A Second DoseThis is the Moderna World. For the second Monday in a row, we awoke to great news about the search for a Covid-19 vaccine. The latest announcement, from pharmaceutical group Moderna Inc., was if anything even more encouraging than last week's from Pfizer Inc. and BioNTech SE. Not only does the Moderna vaccine appear to be slightly more efficacious in preventing Covid infections (with a 94.5% success rate, compared to 90% for Pfizer's) but, crucially, it is much easier to store and transport. The Pfizer vaccine needs sub-Antarctic temperatures. As the Moderna vaccine uses similar technology, the expectation was that it would present similar challenges. But Moderna was able to make the following claims: Vaccine candidate now expected to remain stable at standard refrigerator temperatures of 2° to 8°C (36° to 46°F) for 30 days, up from previous estimate of 7 days Shipping and long-term storage conditions at standard freezer temperatures of -20°C (-4°F) for 6 months mRNA-1273 to be distributed using widely available vaccine delivery and storage infrastructure

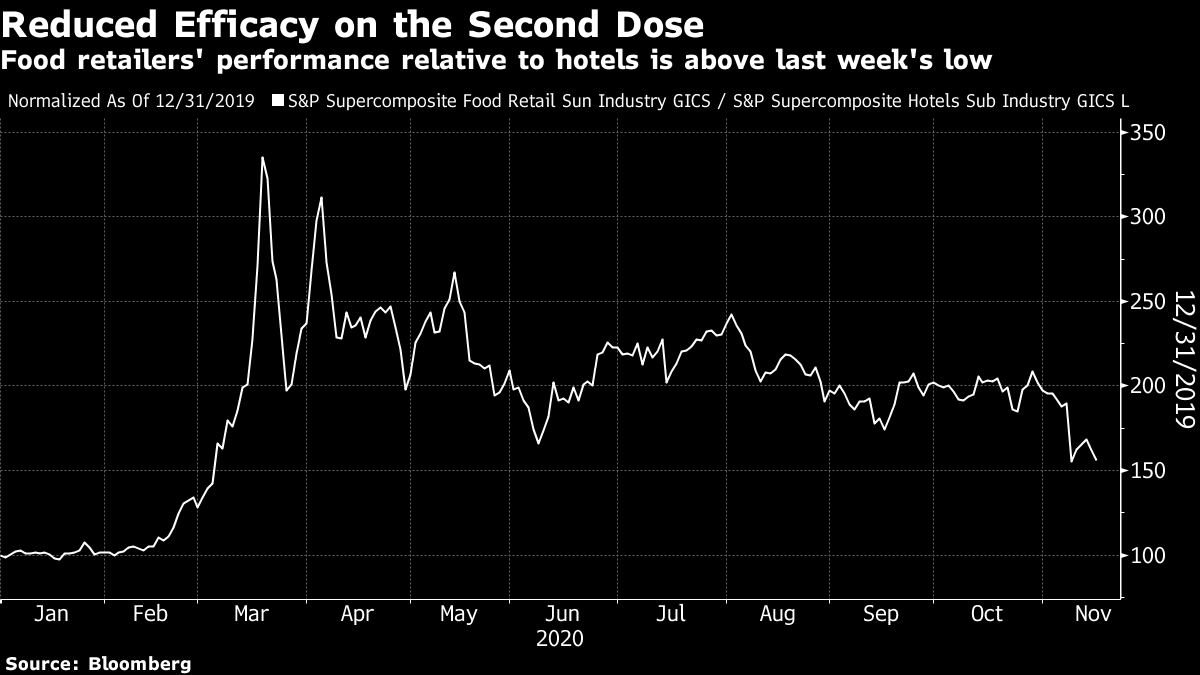

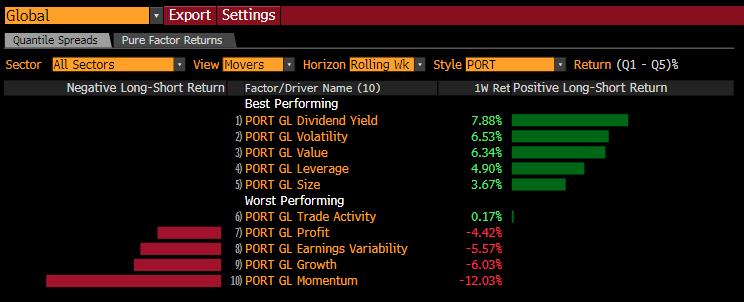

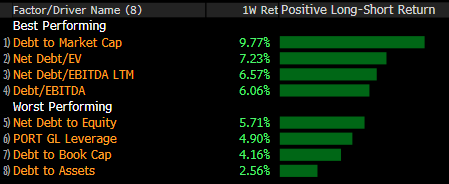

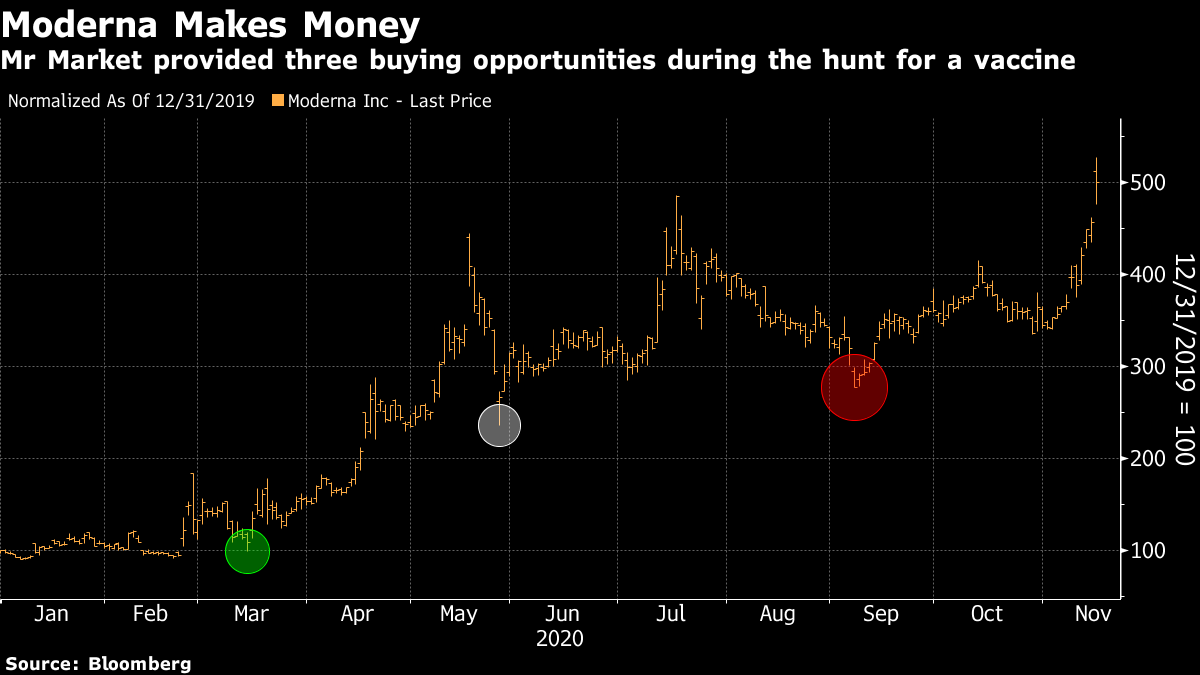

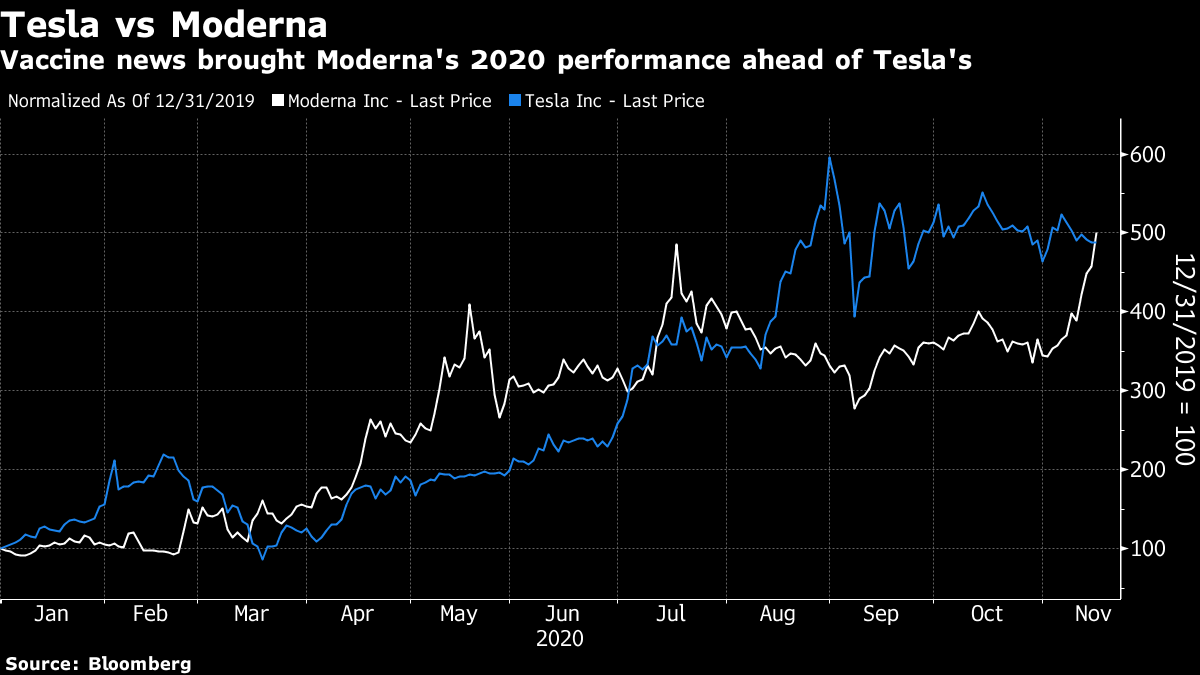

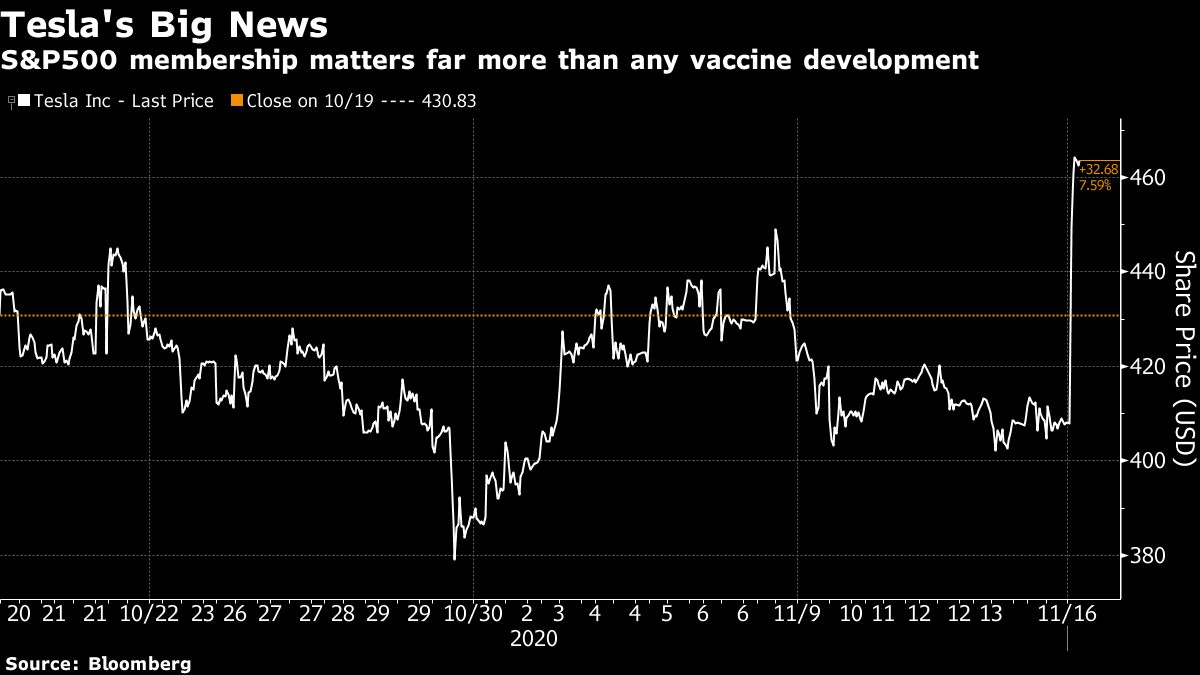

This newsletter is written exclusively by and for humans. For all of us, this is fantastic news. The scientific community has found a vaccine that protects far more successfully against Covid-19 than anyone had expected, and now it appears they have found a way to get it to us reasonably quickly. We should be able to stop living like this before too much longer. Moderna Monday should, then, by all rights be just as big a deal as Pfizer Monday. But it wasn't for markets. The reaction suggests that optimism was a little ahead of itself. Meanwhile, a subtler rotation among stocks continues as we all struggle to adapt to the impending arrival of a new reality. This is my favored "Covid Fear" index, which shows the S&P 1500 food retailers relative to hotels, resorts and cruise lines. It is still up a bit more than 50% for the year, and it closed this Monday slightly higher than a week ago. Moderna brought material good news, but this doesn't show up in the stocks most sensitive to when normal life can resume:  As for the FANG internet platform companies, which have been bought all year long for their perceived defensive properties, they continue to underperform the average stock in the S&P 500. Again, for no obvious reason, the news from Moderna has done no more than reconfirm the news from Pfizer, in the eyes of the market. There is nothing to suggest that this was significant news.  Meanwhile, bond markets were downright quiet. In the U.S., where 10-year yields had looked set to break 1% last Monday, trading was much tamer. German bund yields had a much smaller leap than a week ago and ended almost unchanged for the day, still negative. This is how bund yields have moved this month. Pfizer registers as the only conclusive event; the Moderna news, and the confused U.S. election are barely visible:  Within stock markets, however, the tectonic plates have been shifting. This is the Bloomberg Factors to Watch (FTW) function for the year to date. In all cases, this involves looking at the top quintile of stocks globally as measured by a factor, compared to the bottom quintile:  For the year as a whole, it has been a story of piling into anything that can show reliable sales and momentum, while avoiding value stocks, or anything highly levered. This is how the main factors have performed for the last five days (starting immediately after the first Vaccine Monday):  Cheap stocks are suddenly much more popular, as are companies that are heavily indebted. There is growing confidence, justified or otherwise, that a major solvency crisis can be avoided. This is the breakdown of how the main measures of leverage have performed over the last five days, for global stocks:  Meanwhile, if we look at the pure factor return to leverage in the U.S. for the year so far, relative to the pure factor return for growth, we again see something that looks very much like the beginning of a significant rotation:  For obvious reasons, leveraged stocks have been very unpopular compared to growth stocks in 2020. Now, they are the closest they have been to breaking this trend since the pandemic began. A disciplined rotation within the stock market continues. Beyond that, even though both the S&P 500 and all-world indexes hit all-time highs, the market today seemed strangely underwhelmed. Moderna MondayThere are some more lessons to be gleaned about Moderna. Genuine innovation will be rewarded by Mr. Market. And Mr. Market will also offer new opportunities to profit from it. Moderna's stock has gained more than 400% so far this year. It faces controversies ahead; it has to mass-produce and distribute its vaccine next, and to defend a price point that is higher than its competitors (for a commentary on how difficult that could be, watch this livestream, with me and Bloomberg Opinion colleague Sarah Green Carmichael). But this is still an example of capitalism working as intended; showering rewards on those who make an innovation that will help mankind, along with those who had the courage to back them. What is interesting looking at Moderna's chart for the year is that it suffered three sharp pullbacks that created great new entry points, even though it was possibly the most closely watched company of its size on the planet. The most impressive was in May, after its equity issue, but the market also offered opportunities in March and September. For those who really knew enough about vaccine technology to handicap the runners, it should have been possible to see that Monday's news wasn't in the price, and to profit. Kudos to those that did — and let's hope that Moderna handles the challenges of the next few months on which those gains depend.  If Moderna is an example of capitalism working as intended, though, what should we make of Tesla Inc.? The electronic vehicle manufacturer founded by Elon Musk is one of the sexiest companies in the world, and it manages to keep itself in the news. But nothing material has happened to change the Tesla story this year in the way that Moderna's prospects have been transformed. Despite this, Tesla had outperformed Moderna for the year until Monday's price action:  But wait, there's more. After the market closed, S&P Dow Jones Indexes announced that Tesla will be joining its flagship S&P 500 index next month. It will be by far the biggest company ever admitted, in terms of market cap. Tesla's difficulties turning a consistent profit had kept it out until earlier this year, while the members of the S&P 500 selection committee used their discretion to exclude it for a little longer. Including Tesla in a market index will have no effect whatever on its revenue, sales, profitability, or anything else that will determine the present discounted value of its future cash flows. This didn't stop its share price from rising more than 13% in after-hours trading:  There are times when it is necessary to step back and ask if something makes sense. This is one of those times. Index investing is a great product that has made it far cheaper for people to invest in the stock market and for institutions to switch between asset classes. But it has had negative effects. If the after-hours bounce translates into Tuesday's opening, Tesla's market cap will rise by some $50 billion. For perspective, the entirety of Kimberly-Clark Corp. is currently deemed to be worth $47 billion. Moderna's market cap, after all the excitement, is $38.7 billion. So the selection committee of the S&P 500 have managed to create more market value by adding Tesla to an index than the team of scientists at Moderna did by inventing a successful vaccine against a global pandemic. It makes sense for people to buy Tesla now, because they know that index funds and exchange-traded funds will be obliged to buy it in due course; the index-selection process effectively allows them to front-run those purchases. But it shouldn't make sense. Moderna may or may not prove well priced at $38.7 billion, but its story in 2020 is an example of capitalism working as intended. Tesla may or may not prove well priced at almost exactly 10 times that much (its market cap at the close Monday was $386.8 billion, before the after-hours trading), but its story in 2020 is an example of capitalism going badly awry. Survival TipsMy latest survival tip is not for anything undiscovered. The fourth season of The Crown has started streaming on Netflix, and it's great. The current season is particularly