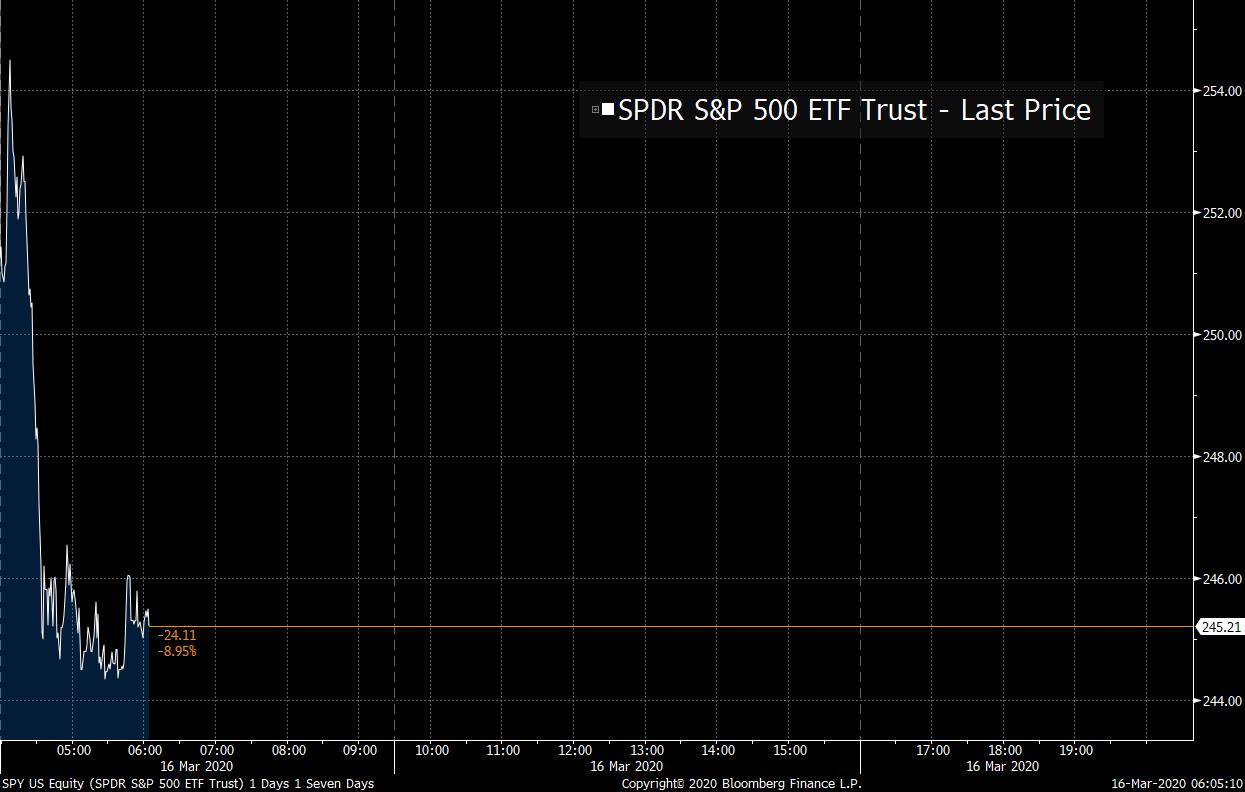

| Central banks cut again, markets fall again, and outbreak continues to spread. Rate slash In its second emergency rate cut in two weeks, the Federal Reserve reduced its benchmark to basically zero, dropping the target to 0-0.25%. The bank also said it would boost its bond purchases by $700 billion. The central banks of both South Korea and New Zealand both also slashed rates, while the Bank of Japan upped its asset purchases. Global central banks agreed to widen the scope of their dollar swap lines with the Federal Reserve. Market crash Investor reaction to the surprise further central bank easing has been to use it as an opportunity for more moves to safety. S&P 500 futures hit the bottom of their trading limit shortly after opening and Treasury yields dropped. Overnight, the MSCI Asia Pacific Index was down 3.8% as data from China showed an even worse than expected slump in the first two months of the year. In Europe, the Stoxx 600 Index was more than 7% lower at 5:40 a.m. Eastern Time, with the gauge hitting the lowest level since 2012. While S&P 500 futures remain limit-down, investors are looking to ETFs to see how bad the carnage at the open could be. The 10-year Treasury yield was at 0.76% and gold reversed earlier gains. Lockdown Europe is moving to something resembling the closure of their economies as people in most countries on the continent are told to stay at home. The World Health Organisation said the region is now the center of the global virus outbreak. Efforts to contain the spread of the coronavirus in the U.S. are increasing with the Center for Disease Control and Prevention recommending all gatherings of more than 50 people be cancelled for the next eight weeks. New York City has closed its school system, while businesses are shuttering across the country. Goldman Sachs Group Inc. sees U.S. GDP shrinking 5% in the second quarter after 0% in the first three months. Response Corporations are doing what they can to react to the situation, with airlines by far the hardest hit so far, with many grounding large portions of their fleets. Eight giant U.S. banks have agreed to stop buying back their own shares, saying they will instead focus on supporting clients and the nation during the pandemic. Almost all companies are recommending their employees work from home where possible. On the government side, the calls for more fiscal stimulus are becoming louder as politicians move to increase spending. There is a G-7 heads of state video conference scheduled for 10 a.m. this morning, where a coordinated response will be discussed. Crude drop The fallout from the bitter breakup of the OPEC and Russia alliance has come at a terrible time for the oil market, with the increase in supply from both sides pushing the world towards its biggest ever surplus, according to IHS Markit. The spread between Brent and West Texas Intermediate closed to within a dollar, after the announcement from President Donald Trump that the U.S. would make purchases for emergency reserves. A barrel of WTI was trading below $30 this morning. What we've been reading This is what's caught our eye over the weekend. And finally, here's what Joe's interested in this morning The House passed a bill on Friday night to provide relief to some people who are affected by the virus, but it's far short of the fiscal bazooka that several economists believe we urgently need. What's weird about this situation is that we need massive fiscal help from DC, but we don't exactly need stimulus, per se. Stimulus typically implies an attempt to get the economy moving positively again. But that's not exactly what we want right now, because in the ideal scenario everyone could just wait this thing out by spending a month or two in their homes eating canned goods, watching Netflix and facetiming. Then when the virus is mostly gone, go out and have a bacchanal for the ages in the warmer weather. The problem, as Larry Summers eloquently put it, is that "economic time has been stopped, but financial time has not been stopped." In other words, if we all cocoon for two months, we might physically survive, and the infrastructure of the modern world would be waiting for us upon our re-emergence, but in the meantime the bills pile up. The rent's due. The mortgage is due. Or the landlord's mortgage is due. The credit card bill is due. Taxes are due. For a business, paychecks must go out. Suppliers must be paid. Sp we don't need economic stimulus right now. We don't need people out shopping or building new infrastructure or building new homes. Every one of those things involves people congregating and risks spreading the virus. What we need is cash to keep people from going bankrupt or evicted. Cash to keep the lights on. Cash to keep people employed; to keep their healthcare. Cash to buy basic necessities, like food and medicine. So let's not think in terms of reviving growth for now. Let's think in terms of cash, so that for as long as we're in deep freeze, people can stay alive and continue to meet their financial obligations.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment