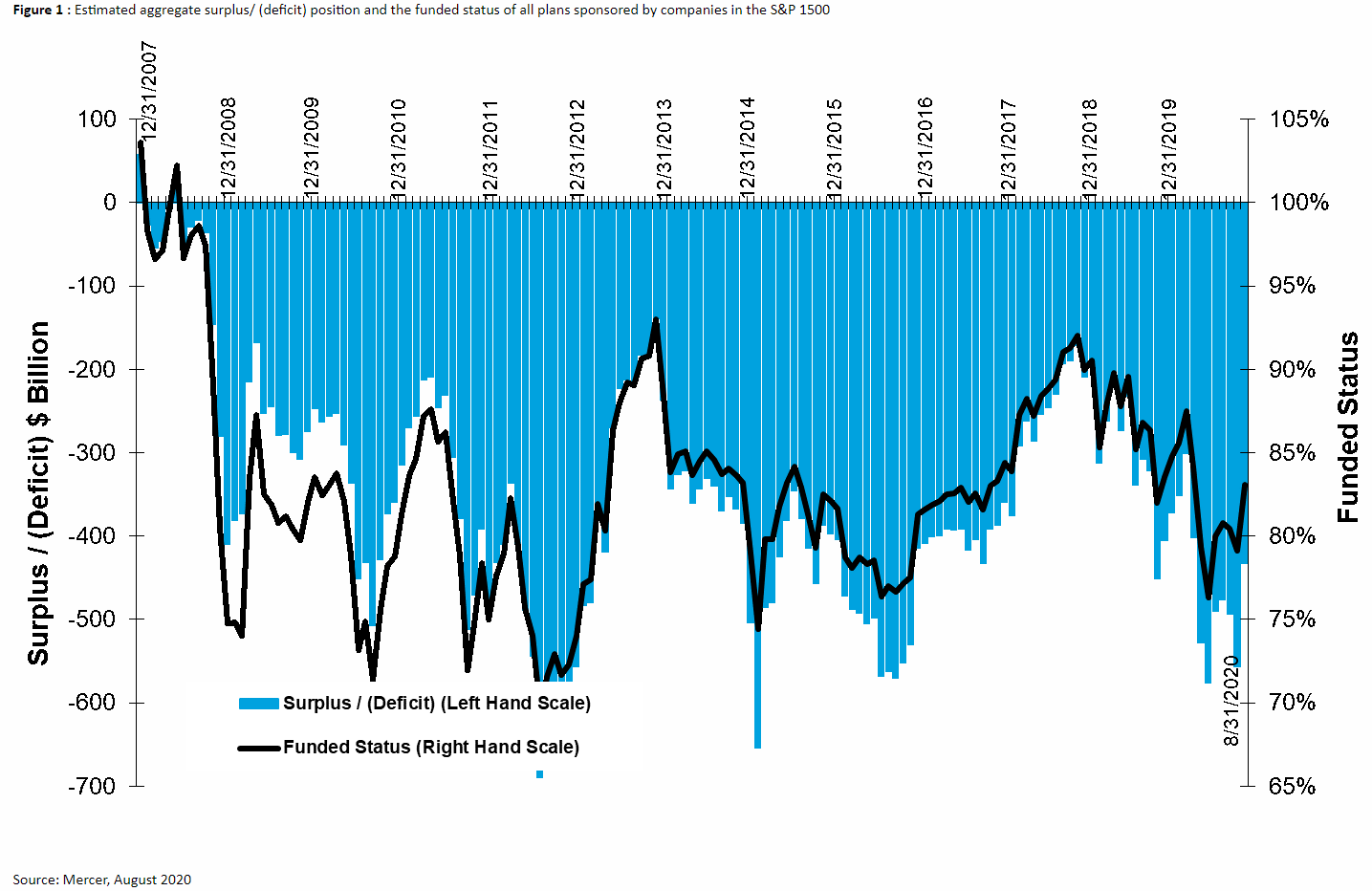

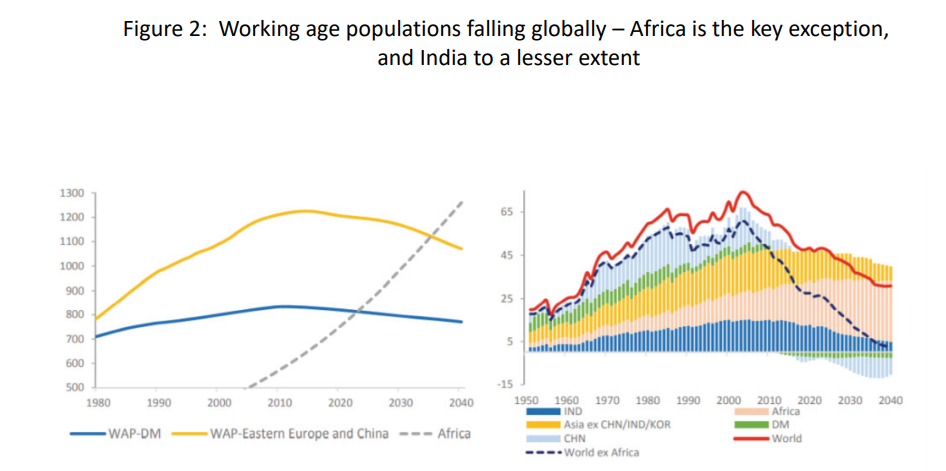

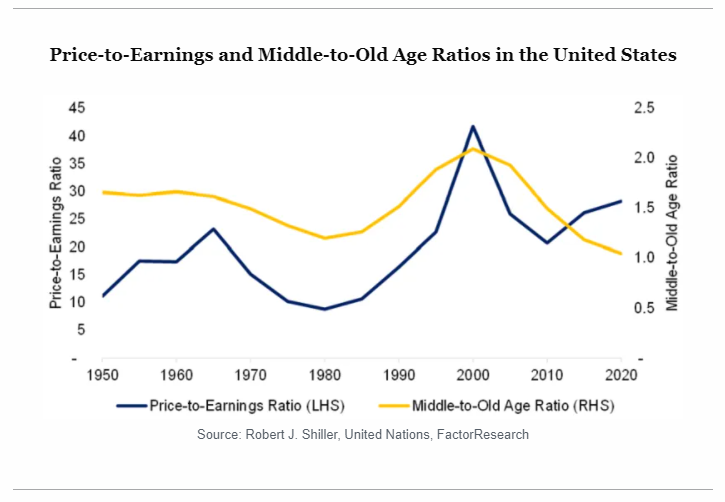

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Assume No PandemicLet's start with an assumption many of us would love to make. We are two years into the future, and the pandemic, one way or another, is over. It is no longer having an effect on longevity and public health, and it is no longer affecting economic activity. How will it have changed our attempt to save for retirement? What will be its long-term effects? If you thought that would be a good assumption, however, there is a catch. It turns out that there will be as much radical uncertainty after the pandemic as there is now, when many courses through the next 24 months still seem possible. The pandemic has intersected with a moment when demographic trends are undergoing a sharp shift. That leads to an array of alternatives. Inigo Fraser Jenkins of Sanford C. Bernstein outlines in this opinion piece for the Financial Times that pension funds will be left with no alternative but to take more risk, and buy more equities, despite the current sky-high valuations of equities, while regulators will have no choice but to let them. Bonds are very risky in the current situation, and likely to be eroded by long-term inflation, he argues. Meanwhile, low yields have left pension managers in a dire position, which is seen most clearly if we look at the pension deficits of big U.S. companies (or in other words, the amount by which their liabilities exceed their assets). The following chart is from the actuaries at Mercer:  Low yields make it far more expensive to fund an income for retirees. As a result, deficits are barely improved, either as a percentage or in total money terms, from their dire position in the depths of the financial crisis. But demographics could have other effects. The number of retirees as a proportion of the population is set to rise, in the U.S. and much of the world. Only Africa, where the population is expected to rise dramatically, and to an extent India will counter this pattern. The following chart is from a presentation given this week by Charles Goodhart and Manoj Pradhan to the Peterson International Institute