good for me, and other British people of my generation, because it starts with the election of Margaret Thatcher in 1979, a hugely significant moment in U.K. history. This was followed two years later by a hugely significant moment in the history of the royal family, Prince Charles's ill-fated wedding to the then Lady Diana Spencer. It's glorious to wallow in the nostalgia, and also to remember that it really did feel as though the country was imploding back then — much as it does now, in the U.K., the U.S., and elsewhere. The number one song at the time of the wedding was Ghost Town by The Specials, a bitter social commentary on the riots that were spreading across Britain at the time. To understand the kind of anger with which Thatcher was greeted, for my money there is nothing quite like the Specials' version of Maggie's Farm. And meanwhile the struggle in Northern Ireland – which saw the assassination by the IRA of Lord Louis Mountbatten in 1979, an event movingly portrayed in The Crown – led to doses of unadulterated but brilliant anger like Alternative Ulster by Stiff Little Fingers. Thatcher herself wasn't interested in maintaining a Britain of the kind represented by the royal family – as The Crown makes hilariously obvious. Maggie — we were all on first name terms with her — wanted something very different, and she ultimately got her way. The country would go on to enjoy three decades of prosperity and growing self-confidence, accompanied by ever growing inequality, before again reaching a point where it seems as though it is falling apart. Looking back, it seems absurd that at the time we all took heart from the royal wedding, and from one of the greatest cricket Test matches ever played, which hogged the headlines in the week before. Fellow Brits of a certain age, enjoy the clips of Ian Botham and Bob Willis (may he rest in peace) at Headingley in 1981, and of the entire remarkable story of Botham's Ashes; and for everyone else, watch The Crown's depiction of a hopelessly divided country in seemingly terminal decline, and remember that somehow or other it is possible to turn these things around. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment