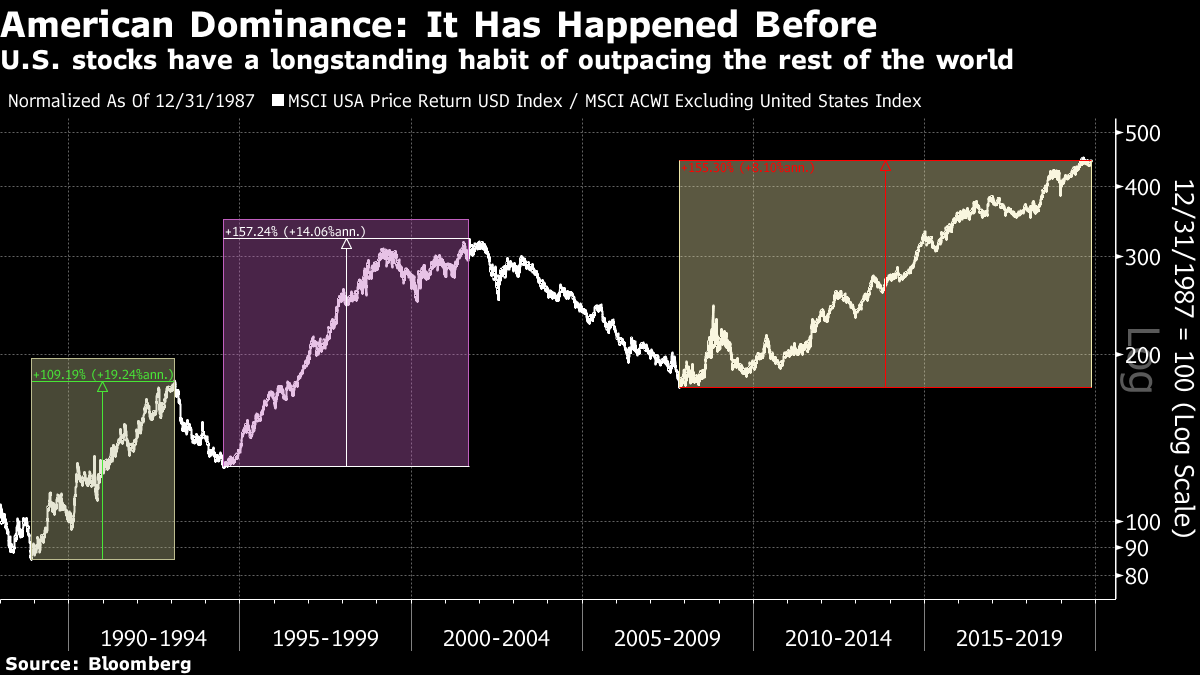

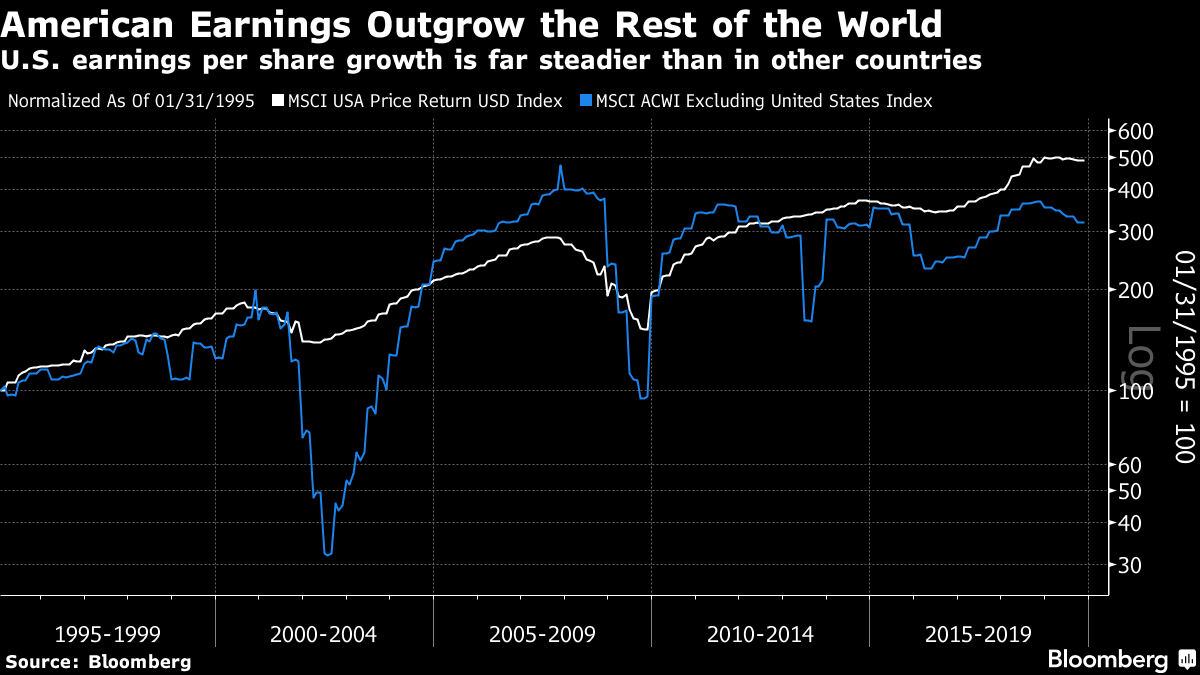

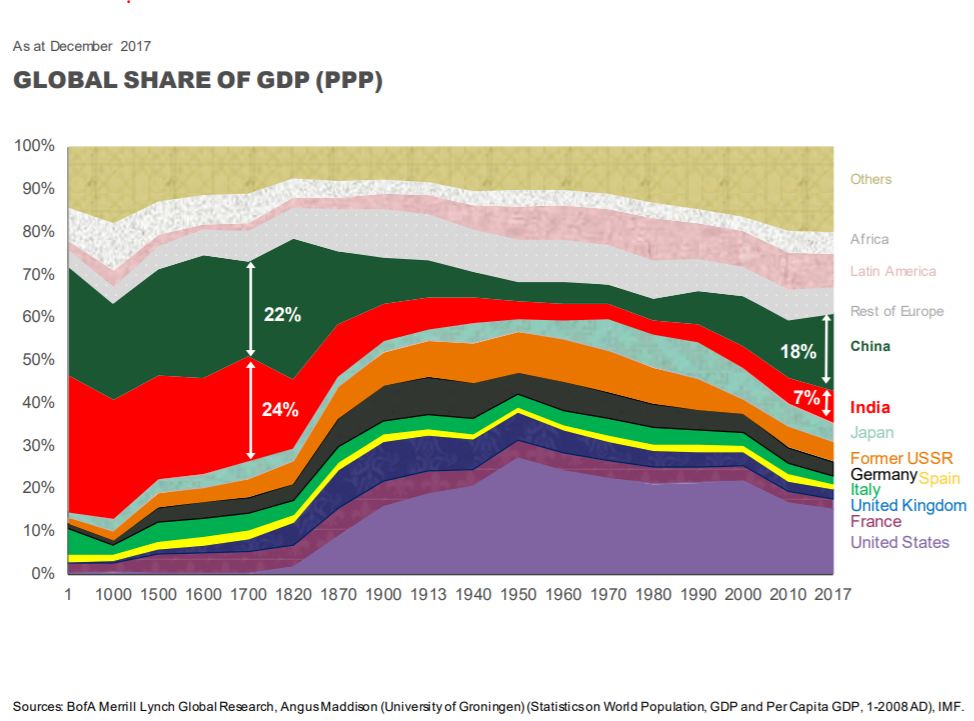

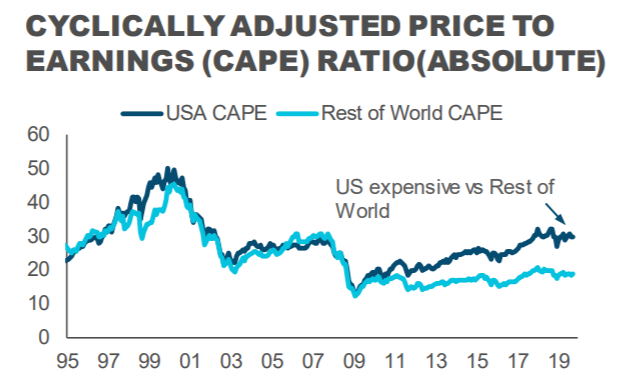

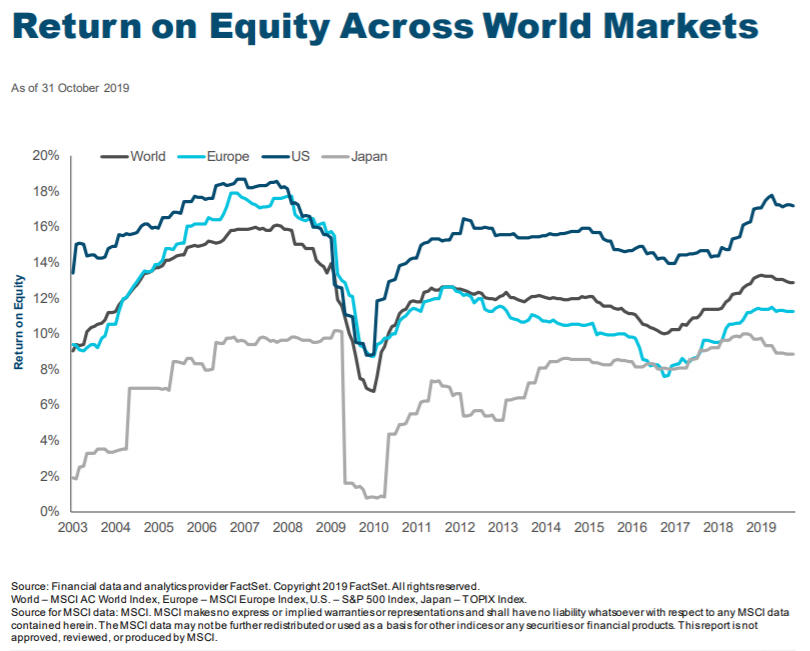

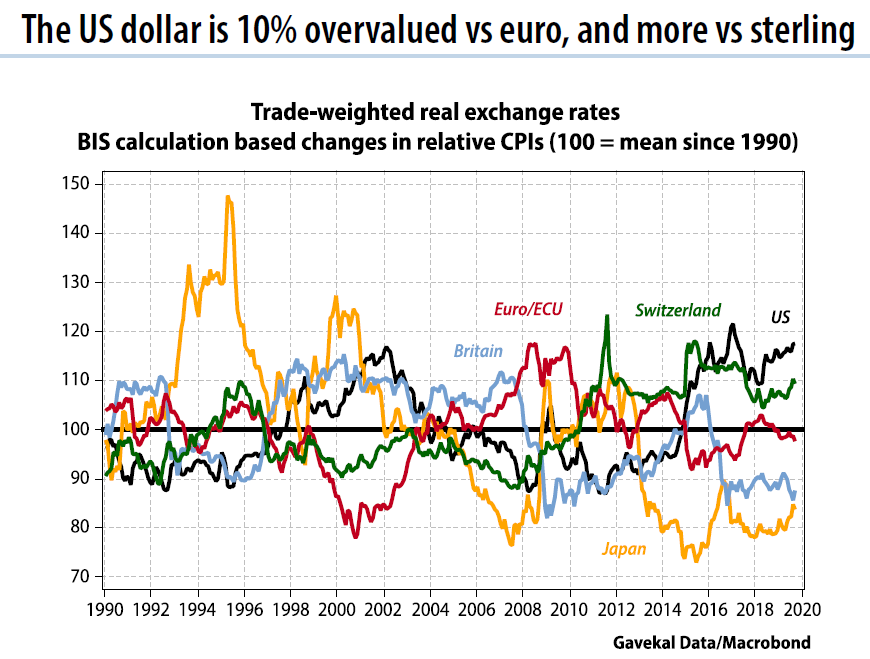

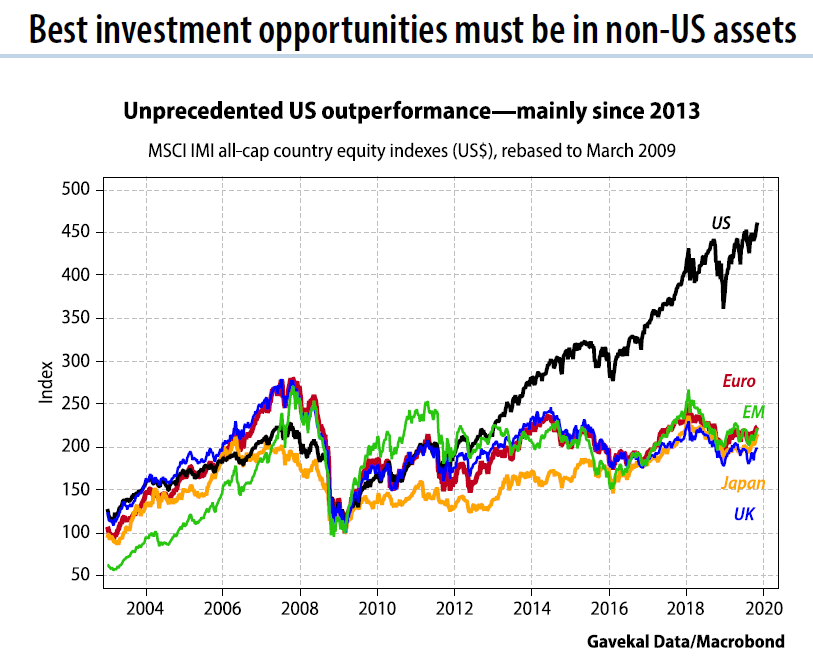

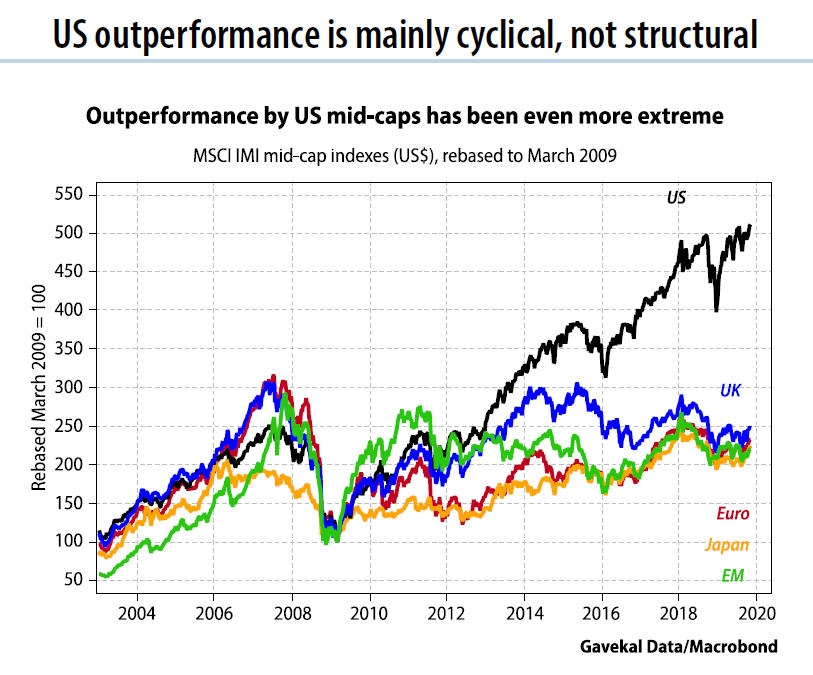

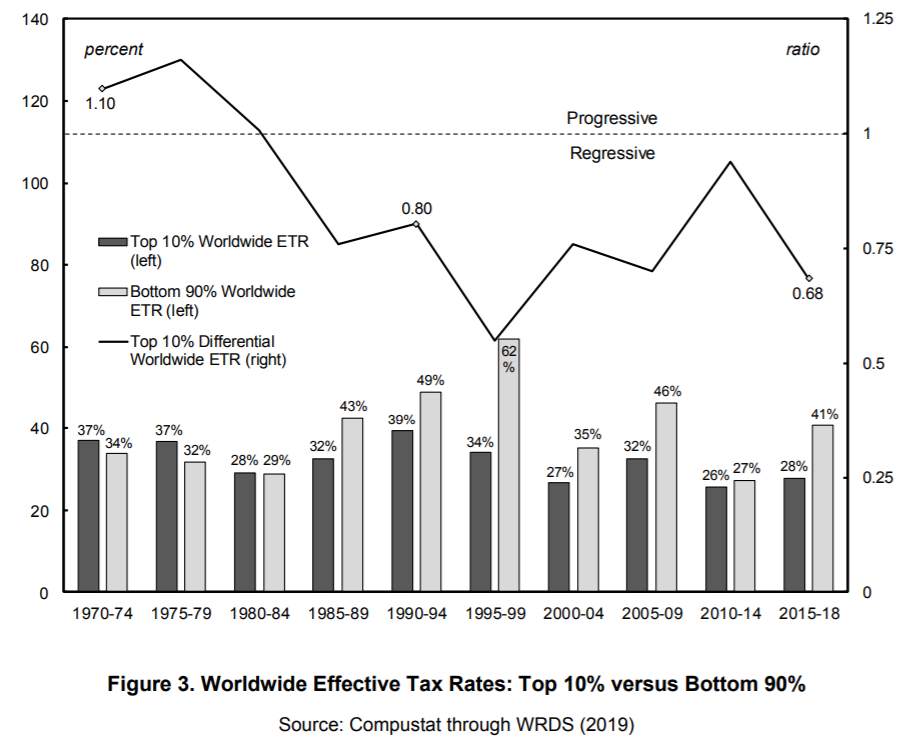

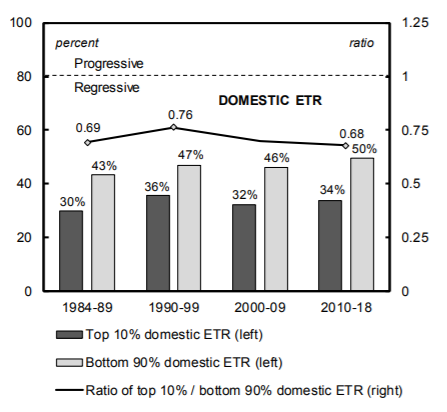

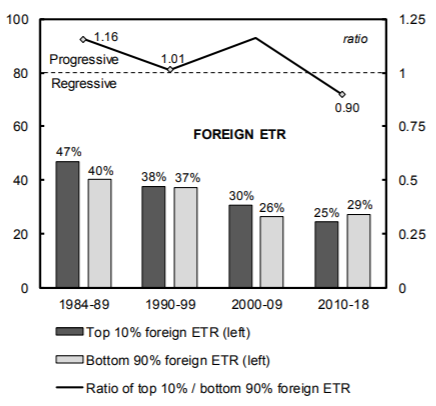

America Second. Could It Happen? Once bitten, twice shy, as George Michael once said, in a song that provided the plot for a movie that I actually enjoyed. Unlike anyone else on the planet. But whatever we think of the song or the movie, Michael's principle was a good one, and it is scalable. Twice bitten, four times shy, and so on. Once you have been bitten as often as I have been by bold predictions that the rest of the world's stock markets will start to outperform the U.S., you get very shy indeed about expressing any such hope. One recurring motif of the prediction season is that prognosticators think the U.S. is ready to widen its lead, so I will review the case. Returns on American stocks have massively outstripped the rest of the planet since the trough of the financial crisis, but that superiority only started, bizarrely, after Standard & Poor's downgraded U.S. sovereign credit in the summer of 2011. At the time it seemed a possible death knell for the country's financial standing. The actuality, at least in terms of stock market performance, has been different:  This dominance is remarkable, and explains why I and others have been keen to bet that the two lines will converge. But protracted ascendancy for the world's largest economy, with its most vibrant technology sector, isn't unprecedented. This shows how the MSCI U.S. index has performed compared to the rest of the world over the last three decades. There have been two similar periods of extended outperformance. Both were followed by a snapback, but the reversal in favor of the rest of the world in the mid-1990s didn't last long before the tech boom took over:  Further, U.S. dominance is at least based on superior and stabler growth in earnings per share. This owes something to better innovation, and a lot to greater willingness to resort to shareholder-friendly financial engineering, but the results are indisputable:  None of this means that we should take U.S. superiority as a given. The following chart, produced by Justin Thomson, chief investment officer for equities at T. Rowe Price, shows how shares of global GDP have changed over the millennia. China and India are growing, and there is every reason to believe that they will continue to outgrow the U.S. Eventually, that should be reflected in superior stock market performance.  Then there is the issue of valuation. Even during the greatest excesses of the dot-com bubble, the U.S. stock market wasn't much more expensive than the rest of the world, if we use cyclically adjusted earnings multiples that compare prices to average profits over the previous 10 years. The outperformance of the last decade, Thomson showed, has been driven by a continuously widening valuation gap.  That gap has also been earned by sharply higher profitability for U.S. companies as reflected by return on equity. 'Twas not ever thus, and it appears unwise to assume that American companies can continue to expand their equity so much faster each year:  But most of these arguments have been valid for years. That is why I have been making them for years, without success. Why should we expect a change this time? Anatole Kaletsky, a former colleague who now heads Gavekal Economics, is prepared to make the case for global outperformance, having also made it incorrectly in the past. To start, there is the dollar, which looks overvalued. If the prevailing extremely low foreign-exchange volatility presages a round of dollar weakness, which seems very possible, then that would be just the catalyst to allow the rest of the world to outperform American assets for a while. The dollar also had a long period of weakness during the last period of U.S. underperformance at the beginning of the last decade:  Then Kaletsky points out that there is almost no differentiation between other geographies. Particularly since 2013, it is as though the only question investors have asked before buying is: Is it American or from somewhere else?  It is popular to attribute U.S. strength to the "FAANG" group of dominant internet companies (a list that generally includes Facebook Inc., Amazon.com Inc., Apple Inc., Netflix Inc. and Google's owner Alphabet Inc., often with a few more added). As these companies disrupt industries and entrench themselves, it is possible to argue that U.S. outperformance is structural — except that it is even more marked at the mid-cap level, which excludes all the internet giants:  This looks like a strong case that the rest of the world will indeed catch up at some point in the next decade. If you needed to buy stocks today to hold for a decade, you should probably make them non-American. But many hanker after perfect timing. Is there any reason why this should happen next year? The best reason to assume it might is called Elizabeth Warren. As I wrote earlier this week, it is remarkable how much the Massachusetts senator's name comes up in conversation, and how scared many investors are of her. But even if she doesn't emerge victorious next year, Kaletsky makes the argument that the balance of political risks is ready to shift across the Atlantic. Europe has avoided a number of political bullets in recent months, largely because populist politicians have overplayed their hand. Italy isn't going to stage a confrontation with Brussels over its budget deficit now that Matteo Salvini, leader of the right-populist League, has removed himself from power. The U.K. isn't going to leave the EU without a deal, as Prime Minister Boris Johnson has been out-thought by his opponents. And populist pressure in a number of countries has abated. Meanwhile, in the U.S. there are all the signs of a coming political mess. Warren might just provide the catalyst for a correction that has been coming for a while. She might be the "someone special" to whom we should give our hearts this year. From Antitrust to Tax Reform There's more to uncompetitive industries and over-concentration than inadequate antitrust enforcement. Aggressive moves to block anti-competitive mergers, or split up dominant companies, might certainly help, but many other policies also contribute to the problem. One of them is tax. This is central to the argument of The Myth of Capitalism, by Jonathan Tepper and Denise Hearn, which we will be discussing on the terminal in two weeks. The Bloomberg book club selection is a polemical attack on how lack of competition has stopped capitalism from working. Tax policy is part of the problem. Tepper pointed me to this paper by Sandy Brian Hager of City University of London and Joseph Baines of King's College, London. The nub of their argument, which should be read in full, is that the largest companies have negotiated preferential tax treatment for themselves, which has further entrenched their dominance. At a global level, this is how the effective tax rates paid by the top 10% of companies and everyone else have varied since 1970. Big companies pay less tax.  This issue might even illuminate the puzzling dominance of American companies. Here is the same exercise, since 1984, for U.S. companies only. This combines both federal and state taxes, and the pattern is clear — the biggest 10% pay far less. And to be clear, the issue long predates Donald Trump:  Here is the same exercise for the rest of the world. Tax rates have come down over time, and smaller companies now pay significantly lower effective tax rates than their U.S. equivalents. But the huge gap in tax rates between the biggest companies and the rest just doesn't exist:  For more reading on this subject, try this great collation of evidence from the Tax Justice Network. And please send all comments and questions for Tepper and his co-author to: authersnotes@bloomberg.net. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment