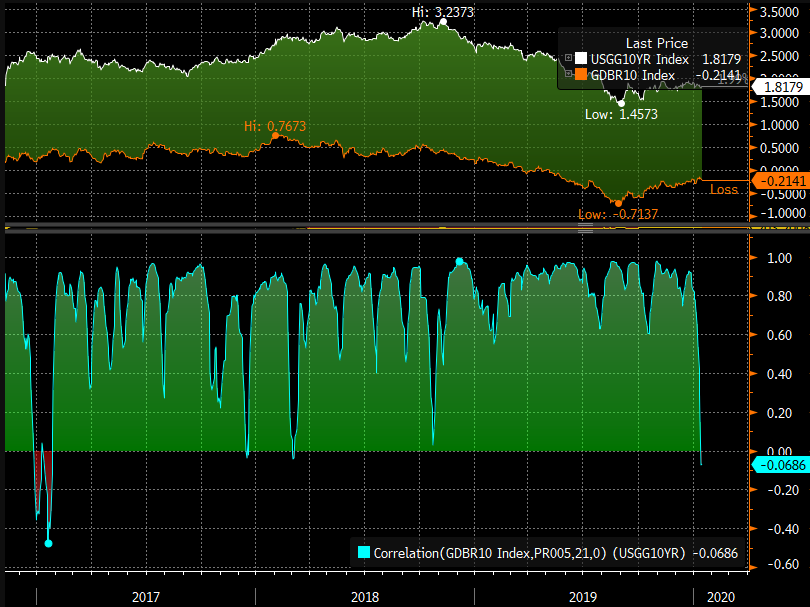

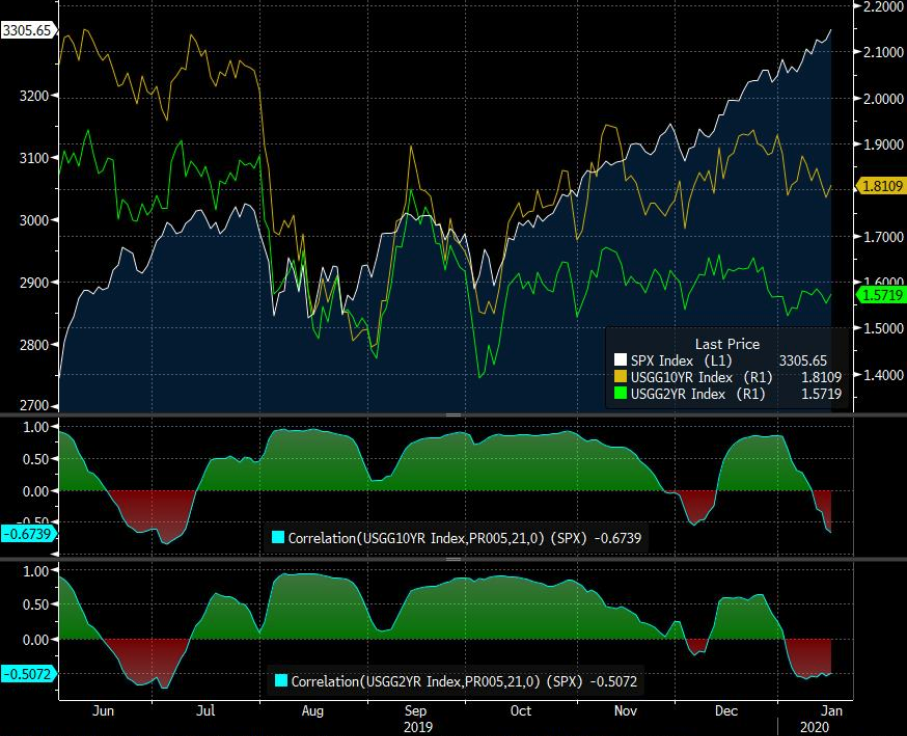

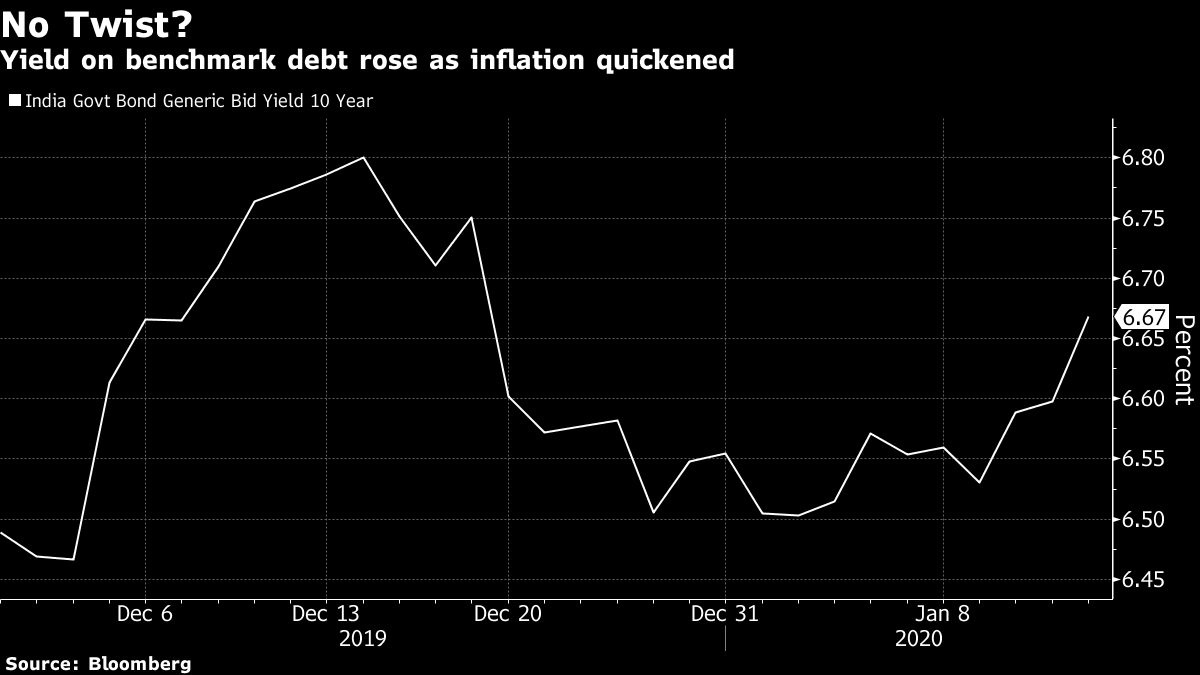

| Welcome to the Weekly Fix, the newsletter that thinks the most interesting thing about the 10-year Treasury yield is how boring it's been for months. –Luke Kawa, Cross-Asset Reporter X-Factor This is not the convergence we were looking for. The yield spread between 10-year Treasuries and German bunds narrowed to less than 200 basis points this week. It was the first such move since U.S. yields tumbled amid the biggest one-day spike in U.S. equity volatility, back in February 2018.  Broadly speaking, the winnowing is a function of German yields falling less than U.S. ones recently. By contrast, the consensus expectation had been that the spread would shrink thanks to a bottoming in global growth driving up overseas interest rates more than their American counterparts. The latest move has coincided with a flattening, rather than a steepening, of the two-year, 10-year Treasury curve since the year began.  Bloomberg Bloomberg Yields have been ticking up this week, but some market participants are wondering why the moves aren't more pronounced, given the backdrop of economic data that continues to exceed expectations in the U.S., euro zone and China. There are some fundamental excuses: U.S. inflation remains contained and the latest American employment data were far from inspiring, with the slower growth in aggregate annual earnings pointing to some downside risks for consumption (though those were alleviated by a robust retail sales report Thursday). Srinivas Thiruvadanthai at the Jerome Levy Forecasting Center flagged that rebalancing from stocks into bonds in passive portfolios as a key spur for bonds, thanks to the outperformance of equities. Certainly, the price action so far this month suggests an element of that was at work. The reasoning comports with an old JPMorgan Chase theory that a key side effect of the strength in the stock market was the prolonging of the decades-old bond rally. Charlie McElligott of Nomura Holdings called for duration-sensitive strategies to do well in stocks and bonds this month as part of a reversal strategy that's worked almost too well. "If past is prologue, the majority of the + returns from the 'one-month price reversal' factor strategy phenomenon in January have already been made over these first few weeks of the new year's turn," he wrote. The strategist insists Treasuries "cannot sell off for all the reasons I have continued repeating." Those include a "Goldilocks economy" with low inflation, an asymmetric Fed attitude towards easing versus hiking rates, and his call that the Fed's current T-bill purchase program will morph into buying Treasuries with coupons. The equity market might need him to have that prediction right, given the changing relationship between stocks and bonds. Ten-year yields have been trendless for the past three months, rangebound between 1.75% and 1.95% for the overwhelming majority of the past three months, with a floor around 1.8% since early December, to boot. The three-month closing range is just a little over 25 basis points. That's the tightest such spread since September 2018 – right before U.S. stocks put in an intermediate top and yields punched through 3% and began to look like they'd keep going and going. "The coiling effect creates kinetic technical tension which is more likely than not to resolve in a range-breaking move at a point in the near future," writes Ian Lyngen, a strategist at BMO Capital Markets. For stocks, recent history suggests the "right way" is lower. The 21-session correlation between the S&P 500 Index and the 10-year and two-year Treasury yields is at its most negative since July. That captures a stretch in which Fed Chairman Jerome Powell pivoted to say the central bank would "act as appropriate" – serving as a conduit for stocks and bonds to rally before an era of "good news is good news" (and vice versa) set in for much of the remainder of 2019.  Bloomberg Bloomberg "It's more factor on/off these days than risk on/off," quipped analyst Josh Demasi on Twitter. Indeed, momentum and growth are back in vogue. Richly valued segments of the market like the tech sector, communication services, and Chinese technology are the most positively correlated with the momentum factor in over a year. The momentum factor, in turn, remains very negatively correlated with bond yields. It's difficult to see the spark for a major repricing of Treasuries or how much higher the short-term ceiling for rates really is. But it's equally tough to guess how much of one would be needed to rattle these massive parts of the market – ones that are punching above their weight in delivering returns so far in 2020. On the other hand, one lesson of September 2019 is that factor rotation need not generate trauma at the index level. Much as a lizard who loses its tail to escape a predator can regenerate the abandoned appendage, so too has the S&P 500 rally proven amazingly adept at shifting to tap into fresh sources of strength when a key pillar falters. Assorted Fed Dallas Fed chief Robert Kaplan doesn't want the Fed's balance sheet to grow too much because he's worried it's contributing to "elevated risk-asset valuations." These remarks from an interview came a day after the New York Fed announced a modest trim to its future repurchase operations. Kaplan referred to the Fed's Treasury purchases as a "derivative of QE," a remark that clashes with Powell's description of its bill-buying as not quantitative easing. As previously observed, this is quantitative normaling, not QE: the Fed's actions are designed to ensure the proper transmission of the current stance of monetary policy, not ease conditions above and beyond that. As for Kaplan's concerns about valuations, it's worth noting that financial conditions have done precisely what the Fed should have expected them to do in light of its rate reductions. The chart below shows the amount of easing implied by the annual change in Goldman Sachs's U.S. financial conditions index almost perfectly matches the move in the federal funds rate over the past 12 months.  Moving on to Judy Shelton, the hard-money advocate turned public uber-dove who has been formally nominated (along with Christopher Waller) to a spot on the Fed's Board of Governors. This newsletter discussed the merits of their candidaciesin July, when Trump tweeted about them.

Sam Bell, the self-styled chief tweeting officer at the Employ America think-tank, on Bloomberg TV Thursday, noted Shelton's shifting ideology throughout the years. Here's an expansive twitter thread he's compiled on her history. And another. And another. Bell was at it again on Thursday evening after news of Shelton's nomination hit the wires following his interview. He argued that she is technically ineligible to serve on the Board, citing the (often loosely interpreted) clause that requires members to come from different districts. Her place of residency (Virginia) is already occupied by Governor Lael Brainard. This technicality was used (as the pretense/justification) to block Nobel Prize-winning economist Peter Diamond's nomination during Barack Obama's presidency. "Will we play by the rules where only monetary doves / fans of the dual mandate get the residency requirement enforced against them?" Bell wondered. "Let's see." |

Post a Comment