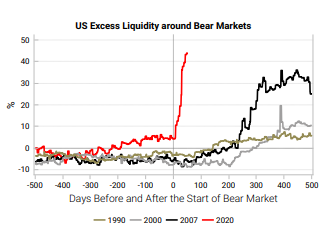

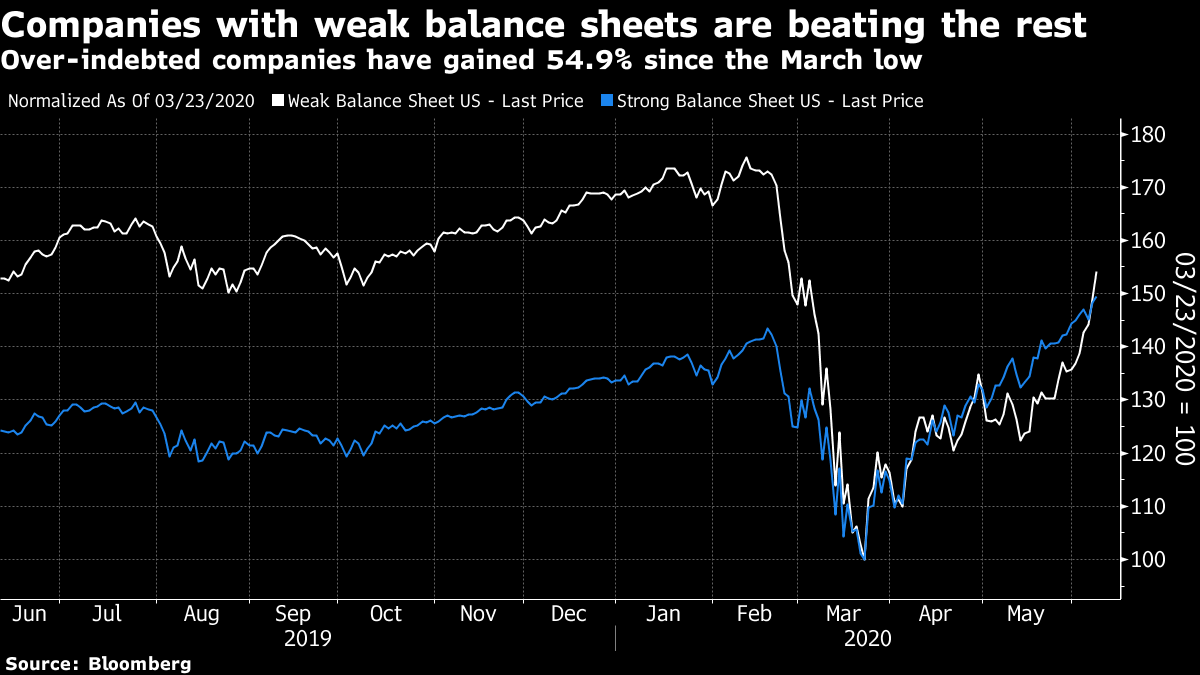

| Round trip has been completed. The fastest stock market collapse on record has been followed by the fastest recovery. As of the close of trading Monday in New York, the S&P 500 is, just, in positive territory for the year. After following the markets for most of three decades, I suppose it is reassuring to learn that I haven't seen it all. And if I have learned anything from the amazing events of 2020 so far, it is that you should never ignore liquidity. Growth in U.S. M2, a broad measure of money supply, has been its strongest since the Federal Reserve's records began in 1960:  For another way to ram home just how unusual and different the Fed response was this time, take a look at this extraordinary chart of how excess liquidity grew during each of the last four bear markets, from Variant Perception. It is usual for the Fed to make liquidity available in difficult times for the stock market, and it has been harshly criticized for the way it did so after the last crash; but nothing compares to what has just happened:  In the context of such an enormous gush of liquidity it is clear at an intellectual level that there was immense pressure on share prices to rise. That doesn't make this surge any easier to process at a personal level, and it doesn't banish the fear that it cannot be sustained once the market has to confront underlying economic and corporate fundamentals. The same applies in the terrible event that human beings put their immune system into a second great contest with the novel coronavirus. But as it stands, the last leg of the rally over the past week has widened the market's advance in just the way we would expect if there were a sustained rally predicated on a belief in economic growth ahead. The clearest evidence comes from the performance of companies with the weakest balance sheets, compared with those with the strongest. The sell-off earlier this year was particularly brutal for companies with weak balance sheets, reflecting the belief that over-leveraged companies wouldn't be able to survive the loss of revenues and profits from the Covid-19 lockdowns. The most leveraged still lag behind the market for the year to the date. But since the bottom on March 23, the following chart shows that they have now outpaced strong balance sheet companies, at least according to the popular baskets of stocks maintained by Goldman Sachs Group Inc.:  Over-leveraged companies, popularly referred to as zombies, have rallied by almost 55% in less than three months. This couldn't happen without strong optimism that any recession will be mild, and that there will be no secondary financial crisis caused by insolvency. Let's hope the market is right about this. Meanwhile, in another sign of encouraging breadth, value stocks have now outperformed growth stocks since the nadir, according to the Russell 1000 U.S. large-cap indexes:  And in a further clear indicator of investors working on the assumption that virtually insolvent companies have been let off the hook, the small companies of the Russell 2000 are also up more than 50% from the trough, comfortably outpacing the previously dominant mega-caps of the Russell Top 50:  In the long run, a true believer in Schumpeterian creative destruction shouldn't be happy about this. If uncompetitive and unprofitable companies are saved from going to the wall, they will continue to hog capital that could be better used by someone else. Big companies, with strong balance sheets recently refinanced at stunningly low rates, will be able to gobble them up, making the overall market less competitive. That makes for an ever less dynamic version of capitalism for the long run. In the short run, we are back to Go for the year, and those who timed the market well have picked up a lot more than $200. Q&A There is a lot more to discuss on this topic. At 10 a.m. New York time today, I will be taking part in an online Q&A on the terminal with our London-based macro strategist Laura Cooper. Markets Live's Kriti Gupta will be moderating. Please bombard Kriti with questions in advance at toplive@bloomberg.net. To follow proceedings and answer questions, just go to TLIV on the terminal.  Private Equity for the Masses Trust the satirical newspaper The Onion to keep its finger on the pulse of opinion. Recently it came up with a great headline:  Private equity has a dreadful image problem, which has worsened as the industry's power has grown and inequality has widened. Investors have made a lot of money as funds have poured in, but generally it has been difficult for individual savers to benefit. According to the Committee on Capital Markets Regulation, a group of academics and financiers lobbying for capital market reforms, a full 98% of U.S. citizens cannot invest directly in private equity. If the profits from "looting" businesses by taking them private flow only to the top 2%, then private equity understandably grows even more unpopular. Defined-benefit pension plans can invest in alternative assets, and increasingly do so, but private equity has been too illiquid for the various forms of defined-contribution plans that are coming to dominate the savings industry. That way, the growth of private equity can be seen, with some justice, as directly ratcheting up inequality, as it enriches the rich but not the rest. Private equity has also lacked access to the kind of patient capital needed to underpin what should be long-term investments. Last week, the U.S. Department of Labor, released new guidelines here making it far easier for 401(k) plans offered by employers to include private equity. This makes sense, asI argued in this newsletter back in October 2018. The committee's case for this reform can be found here. Naturally, few paid much attention to this announcement amid the whirlwind of events last week. But it does matter. And the committee is already out of the gates with a further proposal for the Securities and Exchange Commission to extend this from the employer-controlled pensions regulated by the Department of Labor to broader savings available to all, such as Individual Retirement Accounts. Their argument is that this can be done safely through registered closed-end funds holding private equity. This adds the risk that the fund trades at a discount to its net asset value, but offers a way of making transparent and liquid investments in an opaque and illiquid asset class. To quote John Gulliver, the committee's executive director, "the SEC does not need to issue a new rulemaking to expand retail investor access to private equity. Rather, the SEC can simply allow closed-end funds that primarily invest in private equity funds to register without limiting access to accredited investors. The necessary investor protections for retail investors are in place, as registered funds must provide extensive disclosures as to investment risks and fees." The idea is worth pursuing, though such closed-end funds will need to be monitored and regulated very closely — a process that might just help rein in the excesses of the private equity industry that annoyed The Onion. At best, these moves should allow a necessary democratization of finance, and might actually lean against the extremes of inequality, even if it will take a long time for those effects to be felt. It could also ensure that a controversial but important sector of finance becomes more transparent and accountable, while receiving the kind of patient capital it needs to work best. At worst, it will become another way to dump assets on Main Street, after Wall Street has enjoyed its first-mover advantage to the maximum, and the institutionalization will have the same deleterious effects that it had on hedge funds more than a decade ago. The regulators are correct to take this step, but they need to get it right. Survival Tips Professional sports will soon be back with us. Infuriatingly, baseball still hasn't agreed on a way to play some games in front of empty stadiums, but it sounds like cricket will be back soon, and England's Premier League soccer will be back next week. That may not be cause for celebration for my home town team, Brighton & Hove Albion: They were 15th out of 20 when the season was interrupted, and face a brutal schedule in which they play only one of the five teams below them and eight above. Meanwhile, my kids would like to recommend that everyone keep watching a brilliant substitute for live sports — Jelle's Marble Runs. Thanks largely to the vocal support of John Oliver (Englishmen in New York — you just can't ignore them), the marble runs now have more than a million subscribers on YouTube. In front of packed stands full of marbles, different teams of marbles contest a series of exciting races in a series of ingeniously constructed courses, all with the excitable commentary you would normally expect for a Formula One Grand Prix. It needs to be experienced. There's a great back catalog to look through. For now, my son informs me that the beginning of the Marble League for 2020 on June 18 will be the big event to look forward to. He seems more excited by this than by Brighton's forthcoming backs-to-the-wall restart to the season against Arsenal on June 20, which worries me a little. But anyway, to keep body and soul together, try Jelle's Marble Runs. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment