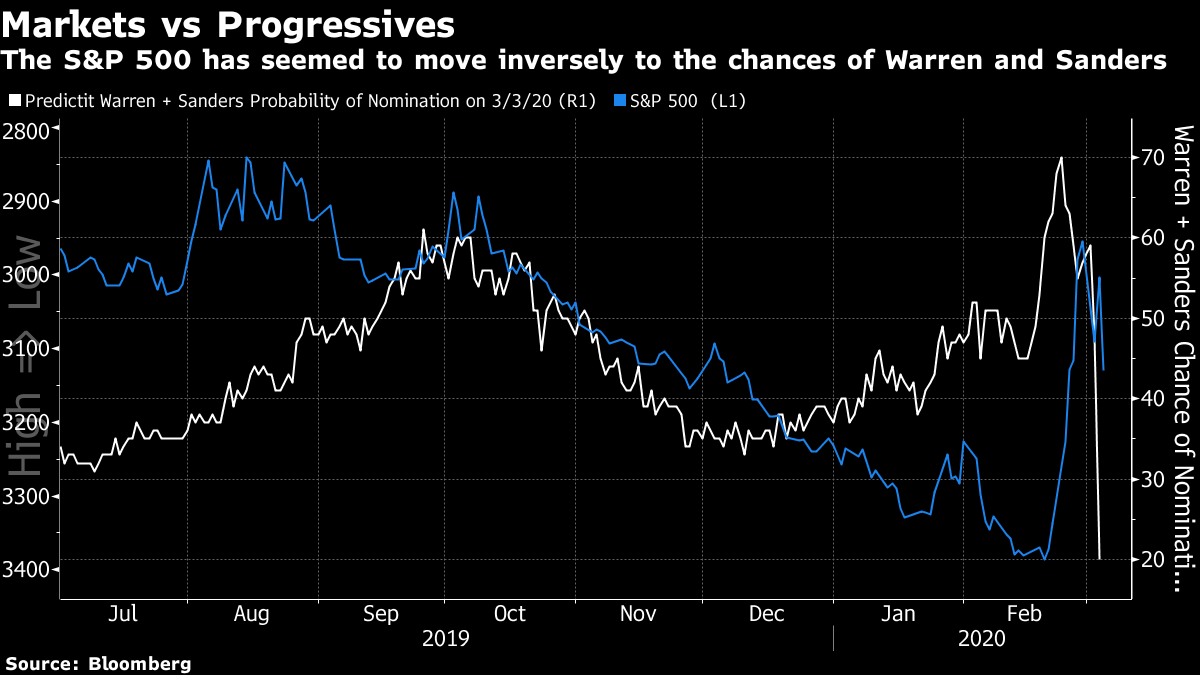

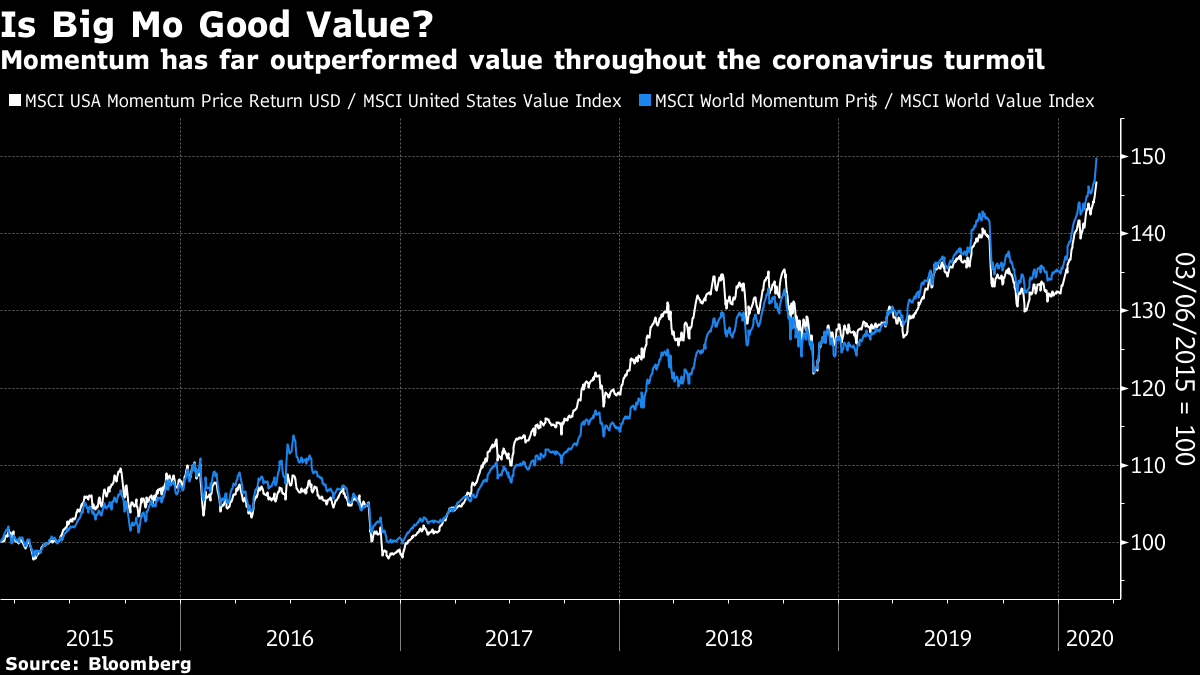

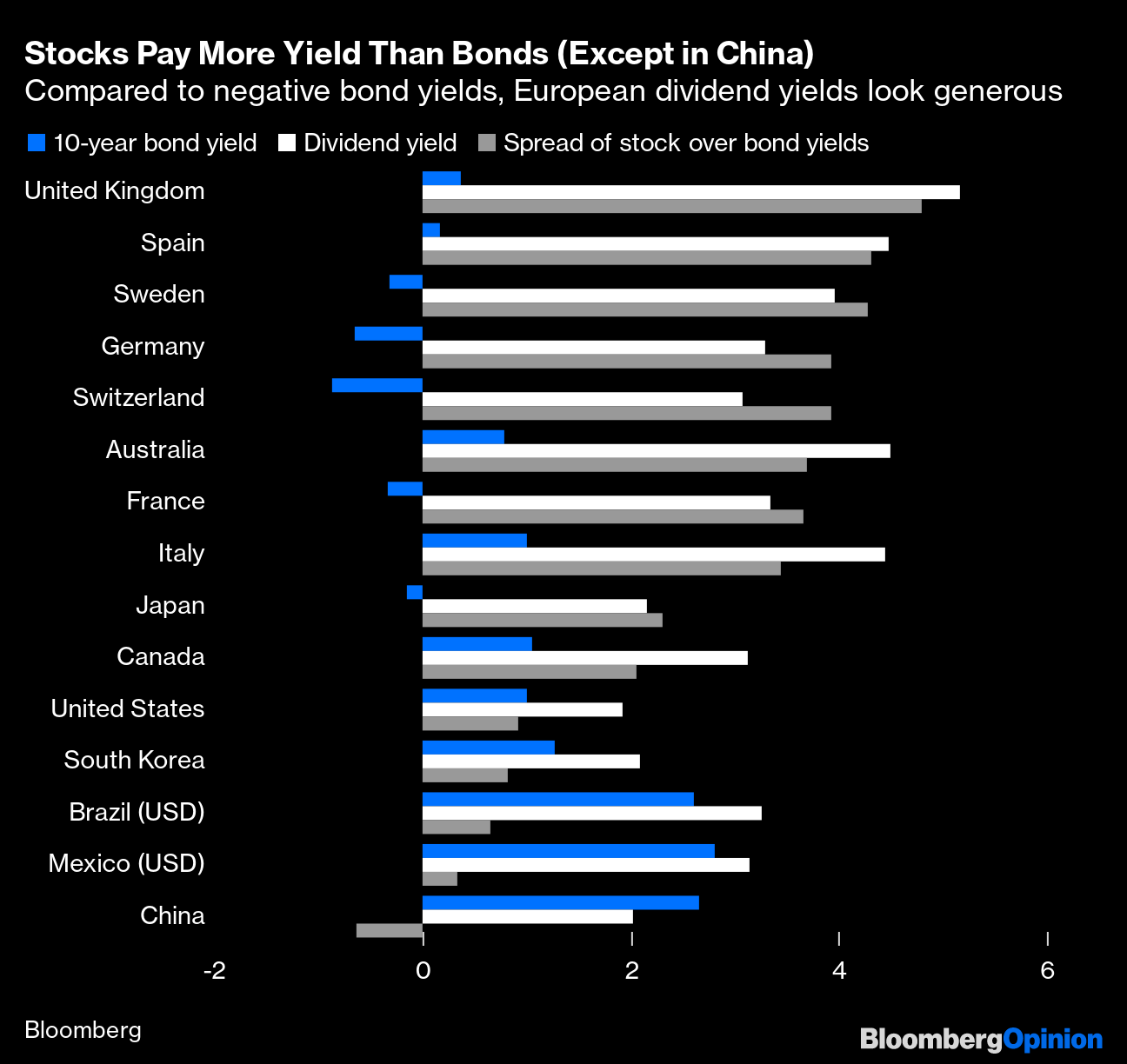

Joementum, Schmomentum Sir Isaac Newton's laws of motion have been around for more than three centuries now, and they have stood the test of time. They remain a powerful description of movement in the physical world. They also appear to offer a great description of movements in markets, and in the political world — but that appearance may be deceptive. Stock markets whipsawed again Wednesday, reversing upward this time. By the close, the S&P 500 had gained more than 4%. Is this because, following Newton, it was compelled to move by a force that provoked an equal and opposite reaction? One popular explanation was "Joementum." The spectacular performance by former Vice President Joe Biden in the Super Tuesday primaries has made him the favorite for the Democratic nomination. It has also suddenly crushed the chance that a "progressive" will be nominated to take on President Trump. In the following chart, the odds of both Elizabeth Warren and Bernie Sanders, the two left-wing standard-bearers, are summed into one line. First Warren and then Sanders had periods when they appeared to be the front-runner, and both overlapped with weakness for the stock market. Wednesday saw those odds collapse, and the S&P 500 rebound:  The managed healthcare sector, which stands to be radically shaken up if not nationalized under a President Sanders, led the market. But beyond that, the importance of the Biden ascendancy can be overstated. The stock market was worried by the ascendancy of Warren last autumn, because she was perceived as a real challenger to Trump. But the market carried on rising even as Sanders rose to become the front-runner earlier this year — because he was seen as virtually certain to lose to Trump. The market's big sell-off last week did overlap with a brief period when Sanders seemed all but assured of the nomination, but there was a very obvious alternative force to push it. Ascribing the index's gains Wednesday to Joementum is a distinct stretch, although it is understandable with politics so much in the news. The Biden victories on Super Tuesday, incidentally, also went a long way to disprove the existence of some Newtonian form of "momentum" in politics. Ever since Jimmy Carter came from nowhere