European Union leaders are inching toward an agreement on how to rebuild their economy when the coronavirus subsides.

But the lowest common denominator approach they are likely to stick with on today's videoconference is as significant for what it doesn't address as what it does.

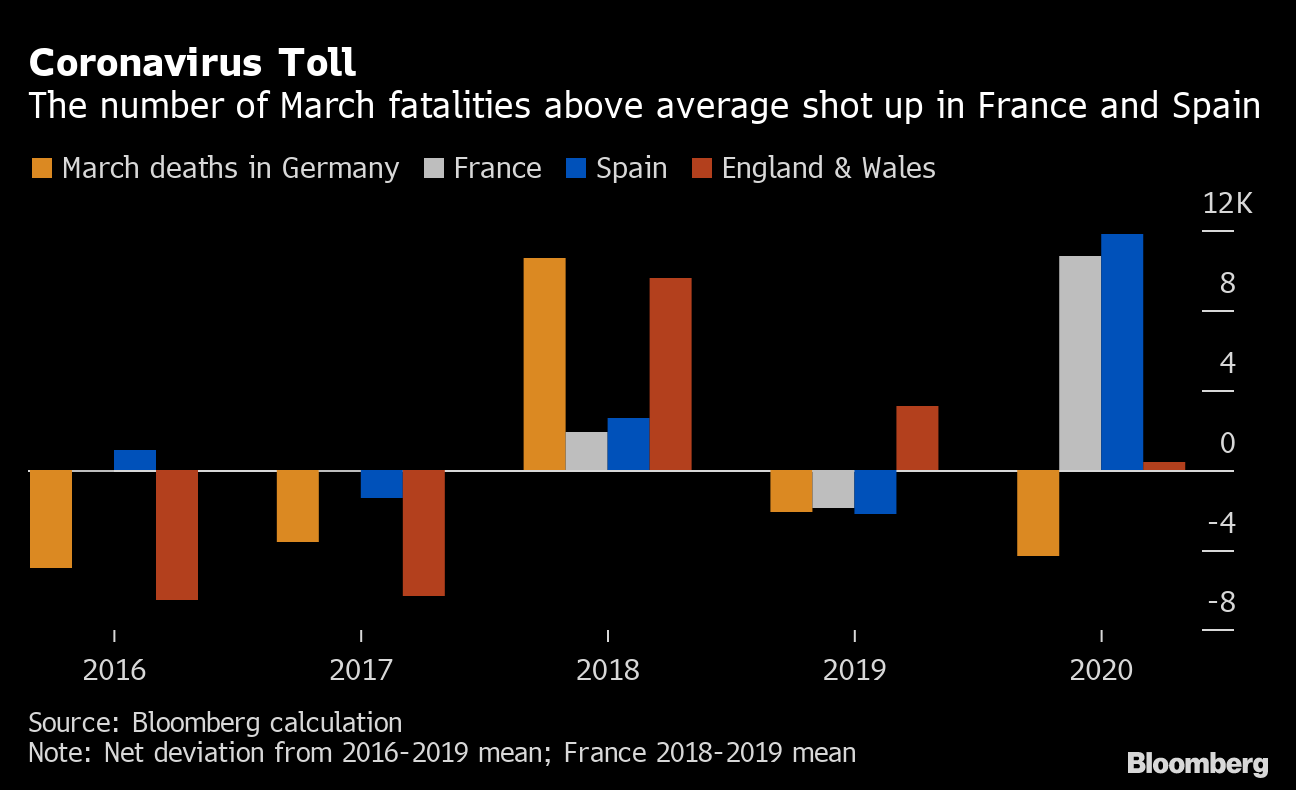

France, Italy and Spain, where both the pandemic and government borrowing in Europe has been most intense, are struggling to persuade the rest of the bloc to share the financial strain that their public spending will create.

Rookie European Commission President Ursula von der Leyen's efforts to take on the traditional role of power broker aren't helping either. Von der Leyen hadn't even read her officials' latest compromise proposal on the eve of the talks.

Italian officials are projecting that the country's government debt will be more than 150% of gross domestic product by the end of this year, way beyond the level Greece was at when it triggered the sovereign debt crisis in 2009. Spain's central bank sees public borrowing reaching 120% of GDP and France forecasts 115%.

The EU has so far offered only a series of stop gaps to address that fundamental challenge – an emergency bond-buying program from the European Central Bank and a range of low-interest borrowing options.

Band aids tend to come unstuck in the end. Perhaps that's why the EU so often seems to be in crisis.

— Ben Sills

Post a Comment