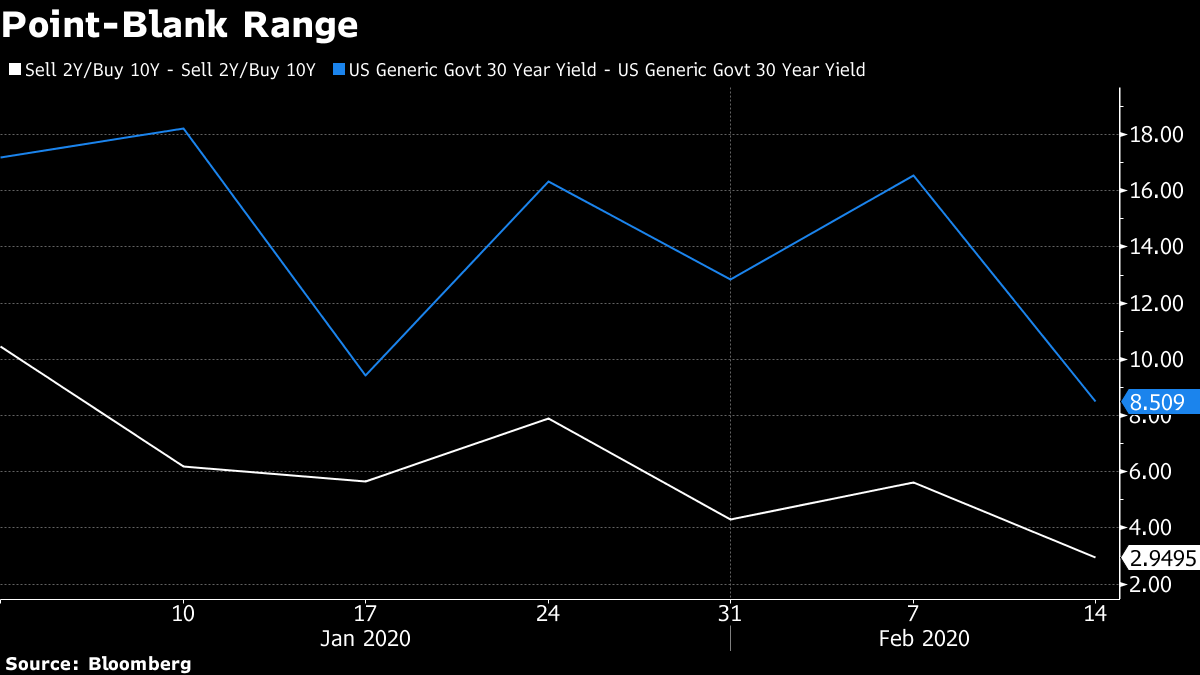

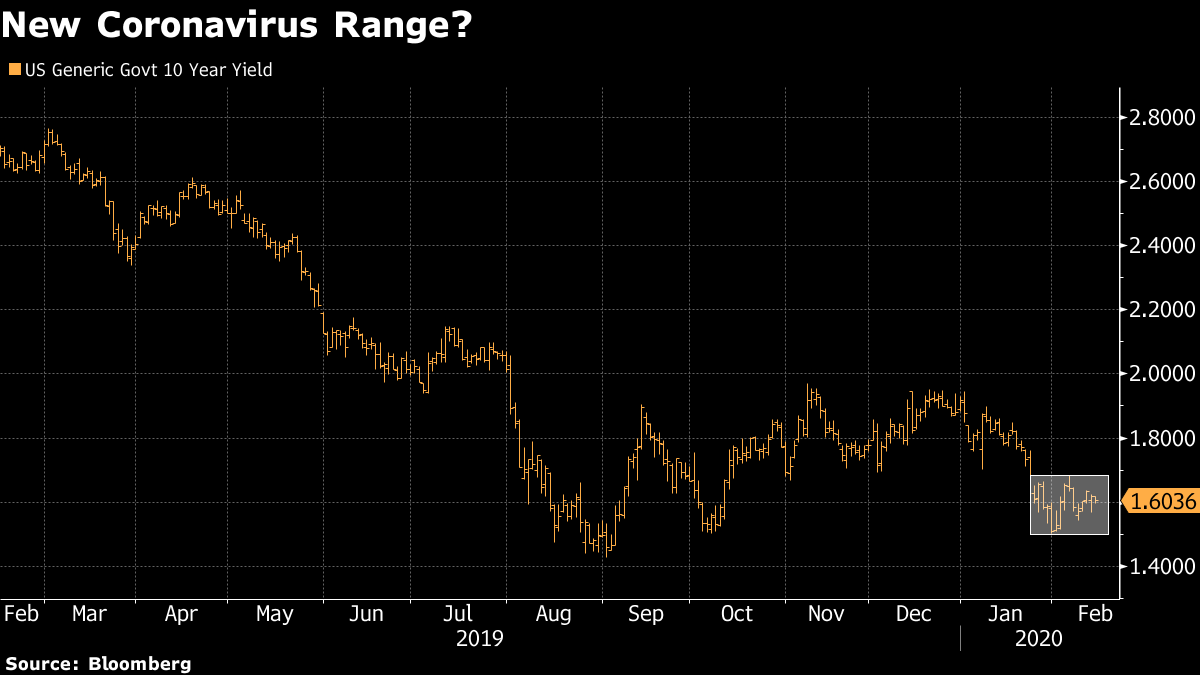

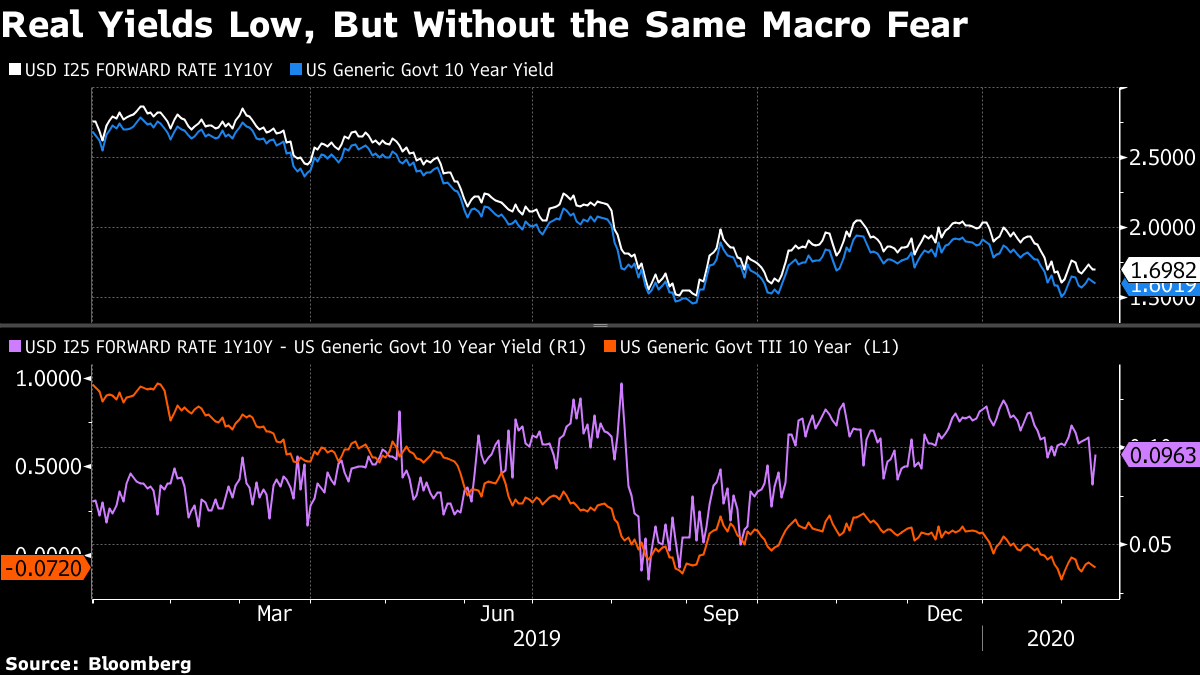

| Welcome to the Weekly Fix, the newsletter marveling at the bipartisan support for an independent Federal Reserve in a world where Congress doesn't agree on anything else. –Luke Kawa, Cross-Asset Reporter. R-R-R-R-Ranges Financial markets are adaptive, by nature, to differing states of nature. Even in an unstable environment – say, one characterized by an ongoing trade war or a virus whose effects on global growth are unknown – markets will usually find a way to go about day-to-day business in a way that doesn't include persistently elevated volatility. There are signs that bonds are settling into their own (unstable) equilibrium while the backdrop of the coronavirus still looms large. In a week in which the U.S. Treasury issued a 30-year bond with the lowest coupon on record, yields on that benchmark have been trading in their smallest weekly range this year. Same story for the two-year, 10-year Treasury curve's weekly range.  Bad news on the spread of the coronavirus (albeit through revisions) sparked a not-too-massive flight to U.S. Treasuries, which was then nearly completely offset by a solid reading of U.S. consumer price inflation and the continued bid for equities. Ten-year Treasury yields were right around 1.6% at the end of Thursday, which is right around the middle of a roughly 20 basis point range defined by the gap lower from the close on Jan. 24 and how it finished the month.  "The lowest yielding long-bond auction in history, at 2.061%, came and went without consequence – a relevant development which double underlines the market's appreciation of the reality that low rates are going nowhere fast," writes Ian Lyngen at BMO Capital Markets. "Even with a solid CPI release to start the decade, the deep-seeded skepticism of upside inflationary risk caps how far yields and term premia can back up." The long end is continuing to signal unease about the future in general, not the near-term outlook in particular. The spread between 10-year yields one year forward and the cash rate continues to stay well above where it was in August.  On the other side of the range, one potential curb on further bullishness for bonds is the the idea that central bankers in developed economies won't necessary be tripping over themselves to ease policy because of the coronavirus. After all, they have little – if any – conventional firepower available, and many of them already moved last year. Such as the Reserve Bank of New Zealand, which this week projected no chance of a rate cut in 2020. "What the RBNZ decision teaches us however is that the bar to do anything on policy – particularly on the easing front – is rather high," writes Mazen Issa at TD Securities. "Most central banks have already hinted that Covid-19 is an emerging and potentially significant risk, but one that probably may not require monetary policy to offset." Despite this, the short-end of the U.S. curve continues to exhibit a great degree of angst. Put-call skew for the two-year note (25-delta put less call implied volatility normalized by at the money) shows one-way traffic looking for lower yields via options. Citigroup has recommended a play that benefits from traders starting to price in a March rate cut, for instance – part of a broader trend of unease about the near-term outlook visible in bets on Eurodollar futures contracts. In addition, the implied volatility of the two-year yield over the next three months remains elevated, despite the asymmetry in the Federal Reserve's potential moves in the short term (tilted towards easing).  All this talk about the nascent calm in Treasuries could be torn asunder by the price action on Friday, however. In the limited history in which the coronavirus is top of mind for market participants, Fridays have seen the largest weekly decline in the 10-year Treasury yield on three out of three occasions. The reasoning is simple: things could always get worse over the weekend, and it's better to be (in) safe (assets) than be sorry. Smooth sailing into the weekend is a necessary, but not sufficient, condition for showing the market has settled into an unstable equilibrium that incorporates a whole lot of uncertainty surrounding the coronavirus. Growth Comes First The coronavirus is indisputably a negative impetus for Chinese growth. But increasingly, it's becoming apparent that it isn't thebiggest threat to the country's debt-fueled boom. If anything it may be an excuse to perpetuate it, as borrowing coststumble. The growth slowdown is going well beyond what stress tests envisaged as a worst-case scenario for Chinese banks. But any downside may well be mitigated thanks to the Chinese leadership's resolve to avoid adverse outcomes on this front. The tolerance for debt may allow for the mitigation of financial risks in the short term, even without a commensurate boost to activity. Anti-epidemic bond issuance is heating up, but lots of that debt is just being refinanced. That means it isn't necessarily adding much to efforts to mitigate the virus's spread or stimulus in general. The virus continues to challenge price discovery, though, with daily turnover on cash bonds slumping to one-third of its 12-month average. |

Post a Comment