on Economics, to which I will return later:  Demographic shifts on this scale will have an impact, but how exactly? In a post for the CFA Institute entitled Ageing and Equities: Selling Stocks for the Long Term, Nicolas Rabener suggests that a rising proportion of retired people will mean more people selling equities and buying bonds. Buying bonds puts downward pressure on yields. Meanwhile, there is a perceptible relationship over time between equity multiples and the proportion of working age people in the population compared to the retired. This is how he charts the relationship for the U.S., using Robert Shiller's cyclically adjusted price-earnings multiple:  The great peak in valuations came at the turn of the century as many baby boomers were approaching retirement and putting a lot of money into stocks. However, it is noticeable that valuations have managed to pick up again despite the drag that should be exerted, on this theory, by boomers drawing down pension savings. This is what we should expect for the future pricing of U.S. stocks if demographics are indeed financial destiny:  If this is right, then equities stand on the verge of a big secular de-rating. On this basis, pension funds would make their lives even harder by buying into equities. Rabener suggests they should be looking for alternative sources of return wherever they can find them. There is some good news to alleviate this gloom. Goodhart and Pradhan wrote earlier this year that the pandemic could mix with the nascent demographic shift and with the already strong air of a shift toward the populist left in many countries to create a major change in economic conditions. With working age populations reducing, workers will at last have some negotiating power: The likelihood is that wage demands in 2021 will match, or even perhaps exceed, current inflation, despite the inevitable pleas for moderation in the context of a 'temporary blip' in inflation. The coronavirus pandemic, and the supply shock that it has induced, will mark the dividing line between the deflationary forces of the last 30 to 40 years, and the resurgent inflation of the next two decades. Secular stagnation and 'lower for longer' will be relegated to the attic of defunct ideas.

They therefore make the breathtaking prediction that inflation could take off to the extent of 5% by the end of next year, or even higher — although the longer the pandemic continues the less will be the impact on inflation. Higher real wages and higher inflation will mean lower inequality, as workers will gain, while those whose wealth depends on assets will be hurt by the lower valuations that come with inflation and higher interest rates. Social tensions could actually reduce. Inflation would also be a relatively painless way of dealing with debt. But on this analysis, the problem for pension funds begins to look truly intractable, even though higher interest rates will at least make it easier to fund liabilities: The losers will be savers, pension funds, insurance companies, and those whose main financial assets take the form of cash. It will no longer be fiscally feasible to protect the real value of pensions from the ravages of inflation. The folly of responding to the crisis of excessive debt in 2007-9 by encouraging all borrowers (except banks) to take on more leverage and debt will become apparent.

Pradhan and Goodhart's ideas are profoundly important. You can see their presentation, moderated by the PIIE's president Adam Posen, here. Meanwhile their book that lays out the thesis at length, The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival, was published this month. Were we not in the middle of the most economically damaging global pandemic in living memory, it would by now be dominating debate. The questions it raises cannot be put off indefinitely. The critical issue will be generational justice. We have spent the last six months in a debate that ultimately revolves around what duties we owe to the elderly, as we ponder how to respond to the coronavirus. Once the pandemic is over, this question will return. Is the rest of the world really obliged to pay retirees in the West the pensions and other benefits that they have been promised, or can we reduce the expense to society by trying to persuade them to take a worse deal? The horns of that dilemma promise to be even sharper than the dilemmas caused by the pandemic. Time for some feedback. Yesterday I reviewed the evidence that the "size effect" in investing (that small-cap stocks tend to beat larger ones in the longer run) may never have existed. Today, I have been sent a report in the Financial Analysts Journal from 1989 by William Fouse, headed "The Small Stocks Hoax". As its title implied, it laid waste to the small-caps effect at a point when it had barely even been promulgated. It is plain from the first paragraph that this article comes from a bygone era: Investment folklore embraces many myths and legends that predate the birth and propagation of modern financial and portfolio theory. With the advent of the modern electronic computer and the parallel creation of databases, scientific method is at last beginning to supplant anecdotal analysis. But, alas, it appears to this writer that scientific method alone does not guarantee the avoidance of interpretive error and the propagation of a new mythology as durable as the archaic.