to grab the presidency in 1976, by putting in months of campaigning in the first states of Iowa and New Hampshire that propelled him forward, it has been held that momentum is a vital property that candidates must have in order to win. This ignores the fact that nobody since Carter has won both Iowa and New Hampshire and gone on to take the presidency (John Kerry came closest in 2004, when he surprisingly won both states, and the nomination, but failed to gain the White House). This year, Biden finished fourth and fifth in the first two states, leaving him with no momentum whatever. What has happened since suggests there is much less to the concept than anyone thought. It also means that the first two states may begin to get less attention from media and candidates in future. If momentum doesn't exist in politics, though, it certainly exists in markets. The momentum style of investing — betting on winners to keep winning and losers to keep losing — has seldom done better. And for all the apparent volatility and change of the last few weeks, that has remained constant. There has been no great reshuffling of the market. The losers, for the most part, are value stocks — bought because they are cheap compared to their fundamentals. Value has been cheap ever since the financial crisis, and continues to grow cheaper relative to other stocks — and, yes, still the momentum stocks are able to leave them all behind. This is true in the U.S. and the world as a whole.  What can explain this? Joseph Mezrich of Nomura Instinet LLC suggests that far from its image of buccaneering speculation, the strength of momentum this year is a sign of growing risk aversion. Safety is in the winners, while risk is perceived to be in the losers, which generally have weak balance sheets and are ill-suited to deal with a deflationary recession. Value stocks are particularly concentrated in financials and resources companies, which are having a terrible time. This is a case where risk aversion and momentum are taking the market to an ever riskier place where it is dominated by a small group of ever bigger companies. If we needed any evidence that Newtonian laws might be ill-fitted for financial markets, remember that he lost much of his fortune buying shares in the South Sea Bubble. When Dividend Yields Beat Bond Yields Finally, another law once regarded