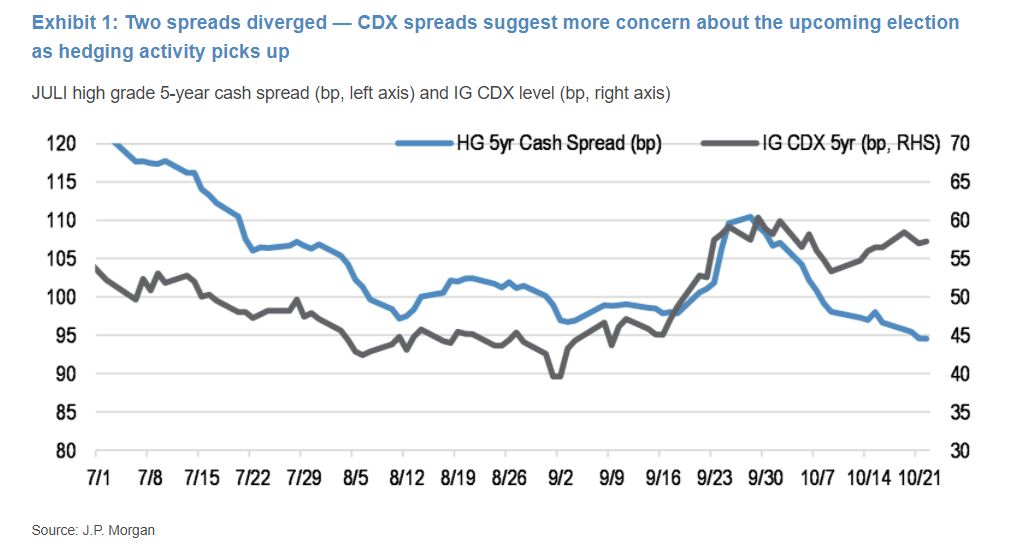

| The U.K. and France report the most coronavirus deaths since the first wave. A test for the yuan's recent rally. And a warning of "enormous" U.S.-China confrontation after the election. Governments across Europe are seeking to tackle rising infections while avoiding full-scale lockdowns, as the U.K. and France reported the most coronavirus deaths since May and April respectively. Italy and Greece posted record numbers of new cases. American Covid-19 hospitalizations have risen at least 10% in the past week in 32 states and the nation's capital. New York Governor Andrew Cuomo is seeking to keep 95% of the U.S. out of New York. Pfizer CEO Albert Bourla said the company may know by the end of October whether or not its vaccine is effective. Eli Lilly said a U.S.-run clinical trial of an antibody therapy will end. The recent strength in China's currency faces a new hurdle after the nation's banks abandoned inclusion of a key factor used to calculate the yuan's daily reference rate. The banks stopped using the counter-cyclical factor recently, which is part of how a quote for the reference rate is calculated. The rate, known as the fixing, restricts the onshore yuan's moves by 2% on either side. Under the tweak, lenders would have more room to guide the currency lower in the spot market, effectively allowing Beijing to give up some influence over the exchange rate. Stocks in Asia looked set to open lower after a retreat in U.S. equities, with lingering concern about the impact of the worsening pandemic on economic activity in some parts of the world. The dollar edged lower. Equity futures in Japan and Australia dipped, while those in Hong Kong rose. The S&P 500 Index declined modestly, though tech shares eked out gains on Advanced Micro Devices's $35 billion takeover of another chipmaker. Treasury yields dipped and Bitcoin rose past $13,500. Relations between the world's two largest economies will deteriorate further no matter who wins the U.S. presidential election, according to Ian Bremmer, who heads the risk consultant Eurasia Group. U.S. criticism of Beijing's detention of Uighurs as well as disagreements over Hong Kong, Taiwan, the South China Sea, intellectual property, trade and technology will escalate under the administrations of Joe Biden or President Donald Trump, he said. "There will be an enormous amount of confrontation and no trust between the U.S. and China, even if Biden becomes president," Bremmer said in a phone interview. Meanwhile, pollsters say Trump's reliance on rallies may only be cementing his electoral defeat. Few initial public offerings have aroused more anticipation than the record $34.5 billion listing of Jack Ma's Ant Group. Several of the numbers are truly astonishing. Still, a smash-hit IPO doesn't always translate into a long-term winner for investors. In Ant's case, the list of risks includes regulation, technology and competition. Here's more on exactly what could go wrong. What We've Been ReadingThis is what's caught our eye over the past 24 hours: And finally, here's what Tracy's interested in todayIn the intellectual hierarchy of markets, credit investors are typically thought to trump stock investors. So, with less than a week to go before the biggest event risk of the year, how is the smart money positioned ahead of the U.S. presidential election? The Cboe's Volatility Index now sits at its highest level in seven weeks at about 33.3, suggesting equity investors are pricing in some volatility. However Bank of America analysts point out that cash spreads in corporate credit have barely budged. By their calculations, the current risk premiums in corporate credit of about 130 basis points suggest that the VIX should be closer to 20, while the VIX suggests credit spreads should be closer to 160 basis points. So what's going on and who's right in the age-old battle of credit v. equities?  Bloomberg Bloomberg One explanation is that credit investors aren't actually hedging their positions through the cash market, but are instead reaching for derivatives, options and ETF shorts that act as more convenient "macro" overlays for big risk events. Analysts at JPMorgan point out that "derivative markets show that there has been more potential hedging interest than meets the eye" with a gap developing between cash spreads and Markit's CDX index (a basket of credit default swaps tied to investment-grade credits) as investors buy more protection. Meanwhile, short positions in the biggest investment-grade ETF are at their highest level in about seven months. Taking into account these more hidden corners of the credit market suggests there's less daylight between stock investors' expectations of volatility and those of credit investors than cash spreads would suggest. You can follow Tracy Alloway on Twitter at @tracyalloway. |

Post a Comment