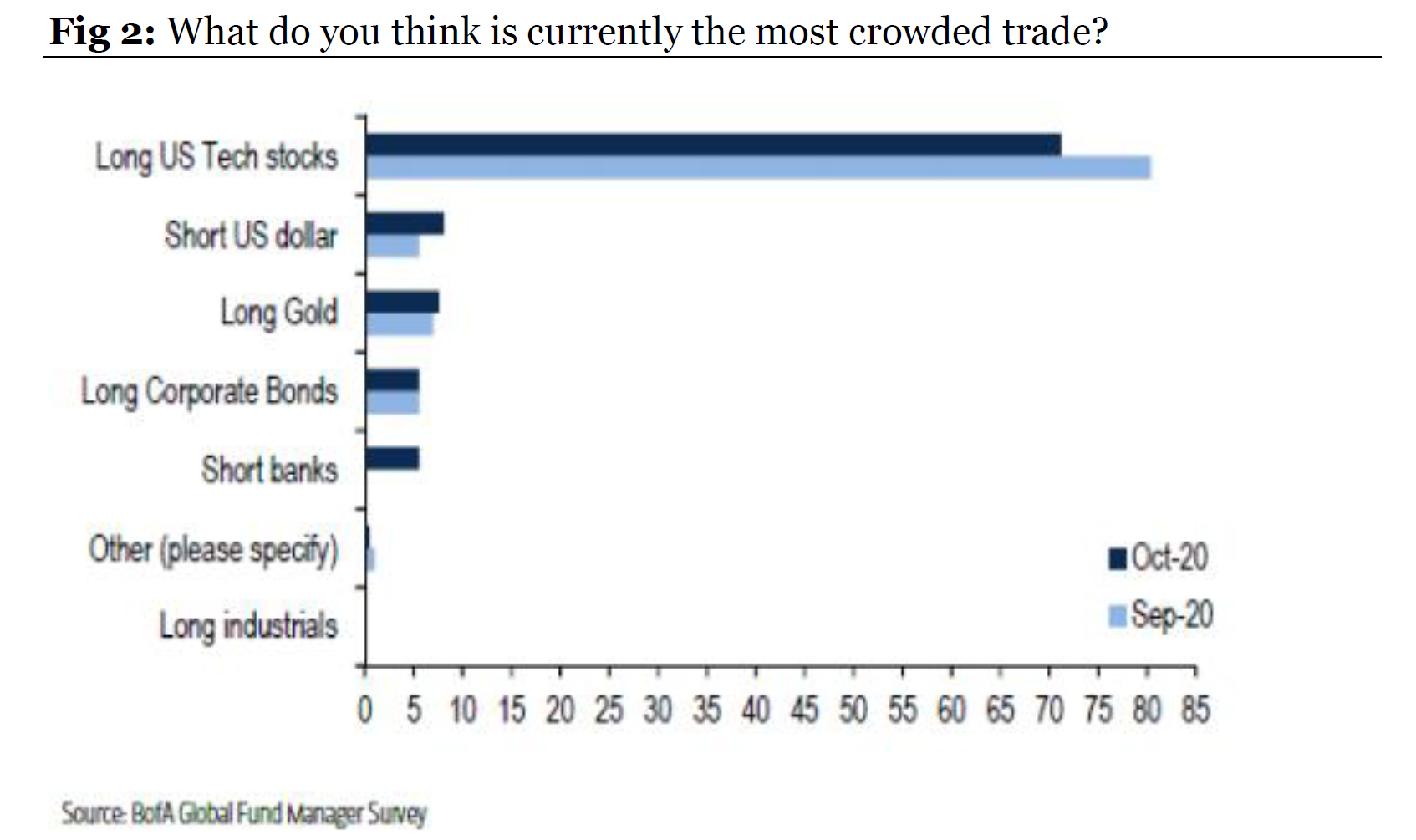

A day like this may indeed just be trading, but it's still the kind that causes a dramatic rotation. However, Kriti makes the valuable point that there is a difference between rotations that are soon reversed as news flows in (maybe you could call them reversals), and the big rotations, involving broader asset classes, that align with underlying changes in the macro environment. For example, people have been waiting for the Great Rotation (with capital letters) out of bonds and into stocks for at least as long as I have been covering markets. Kriti is unquestionably right that we don't yet know if Monday's extraordinary market convulsion is the beginning of a wider rotation. She's also right that we can only know for sure with hindsight. But it would still help to know if we are at the beginning of that process. So let's examine the issue. Fangs The extraordinary strength of the FANG internet platform stocks had much to do with the violence of Monday's moves. They already had one big, abortive sell-off in early September, and were widely recognized as a crowded trade. This chart is from Harry Colvin of Longview Economics in London, and shows the results of the latest survey of global fund managers by BofA Securities Inc.:  The FANGs certainly made up a huge part of the selling action in the first two days of this week. In an email, Jim Paulsen of Leuthold Group made the following points: The last couple days is not so much about a tech selloff as it is a FANG selloff....consider: - In the last two days the S&P 500 technology index is off by 2.65%. However, 52 of the 72 stocks comprising the index were UP over the last two days and only 10 stocks in the index fell more than the overall index.

- In addition, the Russell 2000 technology sector index is only off by -0.55% during the last two days.

- BUT, the NYSE Fang+ index is off by -5.61%!

- This isn't a tech rout, it's a FANG rout!

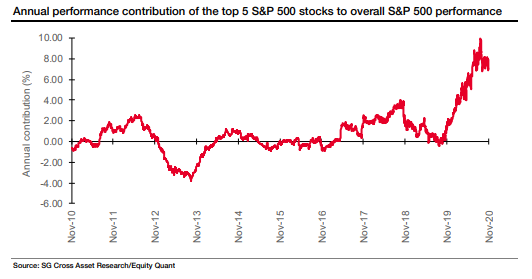

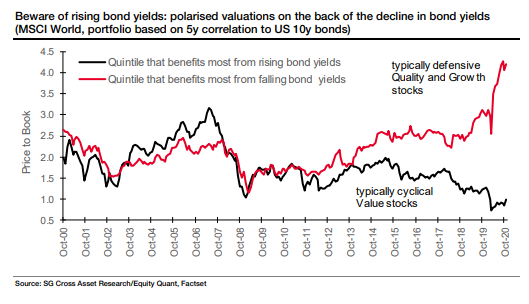

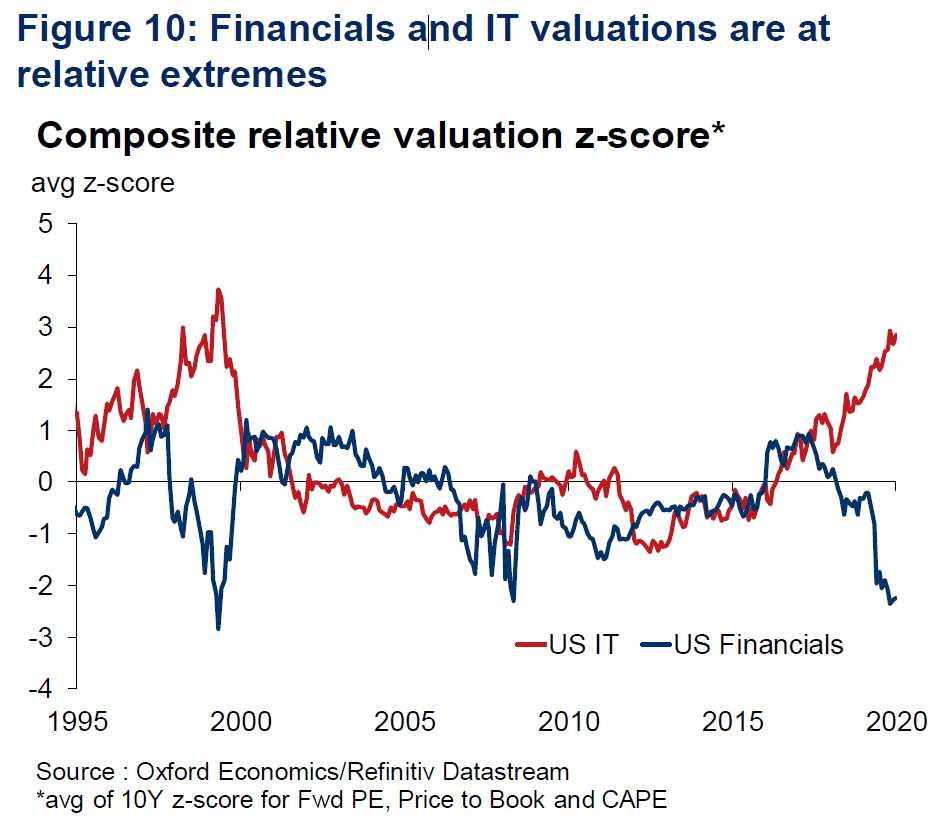

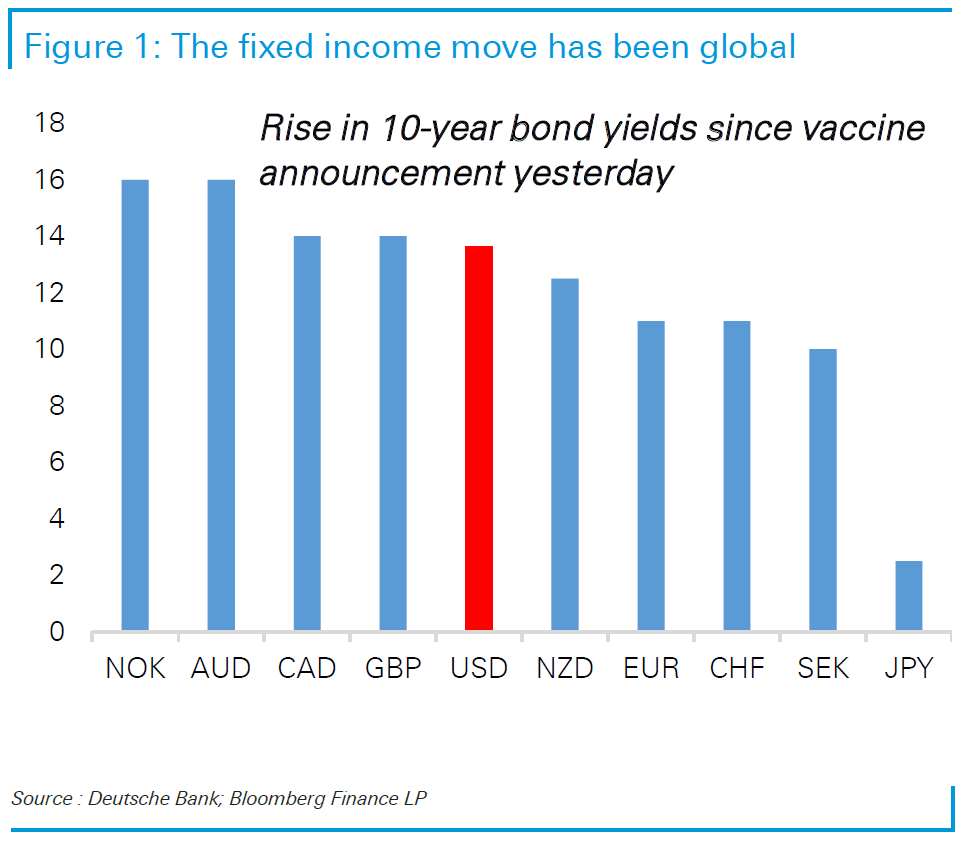

So you could indeed look at this as the liquidation of a massive bet on internet platform companies, and not necessarily as a broader asset reallocation. That doesn't mean that cutting the FANGs down to size won't have an effect. They have had such a huge impact on the performance of the S&P 500 in the last 12 months that any decline more or less guarantees the index will start to underperform the rest of the world. This chart from Andrew Lapthorne, head of quantitative strategy for Societe Generale SA, shows how much they have contributed to the S&P, and how much further they could fall:  Tech and bond yields That said, there is a clear link between the performance of technology stocks in general, and the performance of bonds. The FANGs are all "quality" stocks, with strong balance sheets, and also "growth" stocks, with well-protected profits. As such, they tend to benefit from falling bond yields. As this chart from Lapthorne shows, bonds have increasingly dominated the price-to-book multiples of such stocks as the post-crisis era of central bank dominance and QE has dragged on:  There is an overlap between bond sensitivity and industrial sectors. Banks prefer higher bond yields, and tech prefers them to be lower. Thus Oxford Economics shows that the U.S. tech and financial sectors are similarly at extremes of valuation, using a mix of several measures. The similarity between this chart and the previous one is in no way coincidental:  If there is a significant shift in bond yields, and that persists, we can expect this rotation to continue. To ram that home, George Saravelos of Deutsche Bank AG produced this chart showing that the trend of higher bond yields in the wake of the vaccine announcement was truly global. Treasury yields are in the middle of the pack:  So there is a little more to this than a sudden exit from the overcrowded FANGs trade. There is also a risk that that overcrowded trade could yet inflict more problems on us, if bond yields continue to rise. Chris Watling of Longview Economics invoked the magnum opus on financial bubbles, the late Charles Kindleberger's Manias, Panics and Crashes: as Kindleberger demonstrated in his analysis of bubbles, the one key factor which bursts bubbles is the beginning of the removal of cheap money. In early 2000, that occurred when Greenspan started to withdraw the extra repo liquidity put in because of Y2K concerns. Yesterday's vaccine announcement and the back-up in bond yields, could be today's equivalent.

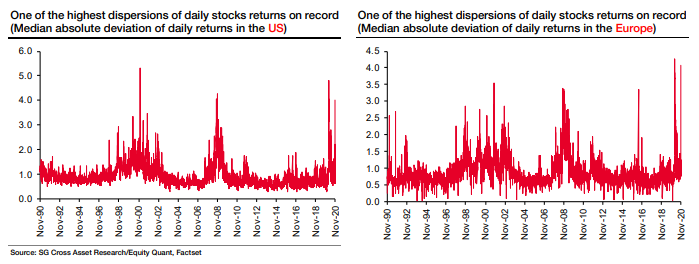

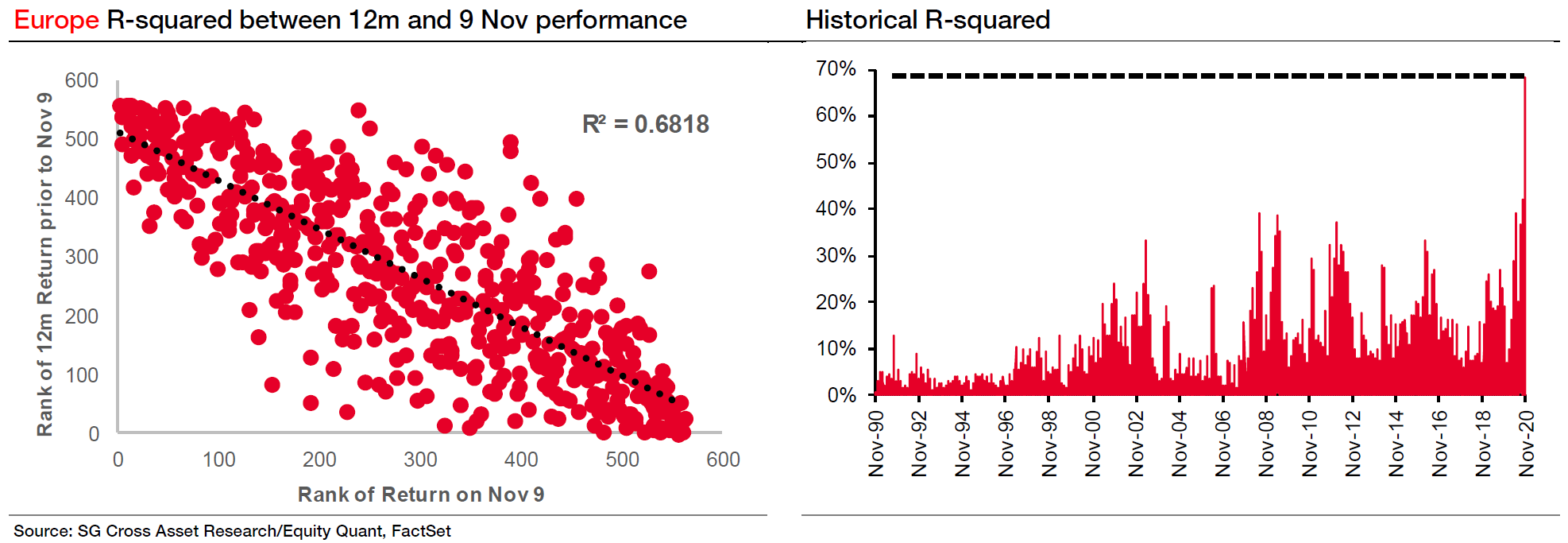

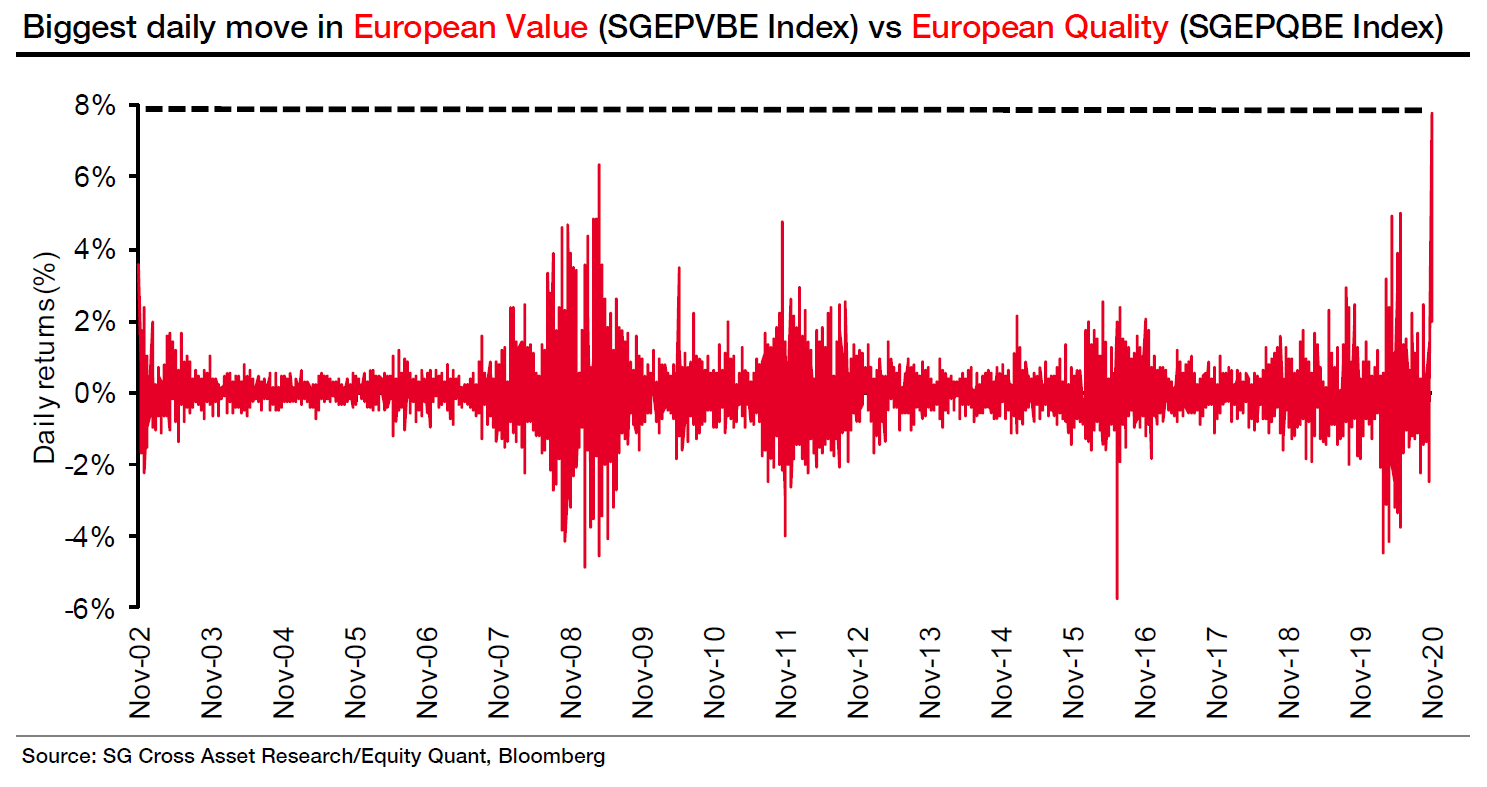

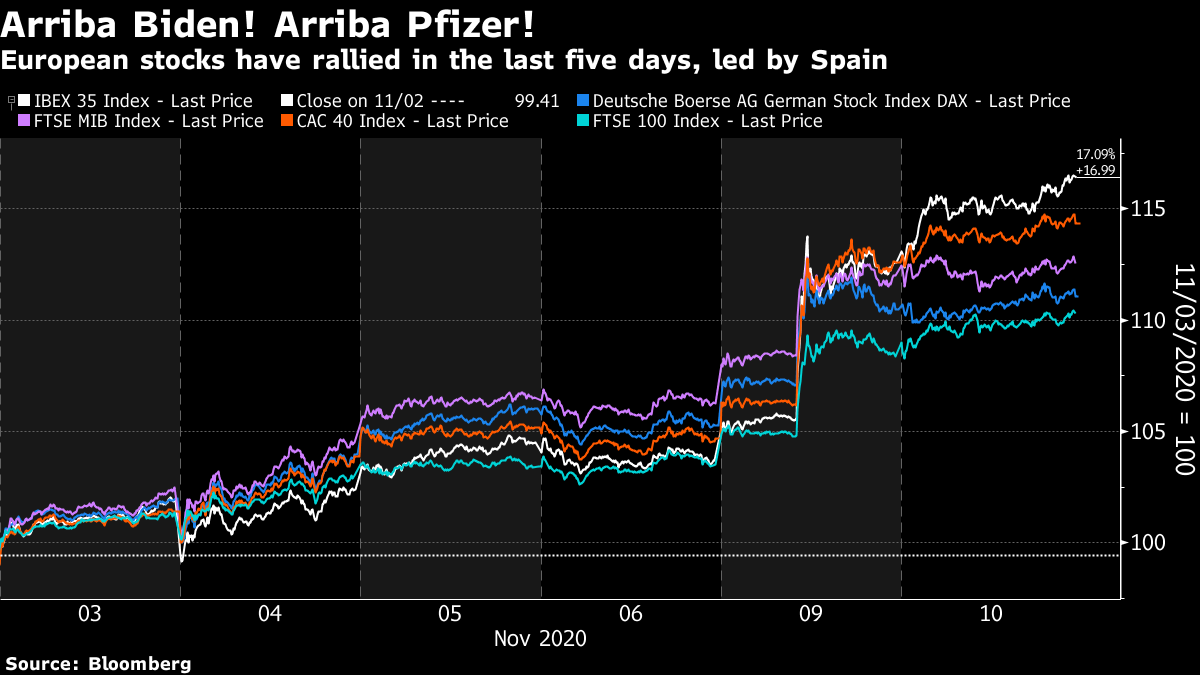

Europe This vaccine is in many ways a European product: It was aided with an injection of German government funds, and BioNTech SE was founded by two Turkish migrants to Germany. And it has had an even bigger impact in Europe than in the U.S. This, incidentally, argues that we shouldn't dismiss what is going on as merely an exit from FANGs. In the following charts, Lapthorne of SocGen looks at the total dispersion of daily returns in the U.S. on the left and Europe on the right, over the last three decades. In the U.S., Vaccine Monday still ranks behind the historic dislocations of the dotcom bubble and Lehman — and the onset of the Covid-19 shock in March. In Europe, Vaccine Monday saw greater dispersion than anything bar the worst day in March:  This happened even though European yields famously have a lot of room to rise. This is the German yield curve; it is as flat as a pancake, and has been with minor interruptions since the middle of last year — but it is currently at the steepest end of its recent range. If the European bond market were to start placing bets on a full-blooded move into reflation, then we would have a true Rotation on our hands:  For another example, of how big a deal Vaccine Monday was for the European stock market, this next chart from Lapthorne shows the degree of negative correlation between prior 12-month returns, and returns on Vaccine Monday. The worse a stock had done over the previous year, the better it did, to a far greater extent than had ever been seen before. The chart on the right shows the strength of the correlation, and shows that on this measure, this was the most powerful rotation in three decades, roughly twice as powerful a turnaround as anything that had preceded it:  Lapthorne also shows that European value stocks outperformed quality stocks to the greatest extent in a single day since measurement began in 2002:  In all cases, there were similar effects in the U.S., but the moves in Europe were far more powerful. Most importantly, the overall effect on Europe's (FANG-less) stock markets was far more positive than on the U.S. European markets already picked up in the last three days of last week following the U.S. election. Then the vaccine announcement sent them heavenward. Returns were roughly proportional to the extent of their current travails with Covid-19. In Spain, seriously stricken by the latest wave of the pandemic, the IBEX index has rallied 17% in five days, closely followed by France's CAC-30. France also has serious problems with the pandemic:  So we can gather so far the following: - There is a specific issue relating to the FANGs, which present the risk of a classic burst bubble;

- Rising bond yields are helping to drive the rotation so far, and could drive it further;

- The degree to which a country is being hit by the pandemic affects how much their markets have reacted.

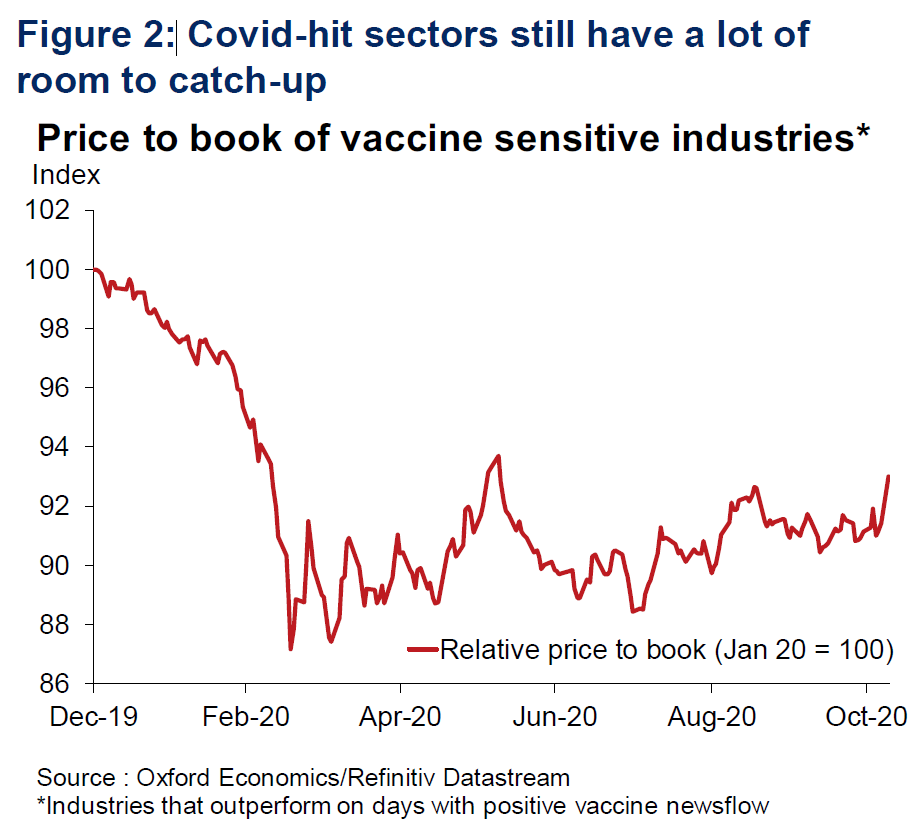

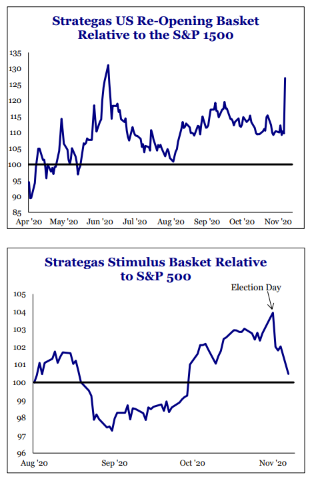

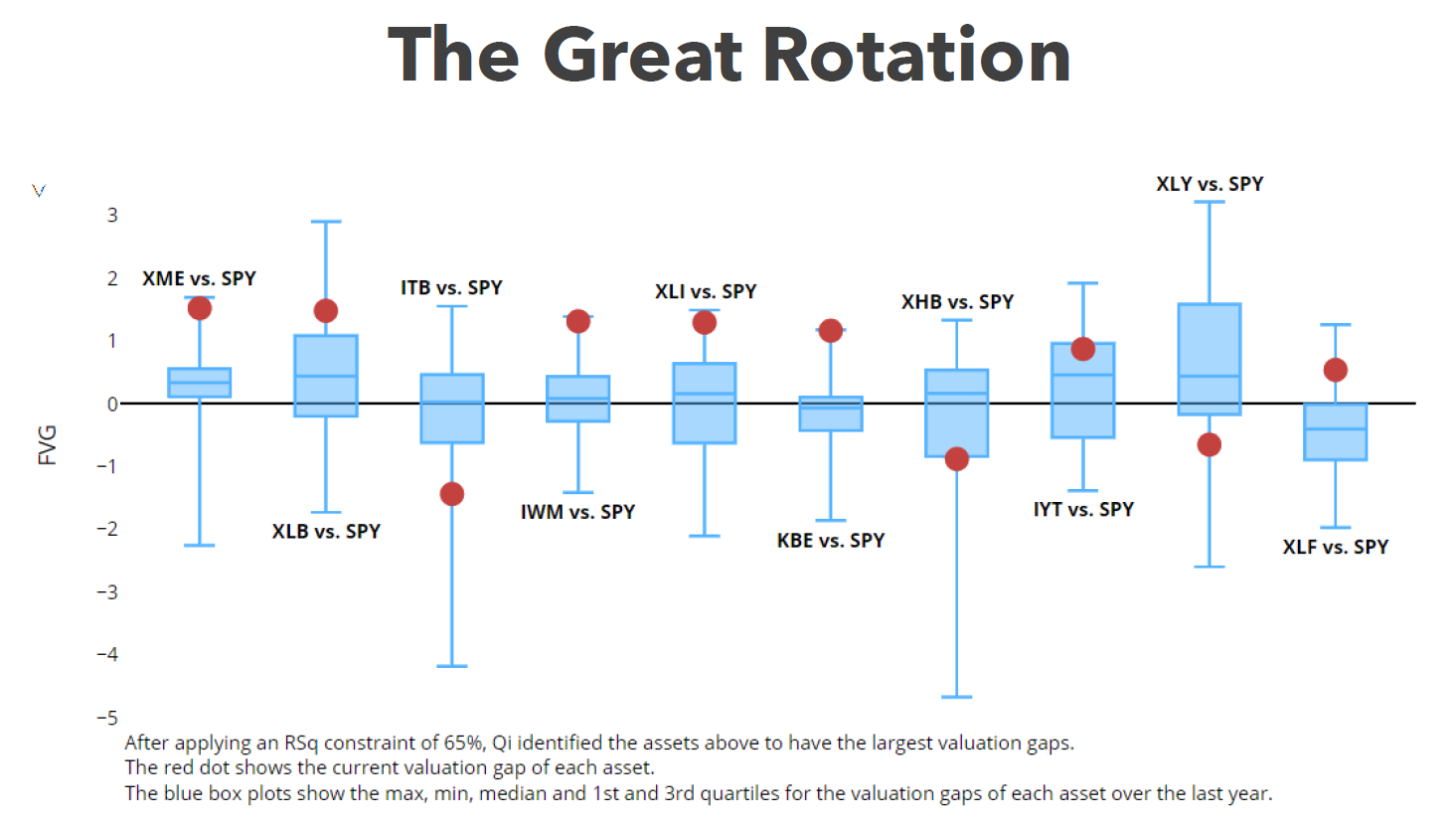

That leads to the critical question with which we started: Is this a rotation or a Rotation? There is ample room for the stock market to adjust much further. Value has lagged growth for a very long time. Or, alternatively, if we look at Oxford Economics' valuation measure for the most Covid-sensitive industries, they could climb very significantly if this plague can be defeated quicker than we had expected:  (For a beautiful visualization of the U.S. stock market and its sensitivity to Covid, try this heat map, produced by a Cambridge University undergraduate.) A similar exercise by Strategas created a basket of stocks that would benefit from reopening the economy. Unsurprisingly, they did fantastically on Monday (AMC Entertainment, which runs the largest U.S. chain of cinemas, gained 51%), and have lots more room to grow. But Strategas Research Partners also offers the counterpoint of its basket of stocks that would benefit from a fiscal stimulus in the U.S. With a vaccine now looking closer than had been thought, the political urgency for a stimulus declines. Those stocks have been pummeled since election day:  There is room for the rotation to go much further, then, but this requires navigating many macro cross-currents. Banishing Covid-19 would probably mean less fiscal stimulus, and less upward pressure on bond yields. The U.S. election also makes stimulus look less likely politically in any case. If the Federal Reserve is as determined to let inflation run "hot" as it currently appears, that might help the longer-term chance of a rotation. In the short