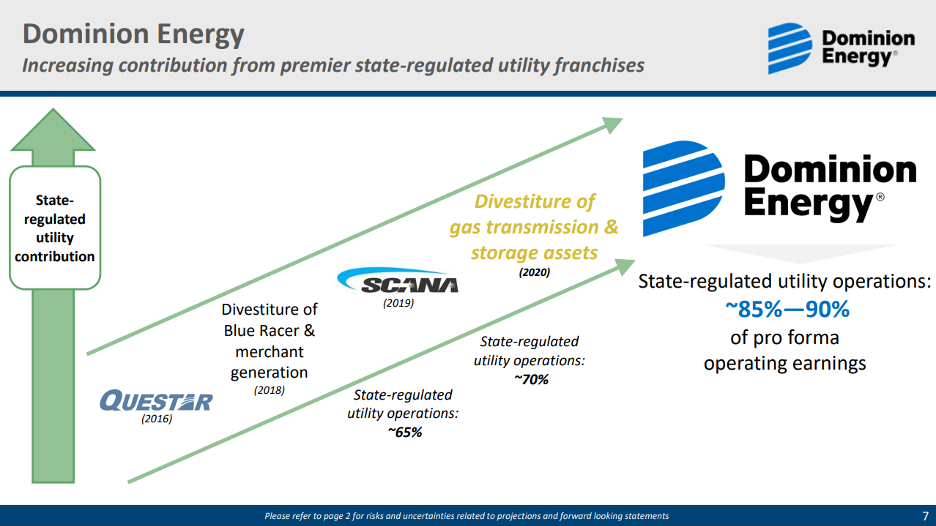

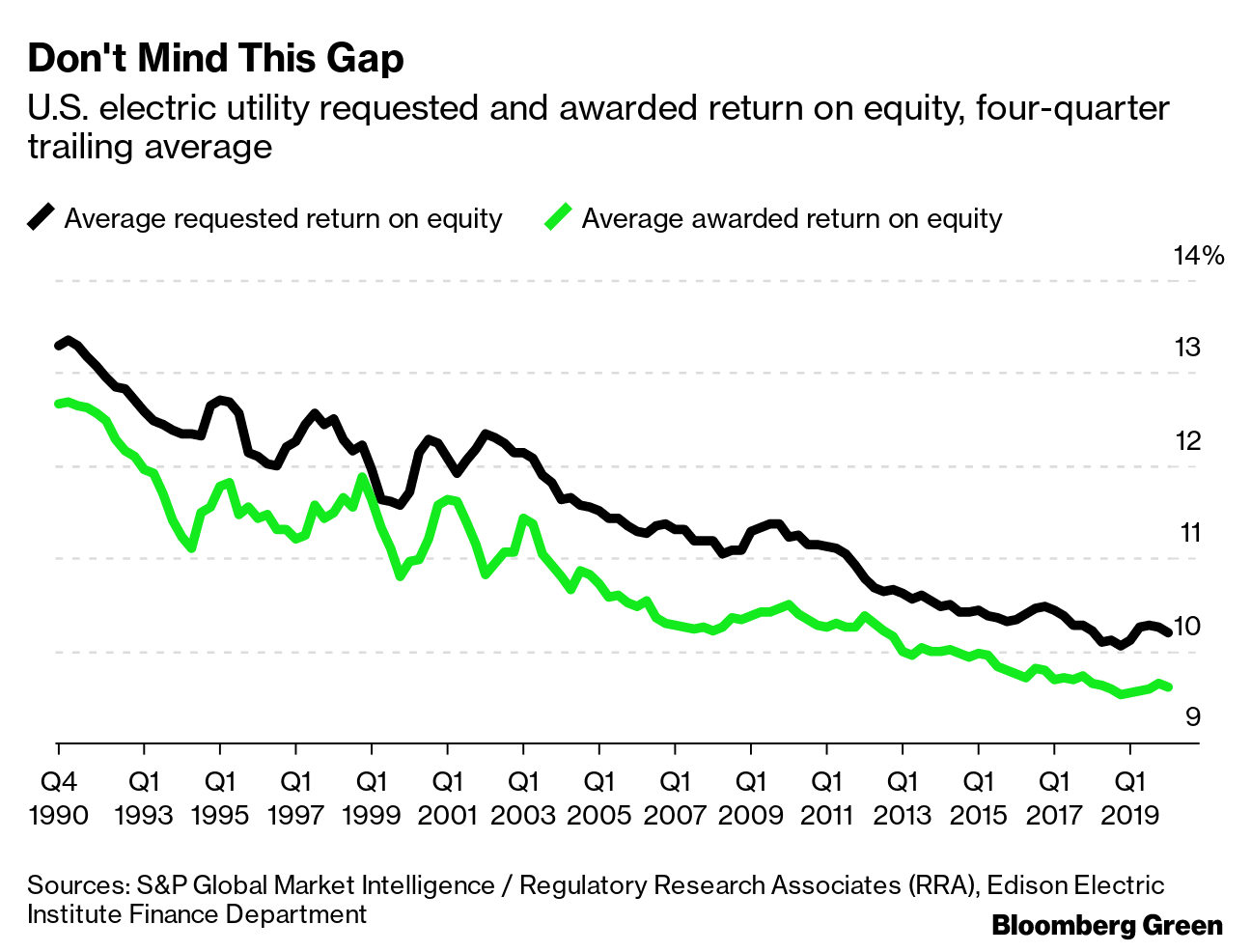

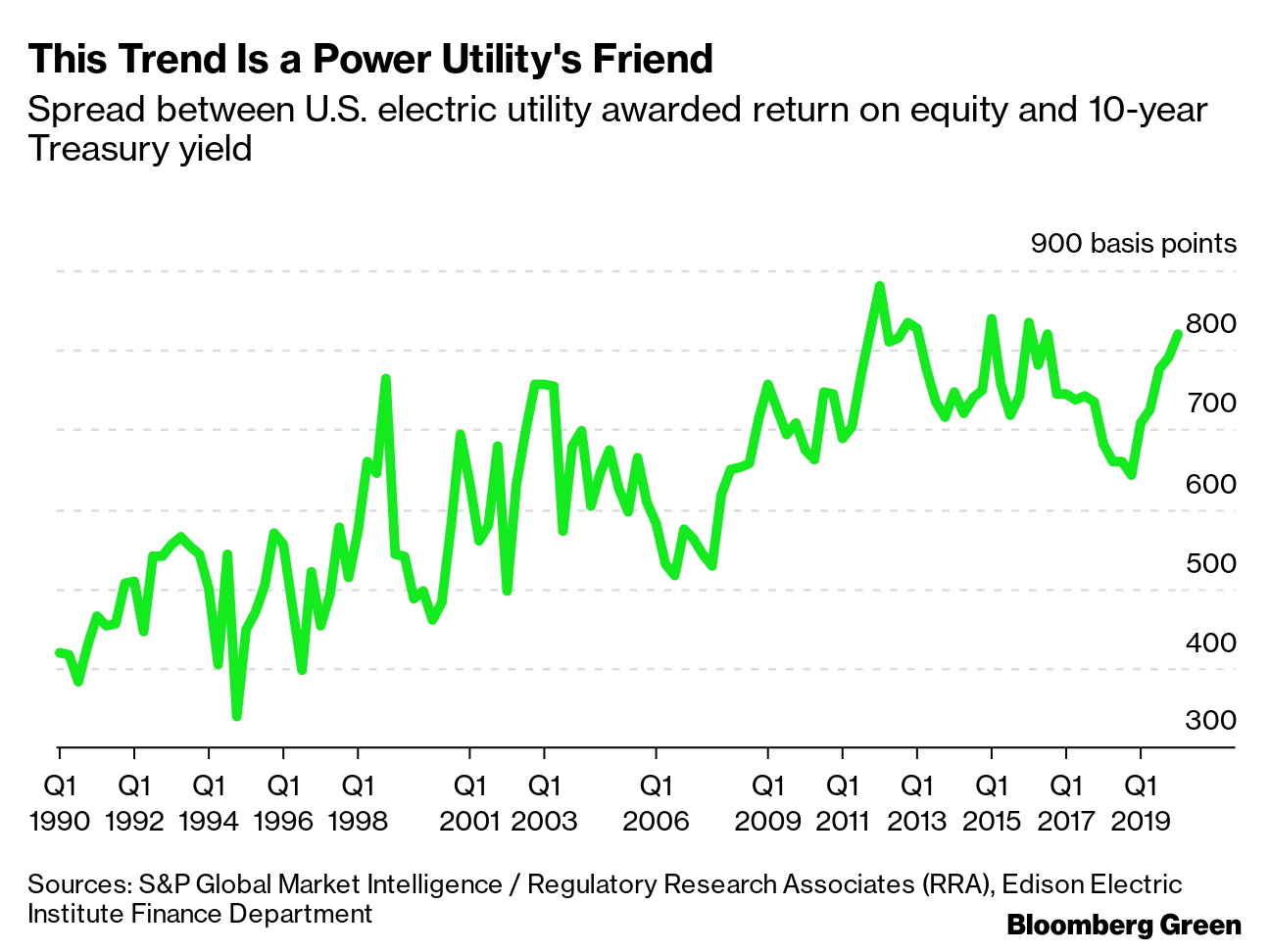

| On Sunday, Virginia-based utility Dominion Energy Inc announced plans to sell almost all of its natural gas pipeline and storage assets to Warren Buffett's Berkshire Hathaway Inc for $4 billion. At the same time, the Virginia-based utility said that it's killing the Atlantic Coast gas pipeline despite a Supreme Court ruling that would grant it passage underneath the Appalachian Trail. There's a lot going on here, and not just for the second-biggest U.S. power company by market value and the Oracle of Omaha. Natural gas, the "bridge fuel" to decarbonize the U.S. electricity system, is under pressure. But it's not yet a bridge to nowhere. There are a number of factors motivating Dominion's strategy. The first is that permitting for gas infrastructure is "increasingly litigious, uncertain, and costly," Chief Executive Officer Thomas Farrell said during a call with analysts to discuss its plans. The second factor is that the economics of operating a midstream pipeline—even one that has had no trouble attracting customers—aren't great, Farrell admitted. That doesn't mean the company is getting out of gas 7entirely. It still burns gas in power plants and will for some time. It also still owns distribution networks, which deliver gas to customers. That's the infrastructure Dominion sees carrying it into the future. The whole thing is part of a strategy to generate more of its earnings from assets with a return on equity that's determined by state regulators. That may sound unexciting, but that's part of the point. It's predictable, and it gives Dominion a clear story to tell capital markets: for every dollar we invest in regulated assets, we'll receive X amount back, guaranteed. There's a slide in Dominion's analyst presentation that illustrates this idea. It shows the company's past acquisitions of mostly-regulated companies such as gas distributor Questar and electric and gas utility Scana leading directly to Dominion's decision to sell its midstream gas interests and other assets. The result, it hopes, is that 90% of its operating earnings will come from state-regulated operations.  There's a financial strategy at work here too, one that I've written about before. It has three parts, the first of which is that returns on equity—both what utilities ask regulators for and what they're awarded—have been falling for decades. Not only that, the spread between asked and awarded is also fairly tight, and definitely tighter than it was in the mid-2000s and in the mid-1990s. That's good for messaging: it means you can say that what you want is pretty close to what regulators think you deserve. The second part of this strategy comes from the long-term decline in the risk-free rate of return on investments, as represented by the U.S. 10-year Treasury yield. We can think of 10-year Treasuries as a utility's opportunity cost for not investing in regulated businesses; the spread between a utility's awarded ROE and the 10-year note is effectively the risk-adjusted return on equity for regulated utilities. That spread is at a near-record high, north of 800 basis points, and it's more than double the risk-adjusted return of 25 years ago. The third part of this strategy is that Dominion can match a clear growth path to this return on equity. Virginia's power sector aims to be 100% clean energy by 2045, which requires building at least 16 gigawatts of wind and solar generation assets. Dominion is allowed, by Virginia law, to own up to 65% of those assets. Those it owns will become part of the utility rate base, the assets on which it earns its ROE. It's not quite risk-free, but it's not far off. The same is happening all over the country, meaning that gas networks on the other coast face pressure, too. In California a number of municipalities have mandated all-electric new construction—that is, gas won't be connected even for cooking purposes. In the past three weeks, two of the state's big utilities, Pacific Gas & Electric and Southern California Edison, have written to the California Energy Commission in support of a statewide all-electric buildings mandate. SCE's letter says it wants the Commission to move "as quickly as possible" so that utilities might "avoid costly spending on natural gas infrastructure that may become stranded before 2045." Implicit in that statement: not every gas infrastructure operator can count on Warren Buffett or his successors to buy their assets when the time comes. Nathaniel Bullard is a BloombergNEF analyst who writes the Sparklines newsletter about the global transition to renewable energy. |

Good information. Thanks for sharing. If you want to know more about stock market related topics then visit

ReplyDeleteAffle India

National Stock Exchange

Sterling & Wilson IPO

Unified Payment Interface