Welcome to the Weekly Fix, the newsletter that dabbles in amateur ornithology in its spare time. –Luke Kawa, Cross-Asset Reporter

The Outfliers

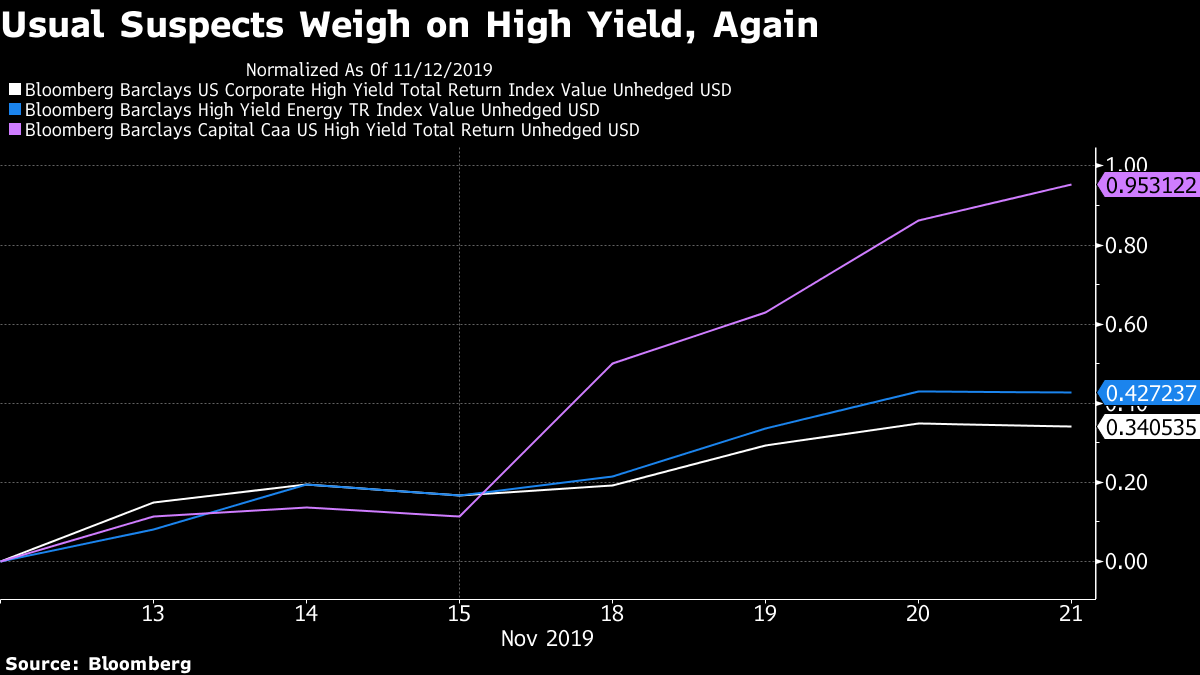

CCCs are once again being highlighted as the poster child for what is about to go wrong across markets. The reason is simple: they're doing poorly, while stocks remain near record highs.

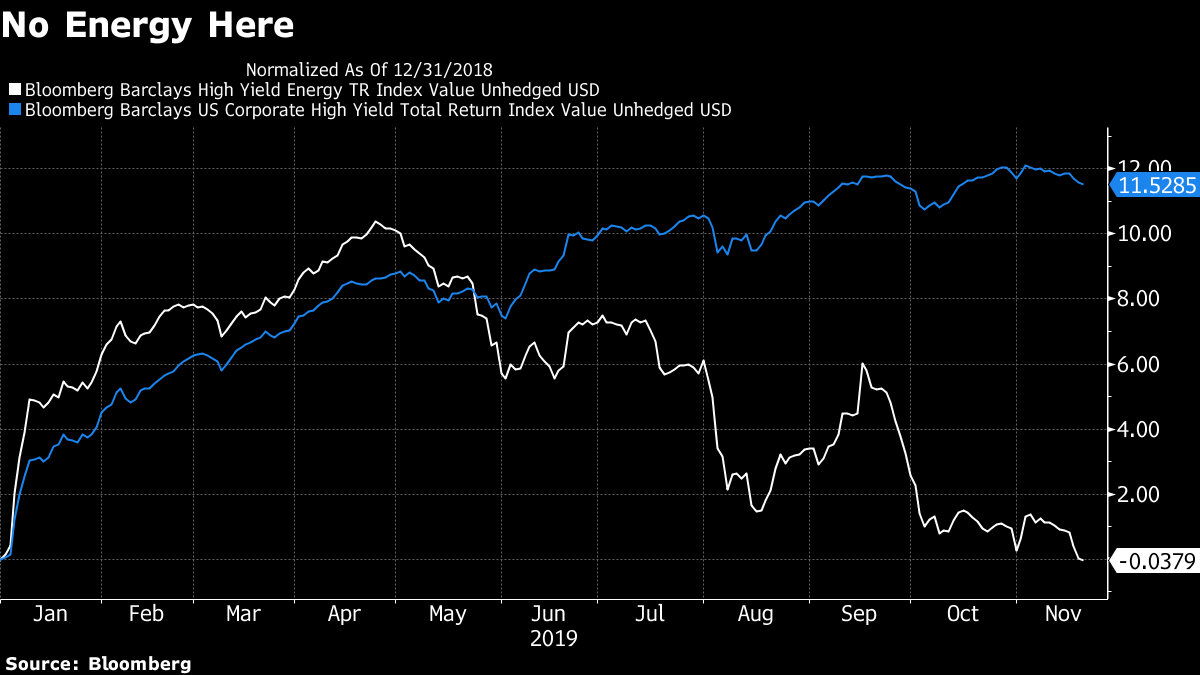

In this newsletter, we've often highlighted why reasoning from price action in CCCs can be a relatively fruitless endeavor. The riskiest junk bonds are a smaller share of the index, and therefore their twists and turns are less representative of high yield as a whole. To boot, the weakness is primarily concentrated in a handful of energy companies and the odd communications firm.

All of these elements are still in play; those are the only two sectors of the high yield space that have underperformed during this vicious bout of CCC widening. Energy junk bonds have posted a negative total return year to date, while the index as a whole is up more than double digits.

In addition, junk bonds in general have been facing heavy supply that has been received well – but the success in the primary market during the busiest week since March 2017 does entail somewhat of a drag on the secondary market.

That isn't stopping some commentators from claiming that the dangers are immense because the spread between CCCs and less risky debt has "never" been this wide. This is patently false unless your definition of "ever" doesn't reach as far back as 2016.

Certainly, it is odd for spreads on CCCs to be diverging so notably both from equities and from other grades of corporate debt.

But what's the signal here, and what's the noise?

The composition of the U.S. economy and stock market are much less weighted towards the types of industries and companies that are suffering in the CCC space; and this area doeslook out-of-place compared to the January and September 2018 peaks in U.S. equities.

The low level of interest rates may be key to this bifurcation: the costs of servicing debt for corporates are (generally) super low. The primary market, both in the U.S. and Europe, has been quite forgiving and willing to give second chances (look at Teva, Mattel, Jaguar, etc). So if a firm can't cut it in this backdrop, it's probably the micro, not the macro, that's at fault.

There is an argument to be made that CCCs are the so-called canary in the coalmine. But it isn't that they're a leading indicator, but that birds (and bonds!) can die if you put them in an unhealthy environment that isn't indicative of the broader ecosystem. We're not expert ornithologists here, but it seems like most birds live the lion's share of their natural lives above the Earth's crust.

Less Fear in This Flattener

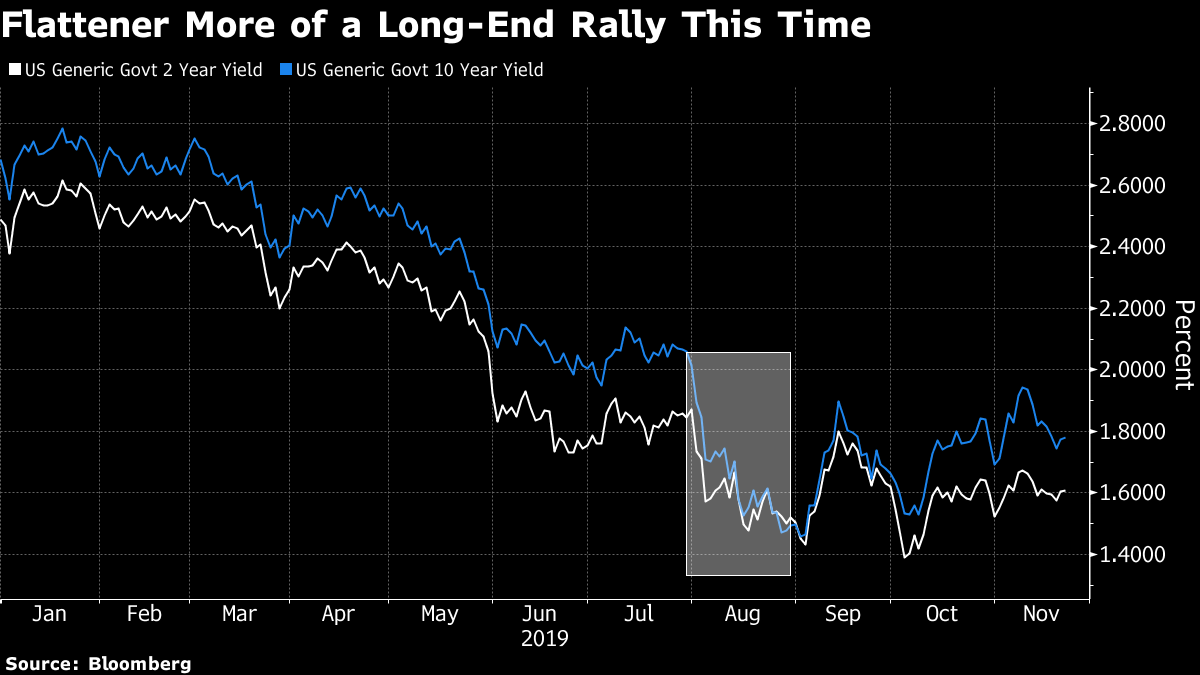

The bond market story of the week – if not the month – is the renewed flattening in the 2s10s Treasury curve. The magnitude of the shrinkage of this spread is the most since August, when the gap turned negative, while the six consecutive sessions of narrowing was the longest since August – of 2018.

It's possible, however, to point to many differences between now and August purely via financial market variables without any mention of how the global economic data or trade talks have transpired (generally, for the better).

Both the two and 10-year yields were falling fairly swiftly in August. That is, conditions were seen as evolving in a materially negative fashion for the global economy so as to lower long term yields precipitously and also boost the degree of monetary accommodation the market was demanding of the Fed.

This is still being viewed, in the market's eyes, as more of a recalibration on the extent of any reflationary impulse for the global economy, and not something that the Federal Reserve will need to react to with easier policy.

Even a Wednesday intraday selloff in risk assets related to jitters that a phase one deal wouldn't go into effect by year end didn't spur a knee-jerk bond reaction that implied the Fed put would soon be activated. What's more, 10-year yields didn't even set a fresh daily low on that news, a sign that the bond rally was running out of steam. Thursday's session brought about an "outside day" – one in which the low yield was lower than the prior day, and the high yield was higher than the last session, too.

"It's notable that since early summer all but one of the yield extremes (both selloffs and rallies) have been marked by outside-days higher in rates," wrote BMO's Ian Lyngen on Thursday. "The simple fact that today was such a formation speaks to the risk that yields have established at least a temporary floor."

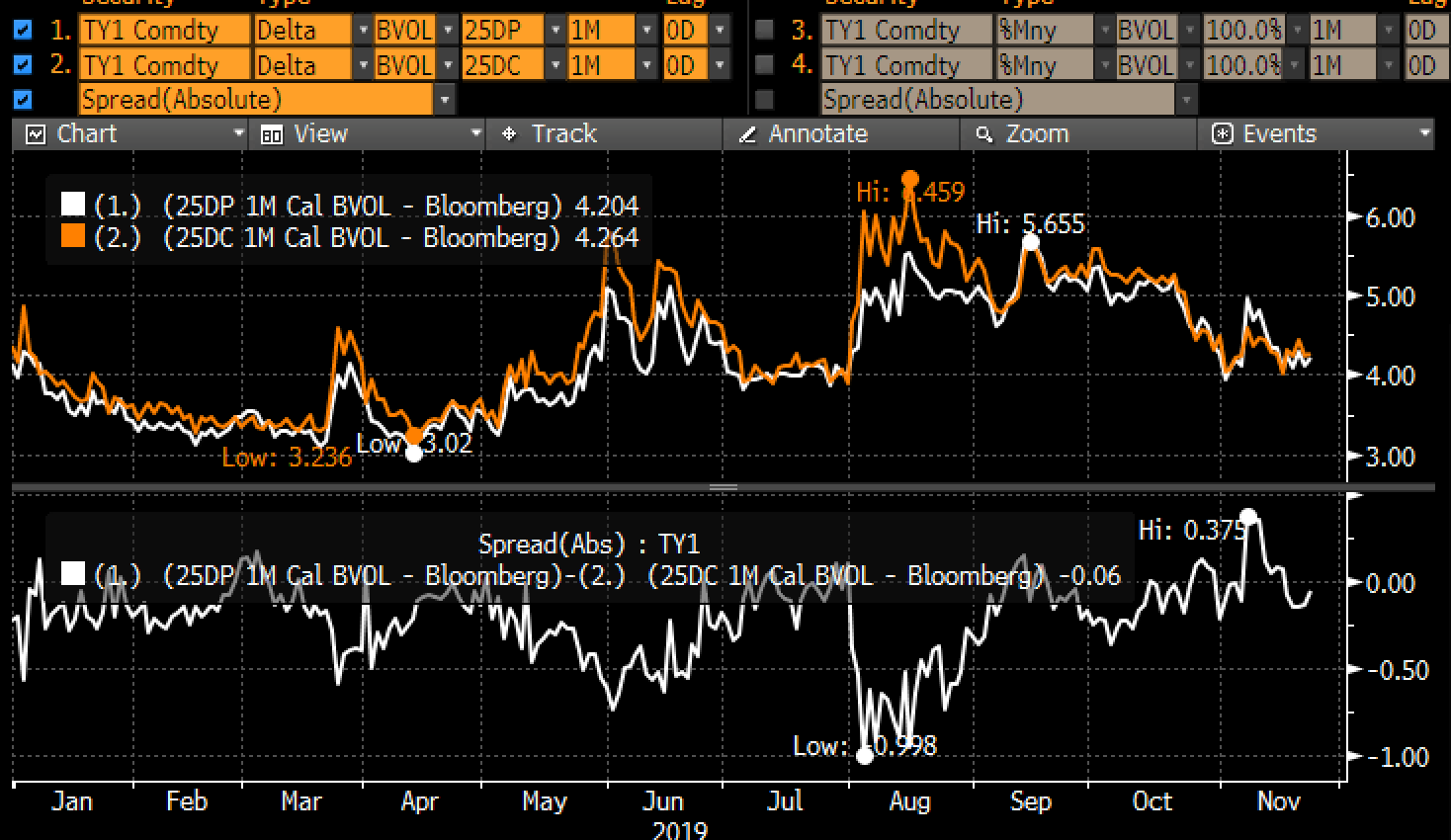

Another this-is-not-August sign can be found in the options market. The bid for calls relative to puts for the 10-year futures note went haywire in early August – an indication that the bond rally was expected to crescendo, which it did – while now, the pricing of bullish to bearish options is much more neutral. On a gross level, the implied volatilities of both puts and calls are much more subdued.

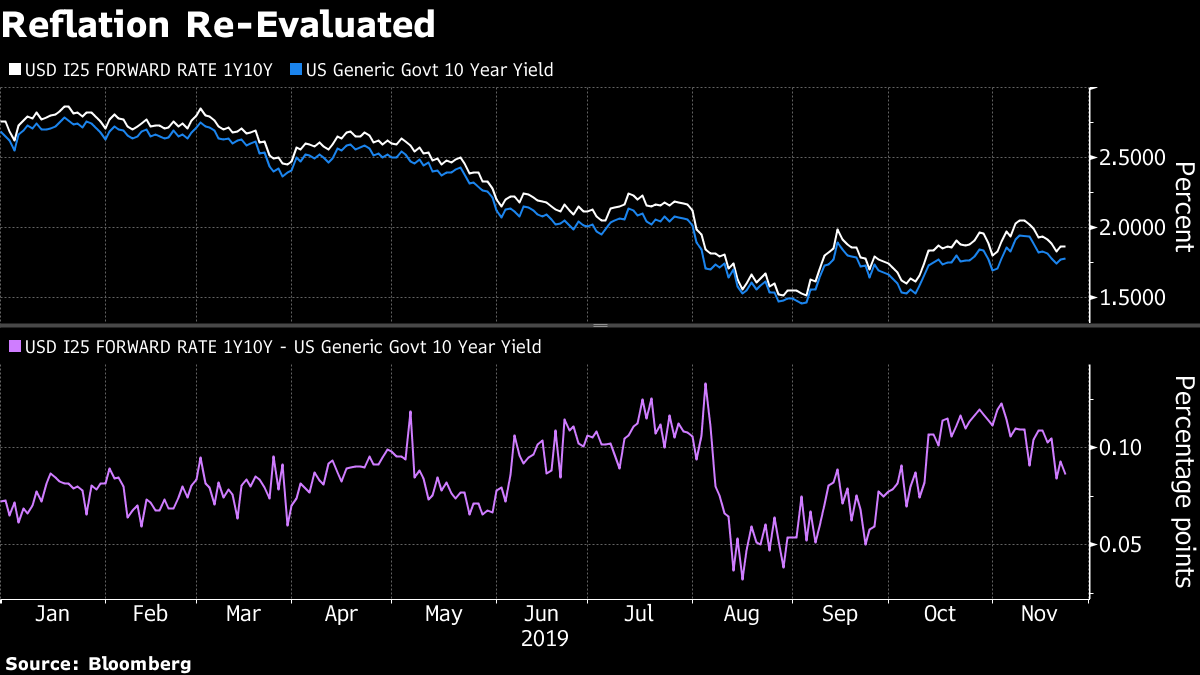

One more: the extent to which the bull-flattening in yields is (or isn't) dashing hopes that the 10-year yield will be able to rise thereafter. During August's flattening spree, the difference between the 10-year yield's one-year forward rate and its current level narrowed from double digits to as low as three basis points. In this episode, it's narrowed half a basis point so far.

Post a Comment