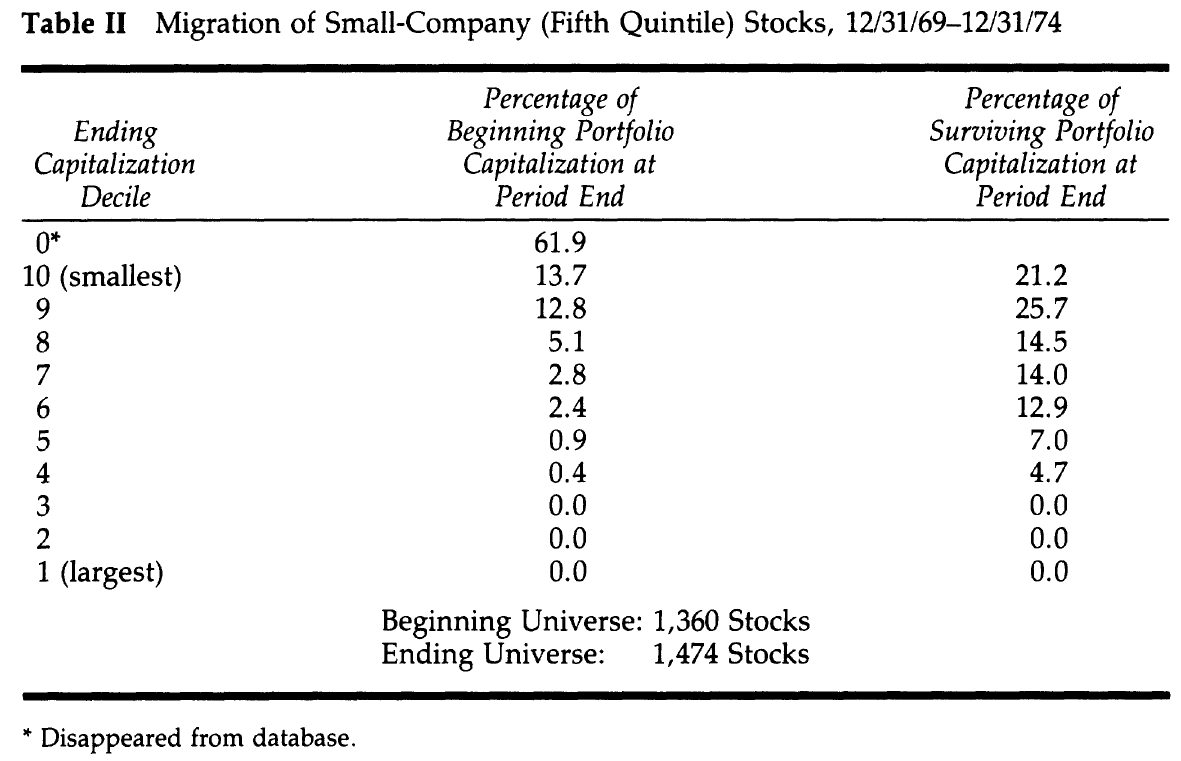

Fouse's writing style is a little dense for today's tastes, and the presentation of his results is tight and condensed. But for those with the time and energy it is an interesting piece. He reaches the same destination as today's skeptics, but by a very different route. Trading and rebalancing costs, particularly with the wide bid-offer spreads in small-cap stocks, would make it impossible to execute the strategy in practice, he points out. And he also crunches the numbers on how many small-caps actually stay small-caps over a five-year period. With the computing power of the time, this was a heroic undertaking. This is one sample. He looked at all the stocks in the Compustat database which had a market cap of at least $10 million on New Year's Eve 1969, took the bottom 20%, and then ranked them into equal deciles. By the end of 1974 (after admittedly a tough time for the American economy) 61.9% had disappeared from the database, and virtually none of the stocks from the beginning of the decade were in the top five deciles.  In other periods, the problem was that stocks got bigger and needed to be promoted. In all cases, his point was that "smallness" is not a static target. Buying and holding small stocks is not as difficult now as it was then, and the exercise does help reveal quite how much the modern factor revolution and "smart beta" owes to computers. But his bottom line is trenchant, and could have been written yesterday: What should one conclude from all of the above? There is no mysterious return to smallness. There is no free lunch. The moral of the story is: Beware of quasi-academics bearing anomalies!

Survival TipsOne of the great things about modern interactive journalism is that you get to find out a lot more about your readership and their tastes. And it would appear that Chopin has struck a chord, so to speak. I have heard from one proponent of Martha Argerich's recording of the preludes (here's a taste). (And if you want a change from the classic Glenn Gould recording's of Bach's Goldberg Variations, Murray Perahia is recommended. ) I have now been directed to the Cobbe Collection of historic pianos, which includes the Pleyel piano at which Chopin composed his pieces. You can listen to what his 7th and 8th preludes would have sounded like to the man himself as he was writing them here. For some insights into some very different composers and how they went about their work, you can also listen to the piano of Johann Christian Bach (son of Johann Sebastian), and the grand piano of Gustav Mahler (which I assume must have taken quite a lot of punishment). Have a good weekend. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

This Information is really good and informative. Thanks for it.

ReplyDeleteCheck below links and get useful information.

Share Market

YES Bank