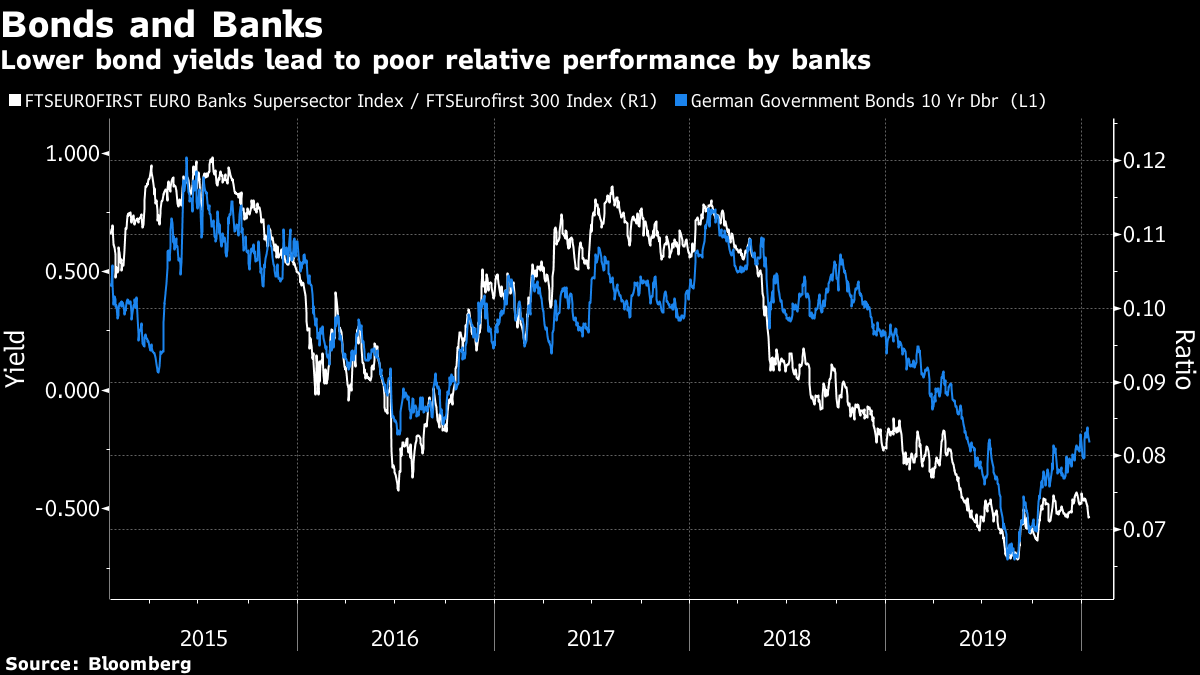

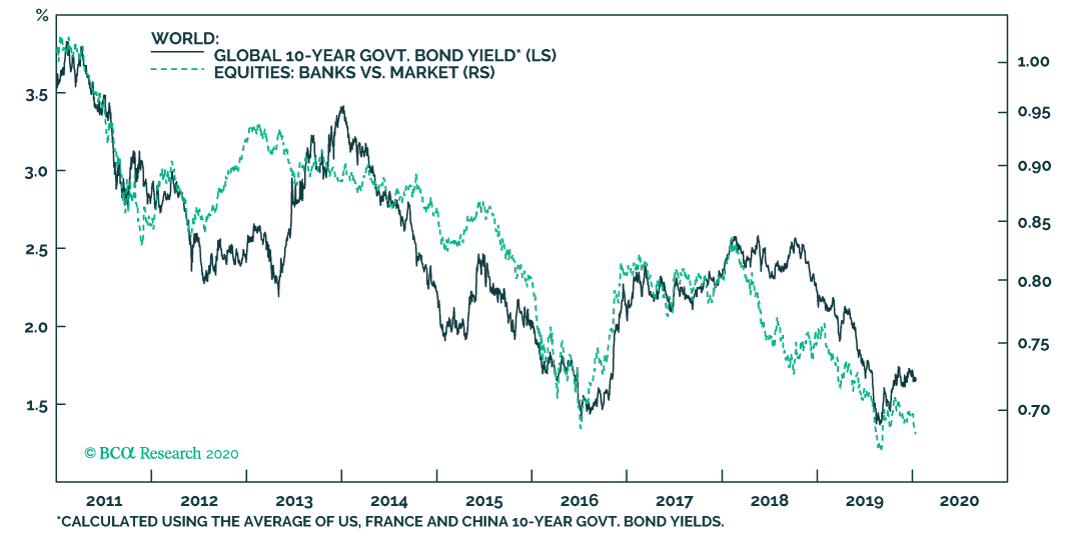

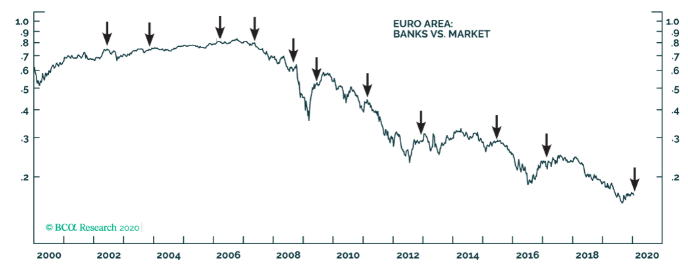

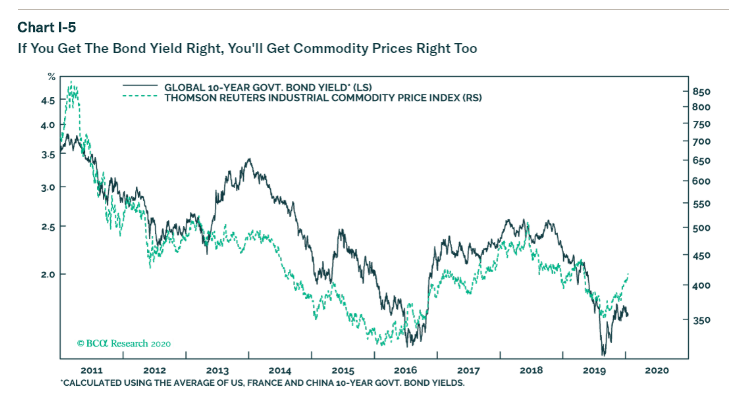

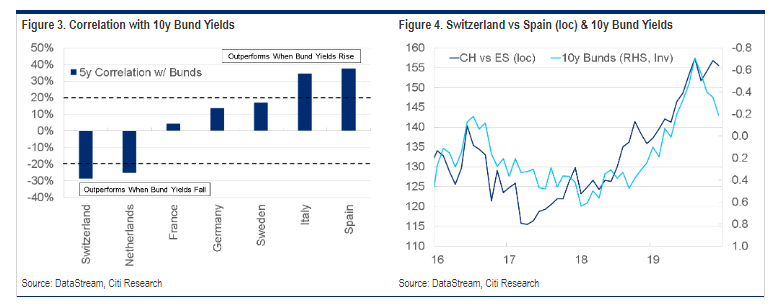

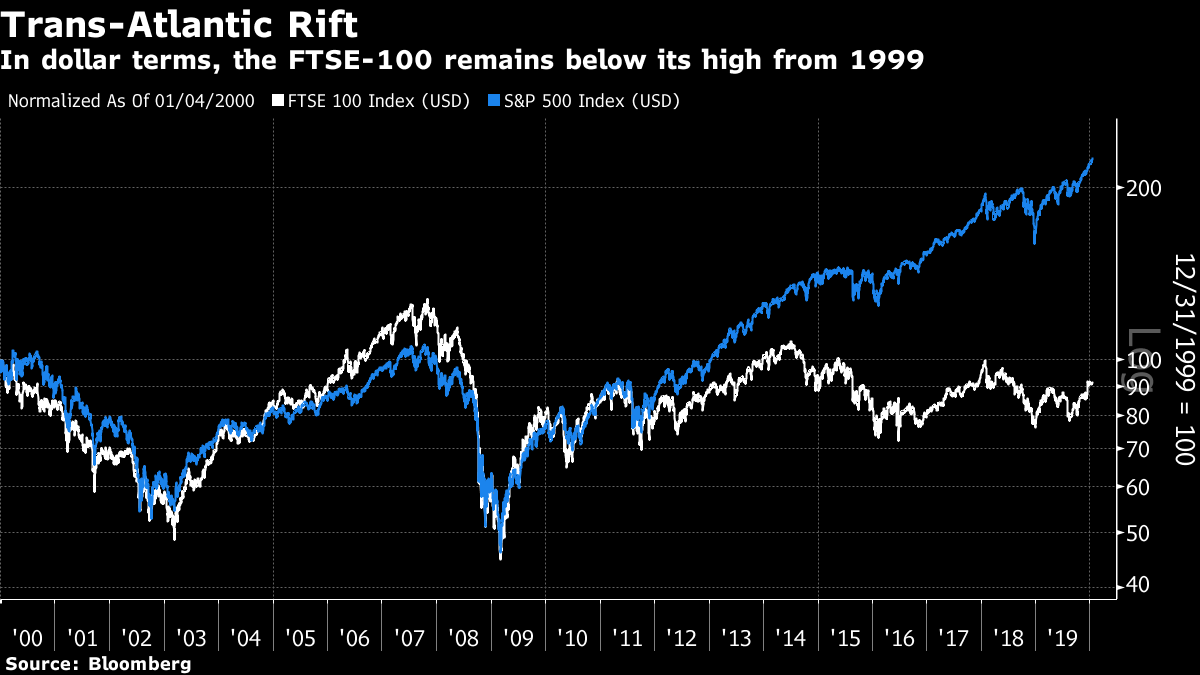

If You Get the Bond Yields Right…. Global finance has a problem child. The European banking system was every bit as complicit in triggering the global financial crisis as its American counterpart (leading some to call the whole disaster the "North Atlantic Financial Crisis"). Its weakness subsequently drove the European Union into the sovereign debt crisis, and the world of negative rates and sluggish growth that has followed. Now, the speed of the rise in bond yields in the last few months, driven by burgeoning optimism that the global economy is ready for a coordinated advance, could be about to force yet another retreat. That at least is the theory of BCA Research Inc.'s chief European investment strategist, Dhaval Joshi, and it makes sense, as banks' profits and share prices are tightly linked to bond yields. The experience of the last five years is clear: When bond yields fall, so do bank stocks:  The relationship between yields and relative bank performance also works at a global level, and in other countries. Joshi produced a "global" yield, based on the U.S., France and China, and tracked it against the global performance of banks:  Why predict a fall in bond yields? The first link in the argument is that it is the impulse that matters most — or in other words, neither the level nor the change in yields, but the change in the speed of the change. When bond yields accelerate upward, that creates a problem. And the six-month bund yield impulse has now topped 100 basis points, as a sharp increase has followed a sharp decrease six months earlier. This is the highest bund impulse in three years, and in all but one of the previous nine times it has reached this level in the last 20 years, a sharp decrease in yields has followed. (The one exception came amid weird conditions at the height of the credit boom in 2006). When the market comes too far too fast, it provokes its own reaction. The 100-basis-point impulses are marked by arrows in this BCA Research chart, which shows that they tend to prefigure problems for banks.  Yet another downturn for European yields would mean yet another headwind for banks — and problems for banks have tended to feed back into problems for the economy. That's because the eurozone, to a much greater extent than the U.S., relies on banking finance. Many of the ECB's attempts to right the eurozone economy over the last decade have revolved around enabling banks to lend more. Eurozone banks have performed so badly for so long now, on the back of valuations that imply deep skepticism about their assets, as the following chart of price-to-book multiples demonstrates, that it is now popular to predict a rebound.  Bond yields also have a strong familial relationship with materials prices (which, like banks, have rallied recently):  On the back of this, European materials stocks also enjoyed a rally last year, although that has already begun to reverse.  The argument for a fall in European yields doesn't rest only on the speed of their recent rise. Expectations are growing that the European Central Bank, now under the leadership of Christine Lagarde, will grow more hawkish over the next year, in response to inflationary pressure. But so far she has kept her cards close to her chest, and a change toward greater monetary stimulus in the form of asset purchases remains quite possible. If the call for yields to fall again is correct, the impact on sectors will directly affect relative geographic performance. Switzerland, home of many large international companies that are perceived as immune to the economic cycle, is least negatively affected by falling yields, while the countries on the eurozone periphery, such as Spain, stand to be hurt. Therefore, Joshi suggests moving money into Switzerland. Robert Buckland, chief global equity strategist for Citigroup Inc., offers this spectacular chart to show how closely the relative performance of Switzerland and Spain follows moves in bond yields:  If yields fall, it also follows that we should expect the U.S. to outperform the eurozone once again, despite widespread hopes to the contrary. Europe has a much higher weighting in both materials and financials than does the U.S. But perhaps the most bearish outlook would be for the U.K., which is widely believed to be on the verge of an interest rate cut from the Bank of England, at the last meeting overseen by Mark Carney as governor later this month. The FTSE-100 has a weighting of 12% in banks (versus 5% for the S&P 500) and 11% for materials (3% for the S&P). Its long-term performance has been dreadful, and long predates the Brexit referendum. Valued in dollars, and in price terms, it is trading about 10% below the level at which it started the century. But if bond yields really take another leg back down, we can expect the underperformance to drag on for longer.  Another Use for a Sharpie The humble Sharpie has had a bad press of late. Last year, a mysterious extra line on a weather map presented in the White House, blatantly drawn with a marker and intended to change the predicted path of a hurricane, prompted widespread derision. But if that was a case of a Sharpie being used to worsen a forecast, they can also be used to improve them. In a new paper called "Forecasts or Nowcasts? What's on the Horizon for the 2020s?," Rob Arnott and Jonathan Treussard of Research Affiliates LLC try to show how we can distinguish which "forecasts" are in fact "nowcasts" (estimates based on the latest real-time or interim data which are meant to try to describe what is happening in the present) that have been projected into the future. When asked to predict the future, they say, a pundit will often say "markets will have to deal with x" where x is an issue "recycled from yesterday." Nowcasting, they say, often fails because markets move on surprises. If a forecast is based on events that are no longer surprising, and fully discounted (or even over-discounted) by markets, then it is at best noise. "At worst, it positions us to be hurt badly if the market-moving surprise dissipates or reverses, and it risks inviting us to chase a trend, rather than taking on informed maverick risk." Forecasts are best if they come with a statistical confidence interval, giving a range of possibilities and avoiding spurious accuracy that leads to over-confidence. They also need to involve information. The best way to deal with a putative forecast, according to Arnott and Treussard, is with Sharpie in hand. Anything that on inspection merely extrapolates the present with information that should already be discounted should be Sharpied. Many readers might prefer to take a Sharpie to Research Affiliates' own forecast for this decade, which includes an expected annual real return of long-dated U.S. Treasuries of -1.6%, while U.S. equities manage a real return of 0.5% (and emerging markets 7.3%). The reasoning, however, is laid out clearly, and cannot be dismissed as nowcasting. The chances are that this forecast won't be exactly correct. But as a basis for allocating assets for the long term, it's a good place to start. A Weekend With Minsky Finally, yet another reminder that our next book club discussion takes place on Thursday, starting at 11 a.m. New York time. Under the microscope will be "John Maynard Keynes" by the late Hyman Minsky, and Robert Barbera's "The Cost of Capitalism," which explains Minsky's ideas and applies them to the contemporary world. You have one more weekend for reading. If short of time, start with the Barbera book, which is an easier read. And if you have difficulty getting hold of it (which I gather some people outside the U.S. have done), head straight for the concluding parts of the Minsky's reinterpretation of Keynes, beginning with chapter 6 on Financial Institutions, Financial Instability and the Pace of Investment. There aren't many Greek letters or equations at this point, and he sets out his idea forcefully.

Barbera will be discussing Minsky's ideas with me and Justin Fox. To follow along, go to TLIV on the terminal. To ask questions or make comments, please send an email to authersnotes@bloomberg.net.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close.

|

Post a Comment