term, though, it will make the prospects for a true rotation rather dim, as yields wills stay low and the yield curve flat. And if we look at macro factors, they suggest that the rotation has gone about as far as it can. The following chart from Quant Insight shows the valuation gaps compared to fair value for 10 sectoral ETFs compared to the S&P 500. The scale is in standard deviations. Remarkably, it shows that the ETFs for metals and mining (XME), industrials (XLI), banks (KBE) and small-caps (IWM) are all at their most expensive compared to fair value in the last 12 months.  How should we interpret this? All of these classic cyclical sectors that have had a miserable time during the pandemic are now fully pricing in current reflation expectations. For them to move further, the macro environment will need to shift further in a reflationary direction. Specifically, the model would need to see tighter credit spreads, lower risk aversion and higher inflation expectations. These things could easily happen, if effective vaccines are swiftly distributed, the pandemic looses its hold on the world economy, and pent-up demand is released. Yes, that could happen. But until we know whether it has, we won't know for sure that this is a true Rotation. Which is what Kriti said. With a lower-case "r," Vaccine Monday remains arguably the greatest single-day stock market rotation ever seen, which is what I said. I hope that helped. Survival TipsDon't be shy to ask colleagues tough questions. Follow @KritiGuptaNews. And as we will still have to wait months before Pfizer's or any other vaccine is ready, keep wearing a mask and avoiding indoor crowds. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment