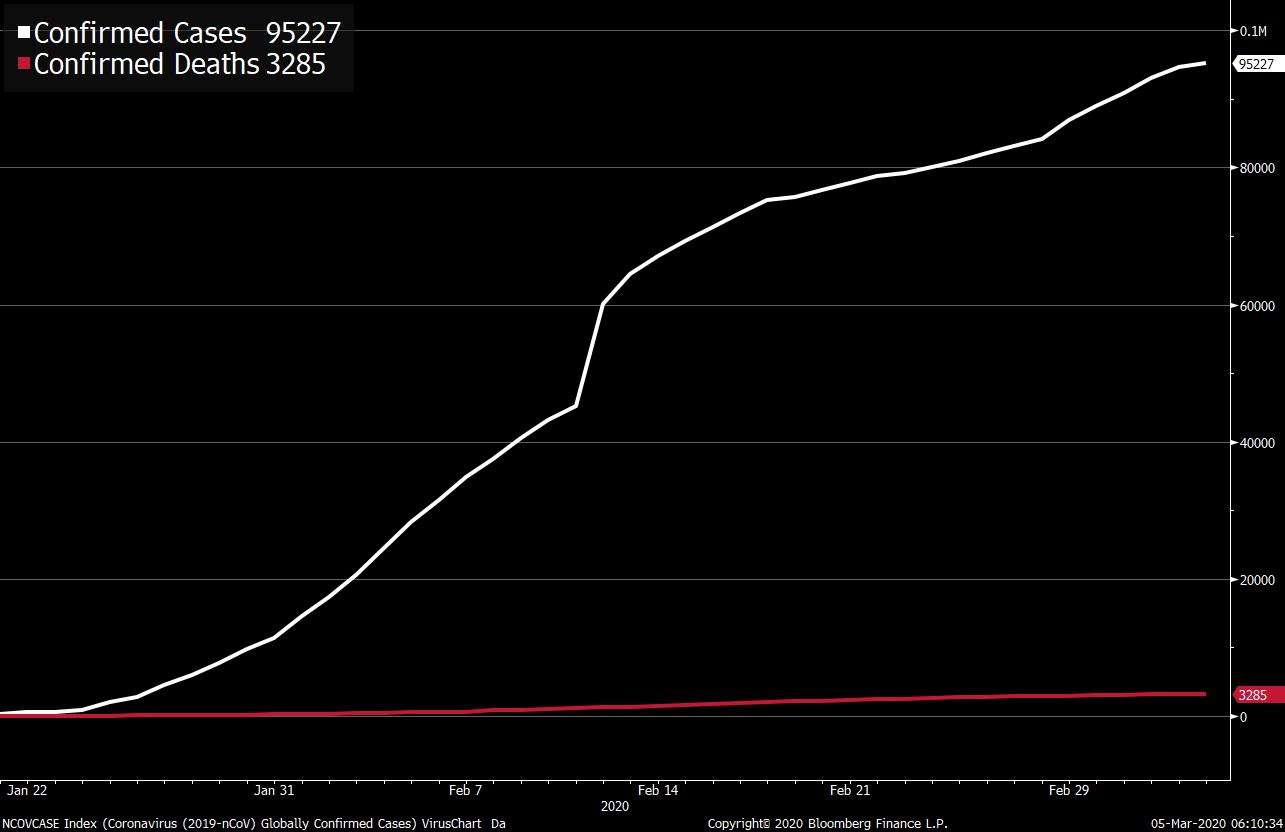

Coronavirus outbreak dominates everything, government spending ramps up, and OPEC ministers agree output cut. ContagionWhile there is some good news in the moderation of fatalities in China, the source of the global coronavirus outbreak, the spread of the illness continues. Switzerland reported its first death from the disease, while the number of cases in Italy and South Korea continues to climb. Restrictions to contain the illness are intensifying, with Italy announcing the closure of all schools and large gatherings of people, and schools in the worst-hit area of Seattle also shutting for 14 days. The list of corporate profit warnings continues to grow while the International Air Transport Association said the outbreak could cost airlines as much as $113 billion. Fiscal responseThe monetary response, while perhaps not as globally coordinated as advertised, saw the Bank of Canada yesterday follow the Federal Reserve with its own 50 basis-point rate cut. Perhaps more important is the arrival of a fiscal response. Governments in Asia have already pledged or are considering $38 billion in new spending to counteract the effects of the outbreak. Yesterday in Washington the House passed a $7.8 billion emergency spending bill to deal with the crisis. In Europe, there has been little beyond the promise of major fiscal measures, despite calls from French Finance Minister Bruno Le Maire for stimulus. High stakesOil ministers gathering in Vienna may be close to bridging the gap between Saudi Arabia and Russia as major oil producing nations seek to deal with the recent huge drop in demand. OPEC ministers have agreed on the 1.5 million barrels a day cut in production, which may still be contingent on Russian agreement at the wider OPEC and its allies meeting tomorrow. In the market, the price of a barrel of crude quickly reversed earlier losses as investors reacted to the news. Rally stumblesYesterday's huge climb into the U.S. close is already coming under pressure. Overnight, the MSCI Asia Pacific Index climbed 1.25% and Japan's Topix index closed 0.9% higher. It is a different story in Europe this morning where the Stoxx 600 Index was 1.2% lower by 5:50 a.m., despite opening higher. S&P 500 futures had dropped by 2%, the 10-year Treasury yield was back under 1% and gold was higher. Coming up…Initial jobless claims at 8:30 a.m. are expected to show a small decrease from last week's number as investors get one last look at the employment market ahead of tomorrow's payrolls number. Factory and durable goods orders for January are at 10:00 a.m. Dallas Fed President Rob Kaplan, New York Fed President John Williams and the Bank of Canada Governor Stephen Poloz all speak later. Costco Wholesale Corp and Kroger Co. are among the companies reporting earnings. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningIt's understandable and logical why the public seeks to avoid bailing out private companies. If a property developer wants to build in some extremely dangerous location (say an area with rising sea levels, or an unstable cliff), then they alone should bear the risk of a disaster. A bailout with public money would not only be unfair, but would create moral hazard, encouraging further dangerous development. With banks things get a little trickier. It's not right for the public to backstop risky financial activities, and yet banks are central to the economy as a whole. Plus they often have public deposits. So the bailout question is more delicate. When it comes to the coronavirus and the fallout, damage will be wrought on a range of industries, just as evidenced by all of the event cancellations which will hit hotels and airlines hard. That will have ripple effects. Depending on how bad things get, bailouts with public money should be part of the official recovery response. The pain from the virus is hard enough, and there's no reason we should let it compound and accelerate by causing liquidations and layoffs, which will then compound into new economic problems. Moral hazard shouldn't be a factor, because unlike building a house on a dangerous cliff or a coast with a rising sea level, participation in society as a whole is not just some choice people make. There are some people who view any attempt by the public to resuscitate the economy in moral terms: Bailouts, stimulus etc. are all bad, and the downturn is the nature of things. But there's nothing positive or edifying about mass, avoidable suffering. There's nothing inherently deserved about it, so when a calamity strikes the entire globe, authorities should do what they can to counteract it economically.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment