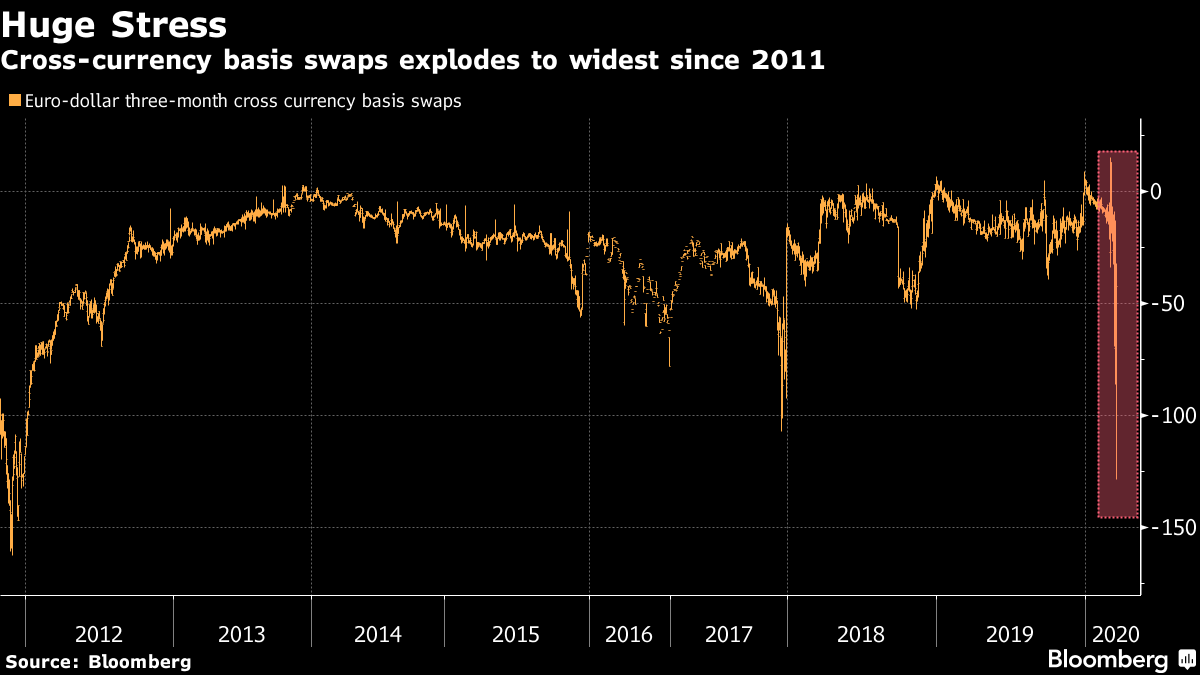

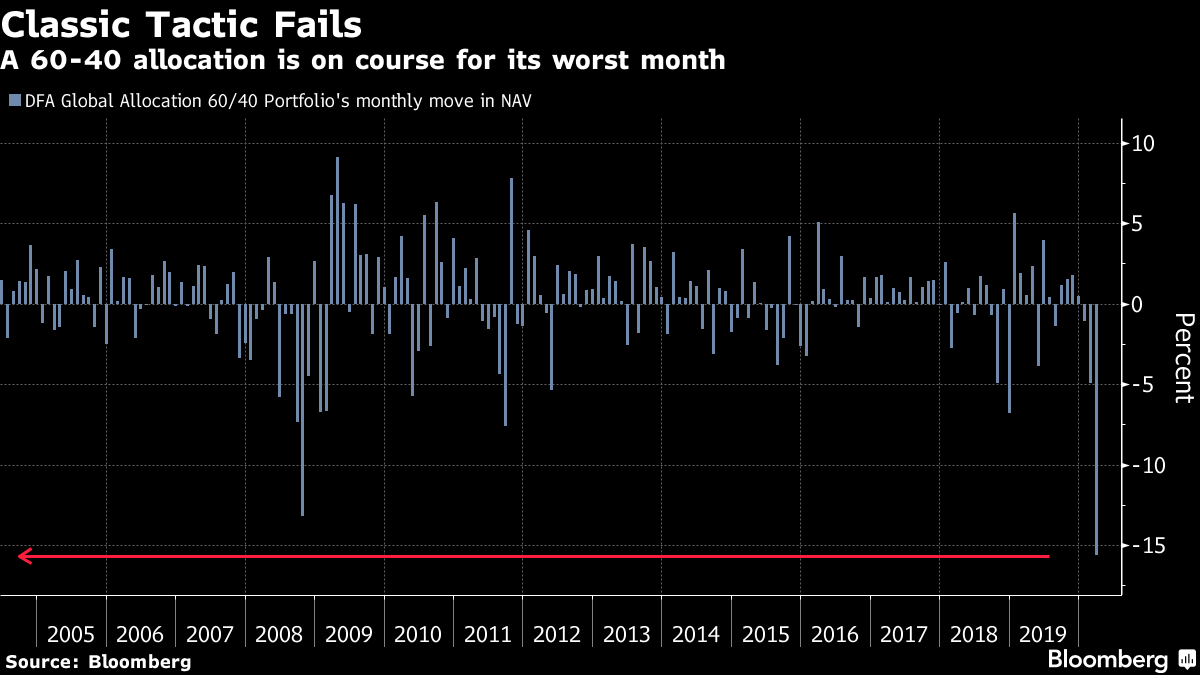

| Welcome to the Weekly Fix, the newsletter that's wondering if the same people who believe the yield curve had forecast this downturn also think Treasuries are selling off because of a brightening outlook for growth and inflation. –Luke Kawa, Cross-Asset Reporter Fire Sale Don't look for reason from a price change. It's common advice. It's also frustrating to hear, for those who work in or cover markets for a living. Prices are often all we have to try to make sense of the world and the conventional wisdom regarding what the future holds. That's problematic at this juncture. Right now, the particulars of the price action leave much to be desired. The price of a financial asset does not seem to matter. All that matters is whether it has a price – and if it does, it will be sold. Liquidity in even the deepest, safest asset class – U.S. Treasuries – is garbage, according to Citigroup. "Order book has collapsed to 10% of historical average and trade impact cost has risen to more than x2 normal market function," writes David Bieber. "Current levels are close to historical extremes." "We interpret the current sell-off in rates as technical with broad based liquidation and deleveraging to 1/ take down balance sheets, 2/ fund margin calls, and 3/ meet redemptions," writes Bank of America's rates team. The Treasury market is not telling us anything about the outlook for growth and inflation. All it is telling us is that investors are desperate to sell anything and everything, including Treasuries. How else to explain 10-year yields rising about 20 basis points in each of the past two weeks as U.S. stocks suffer their swiftest descent into a bear market in history?  The more illiquid the asset class, the more acute this problem. Here's Bieber's colleague Michael Anderson on the high-yield market: "Considering the rapidly deteriorating economic outlook, we expect the market will eventually differentiate between credits with resilient balance sheets and those already on the cusp of insolvency. With funding concerns rising (e.g. 3mo Libor higher today than it was prior to the Fed's rate cut on Sunday) and balance sheet capacity constrained, investors are raising cash by selling anything with a bid. Despite the revival of crisis-era Fed/Treasury programs, market dislocations are proliferating at an alarming rate. As a result, credit quality is not the primary reason for trading. Given the broad dislocations and tight liquidity throughout markets, we anticipate the technical price action will continue." There's no shortage of sell-side trade recommendations advocating for investors to seize this crisis as an opportunity, from the straightforward arbitrage opportunities to the liquidity-induced dislocations that will pay off for the patient investor over the long haul. One of the most popular pitched trade in the rates universe appears to be a long breakeven position. Inflation-protected securities – which are more illiquid than run-of-the-mill Treasuries – have sold off more fiercely – up 100 basis points from their early March low. By extension, this has pressured market-based measures of inflation compensation to their lowest levels since the financial crisis. The bet appears to be a no-brainer, unless America is in for a repeat of the 1930s. Outside of the Great Depression, U.S. CPI has averaged well above 55 basis points throughout history.  Bloomberg Bloomberg But most of these opportunities exist, and will continue to do so, precisely because they cannot be acted upon for most institutions, at least not in any size. In a pan-asset cataclysm, portfolio managers have many more reasons to go to cash than to stick their necks out – and in many cases, don't even have a choice. Margin call? Sell what isn't bolted down. Clients withdrawing funds? Same story. There's another old market saying: "When the time comes to buy, you won't want to." More and more, that quip seems like it needs amending: "When the time comes to buy, you probably won't be able to." The Fed Can Do More In theory, governments are supposed to engage in counter-cyclical tax and spending policy to stabilize the economy, serving as a source of aggregate demand when households and companies are too tapped out or too scared. In the U.S., that's a difficult prospect for state and local governments, which are tasked with running balanced budgets. That puts them in the position of having to cut spending at a time when tax collections are going down (when the economy is in trouble). Enter the central bank. The Federal Reserve has already revived the alphabet soup of programs used to try to ease stresses in important funding markets. But the central bank could do more by marshaling its presumably limitless financial resources to support state and local finances to provide a more tangible contribution to America's quest to contain the spread of the coronavirus and treat the afflicted. Skanda Amarnath of Employ America and Yakov Feygin of the Berggruen Institute have written a proposal pointing out that Section 14(2)(b) of the Federal Reserve Act enables Chairman Jerome Powell and his colleagues to commit to buying municipal bills with a maturity of six months or less. They write: "In this pressing emergency, state governments bear the major financial cost associated with on-the-ground interventions to treat and prevent the spread of communicable diseases. Logistically speaking, were it not for their budget and financial constraints, they are arguably in the best position to allocate expenditures for expanding the capacity of our public health system. To guarantee that state governments make the necessary investments during this trying time , all institutions of the Federal Government should, within their statutory authority, play their appropriate supporting role." Philadelphia Fed chief Patrick Harker is open to the idea of municipal bill purchases. Democratic lawmaker Maxine Waters also urged the central bank to "provide much-needed support to those who are on the front lines of this pandemic." This is a pressing issue because of the continued carnage in the municipal bond market, which is afflicting the same institutions that are trying to keep America safe and healthy. Even as Treasuries rallied on Thursday, the selling in munis continued. Given the backdrop that brought about de-risking of anything with a price, this sea of red in this asset class is downright depressing. As Bloomberg's Matt Boesler pointed out: "Hospitals around the country are trying desperately to contain the pandemic and meanwhile their borrowing costs are surging because investors are dumping municipal debt as markets melt down. This is exactly why people are talking about muni QE." |

Post a Comment