as immutable is in trouble. For a long time, it has been taken as axiomatic that bonds yield more than stocks. They need to do this to compensate investors for the lack of growth possibilities that come with stocks. When bond yields approach or even fall below those on stocks, this means that equities are very cheap. But there is only so far this can be taken. For about 10 years now, a stale argument has persisted between equity bears saying that the U.S. stock market looks expensive, compared to its own history and to fundamentals, and bulls pointing out that equities look dramatically cheap relative to bonds. That has reached the point in the last week where the S&P 500 yields more in dividends than the yield on a 10-year Treasury bond. This has happened only a few times in the past, and only briefly. It implies that equities are radically cheap. When I made this point to Ben Inker of GMO LLC, the Boston fund management group founded by Jeremy Grantham, who is notoriously skeptical about stocks, he replied that if you feel that way about U.S. stocks, "you'll absolutely love European stocks." This brief and utterly unscientific exercise confirms Inker's prognosis. The following chart takes the dividend yield for each country's most prominent equity index (as defined by the WEI page on the terminal, and you can bet I used the S&P 500 rather than the Dow Industrials), and compares it to its 10-year sovereign bond yield, as shown on the WB page. This reveals that at present, China is the only market of any great significance where bonds yield more than stocks. American dividend yields are very low, showing that the country's market is indeed expensive compared to most others. And European stocks are staggeringly cheap compared to bonds.  To use another simple test — ask how much will need to go wrong in the U.K, Spain, Sweden or Germany for anyone who bought a bond rather than stock to feel good about it in 10 years' time. Nothing much short of a full-blown repeat of the Great Depression would make the bond emerge victorious. For those who can afford to wait a few years, European equities look a more than decent investment on this basis. And their bonds look untouchable. Unless, of course, the bond market is right in signalling something very like the Great Depression. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment